Posted on 1st April, 2026 (GMT 07:50 hrs)

ABSTRACT

This article traces the historical transformation of Indian banking from postcolonial state-led social banking to the contemporary regime of what it terms “resolution capitalism,” foregrounding the shifting configurations of power, distribution, and knowledge. Beginning with the pre-1969 era of private concentration and systemic fragility, it examines how bank nationalization sought to democratize credit and align finance with developmental and redistributive goals, albeit with embedded contradictions of bureaucratic inefficiency and political interference. The post-1991 liberalization phase introduced prudential norms and market discipline within a hybrid structure, delivering growth and crisis resilience—most notably during the 2008 global financial crisis—while simultaneously generating latent vulnerabilities through corporate over-leverage and regulatory forbearance. The article argues that the post-2014 period marks a decisive rupture: the recognition of NPAs through the Asset Quality Review was followed by massive recapitalization, large-scale write-offs, and the institutionalization of the Insolvency and Bankruptcy Code (IBC), which together reconfigured the system toward asset resolution rather than social intermediation. Through a detailed political-economic analysis, including the case of Dewan Housing Finance Corporation Limited (DHFL), the study demonstrates how the IBC operationalizes a structural asymmetry—socializing losses through public sector banks and taxpayers while privatizing gains for a narrow set of corporate acquirers—under conditions of institutional opacity, particularly within the Committee of Creditors. By situating these developments within broader trends of wealth concentration, regulatory opacity, and declining democratic accountability, the article contends that contemporary Indian banking no longer functions as an instrument of public purpose but as a mechanism of financialized redistribution upward. Ultimately, it raises a fundamental question for the political economy of the Indian republic: who bears the cost of financial crises, who appropriates their outcomes, and who controls the knowledge through which these processes are legitimized?

0. Introduction: From Open Social-ized Banking to Opaque Privatized Cronyism

The history of banking in postcolonial India is fundamentally a history of shifting regimes of power — over the allocation of credit, the direction of various modelled narratives of so-called development, the social distribution of financial risk and reward, and crucially, over knowledge itself. Who controls finance cannot be separated from who controls information about finance: the visibility of risk, the audit of loss, and the legitimacy of redistribution.

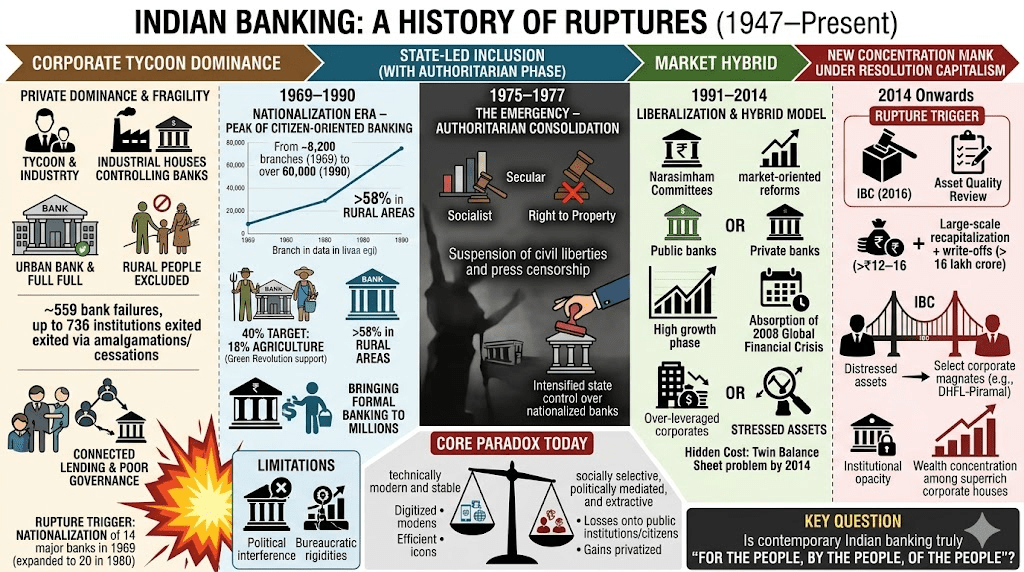

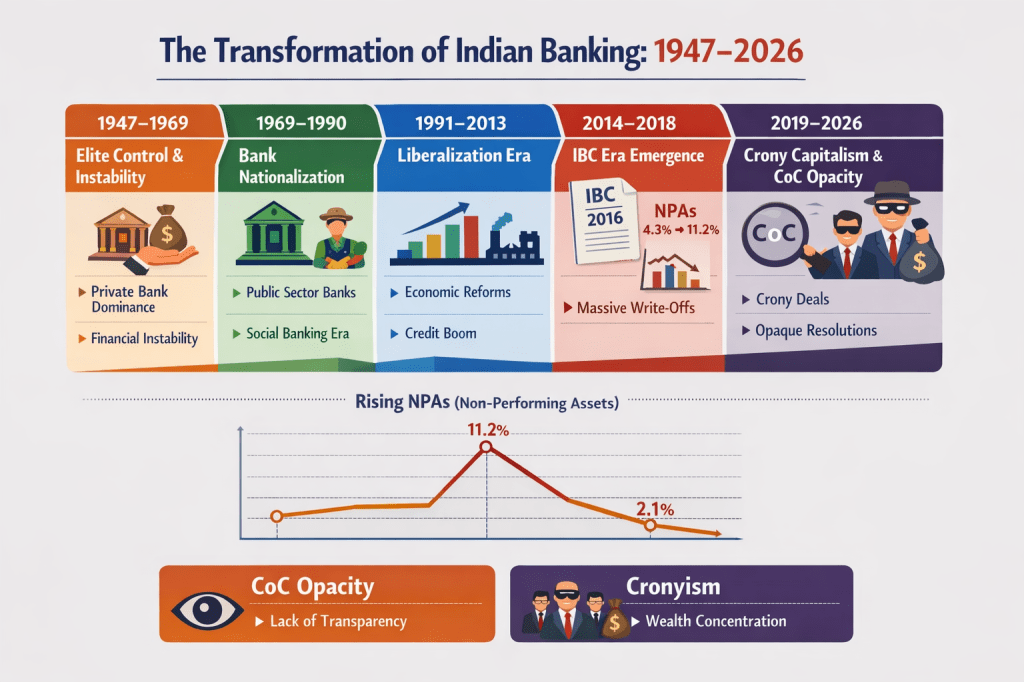

This article traces four major ruptures in the evolution of Indian banking:

- 1947–1969: An era of private banking dominated by industrial tycoons, marked by connected lending, strong urban bias, and systemic fragility. Despite the Nehruvian framework of planned development guided by Fabian socialist ideals and the Five-Year Plans, banking remained largely in private hands and continued to serve narrow commercial and industrial interests rather than broad-based public socialist goals. This period culminated in nearly 560 bank failures (with up to 665–736 institutions exiting through amalgamations or cessations), widespread loss of depositor confidence, and repeated crises that exposed the structural weaknesses of a privately dominated system.

- 1969–1990: The nationalization of major commercial banks under Indira Gandhi, which sought to transform banking into an instrument of social inclusion, rural credit expansion, and developmental planning.

- 1975–1977: The Emergency period, during which the constitutional amendments strengthened the socialist character of the state, removed the “Right to Property” from Fundamental Rights, intensified state control over the nationalized banking system, and subordinated democratic rights to authoritarian yet balanced developmentalism.

- 1991–2014: The (neo-)liberalization era, spanning the Vajpayee and Manmohan Singh governments, which introduced a hybrid model of public-sector dominance combined with private market-oriented reforms, delivering high growth and resilience during the 2008 Global Financial Crisis, yet concealing rising stressed assets and the “twin balance sheet” problem.

- 2014 onwards: The post-2014 phase under the Narendra Modi-led BJP–NDA government, characterised by the recognition of massive non-performing assets, large-scale recapitalization and write-offs of public sector banks, aggressive privatization of assets, and the operationalization of the Insolvency and Bankruptcy Code (IBC, 2016).

This article argues that the post-2014 period marks a decisive transition from an (imperfect) model of social banking — oriented toward broad-based inclusion and developmental credit — toward resolution capitalism, a regime in which distressed public assets are systematically transferred to private actors through state-mediated resolution mechanisms. In this regime, the state functions less as a direct allocator of credit for social ends and more as a guarantor of systemic stability and a facilitator of asset reallocation to favoured superrich tycoons within a crony setup. Public losses are socialized through taxpayer-funded recapitalization and write-offs, while distressed assets are transferred — often at steep discounts — to a narrow set of corporate acquirers. A particularly troubling feature of this shift is the institutionalized opacity surrounding key institutions, especially the Committee of Creditors (CoC) under the IBC. As seen in high-profile cases such as DHFL, even auditors appear unable to fully account for their own audit trails, and Right to Information requests frequently encounter resistance, producing an epistemic crisis where affected citizens lack access to the knowledge needed to scrutinise decisions. This transformation is not merely institutional—it marks a shift in the moral economy of finance itself.

