Posted on 17th April, 2026 (GMT 03:55 hrs)

ABSTRACT

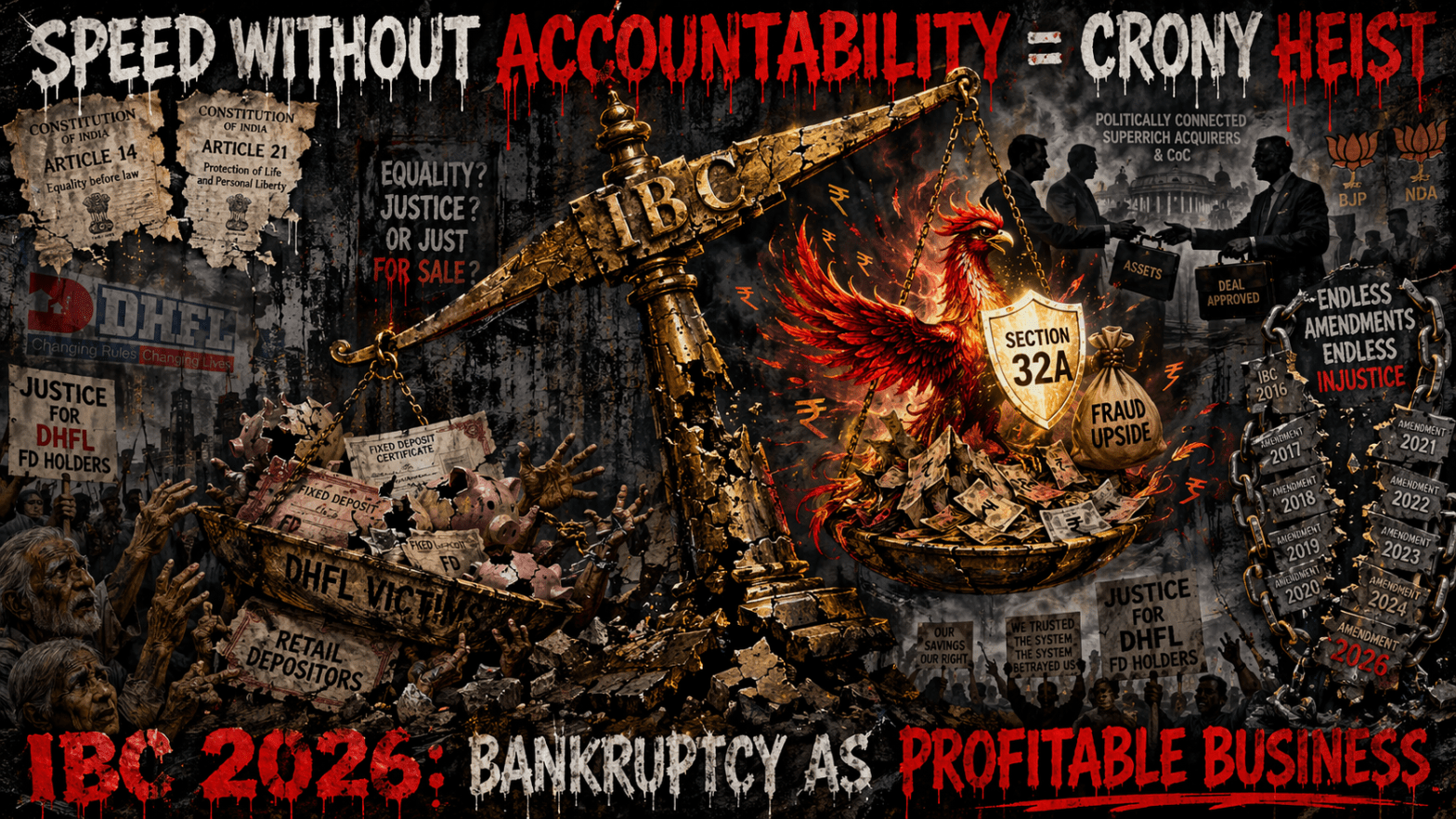

This report by Once in a Blue Moon Academia indicts the IBC (Amendment) Act, 2026 as a high-speed polish on a structurally flawed regime. While promising faster resolutions and marginal creditor safeguards, it leaves untouched the core contradictions — especially the tension between Section 66 (fraud recovery for creditors) and Section 32A (clean-slate immunity) — that enabled the DHFL heist, where retail depositors lost 75–80% while fraud upside flowed to Piramal. The amendment accelerates crony capture rather than correcting it, turning bankruptcy into a profitable tool for the superrich at the expense of the common people.

