Posted on 27th February, 2026 (GMT 04:57 hrs)

Updated on 3rd March, 2026 (GMT 07:05hrs)

ABSTRACT

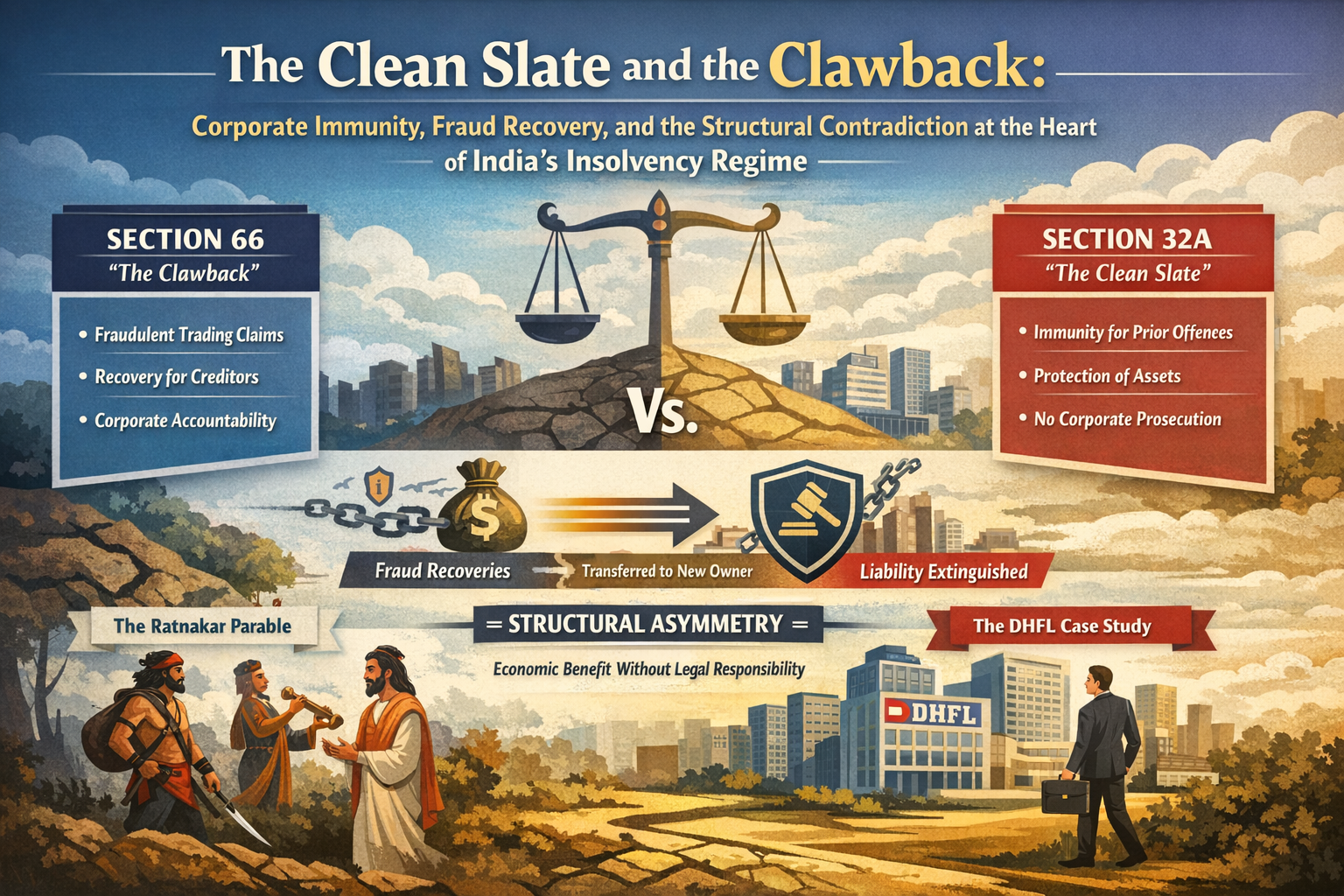

The Insolvency and Bankruptcy Code, 2016 establishes a dual legal framework combining fraud recovery and insolvency resolution. Section 66 embodies the Code’s accountability function by empowering recovery from fraudulent and wrongful trading, thereby restoring value to creditors. In contrast, Section 32A, introduced in 2019 with retrospective effect, extinguishes corporate criminal liability once a resolution plan is approved and control passes to new management. This paper argues that these provisions operate in structural tension: Section 66 presupposes continuity of corporate liability to enable recovery, while Section 32A extinguishes corporate criminal liability while preserving corporate identity, assets, and economic continuity. Through a doctrinal case study of Dewan Housing Finance Corporation Ltd. (DHFL), this paper demonstrates how avoidance recoveries identified under Section 66 remained corporate assets transferred to the resolution applicant, even as Section 32A extinguished the corporate debtor’s criminal liability for the underlying misconduct. This produced a structural asymmetry in which the corporate entity retained the economic benefits of fraud-linked recoveries while being legally immunized from responsibility for the fraud itself. The retrospective insertion of Section 32A further created a temporal dislocation, altering legal consequences after insolvency had commenced. The paper concludes that the interaction between Sections 32A and 66 represents a fundamental transformation in insolvency law—from a creditor-recovery framework grounded in accountability to an acquirer-protection framework grounded in corporate immunity—raising profound questions about equality before law and the political economy of insolvency resolution.

Jai Shri Ram (as they say), folks!

We cherished reading stories as children, though we didn’t always grasp them fully. Some narratives require revisiting, and when needed, they should be recontextualized for relevant understanding in the present. The same applies to the following.

The Metamorphosis of Ratnakar from a Ruthless Highway Robber to the Revered Sage Valmiki

The metamorphosis of Ratnakar from a ruthless highway robber to the revered sage Valmiki is a profound tale, symbolizing redemption, self-realization, and the power of devotion. It underscores the idea that sins are individual burdens, and true transformation begins with acknowledging one’s own accountability.

The Turning Point: Encounter with Sage Narada

