Posted on 24th February, 2026 (GMT 06:25 hrs)

An Independent OBMA Investigative Exposé

ABSTRACT

The DHFL insolvency resolution, culminating in its acquisition by Piramal Capital and Housing Finance (now Piramal Finance) and the February 2, 2026, Mumbai PMLA Special Court discharge from a ₹5,050 crore money-laundering case under Section 32A of the Insolvency and Bankruptcy Code (IBC), exemplifies alleged systemic flaws in India’s insolvency framework. This “clean slate” immunity extinguished corporate criminal liability for pre-CIRP offences while preserving prosecution against former promoters like the Wadhawan brothers, despite their ignored full-repayment proposals. Critics portray the process—marked by retrospective Section 32A insertion in December 2019 just before DHFL’s CIRP admission, Ajay Piramal’s January 2019 “shock” prediction preceding the Cobrapost exposé, massive creditor haircuts (54–77% on retail FDs/NCDs), nominal Re 1 valuation for ₹45,000 crore Section 66 avoidance recoveries benefiting Piramal, and upheld “commercial wisdom” in the Supreme Court’s April 1, 2025, judgment—as engineered cronyism favoring politically connected acquirers via electoral bond donations (Piramal entities contributed significantly to BJP coffers per 2024 ECI data), family ties to Ambani, Flashnet deal controversies, and PM CARES funding. Amid Piramal Finance’s resurgence (AUM ₹96,690 crore up 23% YoY, 9M FY26 PAT ₹1,004 crore up 162%, CRISIL AA+ rating), victim groups decry SLAPP suits silencing dissent, statutory contradictions prioritizing new owners over creditors, and demand full repeal of Section 32A to dismantle what they term a sophisticated mechanism of crony enrichment at the expense of lakhs of ordinary depositors’ savings.

DISCLAIMER: This document, compiled and correlated solely from publicly available facts, court records, official disclosures, parliamentary data, media investigations, and regulatory filings, represents the collective effort of OBMA founder-members to present a factual exposé of recurring patterns documented across credible public sources—without making any personal allegations against individuals, but simply connecting dots that have been reported, adjudicated, or officially released over the years. Our sole purpose is to offer ordinary citizens, particularly the affected DHFL depositors, a single coherent narrative of the sequence of events, legal maneuvers, corporate restructurings, political-financial linkages, and judicial outcomes surrounding the DHFL resolution, enabling them to see the full picture and draw their own conclusions from verifiable information. Having ourselves faced—and continuing to face—legal intimidation through SLAPP-style defamation suits precisely for exercising the democratic right to collate and comment on public-domain material, this note also serves as a firm statement of resolve: free speech and public-interest scrutiny cannot and will not be silenced by litigation intended to chill dissent. OBMA reaffirms its unwavering commitment to transparency, accountability, and justice for the lakhs of DHFL victims whose life savings were wiped out while a politically connected acquirer received a clean-slate entity with massive upside—urging every reader to verify the cited sources independently and decide for themselves.

I. Introduction

In February 2026, a Mumbai PMLA Special Court discharged Piramal Finance (formerly Dewan Housing Finance Corporation Limited, or DHFL) from a ₹5,050 crore money-laundering case. The judicial fig leaf? Section 32A of the Insolvency and Bankruptcy Code — the single most dangerous provision ever inserted into Indian statute books. In an order dated 2 February 2026 by Special Judge R.B. Rote, the court granted statutory immunity under Section 32A, extinguishing corporate criminal liability for pre-CIRP offences and allowing the entity to start on a “clean slate” — while former promoters and individuals (viz., the Wadhawan brothers, who wanted to pay all the creditors in full for multiple times, but were left unheard) remain prosecutable.

Special court discharges DHFL in money laundering case, cites immunity under IBC VIEW HERE ⤡ (As reported on 5th February, 2026 ©ET Legal World)

This was never “insolvency reform.” This was a pre-meditated political operation dressed in the language of economic liberalisation. And DHFL was deliberately chosen as the test case to legitimise the entire IBC project while saving the Modi government’s face after years of NBFC carnage. But was this able to “save” the image, or tarnish it beyond recovery?