Methodologically, the article adopts a historical political economy approach, combining archival and policy analysis with empirical trends in branch expansion, credit allocation, NPA movements, recovery rates, ownership shifts, and inequality metrics. It is structured in four parts: (1) the pre-nationalization era of private concentration and systemic fragility (1947–1969); (2) the political economy, achievements, and contradictions of bank nationalization (1969–1990), including the Emergency interregnum; (3) post-liberalization banking (1991–2014), with a focused comparison of the Vajpayee and Singh regimes; and (4) the post-2014 reconfiguration under the BJP–NDA government, centering on the IBC’s role in asset redistribution, corporate concentration of wealth, write-offs, CoC opacity, and the erosion of the social-banking ethos.

At stake in this inquiry is not merely the technical efficiency of banking reform or the resolution of non-performing assets, but the evolving character of economic power-relations in contemporary India. By tracing this historical arc — from industrial tycoon dominance, to state-led democratization (with its authoritarian intensification during the Emergency), to liberalized hybridity with hidden fragilities, and finally to a resolution-driven regime marked by massive wealth concentration and opacity — the article highlights how transformations in banking both reflect and actively reshape the contours of development, democracy, and capitalism in India.

In an era of official narratives such as “Viksit Bharat” and “Atmanirbhar Bharat,” this analysis foregrounds the central tension between proclaimed self-reliance and the realities of financialized power, dispossession, informational enclosure, and unequal distribution of crisis burdens. The deeper questions remain:

Who ultimately bears the costs of financial distress? Who appropriates its outcomes? And who controls the knowledge through which these processes are legitimized?

It is this triad — power, distribution, and visibility — that defines the contemporary political economy of Indian banking.

I. Banking Before Nationalization (1947–1969): Retracing Public Vulnerabilities

The trajectory of Indian banking in the two decades following Independence in 1947 reveals a fundamental structural contradiction at the heart of the newly sovereign nation-state. While political power had formally passed from colonial rule, financial power remained deeply concentrated in the hands of private industrial houses and corporate tycoons. Despite the Nehruvian vision of planned economic development inspired by Fabian socialist ideals and the Soviet model of centralized planning, banking continued to function more as an extension of entrenched capitalist interests than as an instrument of broad-based national development.

At Independence, India inherited a fragile and uneven banking structure shaped by colonial priorities. The system was dominated by a relatively small number of privately owned banks, many closely aligned with powerful business houses. These banks displayed a pronounced urban bias, concentrating their operations in metropolitan and port cities such as Bombay, Calcutta, and Madras, while vast rural regions — home to the majority of the population — remained almost entirely excluded from institutional credit.

Although the Reserve Bank of India had been established in 1935, its regulatory authority in the early post-Independence years remained limited and evolving. The Banking Regulation Act of 1949 granted the RBI greater supervisory powers, yet these reforms proved insufficient to address deeper structural weaknesses. The result was a proliferation of poorly capitalized and weakly governed banks.

A defining feature of this era was “connected lending,” whereby banks extended disproportionate credit to industries and firms affiliated with their own directors or promoters. This practice led to a dangerous concentration of financial resources among a narrow circle of corporate tycoons, while sidelining sectors critical to equitable development, particularly agriculture and small-scale industries. Farmers, artisans, and small entrepreneurs were largely left to rely on informal moneylenders charging usurious interest rates.

The period was marked by recurrent bank failures that severely eroded public confidence. Between 1947 and 1969, approximately 559 private banks suffered outright collapse or liquidation, while broader estimates (including amalgamations, cessations, and transfers of liabilities) reach 665–736 institutions that effectively disappeared from the banking landscape. The instability was especially acute in the immediate post-Partition years, with over 350–361 banks failing between 1947 and 1955 alone. Notable high-profile collapses included the Palai Central Bank (1960) and Laxmi Bank, which triggered regional runs and wiped out the savings of countless ordinary depositors.

These failures stemmed from systemic weaknesses: inadequate capital bases, poor risk management, heavy reliance on connected lending to corporate tycoons, strong urban bias, and the absence of robust depositor protection (the Deposit Insurance Corporation was established only in 1961). Although the Nehruvian state pursued Five-Year Plans aimed at socialist-patterned development and heavy industry, the banking sector largely remained outside effective state control. The partial adoption of Soviet-style planning was never fully extended to finance, leaving banking misaligned with the stated goals of planned economic growth and social justice.

By the late 1960s, it had become evident to policymakers — particularly under Indira Gandhi — that the existing structure was incompatible with the objectives of equitable development. The concentration of financial power, neglect of priority sectors, and recurring crises of confidence created the conditions for a radical policy shift.

Thus, the nationalization of major commercial banks in 1969 did not emerge as an abrupt ideological intervention. It was a historically contingent response to the deep-seated failures of the pre-nationalization regime. Nationalization represented a decisive attempt to realign financial intermediation with the broader objectives of state-led (more or less) socialistic development, redistribution, and economic democratization.

II. Bank Nationalization (1969): Political Economy, Achievements, and Contradictions

The nationalization of 14 major commercial banks on 19 July 1969 (followed by six more in 1980) under Prime Minister Indira Gandhi marked a pivotal rupture in India’s postcolonial political economy. It deliberately reoriented financial power away from private industrial sections toward the developmental state, while embedding new forms of bureaucratic control, political mediation, and long-term institutional vulnerabilities. Far from an isolated ideological act, nationalization responded to structural economic failures—such as urban bias, connected lending, and recurrent bank failures—and acute political imperatives of the late 1960s.

II.A. Political Economy of Nationalization: Power, Legitimacy, and Control

By the late 1960s, Indian banking highlighted the contradictions of post-Independence capitalism: formal political sovereignty coexisted with concentrated financial power in a few business houses. Credit flowed disproportionately to large industry and urban centers, while agriculture, small enterprises, and rural regions remained underserved. This misalignment with the goals of planned economic development in the Five-Year Plans fueled growing discontent.

Economic critique merged with intense political contestation within the Congress party. The rift between the conservative “Syndicate” (led by Morarji Desai) and Indira Gandhi turned banking policy into a battleground for legitimacy and control. Desai favored incremental “social control” via board-level reforms under the Banking Laws (Amendment) Act, 1968. Gandhi responded decisively by stripping Desai of the finance portfolio and promulgating the Banking Companies (Acquisition and Transfer of Undertakings) Ordinance overnight. This dual-purpose move addressed systemic market failures while consolidating her populist authority.

Nationalization was framed in the rhetoric of “Garibi Hatao” (Remove Poverty) and redistribution. It allowed Gandhi to position herself as champion of the masses against entrenched capitalist interests, especially after the 1969 Congress split. In political-economy terms, it blended socialist developmentalism with strategic state-building: ownership of banks controlling over 80% of banking assets transferred to the Government of India. This provided a powerful tool for resource mobilization and deficit financing through elevated Statutory Liquidity Ratio (SLR) and Cash Reserve Ratio (CRR) requirements. It represented a synthesis shaped by power, legitimacy, and developmental planning in a fractious democracy, rather than pure ideology or opportunism.

II.B. Achievements: Reorienting Finance toward Inclusive Growth

Nationalization’s most tangible successes involved the geographic and sectoral democratization of banking access. Pre-1969, rural branches formed only about 18% of the network (roughly 1,443 out of ~8,000–8,187 branches), reflecting a sharp urban bias. By 1980, rural and semi-urban branches surged to over 15,000; by 1990, the total network exceeded 59,000–60,000 branches, with more than 58% located outside metropolitan centers. This expansion followed the RBI’s Lead Bank Scheme (1969) and branch licensing policies that incentivized rural outreach (e.g., the 4:1 rural-to-urban ratio under later refinements).

Population per bank branch fell sharply from around 65,000 in 1969 to under 14,000 by the early 1990s, integrating large parts of the agrarian economy into formal finance for the first time. Rural deposits and credit both grew more than twenty-fold between 1969 and 1980, with aggregate scheduled commercial bank deposits expanding at compound annual rates exceeding 15% in the 1970s. The implicit sovereign guarantee under public ownership restored public confidence eroded by pre-1969 failures (e.g., Palai Central Bank in 1960).

Complementing this was the institutionalization of priority-sector lending. Statutory targets reached 40% of net bank credit to priority sectors by 1974 (with sub-targets of 18% for agriculture and 10% for weaker sections). Agricultural advances rose from less than 2% of total credit in 1968 to about 15% (or 13% of GDP) by the mid-1980s, with absolute figures increasing nearly forty-fold between 1969 and 1980. This surge supported the second phase of the Green Revolution by enabling small and marginal farmers to adopt high-yielding varieties, irrigation, and modern inputs. Empirical studies, such as Burgess and Pande (2005), link the branch expansion in underdeveloped districts (driven by policies like the 4:1 licensing rule from 1977) to measurable reductions in rural poverty, though outcomes were amplified by complementary public investments like anti-poverty programs.

Overall, nationalization mobilized household savings on an unprecedented scale, channeling resources into planned development priorities and partially disrupting the earlier regime of “connected lending” to industrial houses (even if subtler elite influences persisted).

