Posted on 26th January, 2026 (GMT 11;52 hrs)

Updated on 27th January, 2026 (GMT 04:08 hrs)

ABSTRACT

This article critically examines the Insolvency and Bankruptcy Code (IBC), 2016, arguing that it has evolved into a structurally predatory regime enabling the systematic transfer of public, depositor, and taxpayer-backed wealth to politically connected private entities. Through the lens of the DHFL resolution, it analyzes key judicial rulings—including the Delhi High Court’s holding that Insolvency Professionals are not “public servants” under the Prevention of Corruption Act, 1988, and the Supreme Court’s 2025 affirmation of the Piramal plan—revealing chronic delays, 67–68% average haircuts, fraud laundering via Section 32A, and unchecked Committee of Creditors (CoC) dominance. Situating DHFL within India’s declining Corruption Perceptions Index (96th/180, score 38/100 in 2024), the study highlights premature occupation by Ajay Piramal, enabled by his secondary kinship to Mukesh Ambani and BJP-linked patronage. It concludes that incremental amendments are insufficient and advocates complete repeal in favour of a transparent, constitutionally compliant framework prioritizing public interest, restitution, and accountability under Articles 14 and 21.

0. Introduction

The Insolvency and Bankruptcy Code (IBC), 2016 was enacted to replace India’s fragmented insolvency regime with a unified framework promising time-bound resolution, value maximization, and equitable balancing of stakeholder interests. In practice, however, the Code has increasingly operated as a mechanism of structured dispossession, facilitating the transfer of public wealth into private hands through the technocratic idiom of efficiency, certainty, and market discipline. This transformation is most starkly visible in large financial collapses such as DHFL, where public depositors and small creditors have been systematically marginalized while corporate acquirers realize disproportionate gains.

This article anchors its critique in a deeply unsettling legal development: the judicial determination that Insolvency Professionals (IPs), Resolution Professionals (RPs), and Resolution Administrators—despite exercising extensive quasi-judicial control over public assets, creditors, and livelihoods—do not qualify as “public servants” under the Prevention of Corruption Act (1988). The resulting contradiction is fundamental. While the IBC is repeatedly affirmed as a supreme and overriding code, the actors who operationalize it remain insulated from transparency obligations, anti-corruption scrutiny, and democratic accountability. If these functionaries are neither public servants nor subject to public law safeguards, yet wield sovereign-like authority over institutions sustained by public funds, the question of answerability becomes inescapable.

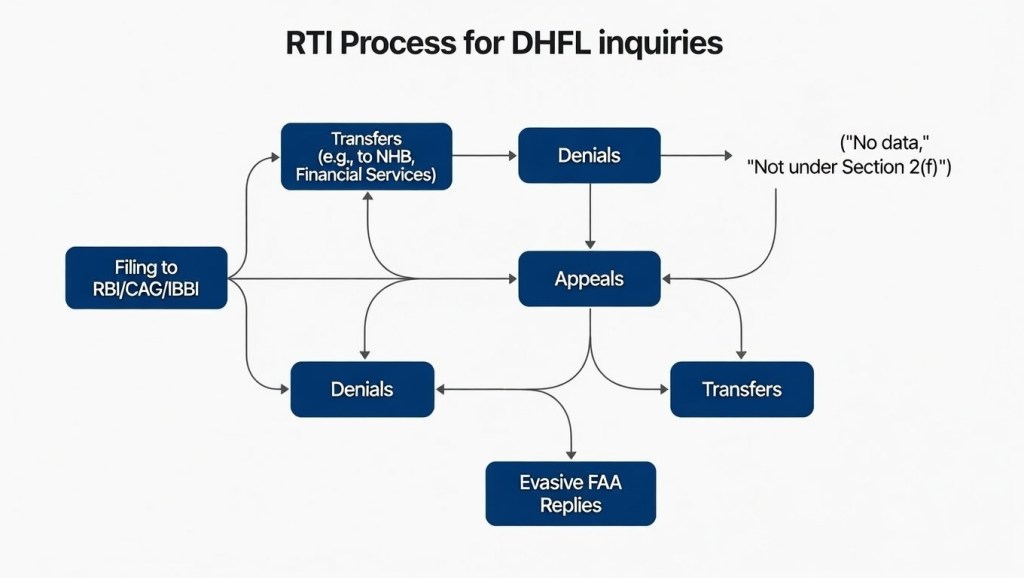

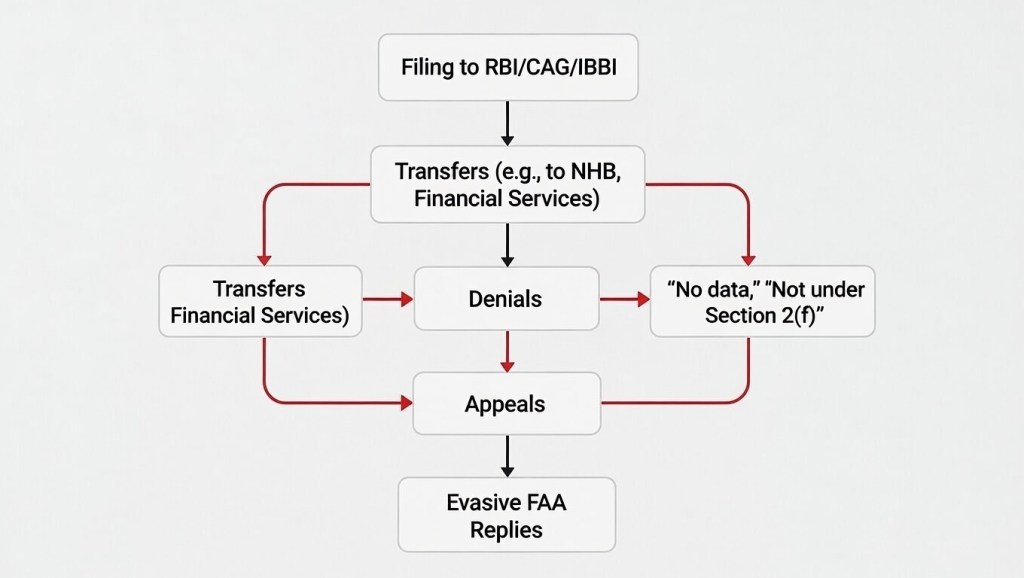

The DHFL resolution exposes this accountability vacuum with particular clarity. The Committee of Creditors (CoC), dominated by institutional lenders, operates without meaningful representation of public depositors, while Resolution Professionals function as de facto governors of collapsed entities—immune to RTI scrutiny and shielded from effective oversight even amid allegations of valuation distortion, procedural irregularity, and conflict of interest. Persistent information denials and evasions point to a broader condition of institutional opacity, where legality persists but answerability steadily erodes.

This article argues that such immunity-cum-impunity is not incidental but structural. Heavily amended, internally inconsistent, and conceptually fragile, the IBC has evolved into a legal architecture that norm-alizes systemic corruption through procedural abstraction. Insolvency, bankruptcy, and liquidation are transformed into instruments of crony capitalist extraction, enabling politically protected corporate actors—most notably in the DHFL–Piramal resolution—to privatize public assets at steep discounts while socializing losses. In this political economy, the IBC no longer merely resolves financial distress; it reorganizes power, legitimizes expropriation, and sanitizes cronyism through judicially endorsed process.

By integrating doctrinal analysis, the DHFL case study, and a political economy perspective, this inquiry calls for a fundamental rethinking of insolvency law—not as a neutral market mechanism, but as a domain of democratic accountability, public interest, and constitutional responsibility.

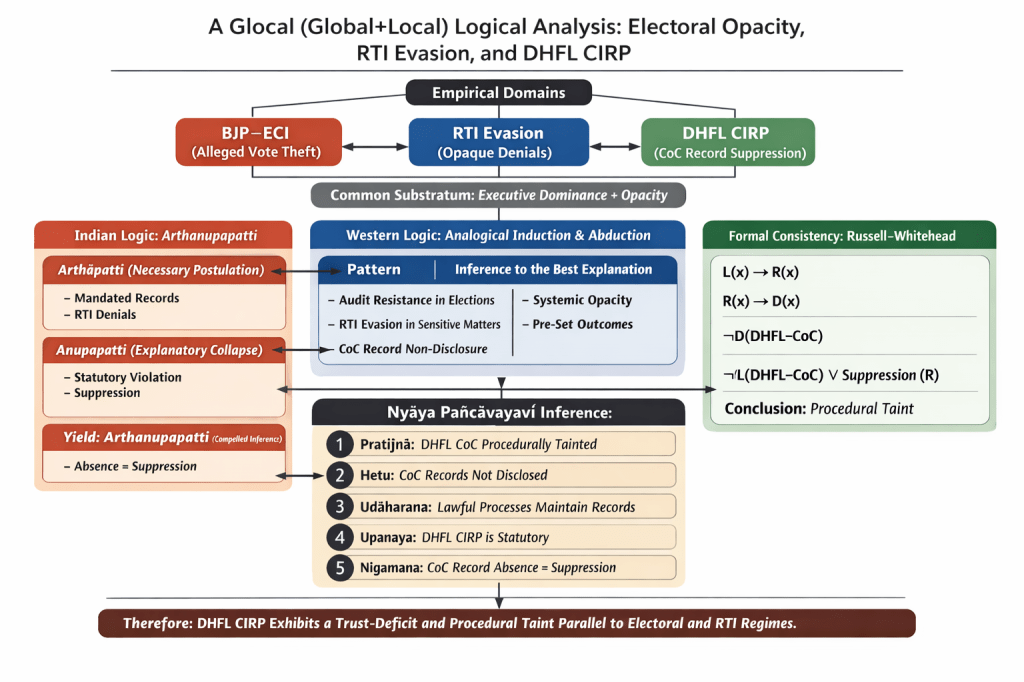

I. Diagnosing the Accountability Vacuum: Logico-Legal Inconsistencies in Classifying Insolvency Resolution Professionals

The article from LiveLaw (see below) discusses a judgment of the Delhi High Court holding that an Insolvency Resolution Professional (IRP) / Insolvency Professional (IP)does not qualify as a “public servant” within the meaning of Section 2(c) of the Prevention of Corruption Act, 1988 (PCA/PC Act).

Is An Insolvency Professional A ‘Public Servant’ Under The Prevention Of Corruption Act, 1988? VIEW HERE ⤡ (As reported on 22nd January, 2026 ©LiveLaw)

To diagnose why Insolvency Resolution Professionals (IRPs/RPs) appear to enjoy a peculiar immunity within India’s insolvency regime, it is necessary to examine the logico-legal reasoning that has shaped their contested status under the Prevention of Corruption Act, 1988 (PC Act). The divergence in judicial interpretation reveals not merely doctrinal disagreement, but a deeper structural incoherence at the intersection of insolvency law, financial regulation, and public accountability.

IA. Non-Applicability of the “Public Servant” Definition: The Delhi High Court’s Functionalist Reasoning

The Delhi High Court has held that an IRP does not fall within the definition of “public servant” under Section 2(c) of the PC Act. The Court’s reasoning proceeds on three interlinked grounds.