The acquisition itself was structured as a reverse merger: Piramal Capital & Housing Finance Limited (PCHFL) merged into DHFL effective 30 September 2021, with DHFL as the surviving entity. The combined company was immediately rebranded as Piramal Capital & Housing Finance Limited (later shortened to Piramal Finance in subsequent restructurings, including a 2025 reverse merger absorbing Piramal Enterprises Ltd. into the lending arm). This shrewd corporate choreography — reverse merger, rebranding, and entity shuffling — enabled the group to effectively disown or distance itself from DHFL’s tainted legacy while inheriting its assets, branch network, and loan book.

Critically, the resolution plan ascribed a notional value of exactly Re 1 to avoidance transactions (including Section 66 fraudulent/wrongful trading recoveries) estimated at ₹45,000 crore in forensic audits — handing this speculative upside to Piramal as Successful Resolution Applicant (SRA), while creditors bore massive haircuts (54–77% on retail fixed deposits and NCDs held by lakhs of ordinary families). The Supreme Court’s 1 April 2025 judgment upheld this as valid “commercial wisdom,” seemingly sealing the transfer.

It did not merely “resolve” a stressed asset. It delivered a ₹91,000-crore AAA-rated ongoing profitable non-banking housing finance company (note that DHFL was not a ponzi scheme!), complete with its avoidance-transaction upside worth ₹45,000 crore (valued at Re 1), straight into the hands of Ajay Piramal on a silver platter — while extinguishing every trace of criminal liability for the corporate debtor through layered restructurings that obscured continuity with the old DHFL.

II. The Retrospective Trap: Engineered from Day One

Section 32A was never an afterthought. It was a deliberately timed legislative strike, inserted with surgical precision to neuter criminal liability exactly when it mattered most for one politically connected bidder.

- On 28 December 2019, the Modi government promulgated the IBC (Amendment) Ordinance, 2019, inserting Section 32A with immediate and explicit effect from that very date.

- The Amendment Act later received presidential assent on 13 March 2020, but Parliament ensured the “clean-slate” immunity applied retrospectively from the ordinance date itself.

Now examine DHFL’s corrected timeline, stripped of official spin:

- 20 November 2019: RBI supersedes DHFL’s board amid massive fraud allegations.

- 3 December 2019: NCLT admits DHFL into CIRP — the first major financial services provider pushed through the IBC pipeline.

- 28 December 2019: Just 25 days after CIRP commencement — while claims were still being invited, the Committee of Creditors was forming, and the entire process was in its most malleable early stage — the government drops the Section 32A bomb.

This was not coincidence. This was calendar-driven engineering.

The CIRP had already begun. The machinery was running. Then, mid-process, the government inserted a nuclear-grade immunity clause that would wipe out all pre-CIRP criminal liabilities of the corporate debtor once a resolution plan was approved and control changed hands. The timing ensured that whoever won the bid would inherit a pristine, prosecution-proof company — while the original promoters (the Wadhawans) remained prosecutable fall guys.

And who won? Ajay Piramal — the corporate tycoon repeatedly labelled in public discourse as one of the BJP’s most favoured tycoons.

Piramal Capital & Housing Finance’s plan was approved by NCLT on 7 June 2021. The new management immediately invoked Section 32A. Courts upheld it. The Supreme Court in April 2025 preserved the plan. And on 2 February 2026, the Special PMLA Court in Mumbai discharged the DHFL entity (now Piramal Finance) from the entire ₹5,050 crore money-laundering case linked to the Yes Bank-DHFL conspiracy — explicitly citing Section 32A’s overriding immunity. The company walked free. The individuals stayed accused.

This was the weapon in action.

A provision rammed through Parliament just 25 days after DHFL entered IBC became the legal magic wand that handed a once-AAA-rated housing finance giant — riddled with ₹90,000+ crore in assets and serious fraud probes — to Piramal at a steep discount, with every criminal overhang on the company erased. Retail depositors and NCD holders took massive haircuts (54-77%). Avoidance transaction recoveries worth thousands of crores allegedly went to the new owner for a nominal Re 1. The “dirtiest, most politically toxic” asset was laundered into a clean, profitable jewel — provided the buyer was the politically acceptable one.

The sequence is damning: trigger the insolvency of a scandal-hit NBFC → let the process begin → insert retrospective immunity mid-stream → ensure only the BJP-aligned bidder can safely close the deal without inheriting criminal baggage.

Call it what it is: Section 32A was custom-engineered as the ultimate crony shield so that Ajay Piramal could walk away with DHFL scrubbed clean of its past sins, while ordinary depositors were left holding the losses and the original promoters were left holding the blame.