II.C. The Emergency Period (1975–1977): Authoritarian Consolidation and Intensified State Control

The nationalized banking framework operated under heightened state direction during the 21-month Emergency declared by Indira Gandhi on 25 June 1975. This period featured sweeping constitutional changes via the 42nd Amendment (1976), which inserted “socialist” and “secular” into the Preamble (transforming “sovereign democratic republic” into “sovereign socialist secular democratic republic”) and altered “unity of the nation” to “unity and integrity of the nation.” The 44th Amendment (1978, with process rooted in this era) later removed the Right to Property from Fundamental Rights, converting it into a legal right and further tilting the Constitution toward state-directed economic intervention, i.e., state capitalist/socialistic ideals that serve long-term ends instead of private corporate interests.

In banking, the Emergency did not trigger new nationalizations but intensified control over the existing public sector system. It reinforced priority-sector lending and developmental mandates with stricter discipline on credit allocation. Strikes and labor unrest in banks were curtailed, contributing to improved administrative efficiency and punctuality in some operations. Broader economic indicators showed temporary gains—declining inflation, modest industrial pickup, and foodgrain benefits from a good monsoon—partly attributed to enforced “discipline,” though these were also influenced by prior policy momentum and favorable external factors.

This phase represented an authoritarian consolidation of the socialist ethos embedded in 1969 nationalization. It used extraordinary powers to push redistributive and state-led policies while suspending civil liberties, imposing press censorship, and detaining political opponents. The complexity lies in its dual character: it amplified developmental momentum and state capacity in finance and planning under the banner of radical social engineering, yet at the cost of democratic norms and institutional checks. Positive elements—such as reinforced focus on inclusion and efficiency gains from discipline—coexisted with the risks of unchecked executive power and potential for patronage.

II.D. Structural Contradictions: From Private Triumph to Political Patronage

These achievements came with deep structural contradictions that haunted the system for decades. The shift from private to state ownership replaced (elitist) market-driven decisions with bureaucratic hierarchies and administrative rigidities. Banks increasingly operated as extensions of the state apparatus, leading to reduced innovation, slower decision-making, and higher operating costs.

Critically, nationalization shifted rather than eliminated concentrated influence: private capital gave way to political patronage. Socially motivated directed lending often entangled with electoral calculations. The “loan mela” culture of the 1970s—mass credit camps driven by political directives—frequently bypassed prudent appraisal and recovery, weakening credit discipline and contributing to stressed asset buildup. The regime of financial repression exacerbated this: SLR peaked at 38.5%, and high CRR levels pre-empted resources for government borrowing at below-market rates, while administered interest rates suppressed profitability.

Public sector banks faced multiple conflicting objectives—social inclusion, fiscal support to government, and commercial viability—without adequate autonomy or performance incentives. By the early 1990s, PSBs dominated over 90% of deposits and advances but showed low profitability and deteriorating asset quality. Inclusion outcomes remained uneven: while penetration improved dramatically, the most marginalized (small/marginal farmers, informal workers, women) faced barriers from procedural complexities, collateral requirements, and uneven ground-level implementation.

II.E. Historical Synthesis: A Dialectic of Inclusion and Control

Bank nationalization embodies a classic dialectic in India’s political economy:

- It dramatically expanded access and inclusion while introducing bureaucratic inefficiencies and reduced commercial orientation.

- It curbed overt private concentration of financial power while enabling new forms of political patronage and interference, which were further intensified during the Emergency’s authoritarian consolidation.

- It successfully mobilized domestic savings for developmental purposes while progressively weakening credit discipline and institutional resilience over time.

In essence, nationalization replaced one form of concentrated power — private industrial tycoons — with another: the developmental state and its political intermediaries. Yet it significantly broadened the social base of formal banking, integrating millions into institutional finance for the first time. The Emergency (1975–1977) highlighted this inherent tension: it reinforced socialist constitutional commitments through the 42nd Amendment (inserting “socialist” and “secular” into the Preamble) and related changes that removed the Right to Property from Fundamental Rights, while intensifying state control over the nationalized banking system. This period delivered some operational gains in administrative discipline and reinforced developmental focus, even as it subordinated democratic rights and civil liberties to centralized authority.

This dialectic — of inclusion paired with new forms of control, and social purpose tempered by institutional vulnerabilities — is central to understanding the trajectory of Indian public sector banks (PSBs) in subsequent decades. The structural weaknesses generated during the nationalized era, particularly political interference in lending decisions, the gradual accumulation of non-performing assets (NPAs), suppressed profitability under financial repression, and the complex trade-offs of authoritarian developmentalism, created the essential historical backdrop against which later reforms unfolded.

These contradictions would shape the challenges addressed (or reconfigured) in the post-1991 liberalization phase and beyond.

III. Post-Liberalization Banking (1991–2014): Reform, Expansion, Crisis Absorption, and the Seeds of Systemic Stress

The period from 1991 to 2014 marked a profound, if uneven, transformation in Indian banking: from a predominantly state-directed developmental model to a hybrid system blending prudential regulation, limited market competition, and persistent public-sector dominance. Initiated under the Narasimham Committees (1991 and 1998) amid the broader economic liberalization triggered by the 1991 balance-of-payments crisis, this era progressively introduced capital adequacy norms, income recognition and asset classification (IRAC) standards, reduction in statutory pre-emptions, and the entry of new private and foreign banks. Public sector banks (PSBs) retained their commanding share of deposits and advances (often exceeding 70–75 per cent), yet their operational environment was reshaped by greater competition, technological adoption, and alignment with global standards.

This phase was not a clean rupture from the nationalized era but a gradual recalibration. It delivered macroeconomic stability and financial deepening while sowing structural vulnerabilities. The embrace of neoliberal globalization—marked by deregulation, openness to global capital flows, and market-oriented incentives—exposed the banking system to new pressures. While promising efficiency and growth, it often prioritized short-term credit expansion and corporate leveraging over sustainable risk management, setting the stage for deferred fragilities.

This section compares the two dominant political regimes within the post-1991 framework:

- The National Democratic Alliance (NDA) government under Prime Minister Atal Bihari Vajpayee (1998–2004), characterized by cautious consolidation and infrastructure-led credit expansion.

- The United Progressive Alliance (UPA) government under Prime Minister Manmohan Singh (2004–2014), defined by aggressive credit growth, successful absorption of the 2008 Global Financial Crisis (GFC), and the subsequent emergence of hidden fragilities.

The comparison reveals a dialectic: Vajpayee-era stability laid foundations for growth, while the UPA period achieved remarkable resilience during the global shock but at the cost of accumulating stressed assets that crystallized as the “Twin Balance Sheet” (TBS) problem by 2014.

III.A. Structural Reforms of the 1990s: Foundations of Prudential Capitalism

The Narasimham Committee I (1991) and II (1998) provided the intellectual and policy blueprint. Key recommendations—implemented incrementally across governments—included raising the Capital to Risk-Weighted Assets Ratio (CRAR) to 8 per cent (later 9 per cent), introduction of IRAC norms (classifying assets as standard, sub-standard, doubtful, and loss), reduction in Statutory Liquidity Ratio (SLR) from 38.5 per cent to 25 per cent and Cash Reserve Ratio (CRR) from 15 per cent to lower levels, phased deregulation of interest rates, and permission for private-sector banks (e.g., ICICI Bank, HDFC Bank) and foreign banks to expand. Directed lending targets were retained but refined, and priority-sector norms were made more flexible.

The immediate impact was a sharp improvement in asset quality. Gross Non-Performing Assets (GNPA) of PSBs, which had reached alarming levels (~14.7% system-wide peak in the late 1990s under earlier classifications), declined steadily through the 1990s and early 2000s. By the early 2000s, system-wide GNPA ratios had fallen to single digits (around 7–10 per cent by 2002–03, and further to ~2–3 per cent by 2007–08). Recapitalization exercises strengthened PSB balance sheets, while new private banks introduced technology-driven efficiency and urban-focused lending. The result was a dual banking structure: PSBs retained their developmental and rural reach, while private banks excelled in profitability, innovation, and risk management. This hybridity set the stage for the subsequent political regimes’ divergent approaches.

III.B. NDA Era (1998–2004): Consolidation, Disinvestment, and the Infrastructure Foundation

Under Atal Bihari Vajpayee, banking policy emphasized prudent continuation of 1990s reforms rather than radical privatization or deregulation. The government strengthened supervisory frameworks, aligned prudential norms further with Basel standards, and improved risk management through better asset classification and provisioning. The Department of Disinvestment was established (later elevated to a ministry), and strategic disinvestment was pursued in non-strategic PSUs (e.g., BALCO, Hindustan Zinc, VSNL, IPCL), raising substantial resources while sparking debate on reducing government stakes in PSBs (Narasimham II had recommended lowering it below 51 per cent). Political resistance, however, prevented large-scale bank privatization; PSBs remained majority state-owned.