Ratnakar lived as a dacoit in the forests, robbing and killing travelers to support his large family. His transformation began when he attempted to rob the wandering celestial sage Narada Muni, who was chanting divine hymns. Unfazed by Ratnakar’s threats, Narada asked a pivotal question: “Will your family, for whom you commit these crimes, share the burden of your sins?” Ratnakar, confident they would, returned home to ask his parents, wife, and children. To his horror, they all refused, stating that while they shared his wealth, his sins were his alone to bear.

The Denial and the Sharing of Sins: A Shattering Revelation

Ratnakar hurried home, eager to prove the sage wrong. He first approached his father and asked, “I commit sins for your sustenance—will you share my sins?” His father refused outright, saying, “No, son. It is your duty as a provider to support us, but the karma of your actions is yours alone to bear. We only share in the fruits of your labour, not the sins.”

Undeterred, Ratnakar turned to his mother, who echoed his father, denying any responsibility: “We accept what you bring, but your sins are your own. How can we share what we did not commit?”

Next, he asked his wife, who had borne his children and managed the household with the ill-gotten gains. She too rejected the idea, stating, “It is a husband’s role to provide, but the weight of your evil deeds falls on you alone. I cannot and will not share your sins.”

Finally, in desperation, Ratnakar questioned his children, hoping their innocence and dependence would bind them to him. But even they disavowed any share in his sins, innocently replying that while they enjoyed the benefits, the moral consequences were his personal burden.

This collective denial was a devastating blow. Ratnakar realized the illusion he had lived under: his family gladly shared the material wealth from his crimes but refused to partake in the spiritual debt. The concept of “shared sins” was exposed as a fallacy—sins are not divisible like property; they cling solely to the perpetrator. This moment shattered his worldview, awakening a deep sense of isolation and guilt. He understood that his actions had not only harmed others but also chained his soul in solitude, with no one to alleviate the karmic load.

Sin: an act, omission, disposition, or condition that deflects from divinely authorized moral order as connotated within a given religious tradition/group/community.

I. Introduction

The Insolvency and Bankruptcy Code, 2016 was enacted in India to supposedly/presumably address systemic inefficiencies in India’s insolvency regime by creating a structured, time-bound mechanism for resolving corporate distress. Its foundational objective was twofold: to maximize value for creditors and to ensure accountability for corporate misconduct that contributed to insolvency. These twin objectives were reflected in the Code’s institutional design, which combined resolution mechanisms with statutory provisions aimed at reversing fraudulent and wrongful depletion of corporate assets.