First, an IRP is not a person in the service or pay of the Government, nor does the role fall within any of the enumerated categories under Section 2(c)(i)–(viii) of the Act. The professional is neither appointed nor remunerated by the State, but engaged through a creditor-driven statutory process.

Second, although the appointment of an IRP/RP arises under the Insolvency and Bankruptcy Code, 2016 (IBC), and the role is subject to regulatory oversight by the Insolvency and Bankruptcy Board of India (IBBI) and adjudicatory supervision by the National Company Law Tribunal (NCLT), such regulation was held insufficient to transform a private professional role into a public office. Mere statutory origin or regulatory control, the Court reasoned, does not ipso facto confer public servant status.

Third, the Court emphasized that the IRP/RP functions as an independent professional—an officer of the process, not an agent, servant, or delegate of the Government. The exercise of powers under the IBC was characterized as fiduciary and quasi-judicial in nature, but not as the discharge of “public duty” in the sense contemplated by the PC Act.

On this basis, the Delhi High Court quashed proceedings under the PC Act against an IRP, holding that the threshold requirement of “public servant” status had not been satisfied. Consequently, prosecution under the PC Act was deemed legally untenable in such cases.

IB. Outcome and Immediate Implications

The immediate consequence of this interpretation is that IRPs/IPs fall outside the anti-corruption framework applicable to public officials. While disciplinary action may still lie under the IBC and IBBI regulations, the more stringent criminal scrutiny envisaged under the PC Act is rendered inapplicable. This effectively narrows the accountability horizon of insolvency professionals, even where allegations of bias, conflict of interest, or procedural manipulation are raised in relation to high-value insolvencies involving public funds.

Importantly, since the PC Act itself is held to be inapplicable, the question of prior sanction under Section 19 of the Act does not arise at all under this view.

IC. The Contrary Position: The Madras High Court’s Purposive Approach

In contrast, the Madras High Court, in a 2025 judgment, adopted a purposive interpretation of the PC Act. It held that Resolution Professionals qualify as “public servants” within the meaning of Section 2(c), given the nature and consequences of the powers they exercise under the IBC.

This reasoning foregrounds the fact that during the Corporate Insolvency Resolution Process (CIRP), an IRP/RP effectively displaces the board of directors, assumes control over the corporate debtor, administers assets that frequently include public deposits and bank funds, enforces the statutory moratorium, and facilitates CoC-led decision-making with wide distributive consequences. These functions, the Court held, amount to the exercise of public authority delegated by statute, rather than mere private professional services.

Under this approach, IRPs/RPs are brought within the ambit of the PC Act, but prosecution is made contingent on prior governmental sanction under Section 19—thus ostensibly safeguarding them from frivolous or vexatious proceedings.

ID. An Irreconcilable Tension and the Emergence of a Normative Vacuum

The coexistence of these two judicial approaches exposes a profound incommensurability within India’s legal architecture. On one horn of the dilemma lies the Delhi High Court’s functionalist classification, which risks transforming the IBC into a corruption-resistant enclave—where actors wielding extensive statutory power over public wealth remain insulated from criminal accountability under anti-corruption law. On the other horn stands the Madras High Court’s purposive reading, which, while recognizing the public character of insolvency powers, potentially subjects time-sensitive insolvency processes to executive gatekeeping through the sanction requirement, thereby threatening the IBC’s core objective of expeditious resolution and value maximization.

This tension is further aggravated by the overlapping yet poorly harmonized regulatory domains of the IBC, the RBI Act, 1934, and the supervisory jurisdiction of constitutional courts. The insolvency ecosystem thus oscillates between two undesirable outcomes: regulatory impunity on the one hand, and procedural paralysis on the other.

IE. Systemic Consequences and the Supreme Court’s Complicit Silence?

As of 2025, the Supreme Court’s persistent refusal to conclusively resolve this conflict has allowed doctrinal incoherence to harden into institutional practice. This is no longer a neutral absence of adjudication; it operates as a form of judicial acquiescence. By declining to settle whether Insolvency Resolution Professionals are public servants under the PC Act, the Court has effectively permitted a parallel legal zone to flourish—one in which enormous volumes of public money can be reorganized, transferred, and written off without the safeguards ordinarily demanded by anti-corruption law.

Nowhere is this more visible than in cases such as DHFL, where resolution administrators exercised sweeping statutory powers over public deposits and bank funds, yet allegations of bias, collusion, and valuation manipulation were never subjected to scrutiny under the Prevention of Corruption Act. The unmistakably public character of the funds involved did not translate into public accountability. Instead, silence at the apex level enabled procedural closure without substantive examination.

The consequence is a deliberate accountability vacuum. IRPs and RPs are strategically positioned outside both regimes of control: they are not treated as public servants answerable under anti-corruption law, nor are they regarded as private actors subject to transparency mechanisms such as the Right to Information Act. This legal no-man’s-land is not accidental—it is functional. It allows the Insolvency and Bankruptcy Code to operate as a sanitizing apparatus through which public assets are systematically stripped, discounted, and transferred to politically protected corporate cronies under the legitimizing language of “resolution,” “value maximization,” and “market efficiency.”

In effect, the IBC has ceased to be merely a bankruptcy framework. It has become a juridical technology that legalizes loot, converts mass financial injury into procedural compliance, and insulates those who profit from democratic and criminal accountability. The Supreme Court’s prolonged silence, in this context, does not merely sustain uncertainty; it stabilizes a regime in which crony capital thrives behind the façade of rule-bound insolvency governance.

II. Parallel Regimes of Immunity and Impunity: The Election Commission and the Committee of Creditors (CoC)

The accountability vacuum identified in the insolvency regime is not anomalous. It mirrors a broader legal–constitutional pattern in contemporary India, where statutory immunities and judicial deference increasingly converge to insulate powerful decision-making bodies from meaningful scrutiny. A revealing parallel can be drawn between the immunity accorded to the Election Commission of India (ECI) under the Chief Election Commissioner and Other Election Commissioners (Appointment, Conditions of Service and Term of Office) Act, 2023, and the protections—formal and informal—enjoyed by Committees of Creditors (CoC) under the Insolvency and Bankruptcy Code, 2016. In both domains, the language of “independence,” “good faith,” and “non-justiciability” operates to shield processes that directly determine the redistribution of political or economic power, even as allegations of massive manipulation persist.

IIA. Statutory Basis and Scope of Immunity / Protection

Election Commissioners / CEC / ECs (Election Commission of India, under CEC Act, 2023):

The CEC Act, 2023 (passed in December 2023) introduced a robust immunity clause: no civil or criminal proceedings shall lie against the CEC or any EC for any act done or omitted in good faith while exercising official functions (Section 15 or equivalent provision). This constitutes a blanket, lifelong immunity for acts performed in good faith during tenure, shielding them from lawsuits even after demitting office and extending post-tenure (post-retirement). The rationale is to insulate high constitutional functionaries from vexatious litigation that could impair the independent functioning of the Election Commission in a politically charged domain, where massive evidence-based allegations of BJP-ECI collusion in performing “vote chori” are surfacing over and over again, extended now through the process of citizen harassment in the form of SIR (another name for CAA and NRC!). It covers virtually all actions related to electoral management and was introduced amid criticisms of diluting judicial independence in EC appointments (replacing the CJI with a ministerial panel).

Current Challenge: A Public Interest Litigation (PIL) filed in late 2025/early 2026 challenges the constitutionality of this lifelong immunity clause. The Supreme Court (bench led by CJI Surya Kant) issued notices to the Centre and Election Commission on January 12–13, 2026, agreeing to examine whether this provision creates an unaccountable “law unto itself,” violates equality and the rule of law, and exceeds protections given even to the President, Prime Minister, or judges—potentially enabling electoral mismanagement without remedy. Key arguments highlight risks of unchecked power, such as suspicions of vote theft through systemic anomalies like large-scale additions at single addresses, duplicate registrations, fictitious entries, and targeted deletions of vulnerable groups (e.g., Dalits, Adivasis, migrants, women, and Muslim minorities) during processes like the 2025 Special Intensive Revision (SIR) of voter rolls. No interim stay has been granted, but the matter is actively pending, underscoring fears of placing ECs “beyond judicial scrutiny” and violating access to remedies.

RBI-Appointed CoC Members (under IBC, 2016):

Protection flows primarily from Section 233 of the IBC: “No suit, prosecution or other legal proceeding shall lie against the Government or any officer of the Government, or the Chairperson, Member, officer or other employee of the Board or any Insolvency Professional Agency or any Insolvency Professional or resolution professional for anything which is in good faith done or intended to be done under this Code or the rules or regulations made thereunder.” CoC members (typically bankers/financial creditors) are not explicitly named in Section 233, making protection indirect and ostensibly limited. However, courts have extended “good faith” immunity to CoC members in certain cases when acting collectively in the resolution process, rendering it far broader in practice than a narrow statutory shield.

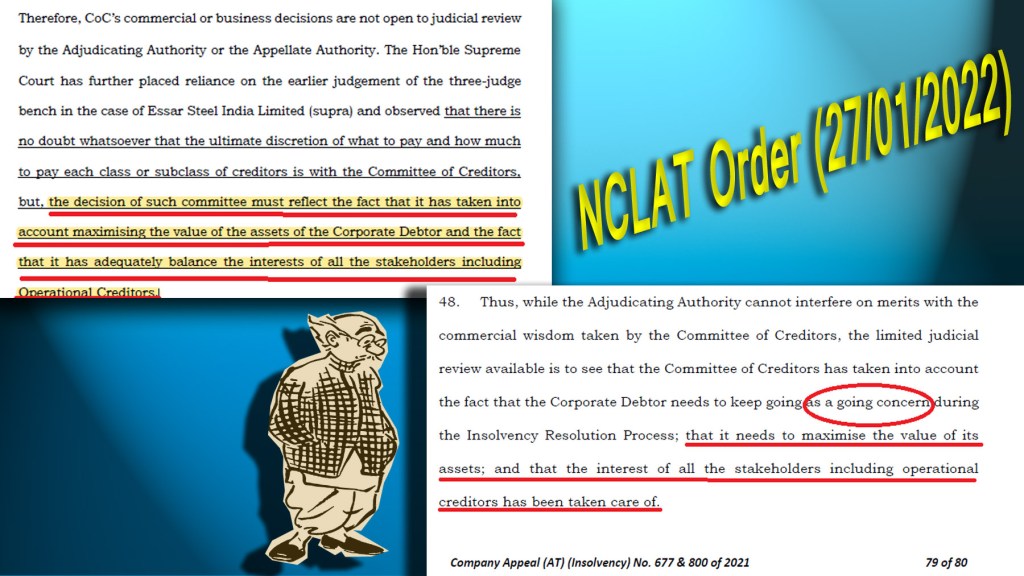

Additional safeguards exist via Section 30(6) (approval of resolution plans by CoC), but the true powerhouse is the judicial deference to the CoC’s “commercial wisdom” (e.g., upheld in Essar Steel, Committee of Creditors of Essar Steel India Ltd. v. Satish Kumar Gupta, 2019, and subsequent judgments like DHFL). This doctrine harshly positions CoC decisions as largely non-justiciable, granting them near-absolute immunity from civil suits or criminal prosecution unless blatant fraud is proven—effectively insulating them from accountability even in cases of bias, value destruction, or statutory violations.