I. Introduction: A High-Speed Polish on a Structurally Flawed Engine?

In the wake of India’s most sweeping overhaul of the Insolvency and Bankruptcy Code since its 2016 inception—the IBC (Amendment) Act, 2026—whistleblowers like us are left wondering whether this legislative sprint truly serves justice or merely accelerates an already lopsided machine. The amendment promises faster admissions, a novel creditor-initiated process, group insolvency frameworks, tighter liquidation timelines, and marginally stronger minority creditor safeguards.

Yet, when viewed through the lens of real-world casualties like the DHFL saga, these changes appear less like genuine reform and more like a high-speed surface-level polish on a fundamentally flawed engine—one that continues to socialize massive losses while privatizing extraordinary gains.

This brief report by Once in a Blue Moon Academia (OBMA) serves as a sharp indictment of the IBC (Amendment) Act, 2026 — exposing not merely what it adds, but what it deliberately withholds, and the deeper structural violence it refuses to confront.

II. Documented Failures and the Promise of the 2026 Amendment

At its core, the 2026 amendment responds to a decade of documented failures: average Corporate Insolvency Resolution Process (CIRP) timelines ballooning to 700+ days, chronic NCLT backlogs, low recovery rates hovering around 31–33 per cent (implying 67–68 per cent haircuts), and endless litigation that erodes enterprise value.

The new law mandates 14-day admissions, introduces a debtor-in-possession Creditor-Initiated Insolvency Resolution Process (CIIRP) with a 195-day cap, empowers the Committee of Creditors (CoC) further in liquidation, and codifies stronger floors for dissenting financial creditors. On paper, these are creditor-friendly tweaks designed to reduce judicial discretion, curb delays, and make the system more predictable.

But predictability for whom? And at what cost?

III. The DHFL Saga as Litmus Test

Consider the DHFL case—not as a historical footnote, but as the litmus test for whether the 2026 regime can deliver equity. Admitted into CIRP in December 2019, DHFL involved over ₹87,000 crore in claims, including ₹6,188 crore from more than one lakh retail fixed deposit (FD) and NCD holders—predominantly senior citizens, pensioners, and middle-class families who had parked life savings in what was once an AAA-rated housing finance company.

The Piramal resolution plan, approved by 93.65 per cent CoC votes in 2021 and upheld by the Supreme Court in April 2025, delivered FD holders a recovery of just 23.08 per cent on admitted claims (often translating to 19–23 paise in the rupee after the December 2019 cut-off date). Fraudulent diversions estimated between ₹31,000 crore and ₹45,000 crore were valued at a notional ₹1 in the Piramal plan, with all future avoidance recoveries (under Section 66) accruing exclusively to the successful resolution applicant (SRA). Post-resolution, the entity received a clean discharge in a ₹5,050 crore PMLA case in February 2026, courtesy of the clean-slate doctrine. The case is now legally closed (is it?!)—prospective law cannot reopen it.

The case is now (supposedly) de facto closed within the domestic geopolitical territory named India — prospective law such as the 2026 amendment cannot perhaps reopen it. However, it remains de jure incomplete: the NCLT order dated 19th May 2021 (which had asked the CoC to reconsider full repayment proposals by the ex-promoters) and the NCLAT order dated 27th January 2022 (which had flagged material irregularities and contrary-to-law aspects in the DHFL resolution process and Piramal’s plan) have been fundamentally sidelined in the implementation of the Supreme Court’s directions. Particularly glaring is the treatment and monitoring of avoidance transactions under Section 66. Despite the Supreme Court’s explicit directive to the NCLT to deal with these applications, there has been no meaningful update or progress on recovery and distribution of proceeds from these fraudulent transactions even as of April 2026.

Yet, even if recoveries materialise, they would — per the approved resolution plan and the Supreme Court’s upholding of the CoC’s so-called “commercial wisdom” — accrue entirely to the successful resolution applicant (Piramal), and not to the dissenting creditors or the common people (the retail FD and NCD holders). This stands in stark contrast to the original intent of Section 66, which targets fraudulent and wrongful trading for the benefit of all creditors and the maximisation of value for the corporate debtor’s estate. This leaves a profound lingering legal and moral gap in what is otherwise aggressively presented as a final and binding resolution.