Section 66 represents the clearest expression of the Code’s accountability function. It empowers the resolution professional to seek orders requiring persons responsible for fraudulent or wrongful trading to contribute to the corporate debtor’s assets. This provision recognizes that insolvency is not always the product of market forces alone, but may result from deliberate misconduct, diversion of funds, or reckless continuation of business despite impending insolvency. Section 66 thus operates as a clawback mechanism, designed to restore value improperly extracted from the corporate debtor and redistribute that value to creditors. Its logic presupposes continuity between corporate misconduct and corporate liability: the corporate debtor remains the legal subject through which fraud-linked losses are recovered and redistributed.

However, the insertion of Section 32A into the Code in December 2019 introduced a fundamentally different legal logic. Section 32A provides that once a resolution plan is approved and control of the corporate debtor passes to new management, the corporate debtor’s liability for offences committed prior to the insolvency commencement date ceases, and the corporate debtor cannot be prosecuted for such offences. The provision also prohibits attachment or confiscation of corporate assets in relation to those offences. Although individual wrongdoers remain prosecutable, the corporate entity itself—despite retaining its legal identity and assets—emerges legally immunized.

The coexistence of Sections 66 and 32A creates a structural contradiction within insolvency law. Section 66 treats fraud-linked recoveries as corporate assets belonging to the corporate debtor, thereby reinforcing corporate continuity for purposes of recovery. Section 32A simultaneously preserves that corporate continuity while extinguishing corporate criminal liability. The corporate debtor survives as a legal and economic entity capable of owning and benefiting from fraud recoveries under Section 66, yet is transformed into an entity immune from criminal prosecution for the very misconduct that gave rise to those recoveries.

II. What is IBC Section 32A?

IBC Section 32A provides immunity to a corporate debtor from liability for offences committed prior to the commencement of the corporate insolvency resolution process (CIRP), provided a resolution plan is approved by the adjudicating authority, resulting in a change of management or control to persons not involved in the prior offences or related to the previous management. This allows the corporate debtor a “clean slate” post-resolution, extinguishing criminal prosecution against the entity itself, though individuals (e.g., former directors) remain liable. Assets of the corporate debtor are also protected from attachment related to such prior offences. It was introduced via the Insolvency and Bankruptcy Code (Amendment) Ordinance, 2019, effective from December 28, 2019, and later enacted through the Amendment Act, 2020, with retrospective effect from the ordinance date.

Section 32A — Liability for prior offences, etc.

(1) Notwithstanding anything to the contrary contained in this Code or any other law for the time being in force, the liability of a corporate debtor for an offence committed prior to the commencement of the corporate insolvency resolution process shall cease, and the corporate debtor shall not be prosecuted for such an offence from the date the resolution plan has been approved by the Adjudicating Authority under section 31, if the resolution plan results in—

(a) a change in the management or control of the corporate debtor to a person who was not— (i) a promoter or in the management or control of the corporate debtor or a related party of such a person; or (ii) a person with regard to whom the relevant investigating authority has, on the basis of material in its possession, reason to believe that he had abetted or conspired for the commission of the offence, and has submitted or filed a report or complaint to the relevant statutory authority or court.

(2) No action shall be taken against the property of the corporate debtor in relation to an offence committed prior to the commencement of the corporate insolvency resolution process, where such property is covered under a resolution plan approved by the Adjudicating Authority under section 31, which results in change in control of the corporate debtor to a person, or sale of liquidation assets under the provisions of Chapter III of Part II of this Code to a person, who was not—

(i) a promoter or in the management or control of the corporate debtor or a related party of such a person; or

(ii) a person with regard to whom the relevant investigating authority has reason to believe that he had abetted or conspired for the commission of the offence.

(3) Subject to the provisions contained in sub-sections (1) and (2), and notwithstanding the immunity given in this section to the corporate debtor and its property, any person who was a designated partner, officer in default, or in any manner in charge of, or responsible to the corporate debtor for the conduct of its business, or associated with the corporate debtor in any manner and who was directly or indirectly involved in the commission of such offence, shall continue to be liable to be prosecuted and punished for such offence committed by the corporate debtor.

Explanation.— For the purposes of this section—

(a) “action against the property of the corporate debtor” includes attachment, seizure, retention or confiscation of such property;

(b) nothing in this section shall bar any prosecution of any person other than the corporate debtor.

Legal Effectuations

- Corporate debtor liability ceases after resolution plan approval.

- Corporate debtor cannot be prosecuted for past offences.

- Corporate assets cannot be attached for past offences.

- Individuals responsible remain prosecutable.