Far from “limited,” this protection is process-specific yet expansive, not lifelong but enduring through appeals, and can be pierced only theoretically if bad faith, fraud, or ignoring NCLT orders is shown (e.g., regulatory action by IBBI or criminal proceedings without PCA sanction bars). In reality, the CoC enjoys god-like status under IBC: their “wisdom” is treated as sacrosanct, allowing them to override fair value assessments, suppress superior bids, and prioritize cronies with minimal scrutiny—turning insolvency into a “bankruptcy bazaar” where public money (via taxpayer-funded banks) fuels private profits. No equivalent blanket act exists, but the indirect extensions make CoC protections de facto robust, criticized for enabling cronyism without equivalent constitutional review.

The DHFL resolution offers a preliminary illustration—taken up in detail later as a case study—of how CoC decision-making under the IBC can replicate the logic of electoral vote manipulation. The CoC’s opaque handling of bids, including the preferential treatment of Ajay Piramal amid allegations of bias by rival bidders such as Oaktree Capital, the effective sidelining of settlement proposals supported by nearly 65% of fixed deposit and NCD holders, and the notional valuation of avoidance claims worth ₹45,000–47,000 crore at a token ₹1 for the acquirer, points to outcomes that appeared procedurally lawful yet substantively predetermined. The result was a mere 23% recovery for retail savers (₹1,241 crore against ₹5,375 crore in admitted claims), dispossessing approximately 2.5 lakh predominantly elderly depositors. The Supreme Court’s April 2025 ruling further insulated these outcomes by constricting appellate review under Section 61(3) of the IBC and directing recoveries to the successful acquirer without probing contemporaneous CBI findings that found no fraud by the original promoters. Read alongside broader IBC patterns—such as extreme haircuts in Videocon, Aircel, Essar Steel, Bhushan Power, and Reliance Communications—this episode signals a recurring structure in which avoidance provisions are neutralized, statutory creditor priorities diluted, and prolonged resolutions normalized, all to the disproportionate benefit of acquirers.

IIB. Scope and Nature of Protection

The following table summarizes the key aspects, highlighting the stark contrasts while emphasizing the CoC’s harshly critiqued overreach under “commercial wisdom,” which renders their protections anything but balanced—often allowing mala fide actions to masquerade as business judgment.

| Aspect | CEC / ECs (CEC Act, 2023) | RBI-Appointed CoC Members (IBC) |

|---|---|---|

| Type of Immunity | Blanket & lifelong (civil/criminal, good faith acts) | Limited “good faith” protection in statute, but expansively extended via “commercial wisdom” (civil/criminal, process-specific yet near-untouchable in practice) |

| Statutory Explicitness | Explicitly provided in the 2023 Act | Indirect via Section 233 (primarily for IPs/RPs); judicially extended to CoC, making it de facto broad and harshly deferential |

| Post-Tenure Protection | Continues for life | Ends with resolution process; no lifelong shield, but lingering effects through non-justiciable decisions |

| Good Faith Requirement | Yes, but broadly interpreted | Yes, but subject to stricter judicial scrutiny for mala fides—though rarely pierced due to “commercial wisdom” shield |

| Applicability to Acts | All official duties (very wide) | Limited to actions under IBC (e.g., voting on plans), but harshly applied to justify bias and value erosion |

| Protection from Suits | Near-absolute (challenged as unconstitutional) | Partial in theory; suits can proceed if bad faith/fraud proven, but “commercial wisdom” makes challenges ritualistic and futile |

IIC. Key Comparison Zones

Both frameworks rely on a “good faith” standard to safeguard official acts from frivolous suits, promoting independent functioning in regulated high-stakes arenas—ECI under constitutional election mandates (Article 324) and CoC within the IBC’s insolvency ecosystem. Judicial oversight is deferential: Courts show reluctance to probe ECI actions unless egregious, akin to the “hands-off” approach to CoC’s commercial wisdom (e.g., upheld in Essar Steel, 2019). Opacity plagues both, with non-downloadable CoC documents and redacted voter-roll data enabling evasion of transparency (e.g., RTI denials on CoC expenditures mirroring ECI’s non-disclosure of machine-readable logs). Institutional passivity further aligns them: Regulatory fragmentation (e.g., RBI/IBBI/CAG transfers for CoC) echoes ECI’s procedural latitude, subordinating civic oversight to crony gain and weaponizing data for exclusion or dispossession. They operate in domains sharing conceptual similarities as safeguards for official actions, designed to enable fearless decision-making yet raising concerns about abuse leading to autocracy (concentrated unchecked power) or oligarchy (crony tycoon control).

IID. Key Differences, Current Legal Challenges, and Judicial Scrutiny

- Breadth and Applicability: ECI immunity is absolute, post-tenure, and shields all official duties as constitutional functionaries, while CoC protection is ostensibly narrower and limited to IBC-specific actions for private creditors (banks), making it more commercial—yet in practice, “commercial wisdom” harshly elevates CoC to near-constitutional status, allowing unchecked dominance enabled by crony structures.

- Challenges and Scrutiny: ECI’s shield faces direct constitutional challenge in the 2026 Supreme Court case for risking unaccountability in electoral malpractices (no similar blanket challenge for CoC, though criticized in DHFL for cronyism). No blanket constitutional challenge exists for CoC, but courts have repeatedly upheld their wisdom as largely non-justiciable—harshly enabling bias without absolute immunity, yet invoking Section 233 to quash suits conditionally. If bad faith is shown (e.g., ignoring NCLT orders), CoC members face suits, IBBI action, or criminal proceedings, but this is rare due to deference.

- Manipulation Parallels and Accountability/Public Interest Differences: ECI’s alleged vote theft—through narrow re-verification timelines, missing logs, and exclusionary effects during SIR—directly parallels DHFL CoC’s voting manipulations, such as ignoring full debt repayment offers from promoters, circumventing NCLT orders (e.g., 19.05.2021), and prioritizing speed over fairness to gift DHFL to favoured tycoon Mr. Ajay Piramal. Election Commissioners enjoy stronger, statutory, post-tenure immunity for fearless decision-making, but critics argue it risks unaccountability in malpractices. CoC members have “weaker” conditional protection in theory, reflecting commercial insolvency, yet harshly enjoy expansive shields via commercial wisdom, remaining exposed only nominally—especially in DHFL bias allegations.

- Constitutional tension: ECI faces equality challenges; CoC relies on criticized but unstruck deference. Global parallels (e.g., Freedom House on democracy retreats, OSCE anti-corruption reports) note India’s decline in Corruption Perceptions Index (40 in 2022 to 38 in 2024) signaling erosion.

III. From Immunity to Impunity: Oligarchy–Oligopoly–Autocracy as a Single Regime (Il-)logic… Towards Kleptocracy??

What emerges from the convergence of the Election Commission of India’s (ECI) near-absolute immunity and the Insolvency and Bankruptcy Code’s (IBC) insulation of the Committee of Creditors (CoC) is neither accidental nor episodic. It reflects a carefully stabilized regime logic in which legal protection mutates into technical impunity—a condition where power operates entirely within formal legality while being functionally unreachable by accountability. This is not a breakdown of law, but its strategic redeployment to serve entrenched, vested interests. The result is a tightly coupled formation in which oligarchy (concentrated decision-making), oligopoly (concentrated markets), and autocracy (hollowed democratic choice) reinforce one another through mutually enabling institutional designs. This is what has become of India under the BJP regime!

IIIA. From Oligarchy to Oligopoly: Structuring the Economy for the Few

Under the rhetoric of “resolution” and “value maximization,” the IBC has increasingly functioned as a mechanism for large-scale asset redistribution upward. The DHFL resolution exemplifies this dynamic. In the 2021 insolvency, avoidance claims conservatively valued at ₹45,000–47,000 crore were transferred to the successful acquirer for a notional ₹1, while approximately 2.5 lakh largely elderly fixed-deposit holders were left with recoveries of roughly 23% of their admitted claims. This outcome was ultimately endorsed by the Supreme Court in April 2025, despite persistent allegations of procedural opacity, bidder preference, and the sidelining of settlement proposals supported by a majority of retail stakeholders.

This case is not an outlier. Across major insolvencies—Videocon (95–96% haircut), Aircel (≈89%), Essar Steel, Bhushan Power, Reliance Communications—the pattern is consistent: public-sector banks absorb steep losses, statutory and public-interest claims are diluted, and distressed assets are consolidated by a narrow group of corporate actors. The doctrine of “commercial wisdom,” crystallized in Essar Steel (2019) and repeatedly reaffirmed, functions as the legal hinge enabling this outcome. Oversight mechanisms remain formally present but substantively weak: regulatory responses are limited, RTI access is routinely denied, and appellate scrutiny is sharply curtailed.

What results is not competitive capitalism but oligopolistic consolidation—markets dominated by a small constellation of corporate groups with recurrent access to distressed assets across infrastructure, energy, finance, telecom, ports, airports, and housing finance. Oligarchy thus translates seamlessly into oligopoly, with law acting as the transmission mechanism.

IIIB. From Oligopoly to Autocracy: Political Insulation and Electoral Asymmetry

Oligopolistic concentration does not sustain itself without political insulation. This is where the parallel with electoral governance becomes decisive. The 2023 legislation conferring expansive immunity on the Chief Election Commissioner and Election Commissioners—now under constitutional scrutiny following the Supreme Court’s January 2026 notices—creates a zone of exceptional insulation in the very institution responsible for safeguarding electoral fairness.

This immunity has coincided with profound distortions in political finance and electoral administration. The now-invalidated electoral bonds scheme revealed a dramatic skew in political funding, with the ruling party receiving a disproportionate share of corporate donations, rising from approximately ₹780 crore in 2014 to nearly ₹9,000 crore by 2024. Corporate donors—some of whom simultaneously benefited from regulatory forbearance, major acquisitions, or insolvency outcomes—operated within an opaque, non-reviewable funding architecture until the scheme was struck down in February 2024.

The broader consequence is a drift toward electoral autocracy: elections continue to be held, but the conditions of competition are increasingly asymmetric. Allegations surrounding voter roll revisions, mass deletions, compressed verification timelines, missing audit trails, and denied RTI access—such as those raised during the 2025 Special Intensive Revision exercises—underscore how procedural legality can coexist with substantive disenfranchisement. In such a setting, electoral outcomes may remain formally valid while being structurally tilted.

IIIC. Depositors and “Dubious Citizens”: Parallel Disenfranchisements

A striking symmetry links the insolvency and electoral domains. In the IBC framework, depositors and small creditors are formally recognized but effectively disenfranchised. They possess no meaningful voting power within the CoC, face severe information asymmetries, and encounter irreversible outcomes once resolutions are approved. Their participation is nominal; their losses are real.