Here lies the first uncomfortable question the 2026 amendment forces us to confront: If the old regime already produced such outcomes, do the new procedural accelerations merely grease the wheels of the same transfer mechanism?

The amendment’s 14-day mandatory admission and record-of-default conclusiveness from Information Utilities will indeed slash preliminary delays. Yet in DHFL-like scenarios—where forensic audits had already flagged massive siphoning—speed without parallel accountability simply shortens the window for victims to be heard. The new CIIRP’s debtor-in-possession model and relaxed moratorium may preserve some value early on, but it still vests overwhelming power in notified financial creditors (largely banks) holding 51 per cent debt. Retail FD holders, classified as unsecured financial creditors, remain structurally subordinate. The “stronger protection” for dissenting creditors—guaranteeing the lower of liquidation value or pro-rata share—sounds ostensibly “progressive”, yet in practice, when liquidation values themselves are distress-sale depressed, it offers cold comfort. In DHFL, even that floor would likely have changed little given the CoC’s commercial wisdom in favour of Piramal prevailed.

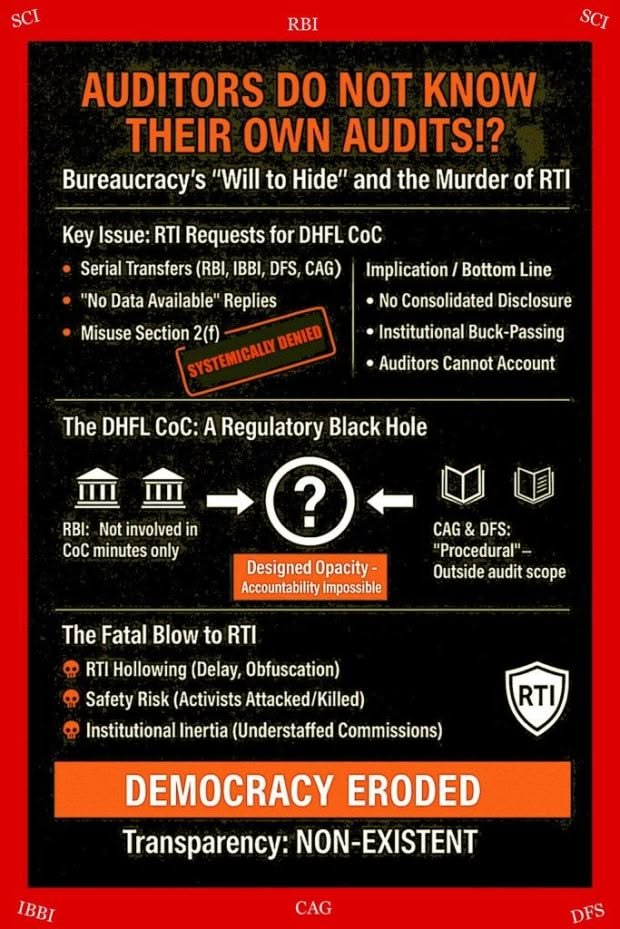

It is a matter of deep regret that we filed multiple RTIs seeking the DHFL CoC’s expenditure breakdowns, minutes, voting records, litigation and travel fund sources, and related accountability documents. The responses are revealing: serial transfers between the RBI, IBBI, DFS, and CAG; uniformly phrased “no data available” replies; and repeated denials under Section 2(f), incorrectly claiming that minutes, voting records, and financial statements do not qualify as “information.” FAA responses merely echoed these evasions.

What emerges is not an administrative lapse but a patterned refusal—an entrenched bureaucratic instinct to deflect, delay, and diffuse responsibility. Transparency is thus reduced to a ritual formality, while accountability is systematically evaded. Bottom line: auditors “don’t know their own audits.” The coherence of the evasions across agencies is itself evidence of systemic secrecy.

IV. The Foundational Contradiction: Section 66 vs. Section 32A

At its core, the IBC contains a structural contradiction: it seeks to penalize fraud (Section 66) while simultaneously erasing its consequences (Section 32A).

More critically, the 2026 overhaul leaves this foundational contradiction untouched. The amendment strengthens and codifies the clean-slate principle through new provisions in Section 31(5) and 31(6), explicitly declaring that upon approval of a resolution plan, all prior claims against the corporate debtor and its assets stand extinguished (except those specifically assumed in the plan), and no proceedings can be continued or initiated in respect of such extinguished claims. It further reinforces this shield by making the clean-slate protection retrospective in effect for plans approved since 2016.

