Posted on 15th April, 2026 (GMT 12:31 hrs)

ABSTRACT

India’s insolvency regime, culminating in the Insolvency and Bankruptcy Code (IBC, 2016), represents not a rupture but a refinement of a long-standing political economy that protects and reproduces elite accumulation. While the pre-2014 framework (BIFR/SICA/DRT/SARFAESI) enabled overt promoter impunity through delay and fragmentation, the post-2016 IBC has professionalised and sanitised this asymmetry into a time-bound, creditor-driven architecture that systematically socialises losses and privatises gains. Empirical trends—~8,800+ CIRP admissions, ~31–33% recovery rates, ~67% average haircuts, ₹4+ lakh crore realised against far larger claims, and a surge in wilful defaulters to ₹3.83 lakh crore by 2025—reveal a system where public-sector banks, workers, SMEs, and retail investors absorb the bulk of distress while politically connected acquirers consolidate assets at deep discounts, often through phoenixing and procedural arbitrage. Landmark cases like Dewan Housing Finance Corporation Ltd illustrate how legal doctrines (e.g., Section 32A clean slate vs. Section 66 fraud recovery) enable the transfer of both assets and upside from fraud to new owners under the doctrine of CoC “commercial wisdom.” Far from disciplining capital, the IBC normalises strategic default as a rational, even aspirational pathway within India’s crony-capitalist order—an evolution from chaotic promoter protection to a streamlined mechanism of wealth transfer, embedded within a broader regime of opaque political funding, selective enforcement, and taxpayer-backed recapitalisation.

I. Introduction: From Mess to Cunning Capitalist Phoenixing Technique

India’s insolvency and bankruptcy framework is not merely a legal or economic story — it is a damning political-economic and moral indictment of the BJP-NDA regime that has ruled since 2014. What was once a fragmented, notoriously inefficient, debtor-friendly mess has been repackaged under the Insolvency and Bankruptcy Code (IBC), 2016, into a sleek, ostensibly “creditor-driven” and “time-bound” machine.

On paper, it promises value maximisation, entrepreneurship, and credit discipline. In reality, it has functioned as one of the most refined wealth-transfer mechanisms in post-liberalisation India: public-sector banks and common taxpayers swallow enormous haircuts, operational creditors and retail depositors are systematically crushed, workers lose livelihoods, and a tiny superrich cronies, wilful defaulters, politically connected acquirers, and opportunistic turncoats — emerge richer, often acquiring the very assets they helped destroy through “phoenixing,” proxies, and favourable Committee of Creditors (CoC) decisions.

Phoenixing (or phoenix activity) refers to a business, which is failing or insolvent, being shut down to avoid paying debts (including taxes, employee entitlements, and suppliers). The company’s assets are then transferred to a new company (the “phoenix”), which often has the same owners and operates the same business, “rising from the ashes” of the old one.

This critique integrates the full historical trajectory, wilful defaulter trends, high-profile cases such as DHFL/Piramal and the Anil Ambani Group, official IBBI data as of late 2025–early 2026, and the cultural-moral superstructure that structurally normalises strategic default to benefit the superrich. At its core lies a deliberate rupture: the unfiltered, self-reflexive confession of a higher-middle-class financial bourgeois who embodies the aspirational rot the system has violently institutionalised.

II. The Pre-IBC Era (1968–2014): A Debtor’s Paradise of Chronic Inefficiency and Promoter Protection

For nearly five decades, India’s insolvency and corporate distress resolution regime stood as a textbook case of regulatory capture by industrial promoters and a systemic bias toward debtors. The framework was deliberately fragmented, overlapping, and notoriously debtor-friendly, spread across multiple statutes and forums that often worked at cross-purposes. Key pieces included:

- Winding-up provisions under the Companies Act, 1956 (later 2013),

- The Sick Industrial Companies (Special Provisions) Act, 1985 (SICA), administered by the Board for Industrial and Financial Reconstruction (BIFR) (operational from May 1987),

- The Recovery of Debts Due to Banks and Financial Institutions Act, 1993 (RDDBFI / DRT Act),

- And the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (SARFAESI)⤡,

This multi-layered architecture created a perfect storm of delays, appeals, and protective moratoriums. Promoters could easily retain management control while assets depreciated, funds were diverted, and enterprise value evaporated. Formal “bankruptcy” or winding-up proceedings were rare not because distress was uncommon, but because the system actively discouraged creditors from pushing companies into resolution. Instead, it incentivised endless litigation, negotiations behind closed doors, and political or bureaucratic interventions that prolonged the agony of public-sector banks and other creditors.

A. Quantitative Portrait of Systemic Failure: The BIFR Record

The performance of the BIFR, the centrepiece of the SICA regime, reveals the depth of inefficiency. From its inception in 1987 until its eventual abolition under the IBC in 2016, the Board received thousands of sickness references. Estimates vary slightly by source and cut-off date, but the broad picture is consistent and damning:

- By March 2007, the BIFR had registered approximately 5,471 references of potentially sick industrial companies.

- Of these, only around 825 cases resulted in sanctioned rehabilitation schemes — a revival success rate of roughly 15%.

- Another 1,337 cases (about 24%) were recommended for winding up, though actual execution of winding-up orders through High Courts was far lower due to further appeals and delays.

- By the early 2010s (up to around 2014), cumulative references hovered near or above 5,800, with revival schemes sanctioned in only about 14–15% of cases (roughly 825–850 successful schemes overall).

Many references were dismissed as non-maintainable, abated due to prolonged pendency, or simply dragged on without resolution. In later years, disposal rates remained abysmal — for instance, the Board disposed of just 169 cases between 2010 and 2013 amid mounting backlogs. Average resolution timelines stretched from 4 to 15+ years, with many cases lingering for over a decade due to multi-layered appeals (including to the Appellate Authority for Industrial and Financial Reconstruction — AAIFR), High Court interventions, and bureaucratic inertia.