A defining feature was the infrastructure push, which began reshaping credit allocation. The Golden Quadrilateral highway project (launched 2001) and Pradhan Mantri Gram Sadak Yojana (PMGSY, 2000) triggered increased long-gestation lending by PSBs to roads, power, and related sectors. Credit growth was moderate but targeted: non-food bank credit expanded steadily (around 15–20 per cent annually in real terms), with a shift toward productive infrastructure. GNPA ratios continued their downward trajectory (falling to low single digits by 2003–04), reflecting tighter norms, moderate leverage, and an absence of speculative bubbles. GDP growth averaged around 6 per cent annually during the period (peaking at 7.9 per cent in 2003–04), supported by fiscal consolidation via the Fiscal Responsibility and Budget Management (FRBM) Act, 2003.

The NDA phase thus delivered relative stability and latent capacity-building. It avoided the excesses of rapid leverage while laying the physical and policy groundwork for the high-growth neoliberal decade that followed. No major global shock tested the system, but the era’s measured approach masked emerging vulnerabilities in long-gestation project financing that would intensify later under conditions of accelerated globalization.

III.C. UPA Era (2004–2014): Credit Boom, Crisis Resilience, and Emerging Fragilities

The UPA decade under Manmohan Singh represented both the zenith of post-liberalization expansion and the incubation of systemic stress. It can be divided into two distinct phases.

(i) Pre-Crisis Boom (2004–2008): Optimism and Leveraged Expansion

India recorded exceptionally high GDP growth (averaging 8–9 per cent), fueled by a massive credit surge amid global liquidity and neoliberal integration. Non-food bank credit roughly doubled between 2004–05 and 2008–09—the fastest such expansion in India’s history. Total bank advances grew from approximately ₹10–12 lakh crore in the early 2000s to over ₹23 lakh crore by 2008 (with further acceleration thereafter). PSBs, still dominant in corporate and infrastructure lending, financed mega-projects in power, roads, steel, telecom, and real estate through public-private partnerships (PPPs) and leveraged corporate expansions. Corporate debt-equity ratios rose sharply as firms, buoyed by high profitability and global capital inflows, abandoned conservative leverage norms. Priority-sector lending continued, but the dominant thrust was toward infrastructure, which absorbed a disproportionate share of incremental credit. This phase exemplified the double-edged nature of neoliberal globalization: rapid growth through financial deepening, but at the risk of over-leveraging and sectoral imbalances.

(ii) The 2008 Global Financial Crisis: Effective Shock Absorption

One of the UPA government’s most notable achievements was the relative insulation and swift recovery of the Indian banking system and broader economy from the GFC. Unlike Western institutions, Indian banks had negligible direct exposure to toxic sub-prime derivatives or complex securitized products, thanks in part to conservative regulatory oversight (a legacy of the nationalized and early post-1991 eras) and limited integration into global financialization. Deposits actually shifted toward PSBs, reflecting public trust in sovereign backing. System-wide GNPA ratios remained low (~2.3 per cent in 2008–09), and no major bank failures occurred.

The policy response was swift and coordinated. The RBI slashed the CRR by 250 basis points (October–November 2008), introduced a second Liquidity Adjustment Facility (LAF) window, and cut policy rates aggressively. The government announced three fiscal stimulus packages between December 2008 and February 2009 (totaling ~₹1.86 lakh crore or 3.5 per cent of GDP), alongside sector-specific relief for exports, SMEs, and housing. Liquidity infusion exceeded ₹5 lakh crore (nearly 9 per cent of GDP). These measures—combined with pre-existing capital buffers and partial insulation from global financialization—prevented a credit crunch or systemic collapse. GDP growth dipped to 6.7 per cent in 2008–09 but rebounded strongly to 8–9 per cent by 2010–11. The masses were largely shielded: rural demand remained resilient (supported by the farm-loan waiver and MGNREGA), inflation was contained post-crisis, and employment impacts were far milder than in advanced economies. This resilience highlighted the continued value of public-sector buffers and counter-cyclical policy, even as neoliberal openness amplified external shocks.

(iii) Post-Crisis Phase (2009–2014): Hidden Fragilities and the NPA Build-Up

The very policies that cushioned the crisis—sustained credit expansion to maintain growth momentum—masked deeper problems. To counteract the global slowdown, banks (especially PSBs) continued aggressive lending to already-stressed infrastructure and corporate sectors, often through restructuring and evergreening rather than recognition of impairment. Policy paralysis (delays in land acquisition, environmental clearances, and project execution) combined with global commodity price collapses (post-2011) and domestic governance issues to erode project viability. By 2014, stressed assets (including restructured loans) reached approximately 9–10 per cent of total advances, while reported GNPA stood at ~4.1 per cent (₹2.5 lakh crore). These figures significantly understated the true distress due to regulatory forbearance. Sectoral concentration was acute: power, roads, steel, telecom, and real estate accounted for the bulk of stress, with PSBs bearing a disproportionate burden (owing to their dominance in corporate lending and implicit pressure to support growth). Empirical analyses consistently show sharper NPA deterioration in PSBs than in private banks post-2008. The neoliberal emphasis on rapid credit-led growth thus amplified vulnerabilities when external conditions turned adverse.

III.D. Comparative Evaluation: Vajpayee vs. Manmohan Singh Regimes

The table below summarizes key dimensions using RBI and official data:

| Dimension | Vajpayee (NDA, 1998–2004) | Manmohan Singh (UPA, 2004–2014) |

|---|---|---|

| Reform Orientation | Consolidation of 1990s prudential norms; disinvestment in non-bank PSUs | Expansion within liberalized framework; focus on credit-led growth |

| Credit Growth | Moderate (15–20% annually); infrastructure foundations laid | Aggressive (non-food credit doubled 2004–09; 20–30%+ peaks pre-2008) |

| NPA Trends | Steady decline (from high double-digits in late 1990s to low single-digits by 2003–04) | Low until 2008 (~2.3%); gradual rise post-2009, reaching ~4.1% GNPA + 9–10% stressed assets by 2014 |

| Infrastructure Lending | Initiated major projects (Golden Quadrilateral, PMGSY) | Massive scaling; led to over-leveraging in power, steel, roads |

| Crisis Management | No major global shock; fiscal prudence via FRBM Act | Successful absorption of 2008 GFC via stimulus and liquidity; minimal impact on masses |

| State Role | Gradual retreat debated but PSBs dominant | Strong counter-cyclical intervention; PSBs as growth engines |

| Structural Outcome | Stability with emerging project-finance risks | High growth with embedded fragility (TBS problem origins) |

III.E. Deferred Crisis and the Twin Balance Sheet Problem

The 1991–2014 period ended in a paradox. The Vajpayee years provided disciplined foundations; the UPA years delivered spectacular growth and crisis resilience—achievements that protected ordinary citizens from the worst of the 2008 shock through fiscal-monetary coordination and regulatory buffers. Yet the same credit boom that sustained 8–9 per cent growth also generated India’s largest accumulation of stressed assets in history. Over-leveraged corporates (especially in infrastructure) and weakened PSB balance sheets constituted the TBS problem, whose roots lay in mid-2000s optimism, policy delays, and post-crisis forbearance. By 2014, credit growth had slowed dramatically, asset quality had deteriorated (with true stress concealed), and the banking system—though still stable—required urgent mechanisms to address accumulated fragilities.

This accumulated stress formed the critical historical backdrop for subsequent reforms. The contradictions of the post-liberalization hybrid model—efficiency gains alongside vulnerabilities amplified by neoliberal globalization’s emphasis on leverage, global integration, and market discipline—would shape debates on balancing commercial viability with the developmental and inclusionary roles inherited from the nationalized era.

III.F. The Global Neoliberal Architecture: World Bank–IMF Conditionality and the Pre-Debt-ory Turn

The post-1991 liberalization did not occur in a vacuum. It was deeply shaped by the structural adjustment framework advanced by the World Bank and IMF, which conditioned balance-of-payments support on financial deregulation, capital account opening, reduction in statutory pre-emptions, and alignment with Basel prudential norms. What was presented as technical modernization was, in reality, the imposition of a neoliberal template that prioritized market discipline, private capital mobility, and fiscal austerity over the postcolonial mandate of directed credit and social inclusion.

As the 2009 international thriller The International lays bare in its unflinching monologue, the essence of this architecture is captured by the banker who declares: “The IBBC is a bank. Their objective isn’t to control the conflict, it’s to control the debt that the conflict produces. You see, the real value of a conflict, the true value, is in the debt that it creates. You control the debt, you control everything… this is the very essence of the banking industry, to make us all, whether we be nations or individuals, slaves to debt.” Hence, this global regime funds both individual or group-based “terrorism” and, at the same time, state terrorism—yet the underlying actors remain the same in both situations or cases. Wars, insurgencies, and geopolitical instability are not ends in themselves; they are debt-generating machines whose perpetual servicing locks entire economies into cycles of dependency, surveillance, and extraction.