III. Core Parallel: “Sins”/Offences Are Individual Burdens, Never Shared

The story of Ratnakar’s transformation into Valmiki and Section 32A of the Insolvency and Bankruptcy Code, 2016 (IBC) both revolve around the profound concept of sins/offences and their non-transferability or non-sharing with others, particularly “dependents” or “beneficiaries” who enjoyed the fruits but refuse (or are barred from bearing) the burden.

In the mythological narrative:

- Ratnakar commits crimes (robbery, murder) to support his family.

- He assumes his family will share the sins (papa/karma), as they share the material benefits.

- Upon confrontation (prompted by Narada), every family member—parents, wife, children—flatly denies any willingness or ability to share the sins. They accept the wealth but reject the moral/spiritual liability.

- This denial shatters Ratnakar, forcing him to confront that sins are personal and non-transferable. No one else can bear his karmic debt; redemption requires his own penance and rebirth as Valmiki.

Section 32A IBC: “Clean Slate” with Strict Non-Sharing of Liability

Section 32A provides a statutory “clean slate” to a corporate debtor (CD) after approval of a resolution plan under Section 31. Key provisions:

- The liability of the corporate debtor for any offence committed prior to the commencement of CIRP shall cease.

- The CD shall not be prosecuted for such prior offences from the date of plan approval.

- The CD’s property/assets are protected from attachment, seizure, or confiscation related to those prior offences.

- This immunity applies only if there is a change in control/management under the approved plan to an unrelated, non-complicit new applicant.

- Importantly, the provision does not absolve the erstwhile promoters, directors, or management responsible for the offences—they remain fully liable and prosecutable.

In essence:

- The “corporate family” (the company as an entity, which “benefited” from the offences through operations, growth, or gains) is shielded from past criminal liability once a new, unrelated “provider” takes over via resolution.

- But the old “family members” (promoters/directors who committed or enabled the offences) cannot shift or share the burden—their personal/criminal liability persists.

- Courts have upheld this distinction: the goal is revival and value maximization for creditors, without burdening innocent new investors, while ensuring accountability for the guilty original wrongdoers.

Key Comparison Table

| Aspect | Ratnakar-Valmiki Story (Mythological/Spiritual) | Section 32A IBC (Legal/Commercial) |

|---|---|---|

| Wrongdoer | Ratnakar (individual robber) | Corporate debtor’s erstwhile management/promoters |

| Beneficiaries who “share fruits” | Family (parents, wife, children) – enjoy wealth from crimes | Corporate debtor (company entity) and indirectly creditors/shareholders via operations |

| Denial/Non-Sharing of Sins/Offences | Family explicitly refuses to share sins; sins are personal | Law explicitly denies transfer of liability to new management; old management retains full liability |

| Condition for “Clean Slate”/Redemption | Personal realization, intense penance (chanting “Mara” → “Rama”), rebirth from anthill | Approved resolution plan with change in control to unrelated, non-complicit new applicant |

| Outcome | Ratnakar reborn as Valmiki (enlightened sage); past erased through transformation | Corporate debtor gets immunity from prosecution/assets protected; company “reborn” under new management |

| Moral/Legal Lesson | Sins/karma cannot be outsourced or shared; true atonement is individual | Criminal liability for prior offences cannot be shifted to new innocent parties; old wrongdoers remain accountable |

Both narratives powerfully illustrate that sins/offences cling to the perpetrator—whether an individual dacoit or a company’s prior controllers—and cannot be offloaded onto dependents or successors who merely benefited materially. In the spiritual realm, this drives personal redemption; in the commercial realm, it enables economic revival without impunity for the guilty.

IV. Section 66 — Fraudulent trading or wrongful trading

IBC Section 66 addresses fraudulent trading and wrongful trading. Under subsection (1), if during CIRP or liquidation, the business of the corporate debtor was carried on with intent to defraud creditors or for any fraudulent purpose, the adjudicating authority may order any persons knowingly involved to contribute to the corporate debtor’s assets. Subsection (2) holds directors or partners personally liable to contribute if, before the insolvency commencement date, they knew or should have known insolvency was unavoidable but failed to exercise due diligence to minimize losses to creditors.

(1) If during the corporate insolvency resolution process or a liquidation process, it is found that any business of the corporate debtor has been carried on with intent to defraud creditors or for any fraudulent purpose, the Adjudicating Authority may, on the application of the resolution professional, pass an order that any persons who were knowingly parties to the carrying on of the business in such manner shall be liable to make such contributions to the assets of the corporate debtor as it may deem fit.