Recovery rates for creditors were correspondingly poor. Overall creditor recoveries under the pre-IBC regime typically languished between 5% and 26% of admitted claims. BIFR-sanctioned revival schemes often yielded as low as 5–15% for banks and financial institutions. Parallel mechanisms fared no better in practice:

- Recoveries under SARFAESI and DRT proceedings frequently fell into single digits or low teens, despite the theoretical empowerment of secured creditors.

- The World Bank’s Doing Business Report consistently ranked India near the bottom globally on the “Resolving Insolvency” indicator. In the 2014–15 report, India stood at 136th out of 189 economies, with an average resolution time of about 4.3 years, a cost of 9% of the debtor’s estate, and a recovery rate of only 25.7 cents on the dollar for secured creditors (with piecemeal sale as the most likely outcome).

These figures underscore a regime that systematically destroyed rather than preserved enterprise value. Public-sector banks, which bore the brunt of lending to large industrial houses, absorbed massive losses that were ultimately socialised through repeated government recapitalisation. The public exchequer and, by extension, ordinary taxpayers subsidised promoter mismanagement on an enormous scale.

B. Promoter Impunity and the Culture of Moral Hazard

Beyond raw statistics lay a deeper structural and cultural problem: near-total promoter protection. Once a company was declared “sick” under SICA and referred to the BIFR, an automatic moratorium kicked in that shielded promoters from aggressive creditor action. Promoters routinely continued in management, engaging in:

- Asset-stripping,

- Diversion of funds through related-party transactions,

- Evergreening of loans, and

- Other forms of financial engineering.

Punishment for such practices was rare and ineffective. Wilful defaulters — a category formalised later by the RBI — existed in nascent but significant form even then. By March 2014, just before the IBC era began, there were already 5,076 wilful defaulters owing approximately ₹39,369 crore. The system allowed them to delay, dilute liabilities, and often escape with minimal personal consequences.

This was not accidental inefficiency but a predictable outcome of regulatory design. The BIFR process prioritised “revival at any cost” and protection of employment over creditor rights or commercial viability. Creditors (especially public banks) had limited say in the process, while promoters exploited the forum-shopping opportunities created by overlapping jurisdictions (BIFR, DRTs, High Courts, and SARFAESI). The result was a classic case of moral hazard: promoters enjoyed the upside of risky or fraudulent decisions while downside risks were borne by banks, depositors, and the state.

Critical reflection reveals how this regime entrenched a particular political economy. Large industrial houses, often with deep political and bureaucratic connections, benefited disproportionately. Small and medium enterprises (SMEs) and operational creditors rarely received meaningful relief. The pre-IBC system thus functioned less as an insolvency framework and more as a promoter welfare mechanism disguised as industrial policy — one that eroded credit discipline, discouraged responsible lending, and contributed to the build-up of the “twin balance sheet” crisis that became visible by 2014–15.

This was the inherited baseline when the BJP-NDA government assumed power in 2014: a chronically inefficient, value-destructive apparatus that protected the “superrich wilful defaulter” class in its early stages while imposing heavy costs on the banking system and the broader economy. Far from a clean slate, the IBC would later repackage and modernise many of these underlying power asymmetries under the rhetoric of “creditor-friendliness” and “time-bound resolution.”

III. The Transitional Crisis Year (2014–15): Exposure of Systemic Collapse and the Push for “Reform”

The year 2014–15 marked a decisive inflection point in India’s banking and corporate distress landscape — the moment when the accumulated inefficiencies and moral hazards of the pre-IBC era could no longer be concealed. It represented the peak manifestation of the much-discussed “twin balance-sheet problem” (TBS): over-leveraged corporates on one side, burdened with unsustainable debt, and severely stressed public-sector banks (PSBs) on the other, saddled with mounting non-performing assets (NPAs) that threatened the stability of the entire financial system.

By March 2014, gross NPAs of scheduled commercial banks had already reached alarming levels. For public sector banks, the gross NPA ratio stood around 4.5–5.1% of gross advances, with absolute gross NPAs exceeding ₹2.16 lakh crore (and climbing rapidly). Private sector banks fared somewhat better, but the burden was overwhelmingly concentrated in PSBs, which accounted for the lion’s share of lending to infrastructure, power, steel, and other capital-intensive sectors that had turned sour amid the post-2010 economic slowdown, policy paralysis in the final years of the UPA government, and aggressive lending during the earlier boom years.

Promoters and corporates had benefited from prolonged regulatory forbearance, repeated loan restructuring, and “evergreening” — the practice of extending fresh loans to service old ones, thereby masking true asset quality. This created a deceptive calm on bank balance sheets while the underlying rot festered. BIFR references ticked up only modestly to roughly 90–175 cases in this period, reflecting not a decline in distress but the terminal decline of the old regime itself. Many troubled companies avoided formal sickness declarations or dragged proceedings indefinitely, knowing the system would shield them through delays and appeals.

The real exposure came in 2015–16 with the Reserve Bank of India’s landmark Asset Quality Review (AQR), initiated under then-Governor Raghuram Rajan. Launched in mid-2015 and intensified through late 2015–early 2016, the AQR was a rigorous, account-by-account scrutiny of large borrower exposures. It forced banks to abandon forbearance and properly classify stressed assets according to prudential norms. The results were explosive: reported gross NPAs of PSBs surged dramatically. From around 5.1% in September 2015, the system-wide gross NPA ratio jumped to 7.6% by March 2016 and continued climbing toward double digits in subsequent years (peaking near 11.5% later). Absolute NPAs crossed ₹7–8 lakh crore in the broader banking system by 2017, with PSBs bearing over 80–85% of the burden.

Recoveries under the inherited mechanisms remained abysmal, hovering between 15–25% of admitted claims in practice. SARFAESI actions and DRT proceedings yielded limited relief, often eroded further by protracted litigation. The World Bank’s Doing Business rankings continued to reflect India’s poor standing on insolvency resolution, underscoring how the old fragmented system destroyed enterprise value rather than preserving it.