At the same time, the amendment makes only cosmetic improvements to avoidance transactions: it extends the look-back period, allows creditors to file applications if the Resolution Professional or liquidator fails to act, and clarifies that avoidance proceedings (including under Section 66) can continue independently even after completion of CIRP, liquidation, or dissolution.

This is no minor drafting oversight; it is structural impunity deliberately engineered and now further fortified into the Code. While the amendment gives slightly more teeth to detection and continuation of avoidance actions, it ensures that any recoveries or benefits ultimately flow according to the approved resolution plan — meaning, in practice, they accrue to the successful resolution applicant rather than the body of creditors. In DHFL, this metamorphosis allowed the corporate debtor to emerge spotless — same assets, same business lines, zero historical sins — while the SRA pocketed the upside of fraud recoveries. Retail depositors lost 75–80 per cent of their principal; the new owner reported soaring post-merger profits and AUM growth. The 2026 law’s liquidation safeguards (CoC supervision of liquidators, 180+90 day timelines) and avoidance look-back extensions are welcome on paper, but they remain toothless when the strengthened Section 32A can retroactively neuter their impact once a plan is approved.

This raises a deeper philosophical and constitutional reflection: Does the IBC’s obsessive deference to “commercial wisdom” of the CoC — now further entrenched by higher withdrawal thresholds (90 per cent) and restricted post-invitation exits — align with Article 14’s guarantee of equality or Article 21’s protection of livelihood?

When CoC decisions routinely favor politically connected acquirers (such as Piramal and his reported intimacy with the BJP) through layered structures, proxies, or family trusts (bypassing Section 29A disqualifications), and when avoidance proceeds are assigned at nominal value, the Code stops functioning as a resolution mechanism and begins resembling a state-sanctioned asset reallocation tool for consolidating concentration of wealth. The 2026 group insolvency and cross-border provisions may appear to handle complexity better, but they do nothing to prevent the phoenixing of fraud-tainted empires. In DHFL’s interconnected web of subsidiaries, coordinated resolution might have been administratively tidier — but would it have altered the outcome for FD holders? Unlikely, given the same CoC dominance and same clean-slate endpoint.

This structural design — ill-conceived from the outset, heavily amended seven times and tweaked through over 140 regulatory changes, yet remaining internally incoherent — has effectively enabled crony capture by the superrich. In DHFL and similar cases, the framework has facilitated the transfer of distressed assets and fraud upside to politically well-connected acquirers such as Mr. Ajay Piramal at steep discounts, while shielding them through the clean-slate mechanism under Section 32A. Public losses are socialized via taxpayer-funded bank recapitalisation; private gains are privatized in the hands of a few chosen conglomerates that emerge stronger, often through phoenixing and circumvention of safeguards. Far from curbing cronyism, the IBC has institutionalised a sophisticated mechanism of wealth reallocation that disproportionately benefits the superrich at the expense of retail depositors, workers, and the public exchequer.

Structural reform must go far beyond procedural tweaks and further empowerment of the CoC. It demands structural surgery: granting statutory priority to small depositors and retail financial creditors up to a defined threshold, mandating full clawback of proceeds from avoidance and fraudulent trading transactions (Section 66) directly to the creditors rather than the successful resolution applicant, imposing clear limits on the clean-slate immunity under Section 32A in cases involving proven fraud or diversion of funds, and introducing mandatory class voting rights for retail financial creditors so that their collective voice cannot be steamrolled by institutional majorities. Without these fundamental correctives, the IBC will continue to function not as a rescue mechanism, but as a sophisticated legal instrument for dispossession and crony enrichment.

V. Efficiency at the Expense of Vulnerable Stakeholders

The amendment’s decriminalization of certain professional offences and stiffer civil penalties for frivolous filings or moratorium breaches signal a shift toward efficiency over moral hazard. Yet this efficiency comes at the expense of vulnerable stakeholders. FD holders in DHFL were never granted separate class voting or statutory priority despite the company’s deposit-taking mandate under RBI/NHB frameworks. The IBC was applied despite the pre-existence of SARFAESI, RDB Act, and Companies Act remedies that could have enabled faster, less destructive recovery. The 2026 law does not revisit this selective applicability or create carve-outs for retail depositors in financial service providers. Instead, it doubles down on speed and creditor (read: institutional) control.