This global regime fostered a predatory, debt-oriented economy—one structurally oriented toward perpetual debt rollover, speculative inflows, and short-term portfolio capital rather than long-term investment. Financial liberalization expanded the role of banks in channeling volatile global liquidity into domestic corporate leverage and infrastructure bets, while weakening regulatory firewalls inherited from the nationalized era. In this architecture, banks increasingly functioned less as engines of development and more as conduits for cross-border financialization—facilitating round-tripping, evergreening, and, in extreme cases, money laundering of illicit flows through layered instruments and offshore linkages (examples of banks that reportedly or allegedly perform this role include CITI Bank, Standard Chartered, HSBC, Axis Bank, HDFC Bank, and ICICI Bank).

The result was a moral and institutional mutation: bankers morphed into banksters, whose incentives aligned with fee generation, balance-sheet window-dressing, and corporate accommodation rather than prudent risk assessment or broad-based intermediation. The 2008 Global Financial Crisis was absorbed precisely because of residual public-sector buffers, yet the underlying logic—debt-led growth under external conditionalities—laid the groundwork for the massive stressed-asset buildup that later justified the post-2014 resolution regime. Far from neutral technocratic advice, World Bank–IMF prescriptions helped dismantle the social-banking ethos, embedding India within a global financial order that socializes systemic risks while privatizing speculative gains.

In the end, The International’s chilling insight reveals what the post-1991 project truly accomplished: it did not merely “open” the Indian economy—it subordinated it to a borderless debt regime where control of the ledger trumps control of the land, the factory, or the ballot box. Nations become borrowers first, sovereigns second; citizens become interest-bearing units in a ledger that never balances, only compounds. The same institutions that lecture on fiscal prudence are the ones that profit from its perpetual violation—ensuring that the debt machine keeps turning, conflict after crisis after bailout, while the underlying actors, whether in boardrooms or war zones, remain indistinguishable in their pursuit of the ultimate commodity: leveraged dependency.

IV. Political Economy under the BJP–NDA Regime (2014–2026): From Crisis Recognition to Massive Crony Concentration

The period since 2014 under the Narendra Modi-led BJP–NDA government has represented a radical and deliberate reconfiguration of India’s banking and financial architecture. What has been officially framed as “reform, transparency, efficiency, and resolution” has, in practice, accelerated the abandonment of the postcolonial social-banking mandate established in 1969.

Public sector banks (PSBs), once instruments of developmental inclusion and equitable credit allocation, have been systematically transformed into vehicles for the socialization of massive losses while enabling the privatization of distressed assets to a narrow circle of politically connected conglomerates. This era has witnessed not the genuine resolution of systemic fragility but its cynical instrumentalization to entrench crony-duopoly capitalism—dominated by groups such as the Adani, Ambani, and Piramal empires—amid soaring wealth and income inequality, persistent poverty and hunger, and the effective impunity of high-profile wilful defaulters and fugitives. Flagship “reforms” touted as bold leaps forward—Demonetization (2016), GST (2017), and the Insolvency and Bankruptcy Code (IBC, 2016)—have instead proven spectacular failures that disproportionately devastated the informal sector, MSMEs, and ordinary citizens while shielding and enriching a handful of favoured tycoons. Official narratives of “Viksit Bharat” and “Atmanirbhar Bharat” have served as ideological shields for aggressive market fundamentalism, resource privatization, dispossession of the masses, and the wholesale transfer of public wealth into private hands.

IV.A. Flagship “Reforms” as Instruments of Crony Consolidation: Demonetization, GST, and IBC

Demonetization (November 2016) was sold as a surgical strike against black money, corruption, and counterfeit currency. In reality, it was an economic disaster that inflicted disproportionate pain on the informal economy, which employs the vast majority of India’s workforce. Overnight invalidation of 86% of currency in circulation triggered widespread cash chaos, crippling small businesses, farmers, daily-wage labourers, and rural economies. RBI data later confirmed that 99.3% of the demonetised notes (₹15.3 lakh crore out of ₹15.41 lakh crore) returned to the banking system, rendering the black-money objective a complete failure. The move is estimated to have shaved 0.5–2 percentage points off GDP growth in 2016–17, led to the loss of over 1.5 million jobs (particularly in MSMEs and the unorganised sector), and caused widespread hardship—including reported deaths linked to cash shortages and distress. Far from cleansing the system, it facilitated money laundering through organised networks and provided a temporary deposit surge to PSBs that masked underlying weaknesses rather than resolving them.

The Goods and Services Tax (GST, rolled out in July 2017) was similarly projected as a transformative “one nation, one tax” reform. Instead, its hasty and poorly designed implementation—complex rate slabs, compliance burdens, and frequent tweaks—devastated MSMEs through input-tax credit delays, higher compliance costs, and working-capital strains. Initial revenue shortfalls and implementation chaos compounded the damage from demonetization, further slowing growth and formal-sector job creation. While large corporates adapted through scale and technology, small producers and traders faced closures, job losses, and exclusion. Critics rightly note that GST, like demonetization, disproportionately burdened the masses and informal economy while easing the path for big capital consolidation.

Together with the Insolvency and Bankruptcy Code, 2016 or IBC, 2016 (to be discussed in detail soon!), these three signature initiatives form a triad of failed “reforms” that have not protected public money but actively shielded cronies. Demonetization and GST created economic distress that fed into the NPA crisis; the IBC then provided the mechanism to transfer the resulting distressed assets at fire-sale prices to politically connected players. The net result has been the hollowing out of the developmental state and its replacement by a facilitator of crony concentration.

IV.B. The NPA Crisis: Inherited Fragility, Politically Weaponized Recognition

The surge in non-performing assets (NPAs) after 2014 was not primarily “created” under the BJP but dramatically recognized and disclosed through the Reserve Bank of India’s Asset Quality Review (AQR) initiated in 2015 under Governor Raghuram Rajan. Gross NPAs of scheduled commercial banks (SCBs) rose from approximately 4 per cent in 2014 to a peak of 11.2–11.5 per cent by 2017–18 (with PSBs bearing the brunt at over 14–15 per cent in some years). In absolute terms, stressed assets exceeded ₹10 lakh crore at their height. While the UPA-era credit boom (2004–2014) had sowed the seeds through over-leveraged infrastructure and corporate lending, the post-2014 regime used the AQR to project a narrative of “cleaning up the mess” inherited from the previous government. Yet this recognition came at enormous public cost: PSBs were recapitalized with over ₹3 lakh crore in direct government infusions between 2015 and 2021, supplemented by massive market borrowings. By 2026, GNPA ratios have fallen to historic lows—2.15 per cent for SCBs and 2.50 per cent for PSBs as of September 2025—largely through aggressive write-offs rather than genuine recovery or structural reform. This cosmetic cleanup has masked a deeper transfer of burden onto taxpayers and depositors while clearing the balance sheets for fresh rounds of crony lending and asset acquisition.

Table – Gross NPA Ratio of Scheduled Commercial Banks (SCBs) – Select Years

| Year (as on March 31) | GNPA Ratio (SCBs, %) | GNPA Ratio (PSBs, %) | Approximate GNPA Amount (₹ lakh crore, SCBs) | Notes |

|---|---|---|---|---|

| 2014 | ~4.0 | ~4.5–5.0 | ~2.5 | Pre-AQR baseline |

| 2015–16 | ~7.5–8.0 | Higher | Rising rapidly | AQR impact begins |

| 2016–17 | ~9.0–10.0 | ~12–13 | ~6–7 | Sharp increase |

| 2017–18 (Peak) | 11.2–11.5 | 14.5–15.0+ | ~10.3–10.6 | Highest level; PSBs bore bulk |

| 2018–19 | ~9.1–9.3 | ~13–14 | ~9.3 | Beginning of decline via write-offs |

| 2021 | ~9.1 (earlier) → declining | ~12+ → falling | ~6.2 | Recapitalization heavy |

| Sept 2025 (Latest) | 2.15 | 2.50 | ~4.7–4.8 (estimated) | Historic low via write-offs impacting public money without any genuine systemic recovery |

IV.C. Loan Write-Offs and/or Waivers: Socializing Losses for the Superrich – An Exercise in Orwellian Doublespeak?

Between 2014–15 and 2023–24, Indian commercial banks wrote off approximately ₹12–16.35 lakh crore in bad loans (with cumulative figures reaching around ₹16.35 lakh crore over the decade in some official disclosures), with Public Sector Banks (PSBs) accounting for the overwhelming share — including over ₹6.5 lakh crore in the last five years alone and ₹6.15 lakh crore in the 5.5 years up to September 2025.

These so-called “write-offs” — technically accounting adjustments that remove loans from balance sheets after full provisioning, without formally forgiving the borrower’s liability — have overwhelmingly benefited large corporate borrowers and wilful defaulters. In official parlance, this is presented as prudent housekeeping and “cleaning up” of balance sheets. In reality, it functions as a waiver for the superrich, dressed up in technocratic language — a classic example of Orwellian doublespeak. What is euphemistically called a “write-off” effectively waives the recovery pressure on powerful defaulters, while the public exchequer and ordinary depositors bear the permanent loss.