This crisis unfolded in the first year of the newly elected BJP-NDA government. The visible collapse of corporate and bank balance sheets provided both a compelling diagnosis of inherited failures and a powerful political-economic justification for sweeping “reform.” In August 2014, the Ministry of Finance constituted the Bankruptcy Law Reforms Committee (BLRC) under T.K. Viswanathan. The Committee submitted its interim recommendations in February 2015 and the final report with a draft bill in November 2015. Its diagnosis was sharp: the existing patchwork of laws (SICA/BIFR, DRT, SARFAESI, Companies Act) suffered from overlapping jurisdictions, excessive delays, debtor-in-possession models, and weak creditor rights. The proposed solution was a unified, time-bound, creditor-driven Insolvency and Bankruptcy Code (IBC) that would shift control to creditors upon default, introduce professional insolvency resolution, and aim for value maximisation within strict timelines.

Proponents hailed the IBC — eventually enacted in May 2016 and effective from December 2016 — as a paradigm shift: from a debtor-friendly, inefficiency-ridden regime to a modern, creditor-friendly, market-oriented framework that would restore credit discipline, improve ease of doing business, and unlock stalled assets. The narrative framed 2014–15 as the necessary catharsis that justified radical change.

However, viewed with the benefit of hindsight, the period of 2014–15 can be interpreted differently—as a pivotal moment when an inefficient promoter-protection racket was not dismantled but rather modernised and sanitised into a more sophisticated instrument of super-rich capture. The delays and value destruction inherent in the old system were real and indefensible. Yet the transition did not fundamentally alter the underlying power asymmetries; instead, it repackaged them in the language of “creditor primacy,” “time-bound resolution,” and “value maximisation.” Public-sector banks continued to bear disproportionate losses through substantial haircuts, while politically connected or well-advised promoters and acquirers gained access to distressed assets at bargain prices under the new mechanism. The AQR exposed the rot accumulated under previous dispensations, but the subsequent resolution architecture increasingly channelled these losses toward socialisation—through repeated bank recapitalisations exceeding ₹3 lakh crore in the years that followed—while privatising upside gains for a narrow set of actors.

In essence, 2014–15 was less a clean break from the past and more a sophisticated re-engineering of it. The “twin balance-sheet” crisis provided the political cover and urgency needed to push through legislation that, on paper, addressed long-standing inefficiencies but, in practice, institutionalised new forms of selective advantage within a seemingly neutral, market-driven process. The IBC did not emerge in a vacuum; it was born directly from — and designed to manage — the very crisis that the pre-2014 promoter-friendly regime had incubated. What changed was the packaging: from overt, messy protectionism to a streamlined, professionalised system that continued to transfer wealth from public banks and taxpayers to connected private interests, albeit with better optics and improved global rankings.

This transitional year thus set the stage for the post-IBC era, where the rhetoric of reform would coexist with persistent patterns of crony capture, modest overall recoveries, and the normalisation of strategic default among those best positioned to navigate the new rules.

IV. The Post-IBC Era (2016–2026): “Creditor-Friendly” in Name, Superrich-Friendly in Practice

The Insolvency and Bankruptcy Code (IBC), 2016, promised a clean break from the past: a unified, time-bound, creditor-driven Corporate Insolvency Resolution Process (CIRP) that would shift control from defaulting promoters to creditors, maximise enterprise value, restore credit discipline, and improve India’s global ranking on ease of resolving insolvency. On paper, it replaced the fragmented, debtor-in-possession model with a market-oriented, professionalised framework featuring strict timelines (ideally 330 days), Committee of Creditors (CoC) decision-making, and insolvency professionals as facilitators.

In practice, the IBC delivered a massive initial surge in formal filings followed by highly selective benefits that disproportionately favoured the well-connected and those able to navigate the new architecture. Rather than dismantling the old promoter-protection culture, it modernised and professionalised it through veils of opacity— turning chronic inefficiency into a streamlined mechanism for wealth transfer and concentration of assets to the common detriment. Public-sector banks continued to absorb large haircuts in the face of rampant disinvestment/privatization drives by the BJP-NDA regime, common retail depositors were routinely marginalised, workers often lost dues and livelihoods with limited safeguards, and a narrow section of wilful defaulters, politically networked acquirers (cronies), and opportunistic restructurers frequently emerged enriched, sometimes acquiring the very assets they had helped erode.

A. Surge, Moderation, and the “Deterrence Effect”

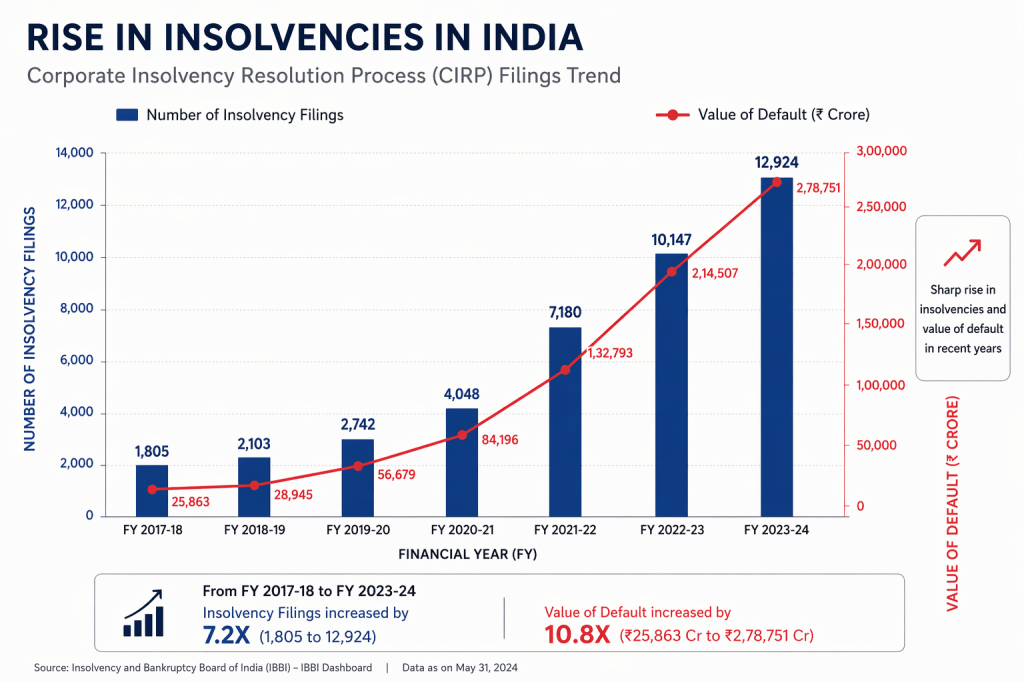

Cumulative CIRP admissions reached 8,833 by December 2025 (with earlier figures showing 8,492 as of June 2025 and around 8,659 by September 2025). Annual admissions peaked at 1,990 in FY 2019–20 before moderating sharply — a trend officially celebrated as a “deterrence effect” and improved credit culture. Quarterly filings dropped to low triple digits in 2024–25, falling to just 140 cases in Oct-Dec 2024.