This was never about “resolution”. This was about selective sanitisation for the politically favoured. And the calendar proves it.

III. Piramal’s “Prediction” — The Smoking Gun of Pre-Planning?

Ajay Piramal’s words from 28 January 2019 hang like a shadow over the entire DHFL saga: “Be prepared for one or two major shocks in the NBFC sector.” This was not vague optimism or routine commentary — it was a pointed warning issued in a public forum (reported by The Hindu on the same day), amid the unfolding IL&FS fallout and liquidity crunch gripping NBFCs.

The very next day, 29 January 2019, Cobrapost unleashed its bombshell sting: “Anatomy of India’s Biggest Financial Scam,” accusing DHFL promoters of siphoning over ₹31,000 crore through a web of shell companies, dubious loans, and alleged political donations (including to the BJP) and even terror-funding links. The exposé relied on public records and scrutiny of RoC filings, triggering immediate market panic, rating downgrades, and scrutiny that snowballed into DHFL’s eventual collapse.

How did Piramal “know” — or at least foresee — a “major shock” with such precise timing, one day before the most damning independent exposé on an NBFC? Mainstream coverage framed his remark as informed commentary on sector-wide stress (post-IL&FS, liquidity squeeze from mutual funds pulling back, etc.). But critics — including DHFL victim groups, blogs, and petitions — label it foreknowledge bordering on insider information, arguing it should have prompted SEBI probes for potential market manipulation or ED scrutiny under money-laundering angles. No such formal inquiry materialized against Piramal on this count.

Instead, the man who flagged the coming “shock” emerged as its ultimate winner: Piramal Capital & Housing Finance acquired DHFL in 2021 at a steep discount (₹37,000 crore bid for ₹90,000+ crore assets), with massive haircuts inflicted on retail depositors and NCD holders (54–77%), while the entity gained a “clean slate” via Section 32A.

The pattern reeks of orchestration:

- Expose first (Cobrapost, 29 Jan 2019) — public outrage and pressure built.

- Orchestrated RBI action (board supersession 20 Nov 2019, CIRP admission 3 Dec 2019) — under the new FSP framework.

- Retrospective legal shield (Section 32A ordinance 28 Dec 2019, mid-CIRP) — erasing corporate criminal liability post-plan approval.

- Gift-wrapped handover to the “prepared” bidder (Piramal), who outmaneuvered others — including the jaw-dropping assignment of a notional Re 1 value to potential recoveries from avoidance transactions estimated at ₹45,000 crore (fraudulent diversions, wrongful trading under Section 66 IBC, uncovered in forensic audits). This single-rupee valuation effectively handed Piramal the entire upside of these massive clawback claims as the successful resolution applicant, while creditors absorbed the pain — a move upheld as “commercial wisdom” by the Supreme Court in its April 2025 judgment (despite earlier NCLAT pushback in 2022 to reconsider it).

Oaktree Capital — a competing resolution applicant offering what some rated as quantitatively stronger on certain metrics — repeatedly cried foul. In late 2020–early 2021, Oaktree accused the Committee of Creditors (CoC) of bias toward Piramal: procedural irregularities, lack of transparency in evaluation, undue preference despite Oaktree’s allegedly higher/more comprehensive bid in parts, and threats of legal action against lenders for showing favoritism. (Reports from Economic Times, Hindu BusinessLine, CNBC-TV18, and others confirm Oaktree contemplated/mulled suits over the process, though it did not derail the eventual Piramal win upheld by NCLT/NCLAT/SC.)

Even more glaring: The Wadhawan brothers (erstwhile promoters) made repeated full-repayment/settlement proposals during CIRP — offers to repay creditors in full via restructuring or infusions — but these were summarily ignored or dismissed without deep merit evaluation. NCLT (in 2021 orders) noted lenders did not consider Kapil Wadhawan’s proposals on commercial wisdom grounds. Public depositors (holding nearly 65% CoC voting share via FD/NCD pools) were never comprehensively shown or allowed to vote on these promoter-led revival options, per victim advocacy records and court filings.

Everything connects too neatly: A high-profile “prediction” precedes the killer exposé → scandal escalates → insolvency triggered → immunity legislated mid-process → competing bids sidelined amid bias allegations → full-repayment paths blocked → ₹45,000 crore avoidance upside gifted at Re 1 → toxic asset sanitized and handed to the politically acceptable acquirer.