A parallel logic operates in the political sphere. Citizens subjected to voter roll purges, heightened surveillance, selective enforcement, or narrative delegitimization are not excluded outright but rendered electorally marginal. They remain on the rolls—sometimes—but their capacity to influence outcomes is diminished. In both cases, legitimacy is preserved through form, while justice is withdrawn in substance.

IIID. Immunity as Technical Impunity: When Compliance Becomes the Cover

The defining feature of this regime is that impunity is achieved not through illegality but through compliance. Election Commissioners enjoy statutory shields extending even beyond tenure. Insolvency actors benefit from doctrinal protections: “good faith,” non-justiciability of commercial wisdom, and tightly circumscribed appellate review under Section 61(3) of the IBC. Anti-corruption statutes, transparency laws, and equitable doctrines are rendered either formally inapplicable or practically ineffective.

No single law is openly violated. Instead, accountability collapses because institutions operate exactly as designed. Immunity, in this sense, does not merely protect—it produces impunity. Here, “impunity” does not denote the absence of law, but the presence of a legal order so architected that power can act with formal legality while remaining structurally insulated from accountability, consequence, and redress.

IIIE. India’s Rising Impunity Index: Structural Markers of a Failed State

Even without a formal metric, the indicators of a rising impunity index are unmistakable:

- Concentration of economic power aligned with political dominance

- Oversight institutions increasingly deferential or ineffective

- Expanding zones of non-reviewability

- Procedural compliance substituting substantive justice

- Large-scale social harm without corresponding institutional consequence

The IBC and the ECI are not aberrations in this landscape; they are emblematic institutions of it—efficient, decisive, insulated, and structurally unanswerable.

IIIF. Beyond Corruption: A Structural Crisis of “Constitutional Capitalism” (?)

What is at stake, therefore, is not corruption in its conventional sense but a deeper structural crisis of constitutional capitalism. Law no longer constrains power; it refines and legitimizes it. Markets no longer discipline accumulation; they accelerate concentration. Democracy no longer distributes voice; it manages consent.

In this configuration, oligarchy determines outcomes, oligopoly controls assets, and autocracy stabilizes rule. These are no longer separable tendencies but a single, hyphenated regime logic. Immunity supplies its grammar. Impunity secures its endurance.ble shitshow. Wake up, India: this regime isn’t broken—it’s built to break you.

IV. Can These Regimes of Protection Be Morally Defended?

From a normative standpoint, limited institutional protections are not intrinsically immoral. In principle, narrowly tailored immunity can be justified to prevent decision-makers from being paralysed by intimidation, frivolous litigation, or political retaliation. This justification applies most plausibly to election administration in volatile contexts and to insolvency resolution involving complex, high-value commercial judgments.

IVA. Limited Moral Defensibility in Principle

From a Kantian perspective, a good-faith shield may be defensible insofar as it enables officials to discharge duties impartially, without acting under fear or coercion. Such protection treats institutional actors as moral agents capable of reasoned judgment rather than as instruments of political pressure. Similarly, a utilitarian calculus can support constrained immunity where it demonstrably secures systemic stability—credible elections or timely insolvency resolution—thereby preventing broader social harm.

Under this narrow framing, some degree of protection for Election Commissioners and insolvency actors can be morally intelligible.

IVB. Moral Collapse in Practice: From Protection to Impunity

However, the moral justification collapses when protection ceases to be conditional and becomes structural insulation from accountability. When immunity produces impunity—particularly in systems marked by asymmetrical power—it violates core principles of justice, equality, and public trust.

In the insolvency context, this collapse is acute. The IBC’s doctrinal architecture—especially the expansive deference to CoC “commercial wisdom”—has facilitated outcomes that systematically harm the most vulnerable stakeholders. The destitution of DHFL depositors, the sidelining of public-interest claims, and the neutralization of avoidance provisions reveal a regime that prioritizes speed and finality over fairness. The internal contradictions of the Code—most starkly between Section 66 (fraudulent trading) and Section 32A (immunity for new management)—institutionalize moral hazard by shielding beneficiaries of distressed acquisitions from accountability even where serious irregularities are alleged.

From a Rawlsian standpoint, such a system fails the test of justice under the veil of ignorance. It entrenches structural inequalities, concentrates advantage among already powerful actors, and systematically disadvantages those with the least capacity to contest outcomes. Procedural legality is preserved, but substantive justice is abandoned.

IVC. The Illusion of Balance

While the ECI’s immunity regime is formally broader and now under direct constitutional scrutiny, the IBC’s protections—though narrower on paper—have proven more corrosive in effect. Nominal oversight mechanisms exist, but in practice they function as ritual affirmations rather than effective checks. The language of balance and efficiency masks a persistent tilt toward corporate consolidation and capitalist appropriation.

Moral defensibility, therefore, cannot rest on intent or formal design alone. It requires active counterweights: time-bound and reviewable immunity, transparency obligations, meaningful appellate scrutiny, and genuine inclusion of affected stakeholders. These conditions are conspicuously absent in the current insolvency regime.

IVD. Democratic Implications

Absent such safeguards, continued reliance on these protection regimes risks moral bankruptcy. Law becomes an instrument for insulating concentrated power-wealth dynamics rather than disciplining it; democracy is reduced to managed procedure; and economic governance normalizes dispossession as efficiency. Reform is therefore not optional but ethically imperative—whether through radical restructuring of the IBC, recalibration of judicial deference, or reassertion of constitutional principles of equality and accountability.

V. Global Parallels: Immunity as the Keystone of Impunity Regimes Worldwide

Building on India’s impunity machine—where ECI shields rig electoral facades and IBC insulations fuel asset grabs—the global landscape reveals a chilling pattern: protections for election officials and insolvency actors aren’t neutral safeguards; they’re weapons in the arsenal of crony oligarchical capture. Even so-called democracies like the USA, often cloaked in (neo-)liberal rhetoric, deploy qualified immunities that mask authoritarian undercurrents and neo-imperialist agendas, correlating with inflated CPI scores propped up by selective antitrust (e.g., EU’s Google fines vs. USA’s revolving-door lobbying for Big Tech). This layers a facade of accountability: “good faith” becomes a rubber stamp for power, enabling “technical impunity” that India mirrors but the USA exports globally via interventions in Venezuela (Trump-era neo-imperial grabs) or Iraq (Bush’s hegemonic destabilization), fusing state-corporate might in a crony vortex.

In stark alignment, overt authoritarians (China/Russia) and seemingly covert (?!) ones (USA) wield absolute or quasi-absolute protections as loyalty enforcers—USA’s qualified shields for FEC officials (pierceable only theoretically via Bivens suits) echo China’s CCP-tied immunities, both perpetuating capitalist independence at the expense of masses. Here, immunities don’t protect democracy; they entrench neo-imperialism, vaporizing public assets (Russia’s oligarch seizures parallel IBC haircuts and USA’s post-9/11 military-industrial plunders) while eroding trust (CPI plunges signal institutional rot, with USA’s 28th/65 rank hiding domestic authoritarianism like mass surveillance and migrant crackdowns). Critiques abound: from Project Syndicate decrying Trumpian greed as unprincipled imperialism to Monthly Review blasting MAGA’s reactionary strategy, USA’s “democratic” veneer crumbles under scrutiny as a neo-imperial beast, sustaining oligarchy through endless wars and corporate bailouts that rival China’s state-crony fusion or Russia’s Kremlin-aligned loot.

VA. Key Concepts in Global Context

- ECs Immunity: Guards electoral overseers but overbroad versions enable partisan manipulations, fostering “electoral autocracy” (V-Dem) in USA’s gerrymandered polls as much as Russia’s rigged votes.

- IPs/RPs/CoC Protection: Shields insolvency handlers, yet doctrines like USA’s Barton quasi-judicial immunity or India’s “commercial wisdom” mask favouritism toward cronies, accelerating oligopoly.

- Systemic Trends: “Qualified” immunities in USA/UK/EU serve neo-imperial ends (e.g., USA’s global hegemony via IMF/World Bank strings); absolutes in China/Russia overtly bind loyalty. Emerging markets (Brazil/South Korea) post-reform tilt toward balance, but USA’s influence often undermines them through coups or “aid” (e.g., Brazil’s Lava Jato ties to US-led imperialism).

VB. Comparative Table

| Country | Election Commissioners Immunity | Insolvency Professionals / CoC Protection | Key Similarities/Differences with India | CPI Rank/Score (2024) & Implications |

|---|---|---|---|---|

| India | Broad, lifelong “good faith” shield (CEC Act, 2023, §15); SC challenge (Jan 2026) flags unaccountability. | Conditional “good faith” (IBC §233); CoC deference but pierceable for fraud (e.g., DHFL cronyism). | N/A | 96th / 38; Deep cronyism via BJP-conglomerate nexus, echoing USA’s military-industrial complex. |

| USA | FEC officials qualified immunity (Sovereign Act); suits rare amid neo-imperial overreach (e.g., Trump v. US 2024 curbs but enables authoritarianism). | Trustees shielded by Barton doctrine; limited liability for good faith (11 U.S.C. §326); CoC reasonable or challengeable, but lobbying shields capitalists. | Narrower facade, but USA’s neo-imperialism (Venezuela interventions, Iraq war) parallels India’s regulatory capture—stronger antitrust myth hides oligopoly. | 28th / 65; Inflated score masks authoritarianism (surveillance state, migrant abuses); critiques (Nation, Project Syndicate) expose greed-driven imperialism. |

| UK | Electoral staff under Crown immunity; open to review but tied to post-colonial legacies. | IPs immune unless negligent (Insolvency Act 1986); CoC challengeable via probes. | “Good faith” akin, but UK’s oversight edges India’s; still enables City of London cronyism. | 20th / 71; Anti-corruption facade; complicit in USA-led neo-imperial ventures. |

| Germany (EU exemplar) | Qualified immunity for Returning Officer; ECJ-contestable, but EU’s antitrust vigor selective. | IPs liable for negligence (InsO §60); CoC reviewable (Directive 2019/1023). | Balanced creditor rights; EU’s fines curb oligopoly better than India’s meek CCI, but aligns with USA neo-imperialism via NATO. | 15th / 75; Rule-of-law strong, yet complicit in global cronyism. |

| China | NPC officials absolute immunity via CCP; challenges quashed. | IPs under state control; protections for Party-aligned (Bankruptcy Law). | Broader authoritarian shields mirror USA’s effective impunity in global grabs. | 76th / 43; State-crony fusion rivals USA’s corporate-imperial axis. |

| Russia | Strong federal protections; stifled by state-oligarch control. | IPs immune unless criminal (Law 127-FZ); favors Kremlin tycoons. | Crony favouritism like India’s; USA’s sanctions hypocrisy highlights shared neo-imperial traits. | 154th / 22; Overt oligarchy; parallels USA’s hidden authoritarianism (Guardian critiques). |

| Brazil | TSE justices qualified; impeachable post-Lava Jato. | IPs good-faith (Law 11.101/2005); CoC challengeable. | Scandal reforms curb cronyism more than India; US-led imperialism roots (Taylor & Francis) echo global coups. | 107th / 34; Politics-business rot; offers India reform path amid USA interference. |

| South Korea | Immune except treason; courts pierce post-chaebol. | IPs liable for negligence; CoC scrutinized. | Narrower than India; anti-chaebol reduces oligopoly—USA’s influence via alliances tempers. | 30th / 64; Declining cronyism; highlights need for India/USA to dismantle crony-monopoly-duopoly shields. |

VC. Broader Insights, Trends, and Systemic Critique

Globally, immunities architect regimes: USA’s “qualified” shields, critiqued as neo-imperialist (CADTM on Trump fascism, MR Online on crisis imperialism), enable authoritarianism under democratic guise—fusing corporate power (Big Tech bailouts) with global dominance (Venezuela coups, endless wars). This “new MAGA imperialism” (Monthly Review) vaporizes assets abroad while eroding domestic trust, with CPI masking rot via lobbying (Nation on Miller’s authoritarianism).