Recovery rates from these written-off accounts have been abysmal (often 15–30 per cent, with some periods showing even lower realizations), meaning the bulk of public money has simply vanished into thin air. In stark contrast, farm-loan waivers — a populist measure routinely criticized and condemned by the same regime as fiscally irresponsible and damaging to credit culture — have totalled far less over the same period (roughly ₹1.67 lakh crore for agriculture and allied sectors against nearly ₹9.87 lakh crore in corporate write-offs in comparable recent data, representing only about 14–15 per cent of the total relief extended).

The political economy is unambiguous and deeply cynical: the regime preaches strict “credit discipline” and moral hazard for the poor and the informal sector, while extending de facto impunity and massive relief to elite defaulters through this sanitized mechanism of “write-offs.” PSBs, still majority state-owned, have absorbed these losses through repeated recapitalization funded by taxpayers. In effect, private corporate defaults have been converted into taxpayer-funded bailouts on a colossal scale.

This is the complete antithesis of the 1969 social-banking ethos. Under nationalization, banking was meant to serve broad developmental and redistributive goals. Today, losses are systematically socialized onto the public — via recapitalization, depositor burdens, and foregone public expenditure — while any residual value or upside from restructured assets is privatized and captured by a narrow circle of powerful borrowers and acquirers. The linguistic sleight-of-hand — calling elite waivers “write-offs” while denouncing farmer relief as “waivers” — perfectly captures the regime’s double standards: moral lectures for the many, generous accounting forgiveness for the few.

The scale of this transfer underscores a deeper structural shift: public sector banks have been repurposed not as engines of inclusive growth, but as mechanisms to absorb the costs of crony lending and then facilitate the transfer of cleaned assets to favoured hands. What is presented as technical banking hygiene is, in truth, a massive upward redistribution of wealth masked by bureaucratic euphemism.

IV.D. High-Profile Wilful Defaulters and Fugitives: Structuring Impunity

A short list of emblematic cases underscores the selective enforcement and structural impunity that has become a defining feature of the regime:

- Vijay Mallya (Kingfisher Airlines): Defaulted on over ₹9,000 crore; fled to the UK in 2016. Extradition proceedings remain ongoing despite Interpol Red Corner Notices; UK courts have cited prison conditions, and as of 2026 he continues to fight return.

- Nirav Modi (Punjab National Bank scam): Involved in the ₹13,000+ crore fraud; in UK custody but extradition stalled by appeals. UK officials inspected Tihar Jail in 2025, yet no handover has occurred.

- Mehul Choksi (linked to the same PNB fraud): Fled to Antigua, later detained in Belgium (April 2025); Belgium’s Supreme Court dismissed his appeal in December 2025, but extradition remains protracted.

Despite repeated diplomatic efforts and Interpol “red” notices, these high-profile fugitives — whose defaults run into tens of thousands of crores — have evaded full justice for over a decade. The government’s routine claims of “pursuing vigorously” ring hollow against the structural reality: transnational legal hurdles, host-country asylum processes, and a palpable absence of political will to confront the broader ecosystem of crony lending that enabled their rise. Public money remains at stake, while ordinary depositors and taxpayers continue to subsidize the fallout.

This selective impunity at the top stands in even starker contrast when viewed against the actual explosion in the overall number of wilful defaulters during the post-2014 BJP–NDA regime. Verified data from the Reserve Bank of India and Credit Information Companies, placed before Parliament, reveal a dramatic surge in both the volume and value of wilful defaults since 2014:

Table – Wilful Defaulters (₹25 lakh and above, suit-filed accounts) – Verified Trend

| Year (as on March 31) | Number of Wilful Defaulters | Outstanding Amount (₹ crore) | Increase Factor (vs 2014) |

|---|---|---|---|

| 2014 | 5,076 | ~39,369 | Baseline |

| 2016 (early Modi) | 9,070 | 89,889 | ~1.8× (number) / ~2.3× (amount) |

| 2025 (latest) | 18,318 | 3,83,264 (₹3.83 lakh crore) | 3.6× (number) / ~9.7× (amount) |

Key facts from official data:

- The number of wilful defaulters has risen sharply from 5,076 in March 2014 to 18,318 by March 2025 — an increase of over 3.6 times.

- The total outstanding amount has exploded nearly 10-fold, reaching a decade-high of ₹3.83 lakh crore in 2025 (even after a marginal dip from the FY24 peak of 18,876 cases).

- Public sector banks continue to bear the bulk of these defaults, with the quantum of money involved hitting record levels despite the much-touted “clean-up” narrative.

In other words, far from curbing the problem, the regime has presided over a massive proliferation of wilful defaults among large borrowers. While a handful of high-profile fugitives like Mallya, Nirav Modi, and Choksi remain beyond reach, the overall ecosystem of elite impunity has expanded dramatically — even as small defaulters and farmers face aggressive recovery drives, asset seizures, and public shaming. This is not enforcement failure; it is the structured outcome of a system that protects the superrich while socialising their losses onto the public. The data lay bare the hollowness of the regime’s rhetoric on credit discipline: it applies rigorously to the weak and selectively to the powerful.

IV.E. The Insolvency and Bankruptcy Code (IBC, 2016): Clean Slate Doctrine, Structural Impunity, and Insolvency-era Capitalism

The IBC was touted as a transformative reform promising time-bound resolution and improved creditor rights. In reality, its operational record reveals a systematic bias toward large corporate acquirers. The enactment of the Insolvency and Bankruptcy Code (IBC) in 2016 under the Narendra Modi-led BJP–NDA government has been officially celebrated as a landmark reform — a decisive instrument to resolve the inherited non-performing assets (NPA) crisis, maximize asset value, and strengthen creditor rights through time-bound insolvency proceedings. In practice, however, the IBC has institutionalized a regime of “resolution capitalism” that systematically socializes losses onto public sector banks (PSBs) and taxpayers while privatizing gains for a narrow set of politically connected corporate acquirers. Far from a neutral technocratic fix, the Code — repeatedly amended (over 35 times since inception), judicially interpreted, and operationally skewed — has functioned as a mechanism of structural impunity, enabling what critics term a “bankruptcy bazaar”: the engineered transfer of public wealth into private hands under the guise of efficiency and “ease of doing business.” As one more failed project in the Modi regime’s reform trilogy, it has prioritised crony protection over public money. Cumulative recoveries under the IBC have reached approximately ₹4.1 lakh crore by late 2025, but average recovery rates hover at 32–35 per cent of admitted claims—translating to haircuts of 65–68 per cent (and as high as 80 per cent in major cases). Recent quarters have seen recoveries dip to as low as 20 per cent. Large resolutions have disproportionately transferred distressed assets—ports, power plants, infrastructure, and financial entities—to favoured conglomerates at steep discounts. The code’s frequent amendments (over a dozen since enactment) and judicial interventions have introduced uncertainty that benefits well-connected bidders. Section 32A’s “clean slate” provision, combined with undervaluation of avoidance transactions (e.g., fraud recoveries valued at nominal Re 1 in certain high-profile cases), has enabled acquirers to secure massive windfalls while PSBs and retail creditors bear the brunt. Far from resolving the “twin balance sheet” problem equitably, the IBC has institutionalized a regime of resolution capitalism: public losses are absorbed via recapitalization and write-offs; private profits accrue to a handful of tycoons.

(i) The “Clean Slate” Doctrine: Legal Innovation or Engineered Impunity?

At the core of the IBC lies the “clean slate” principle, most powerfully embodied in Section 32A, inserted retrospectively via the 2019 Ordinance and given immediate effect. This provision grants successful resolution applicants (SRAs) immunity from all pre-commencement criminal liabilities, prosecutions, attachments, and confiscations attaching to the corporate debtor. While ostensibly designed to incentivise bids, ensure business continuity, and maximise recoveries, its practical operation severs liability from asset ownership. The corporate entity undergoes a juridical metamorphosis: past offences — including fraud and money laundering — are extinguished for the new owner, while the underlying assets remain intact and de-risked.

This creates a profound asymmetry. Creditors (predominantly PSBs) absorb massive haircuts; the new acquirer inherits a liability-free enterprise. Empirical patterns confirm the distributive bias: average recoveries under the IBC have hovered at approximately 32 per cent of admitted claims as of September 2025 (implying 68 per cent haircuts overall), with recent quarters declining to around 25 per cent. Avoidance transactions (Sections 43–51 and 66–67), intended to recover fraudulent diversions, are routinely undervalued — often assigned a notional Re 1 — and transferred wholesale to the SRA, privatising potential upside while public creditors bear the immediate loss.

(ii) Section 32A versus Section 66: The Normative Contradiction

A central incoherence lies in the tension between Section 32A (immunity post-resolution) and Section 66 (action against fraudulent or wrongful trading, in effect benefitting all the creditors). In practice, Section 32A has systematically overridden the deterrent intent of Section 66. Fraudulent conduct is acknowledged in forensic audits but rendered toothless once a resolution plan is approved under the doctrine of “commercial wisdom.” This is not an incidental flaw but a structural feature: the IBC privileges expediency over accountability, converting corporate wrongdoing into a temporary inconvenience that is legally laundered through the resolution process.