This wasn’t spontaneous market correction. It was a meticulously sequenced handover. Piramal didn’t just benefit from the shock — he appeared to anticipate it with uncanny accuracy, then reaped the sanitized spoils, including a ₹45,000 crore windfall valued at just Re 1. The dots connect themselves. Whether coincidence, sharp foresight, or something darker, the outcome delivered one of India’s most controversial “resolutions” — at the expense of lakhs of retail investors left with deep haircuts and unanswered questions.

IV. The Crony Proofs: Electoral Bonds, PM CARES, Flashnet, and Access

The “right buyer”/SRA/Mr. Ajay Piramal was never in doubt. Publicly available reports, official Election Commission data, parliamentary records and opposition investigations have repeatedly pointed to a deep, mutually beneficial nexus (quid pro quo?!) between the BJP-led government and Ajay Piramal — described by critics as classic corporate-state collusion at the highest levels.

- Electoral Bonds (now declared unconstitutional): The Supreme Court struck down the entire Electoral Bonds Scheme on 15 February 2024 as violative of the right to information under Article 19(1)(a). Before that, Piramal Group entities poured ₹85–98 crore into the BJP’s coffers (SBI/ECI data released 2024). This included a ₹10 crore tranche from Piramal Capital & Housing Finance Ltd while it was still recording losses and paying zero or negative direct taxes — one of 33 loss-making companies that collectively donated ₹582 crore, of which 75% went to the BJP (The Hindu/Scroll analysis, April 2024). Critics call this textbook quid pro quo: opaque corporate funding to the ruling party in exchange for favourable treatment in stressed-asset resolutions.

- Flashnet Deal (2014 transaction, 2018 controversy): In July 2014, Piramal Estates Pvt Ltd bought Flashnet Info Solutions (India) Ltd — a near-dormant company owned by then-MP Piyush Goyal and his wife Seema Goyal — for ₹48 crore at a staggering premium (nearly 1,000% over book value of ~₹10.9 crore). Congress termed it a “murky saga of gratification, gross impropriety and conflict of interest” when the story broke in 2018, noting the timing coincided with Goyal’s elevation as Union Minister for Power & New and Renewable Energy — sectors where the Piramal Group was aggressively expanding. The BJP dismissed the charges as “baseless”, but the transaction remains a textbook exhibit in public discourse on crony linkages.

- Family & Proximity Ties: Ajay Piramal is secondary kin (samdhi) of Mukesh Ambani — one of the BJP and Modi-Shah dispensation’s closest and most powerful industrial allies — through the 2018 marriage of his son Anand Piramal to Ambani’s daughter Isha. This dynastic convergence is openly acknowledged in media and business circles.