One cannot ignore the broader macroeconomic and societal implications. Cumulative haircuts under the IBC now exceed ₹8 lakh crore, disproportionately borne by public-sector banks recapitalized by taxpayer funds. These losses are socialized; the gains—distress assets acquired at 30–35 cents on the dollar, fraud upside privatized, and empires expanded—are not. The 2026 amendment’s emphasis on faster resolutions and competitive bidding may improve India’s World Bank (the neo-imperialist design, of course!) ease-of-doing-business metrics, but it risks accelerating the very wealth transfer it claims to curb. For lakhs of FD holders across similar NBFC/HFC crises (past and future), the message remains unchanged: your contractual rights, your life savings, and your faith in regulatory safeguards are subordinate to the CoC’s opaque commercial calculus in alignment with the interests of the political establishment, viz., the BJP-NDA regime as of now.

VI. The Violence of Trials and Errors: Multiple Amendments and Endless Tweaks

Some people might say that the 2026 amendment is not without merit. It acknowledges real pain points—judicial delays, fragmented group proceedings, cross-border gaps—and attempts pragmatic fixes.

Yet a critical reflection demands we ask the harder questions the tweaks evade:

Why does the IBC continue to treat fraud as a temporary inconvenience rather than a disqualifying sin?

Why does “resolution” so often mean extinguishing retail claims while granting new owners a corporate rebirth unburdened by history/past sins?

And if the Code has required multiple amendments (including this seventh major overhaul) in under a decade, is incremental (short-term, surface-level) patching at all sustainable, or does the architecture itself require fundamental re-examination from scratch?

Major Amendments (Year-wise):

| No. | Amendment Act | Year | Key Notes |

|---|---|---|---|

| 1 | IBC (Amendment) Act, 2017 | 2017 | First major changes (promoter eligibility, etc.) |

| 2 | IBC (Amendment) Act, 2018 | 2018 | Homebuyers as financial creditors, Section 29A refinements |

| 3 | IBC (Amendment) Act, 2019 | 2019 | Extended CIRP timeline to 330 days, minimum payouts to operational creditors |

| 4 | IBC (Second Amendment) Act, 2020 | 2020 | COVID-related suspension of filings, pre-pack for MSMEs |

| 5 | IBC (Amendment) Act, 2021 | 2021 | Relaxed thresholds for startups/MSMEs, performance bank guarantees, etc. |

| 6 | (Any minor or ordinance-based in between, counted in official tallies) | – | Some sources group ordinances that became Acts |

| 7 | IBC (Amendment) Act, 2026 (Act No. 6 of 2026) | 2026 | The latest and most comprehensive overhaul (assented on 6 April 2026) |

Breakdown by Major Regulatory Tweaks (Approximate Counts)

| Regulation | Approximate Number of Amendments (till April 2026) | Notes |

|---|---|---|

| IBBI (Insolvency Resolution Process for Corporate Persons) Regulations, 2016 (CIRP Regulations) | 35–40+ | The most frequently amended; multiple amendments every year, including 7–8 in 2025 alone. |

| IBBI (Liquidation Process) Regulations, 2016 | 25–30+ | Several in 2025–26, including two in early 2026. |

| IBBI (Voluntary Liquidation Process) Regulations, 2017 | 15–18 | Steady tweaks. |

| IBBI (Pre-Packaged Insolvency Resolution Process) Regulations, 2021 | 8–10 | Newer framework, still being refined. |

| IBBI (Insolvency Professionals) Regulations + others (Valuers, Information Utilities, Personal Guarantors, etc.) | 40–50 combined | Includes procedural, ethical, and reporting changes. |

Total regulatory amendments across all IBBI regulations: Around 140–160 since 2016 (this includes every “Amendment Regulations” notification, even minor ones that change a single clause or form).

Now, why are there so many amendments and tweaks?

The IBC is a framework law — the main Act sets broad principles, while IBBI fills in the operational details. Issues discovered during implementation (delays, valuation disputes, CoC functioning, avoidance transactions, etc.) lead to quick fixes via regulations. Every major Parliamentary amendment (like the 2019, 2020, or 2026 ones) triggers a fresh wave of 5–15 regulatory changes to align the rules with the new law. In 2025–26 alone, IBBI issued multiple batches of amendments (e.g., February 2026 saw 5+ amendments notified on the same day covering CIRP, Liquidation, Pre-Pack, etc.).