(2) On an application made by a resolution professional during the corporate insolvency resolution process, the Adjudicating Authority may by an order direct that a director or partner of the corporate debtor shall be liable to make such contribution to the assets of the corporate debtor as it may deem fit, if—

(a) before the insolvency commencement date, such director or partner knew or ought to have known that there was no reasonable prospect of avoiding insolvency; and

(b) such director or partner did not exercise due diligence in minimising the potential loss to creditors.

Legal Effectuations

- Persons involved in fraud must contribute to corporate assets.

- Directors can be personally liable for wrongful trading.

- Provision exists to recover value for creditors.

V. Structural Incommensurability Between Sections 32A and 66

The contradiction between these provisions is doctrinal, structural, and economic.

A. Doctrinal contradiction

Section 66 assumes corporate wrongdoing must be legally rectified. Section 32A extinguishes corporate liability for those same offences. Thus, the same corporate entity is:

- Legally culpable under Section 66,

- Legally immune under Section 32A.

B. Temporal contradiction

Section 66 operates retrospectively. Section 32A operates prospectively. This creates discontinuity in corporate legal identity.

C. Institutional contradiction

Section 66 empowers: resolution professionals, creditors, adjudicating authority. Section 32A protects: corporate debtor, resolution applicant.

D. Ontological contradiction: corporate identity continuity vs liability discontinuity

Under corporate law: corporate entity continues after resolution. Under Section 32A: corporate liability does not. Thus: identity continues, liability does not.

| Dimension | Section 66 | Section 32A |

|---|---|---|

| Objective | Recover losses caused by fraud | Extinguish corporate liability for past offences |

| Legal direction | Backward-looking recovery | Forward-looking immunity |

| Beneficiary | Creditors | Corporate debtor and new owner |

| Legal effect | Reinforces accountability | Eliminates corporate criminal liability |

| Economic effect | Restores creditor value | Enables “clean slate” takeover |

VI. Economic Consequences

The provisions create a dual legal economy:

Section 66: recovery oriented, creditor protective.

Section 32A: transfer oriented, resolution applicant protective.

This dual structure prioritizes resolution finality over accountability continuity.

The Clean Slate Doctrine

Section 32A creates a statutory “clean slate”. Corporate debtor becomes: same legal entity, without prior criminal liability. This is a form of legislatively imposed legal discontinuity. Section 66 represents the accountability logic of insolvency law. Section 32A represents the resolution-finality logic. Their coexistence creates a structural legal paradox: one provision seeks to restore the past, the other extinguishes the past. Section 32A therefore operates as a statutory immunity shield, transforming the corporate debtor into a liability-extinguished legal entity upon resolution.

VII. Corporate Immunity vs. Fraud Recovery: A Doctrinal Case Study of DHFL under Sections 32A and 66 of the IBC

The resolution of Dewan Housing Finance Corporation Ltd. (DHFL) represents the clearest real-world demonstration of the structural contradiction between Section 66 (a recovery-oriented fraud accountability mechanism) and Section 32A (a corporate immunity provision extinguishing liability upon resolution). The DHFL case shows how immunity under Section 32A operated in practice to neutralize the legal and economic consequences of Section 66 recoveries—even where fraud-based avoidance claims existed.

A. Section 66 in DHFL: Fraudulent Trading and Avoidance Recoveries Identified

Forensic audits in DHFL identified avoidance transactions—including fraudulent and wrongful trading under Section 66—estimated at approximately ₹45,000 crore. These claims arose from fraudulent diversion of funds, improper lending, and wrongful trading conduct by prior management. Section 66 provides that such recoveries must contribute to the assets of the corporate debtor—thus benefiting creditors. Legally, these recoveries constituted corporate claims, corporate assets, and recoverable value for creditor benefit.

B. Resolution plan valuation of Section 66 recoveries: nominalization of fraud claims

Despite forensic valuation of ₹45,000 crore, the resolution plan (submitted by Piramal Capital and Housing Finance Limited and approved by the CoC) assigned a notional value of exactly Re 1 to Section 66 avoidance recoveries. This had three legal consequences:

- Fraud recovery rights remained with the corporate debtor,

- Corporate debtor ownership transferred to the resolution applicant,

- Thus fraud recoveries became economically transferable to the acquirer.