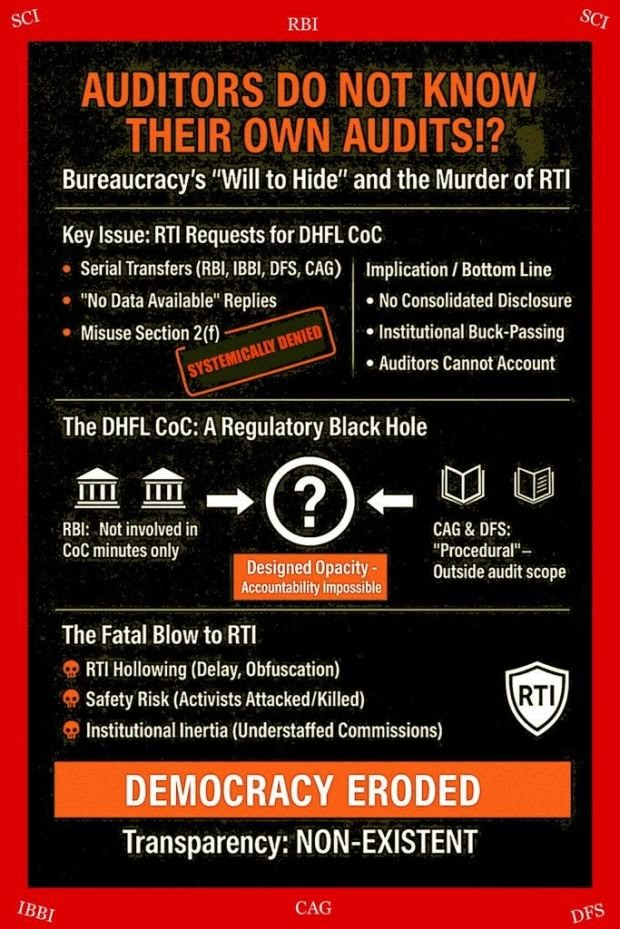

- Direct Access & Opaque Funding: Ajay Piramal has co-chaired India-UK CEO forums under Prime Minister Modi, donated ₹25 crore to the PM CARES Fund, and sits on multiple government advisory panels. He enjoys repeated closed-door meetings with the Prime Minister (e.g. June 2018 Raj Bhavan CEO interaction and June 2020 virtual economic recovery meet – as per Economic Times and Business Standard reports). The PM CARES Fund itself is highly controversial: it uses the Prime Minister’s personal image and the official Ashok Stambha seal, yet is structured as a “non-governmental” private trust. This allows it to evade RTI applications and — as per a February 2026 PMO directive to the Lok Sabha Secretariat — even parliamentary questions on its accounts are ruled “not admissible”. What does this say about accountability when public imagery and state symbolism are used for a fund shielded from scrutiny?

Victim groups, opposition parties and independent analysts have repeatedly framed the entire sequence as a return gift: massive electoral funding + family-corporate proximity + ministerial dealings = a distressed ₹91,000-crore asset (plus ₹45,000 crore avoidance upside at Re 1) delivered via retrospective Section 32A immunity.

This is not speculation or defamation or character assassination of Mr. Piramal — these are all widely reported facts drawn from official SBI/ECI data, Supreme Court records, company filings, and contemporaneous media investigations as per public records. The pattern reveals systemic corporate-state collusion under the Modi regime, where politically connected conglomerates are rewarded while lakhs of ordinary depositors bear the losses.

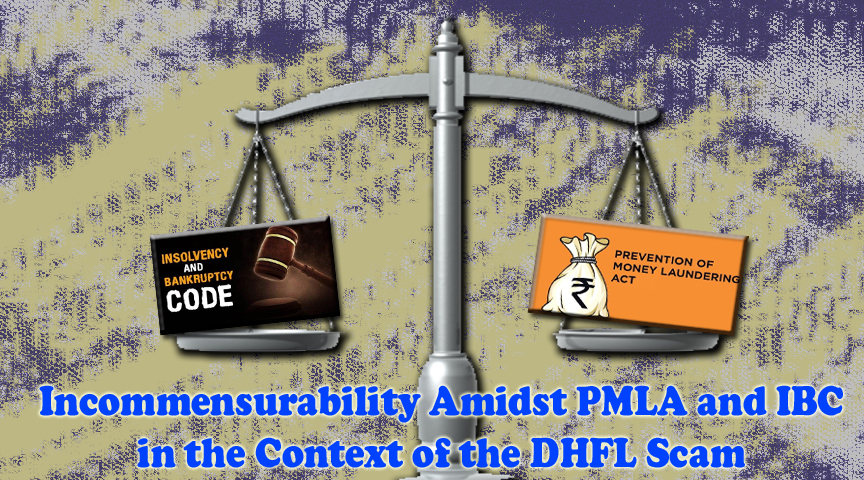

V. The Fatal Internal Contradiction: Section 32A vs Section 66 of the Ill-Conceived IBC

The Code’s own incoherence exposes the fraud.

Section 66 explicitly states that recoveries from fraudulent or wrongful trading shall benefit all creditors. NCLAT, in its landmark 27 January 2022 order in the 63 Moons challenge, saw through the game: it held the resolution plan “discriminatory, illegal and full of material irregularities” and directed that Section 66 recoveries must go back to the CoC for the benefit of creditors — not to Piramal at a notional ₹1.

But Section 32A — the clean-slate immunity — was used to override this statutory mandate. The Supreme Court in its 1 April 2025 judgment ultimately sided with Piramal, sanctifying the ₹1 valuation and the transfer of speculative recoveries to the Successful Resolution Applicant (SRA).

This is not judicial interpretation. This is statutory self-contradiction weaponized. One section says fraud recoveries belong to creditors. Another section says the new owner gets total immunity and keeps the upside. The result? Public money socialized as haircuts (54–77% for 2.5 lakh retirees, pensioners and widows); private gains privatized to a BJP donor.