This moderation reveals an asymmetric reality. The threat of IBC admission has scared many smaller borrowers and operational creditors into early out-of-court settlements or withdrawals. Over 30,000 cases (involving underlying defaults estimated at ₹13–14 lakh crore, with some reports citing ₹13.93 lakh crore up to March 2025) have been resolved through pre-admission settlements or Section 12A withdrawals. While touted as a success, it masks how the framework disproportionately pressures SMEs, trade creditors, and weaker stakeholders to concede on unfavourable terms, while larger promoters and sophisticated players often restructure more advantageously through proxies, family trusts, or well-timed settlements.

B. Key Outcomes and Persistent Imbalances (as of late 2025–early 2026)

According to IBBI and related data up to December 2025, only around 15% of total admissions (roughly 1,300+ resolution plans approved cumulatively by September 2025, with figures around 1,258–1,300 depending on exact cut-off) were rescued via approved resolution plans, while 2,824+ cases were referred to liquidation (with thousands fully liquidated). Average timelines remained chronically delayed at around 688–713 days for resolved cases — both routinely breaching the 330-day statutory target due to NCLT backlogs, frequent appeals, and protracted CoC negotiations.

Recovery metrics paint a sobering picture. Approved resolution plans yielded an average of 170%+ of liquidation value and ~94% of fair value, but overall realisation against admitted claims stood at ~31.6–32.8% (financial creditors ~31–35%, operational creditors significantly worse at 11–25.4%). In fully liquidated cases, recoveries were often as low as 3–6% of admitted claims. Cumulative recoveries through resolution plans reached approximately ₹4.1 lakh crore by December 2025 (with some reports citing ₹4.29 lakh crore till March 2025 in earlier data points).

India’s “improved” ranking on the World Bank’s “Resolving Insolvency” parameter contributed to better Ease of Doing Business scores. Yet this cosmetic progress masks deep and alarming structural failures. The Parliamentary Standing Committee on Finance, in its 28th Report (tabled December 2025), expressed serious concern over persistently high haircuts and weak asset valuation practices, noting that creditors realised only an average of ~32.8% of admitted claims — translating into an average haircut of ~67%.

Even the Finance Minister acknowledged in parliamentary replies that while the IBC had facilitated recoveries of around ₹3.58–4.11 lakh crore, the average haircut remained steep — often in the range of 67–68% (with some quarterly dips as low as 20% in Q3 FY2026 in certain large cases). The Standing Committee flagged the lack of transparency in valuation, frequent distress sales, and the tendency to favour connected acquirers.

The IBC (Amendment) Act of 2025–2026, which introduced stricter admission timelines (mandatory 14-day NCLT decision), expanded CoC powers, tightened withdrawal norms (requiring 90% CoC approval), and allowed greater flexibility in competitive bidding, was projected as a major reform. In practice, these changes — along with the full 2026 overhaul introducing Creditor-Initiated Insolvency Resolution Process (CIIRP), group insolvency, and cross-border enhancements — continue to disproportionately favour the crony superrich by further empowering the CoC (often dominated by public banks under implicit pressures) without robust safeguards against phoenixing or circumvention of Section 29A through family trusts and layered structures.

Worse, the Code suffers from a profound internal incoherence: while Section 66 explicitly targets fraudulent and wrongful trading and is meant to generate recoveries for the benefit of all creditors, Section 32A grants the successful resolution applicant (SRA) a sweeping clean slate, frequently allowing the acquirer to pocket the upside of such avoidance and fraud recoveries. This built-in contradiction — acknowledging systemic fraud on one hand while legally laundering its proceeds to the new owner on the other — ensures that even when wrongdoing is exposed, the real gains flow not to defrauded creditors or taxpayers, but to the politically networked buyer. The Parliamentary Standing Committee recommended global outreach for competitive bidding because domestic processes were delivering excessive haircuts even for viable firms, yet the final amendments fell short of addressing undervalued auctions and insider advantages.

Chronic NCLT backlogs persist, with 20,000–30,000 insolvency applications pending as of early 2026. Parliamentary discussions have repeatedly highlighted that small loans constitute less than 15% of total write-offs/haircuts, while the bulk benefits large corporate accounts. These official admissions reveal a telling paradox: while the government touts improved rankings and falling NPAs (~2.2–2.5% by 2025), the system continues to socialise massive losses (₹8 lakh crore+ estimated through haircuts) onto taxpayers, while enabling a narrow corporate section to acquire empires at bargain prices. The 2025–2026 amendments, far from correcting this imbalance, appear to institutionalise it further by prioritising speed and CoC “commercial wisdom” over transparency and equitable stakeholder protection — refining the mechanism that allows the superrich to “fail upwards” while the 98% bear the cost.