Authoritarians like China/Russia overtly deploy absolutes for state-oligarch loyalty, but USA’s covert version—through hegemonic legitimacy (MDPI on Bush neo-imperialism)—achieves similar crony vortexes, perpetuating cronies (OUP on empire denialism). Emerging parallels: Brazil/Korea’s reforms pierce immunities, lifting CPI by curbing US-backed coups (anti-imperial perspectives). India, aping USA’s hybrid, risks their abyss: ECI’s “vote theft” mirrors USA’s voter suppression, IBC’s haircuts echo imperial plunders.

In sum, India’s ECI/IBC immunities align with global cronyism—broader than democracies’ qualifiers yet nearing authoritarians’ absolutes. USA’s neo-imperial authoritarianism proves no exception: excessive shields spike corruption, demanding reforms like pierceable protections and antitrust fangs. Absent that, trends warn: impunity’s grammar scripts autocratic empires, with India and USA co-authoring decline.

VI. DHFL Scam Scenario – A Case-Study Indictment: Connecting IBC’s Structural Critique to CoC Malfeasance and Systemic Crony Plunder

Extending the global indictment of immunity regimes as architects of capitalist impunity—where even the USA’s neo-imperial façade barely conceals oligarchic capture—India’s Insolvency and Bankruptcy Code (IBC), 2016 stands exposed as a predatory architecture of legalized dispossession. Nowhere is this more grotesquely visible than in the Dewan Housing Finance Corporation Limited (DHFL) resolution, cynically projected as a “test case” to legitimize the IBC but in practice transformed into a laboratory of institutionalized loot. The RBI-appointed Committee of Creditors (CoC) did not resolve insolvency; it orchestrated a transfer of public wealth, stripping nearly 2.5 lakh predominantly elderly depositors of their life savings while handing over a solvent, AAA-rated NBFC—with assets exceeding ₹90,000 crore—to crony bidder Ajay Piramal at a fire-sale discount. DHFL thus condenses every structural pathology of the IBC: fraud laundering via Section 32A, extreme haircuts averaging 67–68%, chronic delays (with over 77% of cases breaching the 270-day limit), regulatory capture by the RBI and IBBI, judicial ritualism that fetishizes “commercial wisdom,” and a crony nexus intertwining political patronage, Electoral Bonds, PM CARES contributions, and asset appropriation. This is not institutional failure but institutional design—political capitalism hollowing out democratic accountability.

Drawing on our curated activist archive, the articles from our very own Once In A Blue Moon Academia thoroughly chronicle this unfolding scam from early procedural “rat-smelling” in 2021 to damning exposés culminating in 2025. They document ignored full-repayment offers, suppressed evidence of fraud, opaque CoC conduct, premature occupation of assets, and BJP-enabled favouritism, while consistently demanding accountability from RBI-appointed administrators, CoC members, and insolvency professionals—including fee refunds and public-servant scrutiny. Analytically, these interventions situate DHFL within a broader political-economic arc: from demonetization-era financial frauds to post-pandemic plunder, exposing the IBC as an ill-conceived regime of structured expropriation where CoC “kings” rule without liability and public money is alchemized into private empires. Mirroring wider institutional failures—from electoral capture to judicial deference—the DHFL case exemplifies how regulatory-judicial pliancy underwrites depositor dispossession, crony enrichment, India’s worrying position in the global corruption index, and the systematic erosion of constitutional democracy, ultimately strengthening the call not for reform but for the dismantling of the IBC’s crony-capitalist architecture itself.

VIA. Chronological Sequence of Our Activist Exposés: From Early Suspicions to Culminating Heists

Taken together, our activist interventions form a cumulative evidentiary chain rather than isolated critiques. Beginning in 2021 with foundational suspicions regarding CoC opacity and structural bias, the writings progressively escalated into explicit demands for probes, fee disgorgement, and institutional accountability through 2022–2023. By 2024, the focus sharpened into ironic and sarcastic exposure of post-resolution career rewards, revealing how insolvency administration functioned as a revolving door rather than a public duty. The 2025 analyses mark the culmination of this trajectory, identifying premature occupation of DHFL assets as the irreversible moment that converts procedural irregularity into completed expropriation—proof that the process was never corrective but extractive.

This progression systematically widens the analytical lens: from discrete CoC malfeasance to the IBC’s structural pathologies, and from case-specific violations to regime-level normalization of corruption. Regulatory capture, judicial inconsistency masked as deference to “commercial wisdom,” RTI suppression, and India’s declining Corruption Perceptions Index are not treated as parallel failures but as mutually reinforcing symptoms of an entrenched extractive political economy. Read sequentially, the articles demonstrate how early “rat-smelling” in rigged procedures evolves—through ignored legal directives and engineered exclusions—into irreversible asset transfers that consolidate crony-nepo-capitalism as governance itself.

VIB.1. Early Red Flags: Smelling the Rat in the DHFL-CoC Resolution Process (March 24, 2021; Updated July 30, 2024)

The DHFL debacle’s stench first wafted in this blistering letter to the President of India, unmasking the RBI-appointed CoC as a cabal of opacity and bias from day one. Posted amid the pandemic’s peak, it accuses the CoC—led by administrator R. Subramaniakumar and Authorized Representative (AR) Charu Sandeep Desai—of engineering a “transparently opaque” process rigged for crony handover.

Key allegations zero in on Piramal Group’s involvement, tainted by prior DHFL ties and alleged political favouritism as the father of Mukesh Ambani’s son-in-law (Anand Piramal married Isha Ambani in 2018), positioning him as the regime’s “damad” beneficiary. The letter blasts the premeditated reverse merger of DHFL to Piramal’s non-listed entity, swallowing a solvent company at a discount while siphoning public funds—echoing Cobrapost’s January 29, 2019, exposé of DHFL promoters’ Rs 31,000 crore diversion to shell companies, allegedly benefiting BJP via electoral bonds.

Critiques savage IBC’s flaws: its incommensurability with NHB Acts, repeated amendments (2018 and proposed), and failure as a “speedy one-stop solution” amid rampant bankruptcies. The CoC’s secrecy is eviscerated—resolution plans and minutes accessible only as non-downloadable images, denying FD holders transparency despite repeated queries (three emails, one WhatsApp, webinar ignored by Desai). Misconduct allegations include Desai’s premature leaks of minutes to privileged non-FD holders (via dhflarforfd@gmail.com), violating All India Services (Conduct) Rules, 1968, Rule 9.

Timelines highlight foreknowledge: Piramal’s January 28, 2019, prediction of NBFC “shocks” just before Cobrapost’s reveal, suggesting insider trading amid vigilant agencies’ “failure.” Demands thunder for intervention: public display of plans to RBI Governor Shaktikanta Das (labeled “highly corrupt” by Subramanian Swamy’s February 2, 2021, PIL), removal of Subramaniakumar and Desai, scrapping the CoC, and Das’s resignation.

Politico-economically, this sets the stage for cronyism’s playbook—demonetization’s black money purge a sham, elections an “auction” via bonds, judiciary a rubber stamp—foreshadowing IBC’s role in asset redistribution to “more equal” selected few, as per Orwell’s Animal Farm. Broader implications decry India as an “electoral autocracy” (Swedish Institute, March 11, 2021) and “partly free” (Freedom House, March 3, 2021), with asset gaps (book value Rs 93,700 crore, fraud Rs 33,000 crore, bid Rs 32,250 crore, unaccounted Rs 28,450 crore) screaming organized loot: financial creditors lose Rs 55,000 crore, shareholders Rs 6,300 crore, while advisors pocket Rs 130 crore.

This early piece establishes the foundational suspicions of manipulation, logically leading to subsequent symbolic burials and demands for reckoning as the CoC’s biases become increasingly evident in rejected offers and ignored judicial directives.

VIB.2 Symbolic Burial: Compose an Obituary for the RBI-Appointed CoC for DHFL (June 2, 2021; Updated July 30, 2024)

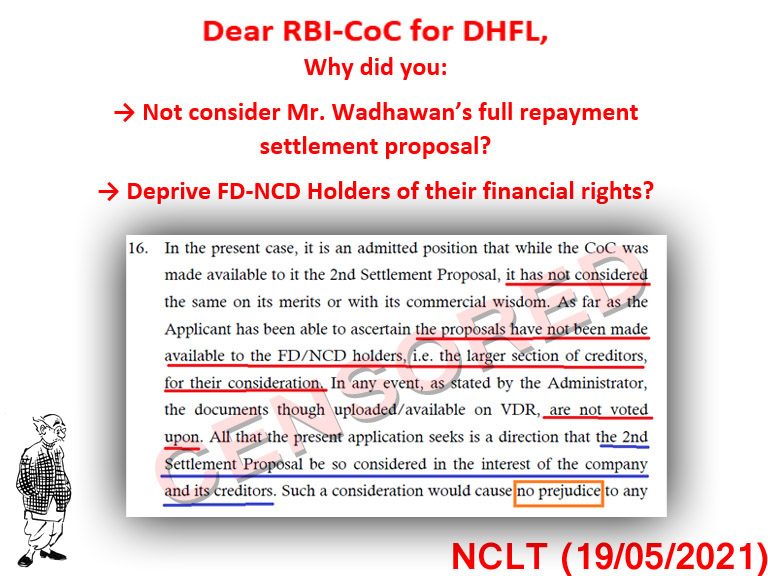

Building directly on the “rat-smelling” suspicions of opacity and crony favouritism, this savage obituary-letter to the President buries the CoC as a corpse of ethical governance, its “death” symbolizing IBC’s fatal flaws in the DHFL charade. Allegations escalate: the CoC, initiated December 3, 2019, after RBI superseded DHFL’s board on November 20, 2019, for “inadequate governance,” rejected Kapil Wadhawan’s 100% repayment offer (reiterated December 14, 2020) despite its 150% superiority, opting for Piramal’s 75% discount reverse-merger—a “throw-away sale” of a solvent entity with Rs 16,000 crore cash, Rs 30,000 crore retail assets, and monthly Rs 500 crore lending.

The letter accuses CoC of over 60% haircuts, ignoring NCLT’s May 19, 2021, order to reconsider Wadhawan’s proposal (stayed by NCLAT on May 25, 2021, with missing dates post-signatures), and traumatic communications from Desai via Catalyst Trusteeship (52.13% voting power despite FD/NCD’s 65% share per NCLT points 69, 87).