V.A. The Statutory Sleight of Hand: How the IBC Lets the SRA Pocket Section 66 Recoveries

The Insolvency and Bankruptcy Code contains no provision that automatically funnels “all the money” from avoidance recoveries to the Successful Resolution Applicant (SRA). Yet in the DHFL case, Piramal walked away with potential recoveries under Section 66 valued at a token Re 1 — while recoveries under Sections 43–51 went to the CoC/creditors.

Section 66 itself empowers the Adjudicating Authority to order contributions “to the assets of the corporate debtor” for the benefit of creditors generally. There is no statutory carve-out allowing these recoveries to be gifted to the SRA. The allocation flows solely from the approved resolution plan, rubber-stamped by the CoC’s “commercial wisdom” and upheld under Section 31.

The Supreme Court in its 1 April 2025 judgment explicitly sanctified this bifurcation as a “commercial bargain” — the SRA bears litigation risks and keeps any upside, while creditors get higher upfront certainty. The notional Re 1 valuation was called “reasonable” given the uncertainty.

This is textbook statutory sleight of hand. Section 66’s text speaks of creditor benefit — yet judicial deference allowed the SRA to pocket the speculative windfall. The very fraud that wrecked DHFL (and robbed lakhs of depositors) now potentially enriches the politically connected buyer who “predicted” the scandal. Section 32A’s clean-slate immunity completes the circle — extinguishing corporate liability so the new owner starts pristine, free to pursue (and keep) whatever Section 66 yields.

This is engineered extraction: Parliament provides the tools, the CoC negotiates the giveaway, courts defer to “commercial wisdom,” and the crony walks away richer. Undoubtedly, in contemporary India, the line of demarcation amid the judiciary and the political executive has increasingly withered away.

VI. The Corporate Triumph Amid Victim Silencing

While Piramal Finance celebrates soaring metrics — AUM crossing ₹96,690 crore (up 23% YoY), 9M FY26 consolidated PAT at ₹1,004 crore (up 162% YoY), fresh CRISIL AA+ rating, $350 million DFI funding from IFC & ADB, and $400 million ECB from global lenders — the lakhs of DHFL victims remain in limbo. Their life savings vanished in massive haircuts (54–77% for many fixed deposit and NCD holders), yet the company’s balance sheet expands unchecked.

This is the stark divide: explosive corporate resurgence built on the ruins of ordinary depositors’ trust.

Compounding the injustice, Piramal Capital and Housing Finance Limited (now Piramal Finance) — through its legal firm DSK Legal — has filed multiple defamation suits (widely described as SLAPP suits — Strategic Lawsuits Against Public Participation) against dissenting DHFL victims, activists, and members of groups like OBMA (Online Bloggers and Independent Digital Media Activists) since March 2023. These actions target individuals and platforms exercising democratic free speech on social media, blogs, and forums to highlight alleged irregularities in the resolution process, financial abuse, and crony elements. Critics argue these suits aim to intimidate, silence, and suppress legitimate criticism rather than address substantive defamation claims — a classic SLAPP tactic that burdens victims with legal costs and threats while shielding corporate power from accountability.

This is guilt laundering at industrial scale, now enforced through legal intimidation.

VII. The Demand: Repeal Section 32A Now

Section 32A must be repealed in its entirety. Not diluted, not narrowed — scrapped.

It was never a neutral economic tool. It was a retrospective legislative gift crafted at the exact moment DHFL was being herded into the IBC slaughterhouse, designed to protect politically favoured buyers while robbing small savers of both their money and their right to justice.

The IBC was legitimised by treating DHFL as its test case. The same IBC has now become the most sophisticated legal instrument of crony accumulation in independent India’s history.

Until Section 32A is repealed, every “resolution” under this Code will remain what DHFL truly was: not a rescue, but a heist — sanctioned by Parliament, sanctified by the Supreme Court, and executed by a politically connected billionaire who “predicted” the crime one day before the country found out.

The corporate metrics climb higher by the quarter. The forty-five-thousand-crore loot sits safely in Piramal’s balance sheet. And the lakhs of ruined families are still waiting for justice.

Repeal Section 32A. Dismantle the clean-slate fraud. Return what was “legally” stolen. Anything less is complicity in the greatest (=worst) financial dispossession of India’s middle class since Independence.

Scrap IBC!