Beneath this relentless cycle of legislative and regulatory patching, BJP-NDA’s cronyism works efficiently in the background — systematically enabling the transfer of distressed public assets and fraud upside to a handful of well-connected superrich acquirers while shielding them through the clean-slate mechanism.

Hence, this relentless trial-and-error approach is not mere legislative learning. It represents a form of structural violence systematically perpetrated by the BJP-NDA regime. At a time when the government has aggressively pursued disinvestment of public sector undertakings, routinely waived off loans of wilful defaulters, and facilitated the transfer of vast public wealth and assets to a handful of favoured conglomerates like Ambani, Adani, and Piramal, the IBC has functioned as a sophisticated laboratory. The lakhs of DHFL fixed deposit holders, mostly senior citizens and middle-class families, have been treated as guinea pigs in this grand experiment — their life savings sacrificed at the altar of “ease of doing business” and crony enrichment. What is presented as incremental reform is, in reality, the normalisation of dispossession through endless patching of a fundamentally extractive framework.

SCAM 2019: THE DHFL MASSACRE VIEW HERE ⤡

VII. Conclusion: Speed Without Accountability

As India’s insolvency regime hurtles toward greater speed and creditor empowerment under the IBC (Amendment) Act, 2026, the DHFL episode stands as a cautionary mirror. It reveals not merely implementation failures or procedural delays, but a deeply entrenched doctrinal and structural design that systematically normalizes dispossession and wealth reallocation under the banner of efficiency and “commercial wisdom.”

True reform cannot remain confined to tightening timelines, empowering the CoC further, or adding cosmetic safeguards. It must dismantle the moral and systemic inversion at the Code’s core — where public pain is routinely converted into private rebirth for a privileged few. Until the architecture itself is fundamentally re-examined and the clean-slate shield is made conditional on the absence of proven fraud, the IBC (Amendment) Act, 2026 risks becoming yet another chapter in the ongoing story of bankruptcy as profitable business rather than equitable justice.

The reflection is sobering: speed without structural accountability is not progress; it is merely acceleration toward the same destination of institutionalized inequity. The question for policymakers, jurists, and citizens alike is whether we are willing to accept this destination — or demand an entirely different road that prioritizes justice for retail victims over the convenience of cronies.

The above matter in the form of correspondence was sent to several institutions and ministries of India. The details of the letter are as follows (17-04-2026; GMT 18:15 hrs):

References

Official Legal and Government Sources

- The Insolvency and Bankruptcy Code (Amendment) Act, 2026 (Act No. 6 of 2026) – Official Gazette Notification (assented on 6 April 2026) https://ibbi.gov.in/uploads/legalframwork/2026-04-07-115842-i5nsk-7ed69ef2a4d23a8b0d472cc0fcd55e79.pdf

- Insolvency and Bankruptcy Board of India (IBBI) – Various Regulatory Amendments (2025–26) https://ibbi.gov.in/ (official notifications section)

- Supreme Court Judgment in Piramal Capital & Housing Finance Ltd. v. 63 Moons Technologies Ltd. & Ors. (Civil Appeal Nos. 1632-1634 of 2022 & connected matters, decided on 1 April 2025) – Upholding the DHFL Resolution Plan https://api.sci.gov.in/supremecourt/2022/5046/5046_2022_9_1501_60698_Judgement_01-Apr-2025.pdf

- PMLA Special Court Order discharging Piramal Finance (ex-DHFL) from ₹5,050 crore case (February 2026, citing Section 32A) (Referenced in multiple reports; full order available via legal databases or Bar & Bench coverage)

Performance Data and Reports

- IBBI Quarterly Reports & Recovery Statistics (Recovery rates rangebound at ~31–33% as of Q3 FY26; average CIRP timelines ~700+ days) https://ibbi.gov.in/ (Quarterly Reports section) Supporting analysis: CARE Ratings – “Recovery Rates under IBC Remain Rangebound at 32% in Q3FY26” (February 2026)

OBMA (Once in a Blue Moon Academia) Series – Core Critical Articles

- The 23.08% Illusion? DHFL Scam and the IBC’s Presumed Finality (Posted 10 April 2026) https://onceinabluemoon2021.in/2026/04/10/the-23-08-illusion-dhfl-scam-and-the-ibcs-presumed-finality/