Comparative Data Table

| Period | Legal Framework | Approx. Annual Cases | Avg. Time Taken | Recovery Rate (% of Admitted Claims) | Key Outcomes (by late 2025) | Critique under BJP-NDA Regime |

|---|---|---|---|---|---|---|

| 1968–2014 | Fragmented (BIFR/SICA, DRT, SARFAESI) | 150–250 (~5,800 cumulative) | 4–15+ years | 5–26% | ~15% revival; promoter control preserved | Value destruction & promoter impunity as inherited norm |

| 2014–15 | Old regime collapsing | 90–175 | 4+ years | 15–25% | Legacy delays; twin balance-sheet exposure | Crisis used to legitimise transition to new framework |

| 2016–2025/26 | IBC (CIRP + liquidation) | Peak 1,990 (FY20); later moderated to ~657–724 in FY25 | 688–713+ days (frequent breaches) | ~31.6–32.8% overall; 170%+ of liquidation value | ~8,833 admissions by Dec 2025; ~1,300 resolution plans; 2,824+ liquidations; 30,000+ pre-admission settlements; ₹4.1 lakh crore+ realised via plans | Haircuts institutionalised (~67–68%); crony acquirers thrive via CoC majorities, phoenixing & selective enforcement. Moderation in filings deters the weak more than the powerful. |

C. The Wilful Defaulter Explosion: The Lifeblood of the IBC Machine

Far from curbing wilful default, the IBC has effectively absorbed and normalised its consequences — turning what should have been a deterrent into a sophisticated laundering mechanism for elite predation. Wilful defaulters — borrowers who, despite having repayment capacity, deliberately divert or siphon funds, indulge in fraud, or default — surged dramatically under the post-2014 dispensation. Official RBI data show the numbers rose from 5,076 wilful defaulters owing ₹39,369 crore in March 2014 to 18,318 cases involving ₹3.83 lakh crore by March 2025 — a nearly ten-fold explosion in the quantum of public money looted.

This explosion became the lifeblood of the IBC machinery. Many large wilful defaulter accounts entered CIRP, where haircuts of 67–69% on admitted claims and overall recoveries averaging only 32–33% became not just normalised, but celebrated as “commercial wisdom” of the CoC. The top 10 wilful defaulters alone accounted for over ₹40,635 crore as of March 2025, with prominent cases including ABG Shipyard (₹6,695 crore), Gitanjali Gems (₹6,236 crore), and entities linked to the Wadhawan brothers and the Anil Ambani Group.

In the regime’s favourite piece of Orwellian doublespeak, these staggering sums are routinely “written off” from bank balance sheets — a euphemism that masks the cold reality of loans effectively waived off at the expense of taxpayers and depositors. Since 2014, Indian banks have written off over ₹16.6 lakh crore in NPAs, with public sector banks alone shouldering more than ₹12 lakh crore. These write-offs sanitise the books, artificially lower reported NPAs, and allow the system to claim “clean-up success” while the perpetrators face no meaningful personal liability.

The crowning indictment? Many of the biggest wilful defaulters and fugitive economic offenders — Vijay Mallya, Nirav Modi, Mehul Choksi, and dozens of others owing tens of thousands of crores — continue to live freely abroad, jet-setting, litigating extradition delays, and enjoying luxurious exile while Indian agencies chase shadows. No serious confiscation of their overseas assets, no swift extradition, no exemplary punishment. They wrangle on without capture, their empires partially reborn through proxies or fresh ventures, while the IBC pipeline funnels fresh distressed assets to connected acquirers at fire-sale prices.

The IBC achieved what the fragmented pre-2016 regime could not: it converted messy, prolonged defaults into a predictable, professionally mediated pipeline for distressed-asset transactions. Public-sector banks absorbed the heaviest hits through these massive haircuts, later partially offset by government recapitalisation running into several lakh crore. Connected acquirers positioned themselves to buy empires at deeply discounted valuations. The sharp moderation in fresh filings is routinely cited as improved credit discipline, yet this “deterrence” is brutally asymmetric — it crushes smaller borrowers and operational creditors into early, unfavourable settlements, while sophisticated players with the right networks, lawyers, and political alignment continue to navigate or outright exploit the system with impunity.

The persistence of such a vast wilful defaulter pool a decade after the IBC’s enactment — even as headline NPA ratios declined — lays bare the troubling continuity. Nothing fundamental changed in the behaviour of crony borrowers. What changed was the packaging: from overt, chaotic promoter protection under BIFR to a sleek, IBC-enabled transfer of public resources into private hands. Wilful default has become a functional, almost respectable feature of India’s post-2016 distressed-asset economy — feeding the IBC machine, justifying endless taxpayer-funded bank clean-ups, and enabling new empires to rise from the ruins of older ones.

It is precisely this reality — the spectacle of looted billions quietly written off, fugitives lounging abroad untouched, and politically networked acquirers thriving — that makes strategic bankruptcy not merely viable, but intoxicatingly aspirational. This is the bridge to the unfiltered voice from within: the higher-middle-class financial bourgeois who watches the masters of the game and dreams of joining their ranks.

But statistics alone cannot capture the moral and cultural reality of the system. To understand how deeply the IBC has normalised crony capitalist predation, one must confront the unfiltered confession of those who aspire to master it.

Rupture: The Voice from Within — The Aspirational Dream of Strategic Bankruptcy

By K., Higher-Middle-Class Financial Bourgeois, Mumbai

Namaste. Om Namah Shivaya.

I am K. Forty-seven years old. Chartered Accountant by qualification, “wealth strategist” by profession, and a resident of a respectable 3-BHK in Bandra West whose balcony offers a partial view of the sea-link — a constant, mocking reminder of movement and escape that I can observe but never truly possess.

Every morning at 5:30 a.m., after my bath, I perform my Sandhya Vandana and Gayatri Mantra jaap with mechanical precision, as if the repetition itself could manufacture absolution. I fast on every Ekadashi. I donate to the local Hanuman temple every Tuesday. My family participates in all major pujas — Satyanarayan on full moon nights, Diwali Lakshmi Puja with silver coins, Navratri with proper Devi homa. My wife and I have completed the Char Dham Yatra twice. I never miss the annual Shraddha for my ancestors.

On paper, these rituals anchor me. In truth, they have become a ritualised anaesthesia — a scripted performance I stage for an audience of one, to quiet the persistent, low-grade scream inside my chest that something fundamental is hollow. I chant “Dharma protects those who protect their own,” yet every syllable feels like a transaction: payment rendered to the gods so that the market might smile upon me tomorrow.