This was not extinguishment of the claim—but economic transfer of the claim’s upside. The Supreme Court (in its April 2025 judgment) upheld this arrangement as part of the CoC’s commercial wisdom, distinguishing Section 66 recoveries (which could benefit the resolution applicant) from other avoidance recoveries (benefiting creditors).

C. Transfer of Section 66 recoveries to the resolution applicant

Because the corporate debtor survives insolvency, and ownership transfers to the resolution applicant: any future recovery under Section 66 becomes part of the corporate debtor/SRA’s asset pool, which now belongs to the new owner. Thus, fraud recovery rights became a contingent economic asset of the acquirer, despite arising from pre-resolution fraud. This is the key structural transformation.

D. Section 32A Intervention: Corporate Criminal Liability Extinguished

Brief Timeline:

- 3 December 2019: DHFL admitted into CIRP.

- 28 December 2019: Section 32A inserted via the Insolvency and Bankruptcy Code (Amendment) Ordinance, 2019, with retrospective effect (deemed to come into force from this date upon later enactment).

- 13 March 2020: The Insolvency and Bankruptcy Code (Amendment) Act, 2020 received Presidential assent, confirming and giving statutory force to the insertion of Section 32A (including its overriding effect and immunity provisions) with effect from 28 December 2019. This occurred after insolvency began but before resolution plan approval. Thus, Section 32A applied to DHFL mid-process. Once the resolution plan was approved, corporate criminal liability for pre-CIRP offences ceased, and the corporate debtor became immune from prosecution.

- 2 February 2026: The Special PMLA Court discharged the DHFL corporate entity (now rechristened as “Piramal Finance” from PCHFL-PEL after reverse merger-rebranding choreography to allegedly forego/disown past liabilities, further amplifying the “clean slate” engineering) from money laundering prosecution, explicitly citing Section 32A immunity. Thus, the corporate entity retained assets and legal continuity but criminal liability was extinguished.

This sequence underscores how the ordinance’s insertion mid-CIRP, solidified by the March 2020 Presidential assent (with built-in retrospectivity from the ordinance date), enabled the “clean slate” outcome for the resolved corporate debtor under the approved plan.

E. The Mechanism of Functional Override: How Section 32A Neutralized Section 66

This occurred through a three-stage legal transformation.

Stage 1: Fraud recoveries defined as corporate assets — Under Section 66, fraud recoveries belong to the corporate debtor and are intended to augment corporate assets for creditor benefit. Thus, recoveries legally attach to the corporate entity.

Stage 2: Corporate entity transferred to new owner — The resolution plan transferred ownership and control of the corporate debtor, including contingent assets such as avoidance recoveries. Because avoidance claims belong to the corporate debtor—not creditors directly—ownership of those claims followed ownership of the corporate entity.

Stage 3: Section 32A extinguished corporate criminal liability — Section 32A ensured that the corporate debtor retained assets but lost criminal liability. Thus, the corporate debtor emerged as asset-continuous but liability-discontinuous.

This asymmetry is decisive. The result of this is basically the legal inversion of Section 66’s creditor-protection logic. Section 66 intended fraud recoveries to restore creditor losses. Section 32A enabled corporate continuity without criminal liability, and transfer of corporate assets—including avoidance recoveries—to new ownership. Thus, the corporate entity retained economic value of fraud recovery claims while corporate criminal liability was extinguished. This constitutes a functional override—not textual repeal, but structural neutralization.

VIII. The Retrospective Trap: Legal Anachronism as Structural Device

The DHFL case reveals a distinctive temporal legal phenomenon: retrospective immunity applied to an ongoing insolvency process.

A. Definition: Legal anachronism in statutory application: Anachronism occurs where a legal provision alters legal consequences of past events after those events have already occurred. Section 32A was inserted after DHFL entered CIRP, but applied retrospectively.

B. Temporal dislocation in DHFL timeline: Corporate misconduct alleged before CIRP; CIRP commenced December 2019; Section 32A inserted December 2019; immunity applied to offences that occurred before insertion. Thus, legal immunity did not exist at the time of alleged offences—but was created later and applied backward.

C. Retrospective immunity as temporal discontinuity: Section 32A produced a three-layer temporal structure:

Time 1: Offences committed → liability exists

Time 2: Insolvency begins → liability still exists

Time 3: Law inserted → liability retroactively extinguished

Thus, law altered the past legal consequences.