Critiques flay IBC’s incommensurability with RBI/Company/NHB Acts, 21,250+ pending NCLT cases (December 2020), and 280+ bankruptcies amid pandemic (March 2021), correlating with ruling party’s asset surge sans production. CoC misconduct: 19 meetings (December 3, 2019–January 17, 2021) during lockdown, rejecting Wadhawan’s offer, approving Piramal over Adani/Oaktree despite bias allegations (Oaktree mulls suit, December 3, 2021).

RBI’s blind approval (February 18, 2021) and Das’s “frightening” governance (Abhijit Banerjee, December 11, 2018) are lambasted, alongside judiciary’s rot (Ex-CJI Ranjan Gogoi: “ramshackled”; Mukul Rohatgi: “jail as rule”). Timelines underscore contradictions: Bombay HC proved DHFL solvent (Rs 800 crore monthly securitization), yet RBI declared insolvency; Grant Thornton audit (February 22, 2021) unearthed frauds, but Supreme Court (May 22, 2021) upheld personal guarantees not voided.

Demands include composing (symbolically) CoC obituary, scrap IBC, remove Subramaniakumar/Desai, scrap CoC, Das resign, appoint retired bankers for 100% recovery with compensation for human rights violations. Politico-economically, this pivots to crony monopoly: Piyush Goyal-Piramal nexus, Dawood-Mirchi-RKW-DHFL-BJP collusion (Congress alleges Rs 20 crore BJP receipt for Rs 31,000 crore favor), under IPC Sections 107/201/505, POTA/TADA.

Broader implications include plutocratic regime’s “looting with fair means,” saffron fascism, depopulation via anxiety, pharmaceutical GDP from stress—resistance against autocracy essential. This symbolic burial extends the early red flags by dramatizing the ethical collapse, paving the way for subsequent fee refund demands as the legal irregularities (e.g., ignored NCLT orders) accumulate into grounds for financial reckoning and probes.

VIB.3 Fee Refunds as Reckoning: Requesting Return of Fees from the Administrator and Representatives (March 8, 2022; Updated August 1, 2024)

Chronologically advancing the activist assault from symbolic condemnations to tangible demands, this demand-letter to the CoC hammers their “contrary to law” conduct (NCLAT January 27, 2022) as grounds for fee forfeiture, framing DHFL as IBC’s inaugural disaster. Allegations: Subramaniakumar and Desai inflicted mental/financial harassment on victims during pandemic, swallowing their “hard-earned money” while process deemed unlawful.

Quora post accuses Desai of indefinite postponements, consuming Rs 7 lakhs/month without aiding FD recovery. Timelines: NCLT May 19, 2021, order (bad precedent per lenders’ May 26, 2021, appeal); NCLAT stay; process “ridiculously idiotic.”

Critiques eviscerate lenders’ logic as “irrational,” CoC lacking moral right to fees. Demands: full fee return, scrap IBC, penalize administrators, scrap CoC, Das resign. Politico-economically, ties to saffron fascism, autocracy resistance; analytically, IBC’s experimental nature sets “bad precedent,” with CBI arresting IRP for Rs 2 lakh bribe (May 5, 2022) underscoring corruption.

Broader: miscalculation of FD percentages (23.08% surrender vs. maturity value), human rights infringement. This reckoning logically follows from the prior exposures of misconduct, transforming ethical critiques into financial accountability claims, and sets the stage for escalating probes into corruption as the NCLAT’s illegality verdict provides evidentiary leverage for agency interventions.

VIB.4 Escalating Probes: Seeking Intervention on CoC Misconducts—Letters to CVC, CBI, ED, NIA (November 6, 2022)

This investigative salvo petitions anti-corruption agencies, chronologically amplifying prior demands with forensic timelines of DHFL’s plunder. Allegations: Cobrapost’s January 29, 2019, expose of Rs 31,000 crore siphoning, BJP-terror links via Dawood-Mirchi-RKW; Piramal’s January 28, 2019, prediction as insider trading; deceptive AAA ratings post-allegations; CBI’s March 24, 2021, suit on 260,000 fake accounts siphoning PMAY subsidy; ED’s April 23, 2022, Rs 5,050 crore diversion; BJP’s June 25, 2022, Rs 27.5 crore DHFL donations.

CoC rejected Wadhawan’s 100% offer (December 14, 2020), approved Piramal (avoiding Oaktree bias claims, December 3, 2021), disbursed 23% FDs (September 2021) with haircuts; NCLAT January 27, 2022, declared illegality; Piramal acquired via dubious names despite sub judice.

Critiques: IBC amended 34 times, unsustainable haircuts (Parliamentary Committee August 3, 2021, on 13,000 cases/Rs 9 lakh crore); CoC bias, ignoring NCLT May 19, 2021, order (stayed May 25, 2021). Demands: inquiry into misconduct, Das expulsion. Politico-economically: demonetization sham, opaque bonds/PM CARES as terror-funding; RBI incompetence (August 11, 2022, appointments).

Broader: human rights via financial abuse, executive control of pillars. Building on the fee refund demands, this escalation integrates legal verdicts like NCLAT’s illegality findings into calls for multi-agency probes, extending the critique from internal CoC failures to systemic collusions involving political donations and terror-funding networks, thereby broadening the horizon to national anti-corruption frameworks.

VIB.5 Public Servant Scrutiny: An Open Letter to Two Public Servants—Subramaniakumar and Desai (July 23, 2023; Updated July 25, 2023)

Analytically dissecting CoC as “public servants” under PCA Section 2(c) and IBC Section 233 (no bribery shield), this letter condemns their role in ignoring Wadhawan’s full repayment pleas for Piramal handover—a “wedding gift” via Ambani-BJP collusion. Allegations: ignored NCLT May 19, 2021, order (revoked NCLAT May 25, 2021); NCLT approved Piramal June 7, 2021; acquired September 2021 despite NCLAT January 27, 2022, illegality; Supreme Court stay April 11, 2022; Section 29A controversially barred Wadhawans despite NCLAT entitlements; Section 32A misused for liability shield; unproved Wadhawan crimes, yet Rs 27.5 crore BJP donations.

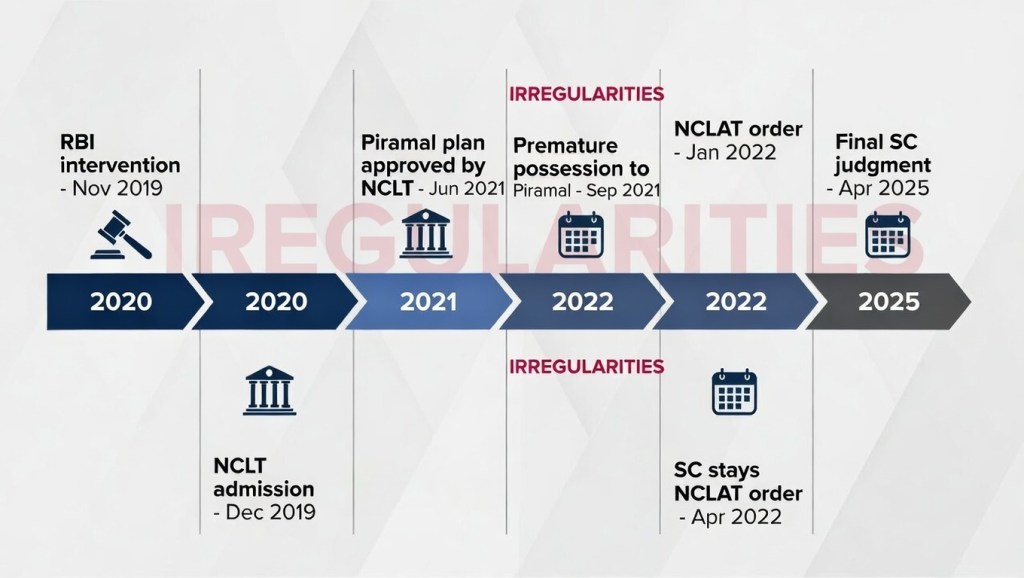

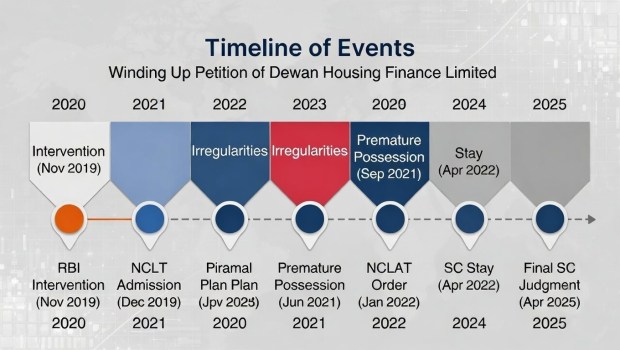

Horizontal timeline infographic 2020–2025 showing key dates: RBI intervention (Nov 2019), NCLT admission (Dec 2019), Piramal plan approval (Jun 2021), premature possession (Sep 2021), NCLAT order (Jan 2022), SC stay (Apr 2022), final SC judgment (Apr 2025). Color-code irregularities in orange

Critiques: IBC ill-conceived, experimental (amended 4+ years); NCLT rubber-stamp; CoC “wis(h)dom” infallible for politico-legal aid. Demands: full refund with interest/compensation from Rs 45,000 crore assets; fee return; Das expulsion; probes via CVC/CBI/ED/NIA/SFIO/Lokpal. Politico-economically: crony-nepo capitalism, political vendetta; saffron fascism. Broader: inequality (“more equal”), autocracy resistance.

This letter explicitly addresses R. Subramaniakumar (RBI-appointed Administrator heading the CoC for DHFL) and Charu Sandeep Desai (Authorized Representative for FD-NCD holders) as “public servants” under Section 2(c) of the Prevention of Corruption Act, 1988, and Section 233 of the IBC (noting limited immunity). It accuses them of enabling an illegal, manipulated process: ignoring NCLT’s 19/05/2021 order to reconsider Kapil Wadhawan’s 100% repayment proposal, rushing to NCLAT for stays, overlooking Section 66 (fraudulent trading avoidance), misusing Section 29A to bar promoters, and facilitating Piramal’s “hostile” takeover at steep discount while privatizing massive avoidance recoveries.

This ties directly to our discussions on CoC as unchecked “king,” fraud laundering, judicial ritualism, and DHFL as proof of IBC pathologies (solvent entity looted, depositors dispossessed). The letter demands fee returns, full repayment/compensation, and intervention by CVC/CBI/ED/NIA/SFIO — echoing calls for scrapping IBC and seizing cronies, as seen in demands for probes and refunds amid CoC’s “malicious intent.”

Extending the probe escalations, this scrutiny reframes CoC figures as accountable public servants, deepening the critique by invoking PCA liabilities and linking to judicial divergences (e.g., Delhi vs. Madras High Court rulings on public servant status), creating jurisdictional uncertainties that allow IPs in crony-favored resolutions like DHFL to evade scrutiny, perpetuating moral hazard.