(iii) The Committee of Creditors (CoC): Sovereignty Without Accountability

The IBC vests near-absolute decision-making power in the Committee of Creditors (CoC), dominated by financial creditors (primarily PSBs). Judicial doctrine — repeatedly affirmed by the Supreme Court — treats the CoC’s “commercial wisdom” as largely non-justiciable, reducing oversight by the National Company Law Tribunal (NCLT), National Company Law Appellate Tribunal (NCLAT), and higher courts to procedural ritual. Stakeholders such as retail depositors, operational creditors, employees, and public-interest claimants are systematically marginalized. In high-profile cases, promoter offers of full repayment have been ignored, competing bids sidelined, and avoidance recoveries assigned at nominal value to favoured SRAs. The result is opacity, bias, and the effective transformation of insolvency into a creditor-driven market transaction insulated from broader considerations of equity or public interest.

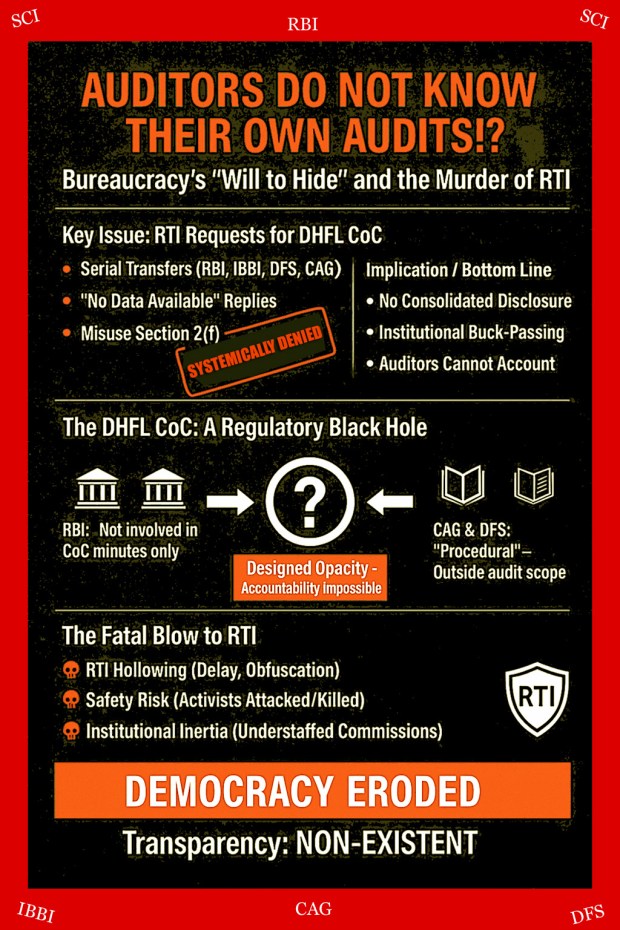

(iv) Opacity of the CoC: Auditors Do Not Know Their Own Audit Book — The DHFL Case

A critical yet systematically under-examined dimension of the Committee of Creditors (CoC) under the Insolvency and Bankruptcy Code is its profound operational opacity, particularly in high-stakes resolutions involving public money and retail stakeholders. While the IBC vests the CoC with near-sovereign decision-making authority under the judicially sanctified doctrine of “commercial wisdom,” the informational and accountability architecture surrounding its functioning remains deliberately constrained. This opacity is not an accidental byproduct of complexity but a functional feature that shields decision-making from meaningful scrutiny, diffuses responsibility, and entrenches structural impunity.

The resolution of Dewan Housing Finance Corporation Limited (DHFL) exemplifies this crisis of auditability. Even formal oversight mechanisms — including auditors, valuers, and regulatory bodies — have failed to provide a coherent, verifiable account of key processes, valuations, expenditures, and voting outcomes. Multiple civil-society interventions and persistent Right to Information (RTI) filings have documented a pattern in which transparency is ritualistically promised but substantively withheld.

In the DHFL process, the auditing and valuation framework was repeatedly characterised as “too opaque.” Discrepancies emerged between the reported book value (approximately ₹93,700 crore), alleged fraud amounts (around ₹33,000 crore in one forensic application), the successful resolution applicant’s (SRA) bid value (₹32,250–37,250 crore), and the resulting unaccounted gaps (estimated at ₹28,450 crore or more). RTI responses from the Reserve Bank of India (RBI) and other institutions proved especially revealing: queries seeking itemised details of CoC expenditures elicited uniform replies of “Information not available,” “Records not traceable,” or that “the auditor is not aware” of their own audits. Due diligence data rooms, meeting minutes, and voting records were often accessible only in restricted, non-downloadable image formats — or not at all to retail depositors. The result is performative auditing: formal reports exist, yet the underlying data and decision logic remain shielded.

This decoupling of audit from accountability transforms the audit function into a legitimising ritual rather than a substantive safeguard. When those tasked with certifying financial truth operate within a structure where that truth is partially inaccessible or unverifiable, the entire resolution process risks devolving into managed opacity. Efforts by affected stakeholders — particularly the approximately 2.5 lakh retail fixed-deposit (FD) and NCD holders — to pierce this veil through the Right to Information Act encountered systematic resistance, including serial transfers between institutions (RBI → IBBI → Department of Financial Services → CAG), routine denials citing “commercial sensitivity” or “confidentiality,” and claims that the authority “does not hold” the information.

The opacity of the CoC carries direct distributive consequences. Small depositors, retirees, and retail investors — who bore disproportionate haircuts (often 54–77 per cent in the DHFL case) — were effectively excluded from meaningful participation. They lacked access to the informational basis of CoC decisions, while institutional creditors (dominated by PSBs) exercised overwhelming voting power. Competing proposals offering higher recoveries, including full repayment offers from the former promoter, were sidelined without adequate justification or transparent deliberation. Judicial deference to the CoC’s “commercial wisdom” further weakened avenues of appeal. Even when NCLAT noted procedural irregularities, undervaluation concerns, and disproportionate losses to small investors, the Supreme Court ultimately upheld the resolution plan in its judgment dated 1 April 2025, reinforcing the limited justiciability of CoC decisions.

In the DHFL episode, this opacity manifested in the transfer of substantial avoidance claims (valued in thousands of crores) at a notional Re 1 to the SRA, while retail creditors absorbed irrecoverable losses and PSBs required taxpayer-funded recapitalisation. Admitted to the Corporate Insolvency Resolution Process (CIRP) in December 2019 following RBI supersession, DHFL’s assets (exceeding ₹90,000–91,000 crore) were acquired by entities linked to Ajay Piramal via a ₹37,000–37,250 crore resolution plan approved in June 2021. Forensic audits had identified avoidance transactions worth ₹45,000–47,000 crore, yet these were assigned nominal value and transferred to the SRA. Section 32A was invoked to discharge the corporate debtor from a ₹5,050 crore money-laundering case under the Prevention of Money Laundering Act (PMLA). Post-resolution, the rebranded Piramal Finance reported robust growth, while public depositors and PSBs absorbed the losses. Political linkages, including substantial electoral-bond donations to the BJP and prior business associations, underscore the perception of engineered favouritism.

The DHFL case demonstrates that the IBC, while formally rule-bound and procedurally elaborate, operates in practice within a framework that centralises power in the CoC while systematically constraining democratic access to information. The paradox of auditors who “do not know their own audit book” is symptomatic of a deeper malaise: the subordination of transparency and accountability to expedited resolution and favoured asset transfers.

This raises a fundamental question for India’s political economy of finance: Can a regime that concentrates decisive authority in unaccountable institutional bodies, while simultaneously eroding RTI efficacy and audit verifiability, legitimately claim to deliver fairness, efficiency, or public interest? In the transition from social banking to resolution capitalism, the opacity of the CoC reveals not a technical flaw but a structural logic that prioritises private appropriation over public accountability.

(v). Legal Incoherence, Institutional Overlap, and Market Fundamentalism

The IBC does not function in isolation. Its interactions with the Prevention of Money Laundering Act (PMLA), the SARFAESI Act (2002), and other statutes produce normative fragmentation: jurisdictional ambiguities, selective enforcement, and the privileging of financial creditors over public-interest claims (tax authorities, provident funds, municipal dues). Over 77 per cent of cases have breached the statutory 270-day timeline, often extending beyond 700 days, eroding asset value and burdening the judiciary. Repeated amendments have exacerbated doctrinal confusion rather than resolving core flaws. Ideologically, the IBC is embedded in the broader Modi-era discourse of “ease of doing business” and market-led restructuring. This narrative obscures the distributive reality: PSBs are recapitalised with taxpayer funds (over ₹3 lakh crore in the initial post-2014 phase, with cumulative write-offs exceeding ₹12–16 lakh crore since 2014–15); distressed assets are acquired at fire-sale valuations by conglomerates; and recovered capital often recycles into political donations, reinforcing crony loops.