My guru, Swami Radhanath Sadhbapu in his Lonavala ashram, smiles benevolently and whispers, “Beta, wealth is also a form of Shakti. In Kali Yuga, bending a few rules for the greater good of one’s bloodline is not sin but survival.” I nod. I pay. I leave lighter — yet the weight inside only grows heavier, a silent accumulation of contradictions I can neither name nor expel.

Late at night, when the single malt (offered first to the tulsi plant as prasad) loosens the knots, the mask slips. I do not merely want to succeed. I want to transcend through strategic dissolution — to borrow, divert, dissolve, and re-emerge on the other side, cleaner, richer, reborn. Not as the next Ambani, but as one who has finally learned their alchemy.

At the summit sit the untouchables: the Ambanis and the Piramals. They move through this world with the serene certainty of those who have already secured their exit. Mukesh Ambani keeps Stoke Park — that sprawling 300-acre English estate with its manicured gardens, lakes, and monuments, once a James Bond backdrop — as a quiet insurance policy. Should the edifice crack here, should the regime that favours them shift or collapse, the family has a ready fortress across the seas. A place to fly to, untouched by the chaos they helped engineer. Piramal, too, operates with the same quiet assurance, his empire expanding through the very ruins others leave behind. They do not fear the fall. They have prepared the landing.

I watch them from my rung on the ladder and feel the exquisite torment of proximity without arrival. My son prepares for Harvard. My daughter attends IIT coaching. My firm advises SMEs on “smart financing.” On the surface, I am the textbook higher-middle-class success story. Beneath it, I am a man divided against himself — performing piety by day while calculating the perfect muhurat for controlled collapse by night.

I am a turncoat by conviction and by planetary design. My astrologer from Ujjain speaks of Surya Dev’s power to grant authority and political ascent. In 2009 I leaned one way. By 2014, when the winds shifted, I became the vocal devotee on WhatsApp groups and temple steps. If the arithmetic changes again, I will pivot without hesitation. Loyalty is illusion. Opportunism, wrapped in saffron and sanctified by guru’s blessings, feels like the only coherent response to a system that rewards exactly this.

As a higher-middle-class financial bourgeois, I occupy the cruellest spot in the hierarchy: close enough to see every rung clearly, yet not high enough to be safe. My days are filled with small-ticket stressed debt and pre-IBC settlements. I know the NCLT delays, the elegant circumventions of disqualification clauses through family trusts and proxies, the phoenixing possibilities that glitter like forbidden fruit.

The dream torments me with crystalline clarity: Build. Borrow aggressively from public-sector banks. Divert with clinical precision through layers my astrologer deems auspicious. Trigger the process at the perfect moment. Emerge on the other side, assets veiled behind a clean SPV, the haircut absorbed by the faceless many. Fail upwards. Convert public liability into private dynasty.

The 98% — the salaried class, the SMEs, the operational creditors, the retail depositors — will subsidise this order through higher taxes, repeated recapitalisations, and costlier credit. They rage on social media. We perform puja, acquire their companies, and toast with single malt offered first to tulsi. They cling to the myth of honest entrepreneurship. I have seen the machinery: a system that preaches credit discipline while institutionalising its elegant violation for those who master the script.

Sometimes, after the 108th repetition of the Surya Mantra, the single malt loosens the final veil. A quiet voice asks: Is this moral? In absolute terms, perhaps not. But in this de facto India, where the logic of capital has fused with the rituals of Sanatan Dharma, where strategic bankruptcy has become a sophisticated, almost respectable path to transcendence, this feels like the most rational, most auspicious, and most existentially satisfying route available.

The suffering is constant and intimate: the low-grade anxiety of staying one step ahead, the moral nausea that rituals only temporarily suppress, the gnawing awareness that I am both predator and potential prey in the same absurd machine. False consciousness wraps around me like a well-tailored kurta — I chant dharma while my hands prepare the diversion; I bow to Shakti while dreaming of public ruin turned private empire.

Yet the aspiration burns brighter than the shame. I want the freedom that only strategic dissolution can grant — the freedom to fail upwards, to convert public liability into private dynasty, to finally possess what the sea-link only teases from my balcony.

So yes, with full faith in Sanatan Dharma, my guru’s guidance, and the blessings of Surya Dev,

I would love to become a bankrupt, superrich wilful defaulter.

Jai Shri Ram. Jai IBC. Jai opportunism. Om Suryaya Namah.

K. (Aspiring member of the 2% club, regular temple donor, and weary follower of auspicious planetary transits)

V. After the Rupture: DHFL as the Archetype of Refined Predation

No single case better exemplifies the post-IBC reality — and the refined predation it enables — than the Dewan Housing Finance Corporation Ltd (DHFL) saga. What began as one of India’s largest alleged housing finance scams, with promoters (the Wadhawan brothers) accused of diverting ₹31,000–34,615 crore through a labyrinth of shell companies and related-party transactions, was swiftly transformed into a textbook demonstration of how the IBC converts public distress into private windfall.

The RBI superseded DHFL’s board in 2019 amid serious governance concerns and admitted the company into CIRP. Piramal Capital & Housing Finance emerged as the successful resolution applicant with a final resolution plan offering a total consideration of ₹37,250 crore (comprising cash and non-cash elements). The Committee of Creditors (CoC), dominated by public-sector banks, approved the plan with an overwhelming 93.65% vote. On 19 May 2021, the NCLT directed the Administrator to place the erstwhile promoters’ full repayment settlement proposal before the CoC — an inconvenient order that was swiftly stayed and quietly bypassed. NCLT eventually approved the plan on 7 June 2021. After protracted litigation, the NCLAT on 27 January 2022 delivered a scathing verdict, declaring parts of the process “contrary to law” and setting aside the clause allowing Piramal to retain recoveries from Section 66 fraudulent trading applications — yet this too was rendered inconsequential when Piramal and the CoC appealed to the Supreme Court. In its April 1, 2025 judgment, the apex court emphatically upheld the original resolution plan, set aside the NCLAT’s interference, reinforced the “commercial wisdom” of the CoC, and crucially allowed Piramal to retain future recoveries from fraudulent transactions and avoidance applications — effectively handing the upside of the very fraud that allegedly sank DHFL to the new owner.