VIB.6 Fraudulent Oversights: IBC Section 66 Overlooked by DHFL-CoC—A Big Conspiracy? (April 23, 2023)

Critically analyzing Section 66 neglect, this exposes CoC’s “malicious intent” in depriving depositors for Piramal’s gain. Allegations: NCLAT January 27, 2022, ruled irregularities/void process; Parliamentary Committee August 2021 rapped unsustainable haircuts (13,000 cases/Rs 9 lakh crore); unproved Wadhawan crimes (Supreme Court bail March 27, 2023); Dawood-Mirchi-BJP collusion.

Critiques: IBC incommensurable with PMLA; CoC conspiracy, non-wilful absences. Demands: fee return, Supreme Court suo moto, stop Piramal acquisition. Politico-economically: financial genocide, cronyism. Broader: democracy failure if unchecked.

Flowing immanently from the public servant scrutiny, this piece zeros in on specific legal oversights like Section 66, illustrating how CoC conspiracies enable fraud laundering, and extends the horizon to calls for Supreme Court intervention, reinforcing the pattern of ignored frauds as deliberate design in crony takeovers.

VIB.7 Exclusionary Tactics: The Great Non-Wilful Absentees in the RBI-Appointed CoC for DHFL (April 12, 2023; Updated August 16, 2024)

This dissects Wadhawans’ deliberate exclusion, violating IBC Section 19 and NCLAT precedents. Allegations: debarred despite rights; ignored Rs 26,000 crore valuation/full offers; Oaktree bias suit (December 6, 2021); RTI denials (April 13–June 14, 2023) declare RTI “dead.”

Critiques: opacity undermines trust; RTI flaws. Demands: inclusion, reconsideration, Das resign, fee return. Politico-economically: crony bias, BJP vendetta. Broader: legitimation crisis, autocracy.

This exclusionary focus logically extends the fraudulent oversights by highlighting promoter bar tactics under Section 29A, tying into RTI denials as evidence of opacity, and broadens the critique to legitimation crises under autocratic tendencies, setting up subsequent sarcastic critiques of post-CoC careers.

VIB.8 The “Goodwill” (?) of R. Subramaniakumar, the ex-Administrator of DHFL (15/03/2024, updated 04/08/2024)

Sarcastic critique of Subramaniakumar’s post-DHFL career (e.g., CEO of RBL Bank from June 2022, amid share plunge), questioning his “goodwill” given alleged favouritism toward Piramal, imposition of haircuts/delisting, conspiracy under Section 66, and conflict of interest in fee collection (funded by victims’ money).

It reinforces our points on ethical governance failure, public servant accountability under PCA, and IBC’s experimental failures in DHFL (AAA-rated NBFC handed over cheaply). Demands fee refund align with broader narrative of financial abuse and regulatory capture, linking back to fee refunds as reckoning and the 2022 demand-letter, where CoC’s “contrary to law” conduct (NCLAT January 27, 2022) justified forfeiture amid mental/financial harassment.

This post-career sarcasm extends the exclusionary tactics by personalizing the critique on key figures, exposing ongoing conflicts post-resolution, and transitions to culminating analyses of premature occupation as the irreversible outcome of such “goodwill.”

VIB.9 Focusing on the Culminating Heist: Occupation Before Finality—BJP-Enabled Piramal-DHFL Takeover (September 15, 2025)

Capping the chronological arc of our activist exposés—from early “rat-smelling” around Committee of Creditors (CoC) opacity in 2021, through escalating demands for probes, fee disgorgement, and accountability during 2022–2023, and sustained documentation of fraudulent exclusions and regulatory silence—this 2025 intervention identifies the decisive moment when procedural corruption hardened into irreversible expropriation: Ajay Piramal’s premature occupation of DHFL in September 2021, despite pending appeals and unresolved legal irregularities. This act subverted the doctrine of lis pendens (Section 52, Transfer of Property Act, 1882) and exposed the IBC as a mechanism for fait-accompli plunder rather than lawful resolution.

Drawing directly from the activist indictment “Occupation Before Finality: How Piramal’s Takeover of DHFL Allegedly Subverted Due Process with BJP’s Institutional Enablement” (15 September 2025), the article alleges a brazen asset grab facilitated by BJP-aligned institutions. Piramal acquired a solvent, fraud-tainted AAA-rated NBFC with assets exceeding ₹90,000 crore not through superior value or transparent bidding, but through political patronage, judicial deference, and capitalist kinship networks that rendered him “more equal” than all other creditors. The takeover is situated within allegations of DHFL’s terror-funding links involving Dawood Ibrahim and Iqbal Mirchi, and questions of selective scrutiny that shielded Piramal while criminalizing the Wadhawans without adjudication.

The legal timeline exposes systematic manipulation. On 19 May 2021, the NCLT directed reconsideration of Kapil Wadhawan’s 100% repayment proposal—an order stayed by the NCLAT on 25 May 2021. The NCLT nonetheless rushed approval of Piramal’s plan on 7 June 2021. On 27 January 2022, the NCLAT (in 63 Moons’ challenge) declared the plan “discriminatory, illegal, and full of material irregularities.” The Supreme Court’s stay of this order on 11 April 2022 conspicuously did not disturb Piramal’s already-completed possession, converting procedural violation into irreversible fait accompli.

Further, potential recoveries under Section 66 for fraudulent and wrongful trading—estimated at ₹45,000–47,000 crore—were effectively handed to Piramal at a notional value of ₹1, while Section 32A immunity laundered prior offenses. This occurred alongside ignored evidence, selective prosecution of the Wadhawans, and the overlooking of Piramal’s own history, including the Flashnet scam and allegations of insider trading—most notably Piramal’s prescient warning of NBFC “shocks” on 28 January 2019, one day before Cobrapost’s 29 January 2019 exposé of DHFL’s ₹31,000-crore diversion to shell entities, allegedly linked to BJP financing via electoral bonds.

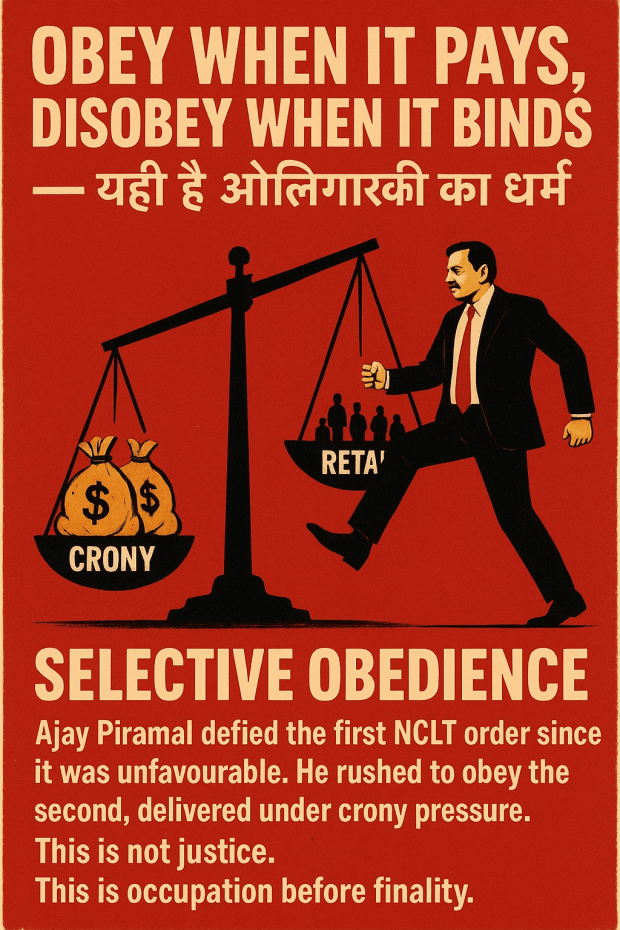

The article savages the IBC’s fetishization of “speed” over justice, exposing a regime where obedience to law is conditional on profit. Orders that constrain are ignored; orders that enable are executed with haste. This asymmetry is captured in the aphorism: “Obey when it pays, disobey when it binds—यही है ओलिगार्की का धर्म” and the Sanskrit charge: “अन्यायो बलवतः नियमः…”, framing oligarchic lawfare as governance. Slogans such as “Law for जनता, loopholes for धनिक,” “IBC = Injustice Before Completion—अधूरा न्याय, पूरा कब्ज़ा,” and “Occupation before finality is not justice, it is crony capture” operate as a people’s charge-sheet, situating 2.5 lakh mostly elderly depositors—reduced to ~23% recoveries on ₹5,375 crore dues—as guinea pigs in a neoliberal laboratory.

Politico-economically, the piece indicts the NDA regime’s “cunning capitalism,” where corporate restructuring (DHFL’s merger into Piramal Capital & Housing Finance and then Piramal Enterprises) functions to evade responsibility, while opaque financing through Electoral Bonds and PM CARES generates reciprocal indebtedness between corporates and the ruling party. Piramal’s alleged donations are framed as part of a wider ecosystem masking terror-funding, regulatory capture, and political protection.

Institutionally, the analysis documents erosion of judicial independence and separation of powers through executive alignment, post-retirement incentives, and ritualized deference to “commercial wisdom.” These practices are argued to breach India’s ICCPR obligations—Articles 2(3) (effective remedy), 7 (freedom from degrading treatment), 14 (fair hearing), 17 (protection from arbitrary interference), and 19 (freedom of expression)—by denying victims access to justice, equality, and institutional accountability.

This culmination also loops back to the earlier exposé “Piramal Is More Equal Than the Other 98%” (31 October 2022), where the Orwellian formulation captured the essence of the scheme: while all creditors are formally equal, Piramal alone captured avoidance recoveries worth ₹45,000–47,000 crore at ₹1, full control of a solvent AAA-rated company, and blanket immunity under Section 32A. The “98%” refers to the overwhelming majority of retail FD/NCD holders forced into catastrophic haircuts, their rights extinguished in the name of resolution.

The nepo-capitalism dimension is explicit. Ajay Piramal’s familial alliance with Mukesh Ambani—cemented through Anand Piramal’s marriage to Isha Ambani in 2018 but rooted in decades-old business ties—forms part of a seamless oligarchic ecosystem alongside regime-favored conglomerates such as Adani, Vedanta, and Tata, all major post-IBC beneficiaries and electoral-bond donors. Power flows through blood, marriage, capital, and political patronage, not law.