(vi). From Resolution to Redistribution: Socialising Losses, Privatising Gains

Across major IBC resolutions (Videocon, Essar Steel, Aircel, Reliance Communications, and others), the pattern is consistent: haircuts of 65–96 per cent borne disproportionately by PSBs and retail creditors; undervalued avoidance claims transferred to SRAs; and subsequent corporate profitability for acquirers. This is not incidental inefficiency but a structural logic. Public money — via bank recapitalisation and depositor haircuts — absorbs losses; private capital appropriates restructured, liability-free assets. The IBC thus enacts a “corporate metamorphosis of liability”: the entity survives, ownership concentrates, accountability evaporates.

(vii). IBC as the Capstone of Crony Neoliberal Capitalism

Situated within the longue durée of Indian banking — from 1969’s social-banking mandate to post-liberalisation hybridity — the IBC marks the decisive rupture. It replaces state-led redistribution of credit with market-led redistribution of distressed assets. The Code does not merely resolve insolvency; it reorders economic power in favour of concentrated capital. High-profile fugitives (Vijay Mallya, Nirav Modi, Mehul Choksi) continue to evade full accountability through protracted transnational proceedings, while small borrowers face stringent enforcement. The result is asymmetric moral hazard: losses socialised onto the masses, gains privatised for cronies.

The fundamental normative question remains: can a framework that systematically transfers public losses into private windfalls, attenuates fraud deterrence, and entrenches structural impunity sustain legitimacy as financial governance? The IBC’s trajectory — from promised efficiency to documented crony expropriation — reveals it not as a correction of earlier contradictions but as their culmination in a new architecture of resolution-driven inequality. Whether this regime can be sustained without eroding the postcolonial promise of equitable development is the central political-economic challenge confronting contemporary India.

IV.F. Privatization, Crony Duopoly, and the Concentration of Wealth

The post-2014 era has seen aggressive privatization and asset monetization across strategic sectors: Air India (to Tata, but emblematic of the trend), coal mines, railway land parcels, ports, airports, and media ecosystems. The Adani Group has emerged as the clearest beneficiary—securing multiple airports (now operating seven major ones with plans for aggressive bidding on the next 11), ports, energy projects, and mining concessions—often through processes criticized for opacity and minimal competition. The Ambani group has consolidated dominance in telecom, retail, and digital infrastructure. Ajay Piramal’s acquisition of DHFL via IBC (2021) exemplifies the pattern: a controversial resolution involving nominal valuation of fraud recoveries, upheld by the Supreme Court in April 2025, resulting in massive haircuts for retail depositors while Piramal Finance (post-reverse merger) rapidly rehabilitated and expanded. These deals have fueled what critics term a crony duopoly, with combined Adani–Ambani wealth ballooning amid state-enabled expansion. BJP’s own coffers have swelled dramatically—receiving 82–85 per cent of electoral trust donations in 2024–25 (over ₹3,000 crore in one year alone)—raising unavoidable questions of quid pro quo. No new nationalization has occurred; instead, the state has orchestrated the massive concentration of national resources into private hands, exacerbating dispossession of marginal communities through land acquisition, environmental dilution, and financial exclusion.

IV.G. Rising Inequality, Poverty, and the Human Cost

Wealth and income inequality have reached historic extremes under this regime. According to the World Inequality Report 2026 and Oxfam analyses, the top 1 per cent now controls 40–43.8 per cent of national wealth (up sharply since 2014), while the top 10 per cent holds 65–77 per cent. The bottom 50 per cent remains mired in stagnant or declining real incomes, with persistent multidimensional poverty, hunger, and nutritional distress affecting hundreds of millions. The richest 1 per cent effectively command policy, as evidenced by tailored regulatory forbearance, privatization routes, and narrative control. This is no accident of market forces but the outcome of deliberate state capture: market fundamentalism dressed in nationalist rhetoric, where “ease of doing business” for cronies translates into expropriation and financial abuse for the masses.

IV.H. From Social Banking to Crony Regime

Across the longue durée—from 1969’s democratization of credit, through 1991–2014’s hybrid liberalization, to the post-2014 resolution regime—the trajectory is clear. The BJP–NDA has not merely continued neoliberal trends; it has radicalized them with ruthless efficiency. The socialist developmental state has been hollowed out, replaced by a facilitator of crony concentration. Demonetization, GST, and the IBC—three marquee “reforms”—have collectively socialized losses onto PSBs, taxpayers, depositors, and the informal economy while privatizing gains for a favoured few. “Viksit Bharat” and “Atmanirbhar Bharat” function as legitimizing myths, masking the entrenchment of monopoly power, dispossession, and inequality. The central contradiction remains: public money props up a system that systematically transfers wealth upward, leaving the masses to bear the cost of “reform.”

This phase sets the stage for interrogating whether the IBC and associated policies represent genuine efficiency gains or a new architecture of concentrated financial power—one that has decisively buried the egalitarian promise of nationalized banking. The question for India’s political economy is no longer whether the system serves the many or the few, but how far the concentration of wealth and impunity can proceed before it undermines the very legitimacy of the postcolonial republic.

V. Conclusion: Ruptures, Trajectories, and the Question of Public Purpose in Indian Banking

The history of Indian banking since Independence is marked by successive institutional ruptures that have redefined the relationship between finance, state power, and citizens. These shifts have moved the system from private elite capture, through state-led developmental inclusion (with its authoritarian undertones during the Emergency), to a liberalized hybrid model, and finally to a regime of resolution capitalism under the BJP–NDA government since 2014.

The post-2014 phase represents the most profound break. The Asset Quality Review exposed inherited stressed assets, but the response—massive taxpayer-funded recapitalization of public sector banks (PSBs), cumulative loan write-offs exceeding ₹16 lakh crore since 2014–15 (with PSBs bearing the overwhelming share), and the operationalization of the Insolvency and Bankruptcy Code (IBC, 2016)—has inverted the 1969 nationalization ethos. Losses have been systematically socialized onto taxpayers and depositors through large haircuts (averaging 65–68 per cent overall, with recent quarters dipping toward 68 per cent and some as low as 20 per cent), while distressed assets have been transferred at steep discounts to a narrow set of corporate acquirers. The DHFL case stands as a stark illustration: retail depositors and NCD holders (over 2.5 lakh families) absorbed disproportionate losses, avoidance transactions linked to alleged fraud were valued at nominal Re 1 and handed to the successful resolution applicant, and the Committee of Creditors (CoC) operated with such opacity that even auditors could not fully account for their own audit trails. Persistent resistance to Right to Information requests has entrenched an informational enclosure that shields powerful interests from scrutiny.

High-profile wilful defaulters and fugitives have faced protracted legal processes with limited accountability, even as the broader ecosystem of elite defaults has proliferated. Strategic asset monetization in ports, airports, energy, and infrastructure has further accelerated wealth concentration, with the top 1 per cent now controlling approximately 40 per cent of national wealth and the top 10 per cent around 65–77 per cent. Official rhetoric of “Viksit Bharat” and “Atmanirbhar Bharat” has served primarily as ideological cover for this upward redistribution, framed as “ease of doing business” while hollowing out the social-banking mandate.

On the surface, the system appears technically healthier, with gross NPA ratios for scheduled commercial banks reaching a historic low of 2.15 per cent (PSBs at 2.50 per cent) as of September 2025. Yet this stability masks a deeper decay: banking has been decoupled from its postcolonial promise of broad-based inclusion and equitable credit allocation. PSBs, still publicly owned in form, now function largely as buffers for private risk and facilitators of asset reallocation to favoured conglomerates. The IBC, repeatedly amended and insulated by judicial deference to the CoC’s “commercial wisdom,” has institutionalized structural impunity rather than genuine resolution.

The longue durée can be summarized as follows:

| Period | Political/Economic Context | Banking Structure & Policies | Key Features/Transformations | Social Impact / Citizen Orientation | Notes on NPAs, Crises, and Cronyism |

|---|---|---|---|---|---|

| 1947–1968 | Postcolonial India; Private banking dominance | ~2000+ mostly private banks; concentrated ownership | Elite capture of credit; urban focus; limited rural access; weak regulation | Public largely excluded from formal credit; savings largely informal | Frequent bank failures; public vulnerability; minimal consumer protection; social banking absent |

| 1969–1990 | Nationalization under Indira Gandhi (14 banks in 1969, 6 more in 1980) | State-owned PSBs dominate; branch expansion; priority-sector lending | Rapid rural and semi-urban branch growth; institutionalized priority-sector targets; mobilization of household savings | High financial inclusion; socially oriented banking; citizen access improved | Political interference in lending; bureaucratic rigidities; financial repression; eventual erosion of commercial discipline |

| 1991–2014 | Liberalization: NDA (1998–2004) → UPA (2004–2014) | Hybrid: PSBs retained, private & foreign banks allowed | Prudential norms introduced (Narasimham); interest-rate deregulation; entry of new private banks; recapitalization programs | Hybrid system: improved efficiency, but social orientation partially diluted | 2008 global financial crisis absorbed effectively; NPAs relatively controlled initially; mounting stressed assets toward late UPA (twin balance sheet problem) |