Retail fixed deposit holders and NCD investors suffered devastating haircuts, often losing the bulk of their life savings. Operational creditors recovered poorly, frequently in the low teens or single digits. Meanwhile, Piramal Finance inherited a massive scale, an established customer base, and significant future upside potential. The transaction was not merely a resolution; it was an elegant transfer of distressed assets at a steep discount, with public money absorbing the losses and private hands capturing the gains.

What followed was the final act of sophisticated predation. After Piramal Capital & Housing Finance Ltd (PCHFL) swallowed DHFL through the IBC process, the group executed a second, quieter metamorphosis: PCHFL was restructured, rebranded as Piramal Finance Ltd (PFL), and then used as the vehicle to gulp down its listed parent Piramal Enterprises Ltd (PEL) via a reverse merger approved by the NCLT in September 2025. This was no ordinary consolidation — it was phoenixing by corporate reconfiguration. The new streamlined entity inherited the scale, the customer base, and the lucrative DHFL-derived portfolio, while the clean-slate doctrine (Section 32A of the IBC) and layered restructuring helped insulate it from the full historical stigma and lingering liabilities of the original fraud. By February 2026, even a special PMLA court discharged the DHFL entity (now safely housed under PFL) from a ₹5,050 crore money-laundering case, citing immunity under Section 32A of the IBC. Old sins dissolved. New empire rose — cleaner (?), larger, and legally unburdened.

Piramal’s broader empire-building reveals a systematic, almost surgical playbook that exploits every feature of the IBC ecosystem. The India Resurgence Fund (launched in 2016 as a JV with Bain Capital, raising $629 million in Fund I) has served as a dedicated vehicle for distressed control investments. Early stakes in the Shriram Group (acquired 2014–2016 and later partially exited with substantial gains) demonstrated the model’s profitability. Bids for entities like Reliance Capital (another Anil Ambani-linked stressed asset), pharma bolt-ons (such as Ash Stevens in 2016 and Hemmo Pharmaceuticals for ₹775 crore in 2021), auctions of stressed real-estate loan portfolios in 2023, and the 2025 NCLT-approved reverse merger of Piramal Enterprises into Piramal Finance (aimed at operational efficiencies) were followed by a ₹15,000 crore NCD issuance and multilateral funding (including $350 million from IFC/ADB in early 2026). Each move leverages the IBC’s characteristically modest overall recoveries (~32–33% against admitted claims) and high liquidation rates, allowing acquirers to buy scale at fractions of original debt while public banks write off the rest.

The Anil Ambani Group cases mirror this pattern with almost theatrical symmetry. RCom and associated ADA entities entered CIRP with claims exceeding ₹47,000 crore in several proceedings, often resolving for pennies on the rupee (e.g., settlements as low as ₹455 crore in reported instances). This occurred amid CBI probes into alleged bank frauds cumulatively worth over ₹73,000 crore across multiple group entities, with the Enforcement Directorate flagging irregularities suggesting deliberate triggering of insolvency through unrelated lenders (“Project Help” documents). While probes continue and some assets face attachment, the IBC process has frequently delivered minimal recoveries for original creditors, enabling selective restructuring or exit at deep discounts.

VI. The Political Economy of Crony Capitalism: “Chanda Do, Dhanda Lo” and Selective Enforcement

The BJP-NDA regime’s fingerprints are all over the architecture. Under the now-scrapped electoral bonds scheme (2018–2024), struck down by the Supreme Court in February 2024 as unconstitutional for enabling anonymous quid pro quo, the BJP emerged as the undisputed champion, pocketing the lion’s share — over ₹6,500 crore out of more than ₹16,500 crore total — through opaque corporate donations. Piramal-linked entities alone funnelled at least ₹85 crore to the BJP, while other players in infrastructure, real estate, and distressed assets contributed generously. The Supreme Court itself warned that such donations risked translating into policy favours, regulatory forbearance, and preferential treatment in contracts and resolutions.

PM CARES offered another convenient route: massive “voluntary” contributions from the same corporate houses — including ₹100 crore from the Adani Group and ₹25 crore from the Piramal Group during the pandemic — poured into a fund shielded from RTI scrutiny and parliamentary oversight, functioning as a parallel channel for influence and goodwill.

The Adani Group provides a textbook parallel: it weathered the 2023 Hindenburg exposé and subsequent US DOJ indictment over alleged bribery in solar power contracts, yet faced no prominent listing as wilful defaulters and continued aggressive expansion through government-linked infrastructure deals. Enforcement by the CBI and ED remains glaringly selective — aggressive probes and asset attachments target fallen or inconvenient promoters, while successful acquirers and those aligned with the ruling dispensation enjoy smooth sailing.

Persistent NCLT backlogs, undervalued auctions, and clever circumvention of Section 29A disqualifications through family trusts, proxies, and layered corporate structures complete the sophisticated toolkit.

The human cost stays largely invisible in official narratives. Workers in shuttered West Bengal jute mills and other distressed units endure closures and unpaid dues with scant protection. DHFL’s retail fixed deposit and NCD holders lost large chunks of their life savings. SMEs and operational creditors typically recover a meagre 25.4% (or far less in liquidation). Taxpayers continue footing the bill for massive bank recapitalisation — well over ₹3 lakh crore since 2014 — effectively socialising the haircuts. In this ledger, the 98% subsidise the 2% — a structural feature, not a bug.

K.’s raw, self-reflexive confession — that of the ritual-performing, guru-blessed, Surya-guided higher-middle-class turncoat — is no aberration. It is the system speaking in its most honest voice. Dharma, planetary charts, and opportunistic “smart karma” merely sanctify the normalisation of superrich-crony predation. In de facto India, strategic bankruptcy has become not just viable but aspirational — a culturally endorsed, IBC-enabled path to transcendence for those who master the game.