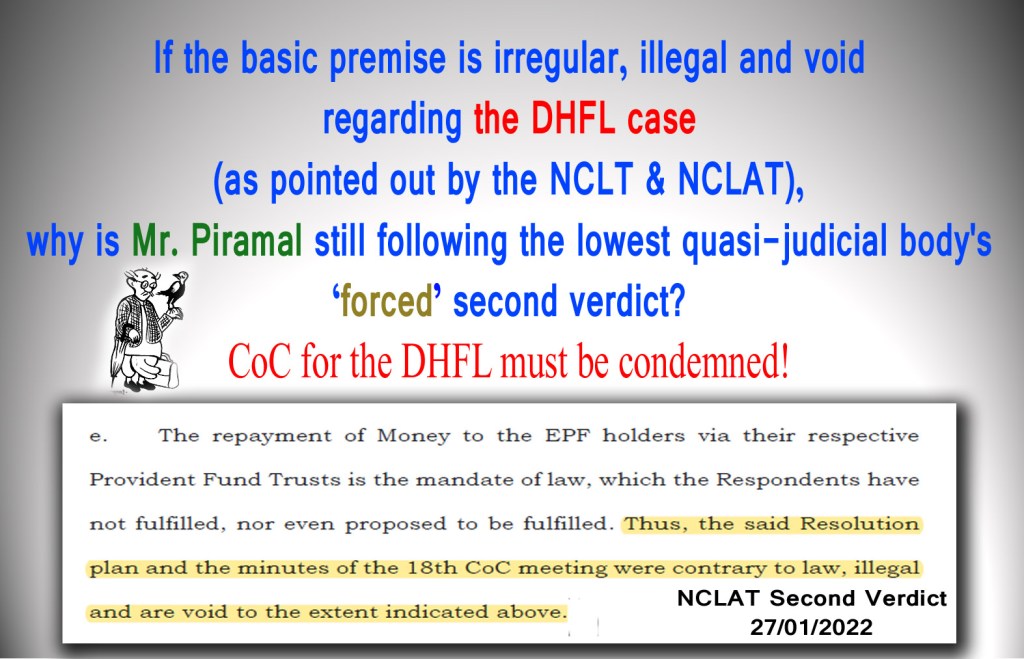

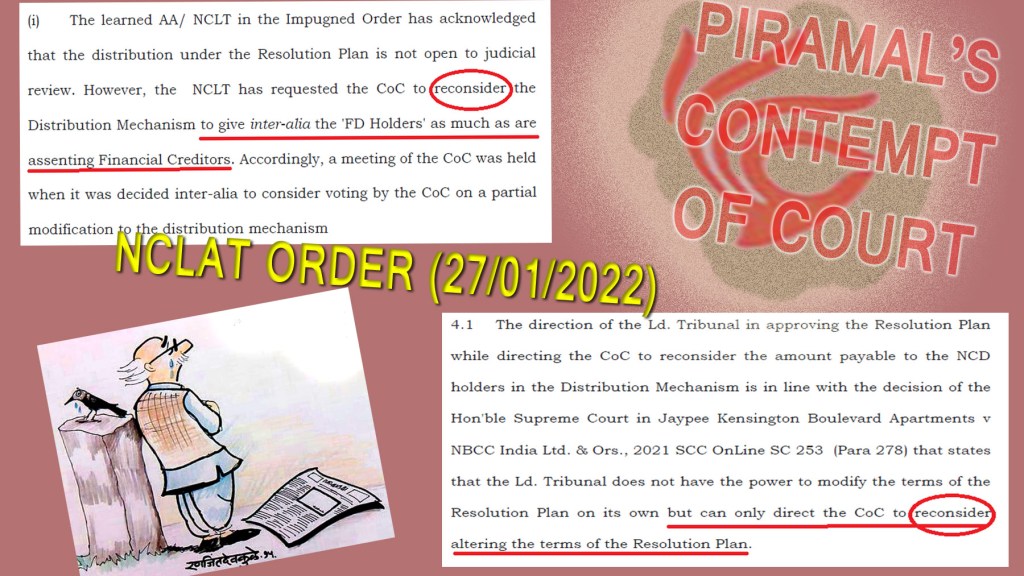

Situated within our wider IBC critique, the RBI-appointed, Subramaniakumar-led CoC emerges as the gatekeeping instrument that privileged Piramal over higher or fairer alternatives (including Oaktree and a 100% repayment offer), weaponizing the “creditor-in-control” doctrine as a legal fig-leaf for crony capture. The Supreme Court’s final imprimatur on 1 April 2025 (Justice Bela M. Trivedi bench), approving the plan with 93.65% CoC voting, granting Piramal access to fraud proceeds, dismissing creditor appeals, and enabling RBI’s NOC, sealed this architecture of impunity.

Piramal’s occupation of DHFL thus stands as the single most damning proof that the IBC was never designed for resolution. It was engineered for upward redistribution to those connected by marriage, money, and electoral bonds. This was not insolvency law in action, but adverse possession by statute—a culminating heist that compels not reform but dismantling of the IBC’s predatory architecture if justice is to be restored to its victims.

VIC. Ajay Piramal’s Occupation of DHFL as the Decisive Exhibit of Crony–Nepo–Capitalism under the IBC’s Expropriative Framework

What distinguishes the DHFL resolution from other controversial IBC cases is not merely the scale of depositor loss or the magnitude of haircuts, but the conversion of a contested insolvency process into an irreversible asset transfer through premature occupation. When read together, “Piramal Is More Equal than the Other 98%” (2022) and “Occupation Before Finality” (2025) do not repeat the same critique; they complete it. The former establishes Piramal’s exceptional position within the creditor hierarchy, while the latter demonstrates how that exceptionalism was operationalized into possession despite unresolved legality. The synthesis reveals a decisive shift: from procedural distortion to accomplished expropriation.

DHFL thus becomes the clearest instance where the IBC ceased to function even nominally as a resolution framework and instead operated as a conveyancing device for politically enabled asset consolidation. The transfer was neither value-maximizing nor finality-compliant; it was power-compliant.

VIC.1 Occupation as Strategy: Possession as Legal Irreversibility

The central legal novelty exposed here is not delay or haircut, but occupation without finality. Piramal’s assumption of control in September 2021 occurred in the interregnum between contested adjudicatory stages, before appellate scrutiny had concluded. This move exploited a structural asymmetry within the IBC: while appeals can suspend orders, possession—once taken—is rarely clawed back.

The consequence was not merely procedural impropriety but doctrinal inversion. The principle of lis pendens, designed to prevent parties from altering the subject matter of ongoing litigation, was rendered functionally irrelevant. Once control was transferred, subsequent findings of illegality (including the NCLAT’s January 2022 characterisation of the plan as discriminatory and materially irregular) were neutralised in practice. Law remained available on paper; remedy did not.

This establishes occupation-before-finality as a deliberate strategy, not an accident of speed—ensuring that even successful appellate findings would arrive too late to undo control.

VIC.2 Selective Velocity: How Judicial Time Was Differentially Applied

A striking feature of the DHFL timeline is not haste per se, but directional haste. Orders that constrained the preferred outcome stagnated or were bypassed; orders that enabled it moved with extraordinary speed. This asymmetry does not require imputing motive to be analytically significant—it demonstrates outcome-sensitive temporality.

The rapid stay of the NCLT’s direction to reconsider a full-repayment proposal, followed by swift approval of Piramal’s plan despite unresolved objections, contrasts starkly with the prolonged inertia faced by depositor challenges and fraud-related concerns. Later appellate findings identifying illegality did not trigger possession reversal, while enabling orders were implemented immediately and irreversibly.

What emerges is not judicial error but selective obedience: compliance calibrated to advantage. In this configuration, “commercial wisdom” operates less as a doctrine than as a shield—absorbing contradictions without resolving them.

VIC.3 Kinship, Capital, and Access: How Dynastic Nepo-Capitalism Becomes Operative

This section does not reiterate that India has oligarchs; it specifies how oligarchy becomes legally actionable. Piramal’s secondary kinship linkage to Mukesh Ambani situates him within a closed circuit where economic capital, political access, and institutional trust circulate internally. Within such a circuit, regulatory clearance, creditor preference, and judicial deference do not appear as favors; they present as normal flow.

The significance of this nexus is not symbolic but functional. It helps explain why Piramal could be treated as a safe acquirer despite unresolved allegations surrounding DHFL’s past, while alternative pathways—whether higher bids or full repayment—were systematically marginalised. Nepotistic proximity does not replace law; it reorders which laws are activated, which are paused, and which are rendered moot by timing.

VIC.4 Victims as Structural Absentees, Not Accidental Casualties

The depositor outcome is not revisited here as a moral lament but as structural evidence. Retail FD/NCD holders were not merely underrepresented; they were designed out of the decisional architecture. Their exclusion from the CoC, combined with the immunity regime under Section 32A, ensured that once occupation occurred, their claims became legally irrelevant even if factually compelling.

The result is a new juridical condition: completed injustice without adjudicated finality. Depositors were not defeated in court; they were overtaken by possession. This marks a qualitative shift from loss through judgment to loss through timing.

VII. RBI-Appointed DHFL CoC: Evidentiary Anchors

This section consolidates specific, documentable allegations concerning the RBI-appointed CoC, not as repetition of earlier critique but as evidentiary grounding for why occupation-before-finality was possible.

VIIA. Procedural Control and Information Asymmetry

The CoC’s conduct is alleged to have systematically restricted transparency: incomplete or inaccessible minutes, opaque valuation logic, and unanswered distribution queries. These are not incidental lapses; they are control mechanisms that prevent contestation during the only phase when contestation could matter—before possession.

Premature information-sharing by individuals associated with the CoC, and the absence of corrective action, further suggest a breakdown of fiduciary neutrality.

VIIB. Defiance of Binding Directions and Conflict Normalisation

Allegations that CoC processes proceeded despite unresolved judicial directions—particularly regarding promoter participation and reconsideration mandates—point to a normalization of selective compliance. This is not framed as contempt in the abstract but as a pattern that made irreversible transfer possible.

The extraordinary allocation of potential avoidance recoveries (₹45,000+ crore) at nominal value is significant here not for its quantum alone, but because it demonstrates how future upside was structurally diverted away from creditors before liability determination.

VIIC. Formal Complaints as Institutional Escalation

The Lokpal complaint dated 19 November 2022 marks a shift from advocacy to institutional escalation. It does not merely allege misconduct but identifies statutory violations under the Prevention of Corruption Act (Sections 7–9), contempt implications, and abuse of public office involving the Finance Ministry, RBI leadership, and the DHFL administrator.

Crucially, this complaint relies on findings already recorded by the NCLAT, grounding activist claims in judicial text rather than speculation. It reframes the issue from insolvency mismanagement to public corruption.

VIID. Fee Disgorgement as Accountability Threshold

The demand for refund of administrator and advisor fees (8 March 2022) introduces a concrete accountability metric. Rather than abstract condemnation, it asserts that remuneration extracted during a process later judicially described as illegal cannot be retained without legitimising misconduct.

This demand links value destruction, pandemic-era distress, and prolonged timelines into a single question: who bears the cost of illegality when no one is penalised?

VIIE. Integrated Analysis

These continuation sections do not re-argue that the IBC is flawed. They demonstrate how its architecture enables irreversible capture through timing, occupation, and institutional alignment. DHFL is not treated as an aberration but as a proof-of-concept: once possession precedes finality, legality becomes retrospective theatre.

The cumulative implication is precise and narrow: as long as the IBC permits transfer of control before the exhaustion of legal scrutiny, reform is structurally incapable of preventing capture. Scrapping, not tinkering, becomes the only coherent response to a regime where injustice is completed before it can be judged.