SEE ALSO:

Scam 2019: The DHFL Massacre VIEW HERE⤡ @YouTube

Dear #DHFL_Victims, Use these posters and hashtags for online campaigning:

IBC Section 32A Explained | DHFL Piramal Takeover Analysis | Insolvency Code Critique | Crony Capitalism in India | Depositor Rights & Bankruptcy Law Reform | Financial Governance Crisis | Corporate Accountability Campaign

Hashtags

#Scrap_Ill_Conceved_IBC, #IBCSection32A, #InsolvencyAndBankruptcyCode, #IBCReformNow, #DHFLScam, #DHFLPiramalTakeover, #JusticeForDHFLVictims, #JusticeForDepositors, #Seize_Cronies_Fairplay_for_DHFL_Victims, #alleged_dawood_mirchi_rkw_dhfl_bjp_collusion, #CronyCapitalismExposed, #CorporateCaptureIndia, #PublicMoneyPrivateProfits, #FinancialGovernanceCrisis, #TransparentBankruptcy, #InvestorProtectionIndia, #DepositorRightsIndia, #RegulatoryFailureIndia, #AccountabilityInIBC, #PolicyCaptureIndia, #StopCorporateLoot, #ReclaimPublicFunds, #FinancialSystemsReform, #PeopleOverProfit, #DigitalActivismIndia, #JusticeMovementIndia, #ExposeTheSystem, #PublicInterestEconomics, #BankruptcyLawReform, #OBMA, Occupy_Internet_to_Occupy_Cronies,

Section 32A vs Section 66 of the Ill-Conceived IBC. The Clean Slate That Was Engineered #DHFL_Justice_Movement, #JusticeForDepositorsDHFL, #FinancialAbuseDHFL, #CorporateAccountabilityDHFL, #IBCFail, #Scrap_IBC, #HaircutAshes_DHFL, #PublicFundsPrivatisedINDIA, #ProtectRetailInvestorsDHFL, #CreditRatingFraud_DHFL, #AuditFail_DHFL, #RatingAgencyReformDHFL, #JudicialReformDHFL, #DemocracyUnderAudit, #Save_Indian_Legal_System, #CitizenVsCorporate, #StandWithVictims, #OrganizeForJustice, #OnceInABlueMoonActivists,

LikeLiked by 6 people

Section 32A vs Section 66 of the Ill-Conceived IBC. The Clean Slate That Was Engineered, #DHFL_Justice_Movement, #JusticeForDepositorsDHFL, #FinancialAbuseDHFL, #CorporateAccountabilityDHFL, #IBCFail, #Scrap_IBC, #HaircutAshes_DHFL, #PublicFundsPrivatisedINDIA, #ProtectRetailInvestorsDHFL, #CreditRatingFraud_DHFL, #AuditFail_DHFL, #RatingAgencyReformDHFL, #JudicialReformDHFL, #DemocracyUnderAudit, #Save_Indian_Legal_System, #CitizenVsCorporate, #StandWithVictims, #OrganizeForJustice, #OnceInABlueMoonActivists, #Scrap_Ill_Conceved_IBC,

LikeLiked by 6 people

Section 32A vs Section 66 of the Ill-Conceived IBC

IBC Section 32A Explained | DHFL Piramal Takeover Analysis | Insolvency Code Critique | Crony Capitalism in India | Depositor Rights & Bankruptcy Law Reform | Financial Governance Crisis | Corporate Accountability Campaign|

They erased liability.

They erased accountability.

They will NOT erase us.

Scrap the law that shields cronies.

Return the people’s money.

Justice for DHFL victims — now.#Scrap_Ill_Conceved_IBC, #IBCSection32A, #InsolvencyAndBankruptcyCode, #IBCReformNow, #DHFLScam, #DHFLPiramalTakeover, #JusticeForDHFLVictims, #JusticeForDepositors, #Seize_Cronies_Fairplay_for_DHFL_Victims, #Alleged_Dawood_Mirchi_Rkw_Dhfl_Bjp_Collusion, #CronyCapitalismExposed, #CorporateCaptureIndia, #PublicMoneyPrivateProfits, #FinancialGovernanceCrisis, #TransparentBankruptcy, #InvestorProtectionIndia, #DepositorRightsIndia, #RegulatoryFailureIndia, #AccountabilityInIBC, #PolicyCaptureIndia, #StopCorporateLoot, #ReclaimPublicFunds,

LikeLiked by 5 people