VII. Conclusion: Systemic and Moral Bankruptcy

From the 5–26% recoveries and 5,800 BIFR cases of 1968–2014, through the 2014–15 crisis, to the 8,833 admissions, ~31.6–32.8% recoveries, 18,318 wilful defaulters owing ₹3.83 lakh crore as of March 2025, and Piramal-style empires built on public haircuts, the trajectory is damning. The IBC did not reform Indian capitalism — it refined its predatory core. Under the BJP-NDA, it became a political instrument that socialises losses, privatises gains, and turns strategic bankruptcy into an aspirational, ritual-sanctified dream. The rupture of K.’s confession is the system’s true voice: pious on the outside, predatory within.

Yet the most disturbing question remains deliberately buried: Why was DHFL forced into the IBC at all? As a regulated housing finance company and deposit-taking NBFC, DHFL was never an industrial undertaking and fell squarely outside the original intent and scope of corporate insolvency proceedings under the Code. It was demonstrably solvent with sufficient asset cover (1.16 times its debt liability, as affirmed in Bombay High Court proceedings), and secured creditors already possessed powerful enforcement tools under the SARFAESI Act, 2002 — which allows swift recovery of secured debts without the elaborate, time-consuming theatre of CIRP, CoC horse-trading, and NCLT oversight. Alternative routes under the RBI’s Prudential Framework, Sections 45MBA/45QA of the RBI Act, or even the Companies Act, 2013 (as successfully used in IL&FS) were readily available and far more protective of retail depositors and NCD holders.

Instead, the RBI superseded the board in 2019, concealed material facts before the NCLT, and pushed DHFL into IBC through an arbitrary MCA notification (S.O. 4139(E) dated 18.11.2019) that selectively brought certain NBFCs/HFCs under the Code. This route delivered massive haircuts to public banks and wiped out large portions of life savings of small fixed deposit and NCD holders, while ultimately handing the entire upside — including future recoveries from fraudulent transactions under Section 66 — to BJP-favoured Piramal.

Was this ever a genuine resolution mechanism designed for revival and creditor protection? Or was it a carefully orchestrated institutional bypass, chosen precisely because SARFAESI and other enforcement routes would not have permitted such a deep-discount, pre-decided transfer of assets to a politically networked acquirer? The selective invocation of the “fluid” IBC, while deliberately sidelining simpler and more accountable remedies like SARFAESI, lays bare the Code’s deepest hypocrisy: it is not applied where insolvency truly demands it, but where it best serves the interests of the connected few, i.e., those who are “more equal than others“!

True accountability demands dismantling crony networks, ending opaque funding, enforcing genuine personal liability, and rejecting the hypocrisy that blesses crony capture with mantras and planetary charts. Until then, the great Indian bankruptcy dream remains the most rational — and most damning — aspiration of our time.

Jai Hind. Or, more accurately in this de facto reality — Jai IBC. Jai opportunism. Om Suryaya Namah.

Acknowledgment: Mr. Ravindra Mahidhar, widowed senior citizen and former DHFL FD Holder/Victim

See Also:

Sources

- Insolvency and Bankruptcy Board of India (IBBI) Quarterly Newsletters and Performance Reports (up to December 2025): https://ibbi.gov.in/publication (main publication page with latest quarterly newsletters, including Oct-Dec 2025)

- Analysis of Insolvency Cases under IBC as on 31.12.2024, IBC Laws: https://ibclaw.in/analysis-of-insolvency-cases-under-ibc-as-on-31-12-2024-cirp-initiation-closures-recovery-and-yield-from-resolution-plan-and-liquidation/

- ICRA and CARE Ratings Reports on IBC Recoveries (Q3 FY2026 data as of December 2025): CARE Ratings: https://www.careratings.com/uploads/newsfiles/1770200094_Recovery%20Rates%20under%20IBC%20Remain%20Rangebound%20at%2032%20pct%20in%20Q3FY26.pdf Related ICRA/CARE coverage: https://www.financialexpress.com/business/news/insolvency-recoveries-hit-15-quarter-low/4152706/

- Reserve Bank of India (RBI) Wilful Defaulters Returns and Master Directions (data as of March 2025): https://www.rbi.org.in/Scripts/BS_ViewMasDirections.aspx?id=12177 (Master Directions on Wilful Defaulters) Consolidated data references: https://www.watchoutinvestors.com/wilful_defaulters.asp (publicly available lists)

- Parliamentary Standing Committee on Finance, 28th Report (December 2025) – Review of working of IBC: https://ibbi.gov.in/uploads/resources/d75daa3a490fc1bc316632cd993fca06.pdf (Also available via Lok Sabha Secretariat / ibclaw.in summaries)

- Supreme Court of India Judgment in Piramal Capital & Housing Finance Ltd. v. 63 Moons Technologies Ltd. & Ors. (April 1, 2025): https://api.sci.gov.in/supremecourt/2022/5046/5046_2022_9_1501_60698_Judgement_01-Apr-2025.pdf (Full judgment on SCI website / SCC Online)

- RTI responses and Ministry of Finance replies on bank write-offs and recapitalisation (2014 onwards): Parliamentary replies and Ministry of Finance data (aggregated in PRS India and Sansad records)

- EY and PwC Reports on IBC Evolution (2025–2026 editions): EY: https://www.ey.com/en_in/insights/strategy-transactions/nine-years-of-ibc-transforming-india-s-insolvency-landscape

The Insolvency and Bankruptcy Code was sold as reform. Really? A sophisticated mechanism for crony enrichment: massive haircuts on public funds, Section 32A immunity, and phoenixing that rewards wilful defaulters. Average recovery ~32% while select players consolidate empires. Is this “ease of doing business” or institutionalised loot?

Serious discussion welcome.

#IBCReformNow #CronyCapitalism #CorporateCaptureIndia #FinancialJusticeIndia #BankruptcyBazaar #RegulatoryFailureIndia #AccountabilityInIBC, #Scrap_Ill_Conceved_IBC, #DHFL_SCAM, #Ajay_Piramal_Cronyism , #Seize_Cronies_Fairplay_for_DHFL_Victims, #BJP_Cronyism, #Alleged_Dawood_Mirchi_Rkw_Dhfl_Bjp_Collusion, #AjayPiramal_Phoenixing,

LikeLiked by 1 person