- Bankruptcy as Profitable Business: India’s Grand IBC Heist (Posted 16 April 2026) https://onceinabluemoon2021.in/2026/04/16/bankruptcy-as-profitable-bijness-indias-grand-ibc-heist/

- Scrap IBC Now: How Section 32A Buried Section 66 – The DHFL Case (Video + Article, Posted 7 April 2026) https://onceinabluemoon2021.in/2026/04/07/scrap-ibc-now-how-section-32a-buried-section-66-the-dhfl-case-video/

- Expose IBC’s Dirty Secret: Resist the Structural Impunity for Cronies (Posted 21 March 2026) https://onceinabluemoon2021.in/2026/03/21/expose-ibcs-dirty-secret-resist-the-structural-impunity-for-cronies/

- The Clean Slate and the Unpaid Sin: Section 32A, Section 66 and Corporate Metamorphosis of Liability (Posted 27 February 2026) https://onceinabluemoon2021.in/2026/02/27/ibcs-clean-slate-and-the-unpaid-sin-section-32a-section-66-and-the-corporate-metamorphosis-of-liability/

- The Bankruptcy Bazaar: How India’s Ill-Conceived IBC Turns Public Money into Private Profits (Posted 5 January 2026) https://onceinabluemoon2021.in/2026/01/05/the-bankruptcy-bazaar-how-indias-ill-conceived-insolvency-and-bankruptcy-code-ibc-turns-public-money-into-private-profits/

- Manifesto for Scrapping the Ill-Conceived Insolvency and Bankruptcy Code (IBC), 2016 (Posted 21 January 2026) https://onceinabluemoon2021.in/2026/01/21/manifesto-for-scrapping-the-ill-conceived-insolvency-and-bankruptcy-code-ibc-2016/

- Non-Applicability of IBC, 2016 on DHFL Scam (with relevant documents, Posted 11 August 2021 – foundational piece) https://onceinabluemoon2021.in/2021/08/11/non-applicability-of-ibc-2016-on-dhfl-scam-with-relevant-documents-for-litigation/

Additional References

- Supreme Court Online / Indian Kanoon summary of the DHFL judgment: https://indiankanoon.org/doc/190999006/

- General IBBI Website for all notifications and statistics: https://ibbi.gov.in/

Another IBC “reform” that changes nothing fundamental. The 2026 Amendment accelerates resolutions while protecting the superrich: socialize 75-80% haircuts on public & retail money, privatize gains via phoenixing, and grant retrospective clean-slate immunity. DHFL victims still waiting for justice while connected acquirers celebrate. This is not reform — it’s structural dispossession! Share if you’re tired of taxpayer-funded crony bailouts.

#IBCHeist #CronyHeist #CosmeticSpeed #DeepeningTheCronyHeist #IBCAmendment2026 #IBCScam #PublicMoneyPrivateProfits #FinancialAbuseDHFL #ReclaimPublicFunds #EndFinancialImpunity,#Scrap_Ill_Conceved_IBC, #DHFL_SCAM, #Ajay_Piramal_Cronyism, #Seize_Cronies_Fairplay_for_DHFL_Victims, #BJP_Cronyism, #Alleged_Dawood_Mirchi_Rkw_Dhfl_Bjp_Collusion, #AjayPiramal_Phoenixing,

LikeLiked by 2 people

The IBC (Amendment) Act 2026 claims to deliver speed and certainty. Really? It papers over deep flaws: unresolved tension between fraud penalties (Section 66) and clean-slate immunity (Section 32A), cosmetic expansion of look-back periods, and continued CoC dominance that subordinates retail creditors. Average recoveries remain low while distressed assets transfer to connected players at steep discounts. Is this genuine reform or acceleration of institutionalized inequity? Thoughtful views welcome.

#IBCAmendment2026 #IBCReformNow #CronyCapitalism, #CleanSlateImpunity #CorporateCaptureIndia #FinancialJusticeIndia #BankruptcyBazaar #AccountabilityInIBC #Section32A, #Scrap_Ill_Conceved_IBC, #DHFL_SCAM, #Ajay_Piramal_Cronyism, #Seize_Cronies_Fairplay_for_DHFL_Victims, #BJP_Cronyism, #Alleged_Dawood_Mirchi_Rkw_Dhfl_Bjp_Collusion, #AjayPiramal_Phoenixing,

LikeLike