D. Doctrinal characterization: Retroactive corporate legal cleansing: Section 32A created retroactive corporate liability discontinuity. The corporate entity exists continuously—but its liability history is legally erased. This is analogous to corporate identity continuity combined with liability discontinuity.

IX. Structural Consequence: Separation of Economic Benefit from Legal Responsibility: After resolution: Corporate debtor retained assets, avoidance recoveries, and legal identity. Corporate debtor lost criminal liability. Thus: economic continuity + legal discontinuity.

Doctrinal Observation– Section 32A as Structural Override of Section 66: The DHFL case demonstrates that Section 32A functionally overrides Section 66 not by eliminating fraud claims, but by altering their institutional beneficiary. Section 66 creates recovery rights belonging to the corporate debtor. Section 32A ensures the corporate debtor survives—but without criminal liability. Thus, the corporate entity emerges as beneficiary of fraud recoveries and immune from criminal prosecution for the underlying fraud.

Critical Observation– The Retrospective Clean-Slate Doctrine: Section 32A operates as a retroactive corporate immunity mechanism that preserves corporate assets, transfers corporate ownership, extinguishes corporate criminal liability, while allowing fraud recovery claims to remain corporate assets. This creates a structural asymmetry: corporate debtor retains the economic consequences of fraud recovery, while being released from the legal consequences of fraud liability.

X. Conclusion: Section 66 as Recovery Mechanism, Section 32A as Immunity Shield, and the Political Economy of Corporate Rescue

The interaction between Sections 66 and 32A reveals a fundamental transformation in the normative structure of insolvency law. Section 66 represents the Code’s accountability function, designed to recover value lost through fraudulent and wrongful trading and restore that value to the corporate debtor for the benefit of creditors. It presupposes that the corporate debtor remains the legal subject through which fraud-linked losses are recovered and redistributed. Section 32A, by contrast, preserves the corporate debtor’s legal and economic continuity while extinguishing its criminal liability for past offences. Together, these provisions create a structural asymmetry: the corporate debtor retains the economic benefits of fraud recoveries under Section 66 while being legally immunized from responsibility for the underlying misconduct under Section 32A.

The DHFL resolution demonstrates how this asymmetry operates in practice. Fraud-linked avoidance claims identified under Section 66 remained attached to the corporate debtor and were transferred along with the corporate entity upon resolution (with Section 66 recoveries benefiting the acquirer per the approved plan and Supreme Court ruling). At the same time, Section 32A extinguished the corporate debtor’s criminal liability, and judicial proceedings (including the 2 February 2026 PMLA court discharge) confirmed the corporate entity’s immunity from prosecution. The corporate debtor thus emerged from insolvency as a legally continuous and economically intact entity, yet one that was legally severed from responsibility for its own past misconduct.

This separation of economic continuity from legal responsibility has profound implications. Section 66 treats fraud recoveries as corporate assets, reinforcing corporate continuity for purposes of economic recovery. Section 32A preserves that continuity while selectively extinguishing corporate liability. The result is a corporate entity that retains the economic consequences of fraud recovery while being shielded from the legal consequences of fraud liability. Insolvency law, in this configuration, ceases to function solely as a mechanism for creditor recovery and becomes a mechanism for reorganizing corporate legal responsibility itself.

This structural configuration also raises concerns about the political economy of insolvency resolution. When corporate entities can undergo resolution, retain assets and recovery rights, and simultaneously receive statutory immunity from prosecution, insolvency law risks becoming a mechanism through which corporate liability is selectively extinguished while corporate economic continuity is preserved. This creates conditions in which the costs of corporate misconduct are diffused across creditors and the financial system, while the reorganized corporate entity continues as a legally protected economic actor.

Section 66, in isolation, represents a mechanism of accountability. Section 32A, in isolation, represents a mechanism of resolution finality. Together, however, they create a legal structure in which recovery and immunity coexist in ways that fundamentally alter the relationship between corporate misconduct and corporate liability. The corporate debtor remains the beneficiary of recovery under Section 66, yet is transformed into a liability-extinguished entity under Section 32A.

The resulting legal architecture reflects a shift in insolvency law’s underlying function—from enforcing accountability for corporate misconduct to ensuring continuity of corporate capital. The DHFL case illustrates how this shift can operate in practice, raising fundamental questions about creditor protection, equality before law, and the role of insolvency law in mediating the relationship between corporate power and legal responsibility.

SEE ALSO:

Appendix

Sin, Memory, and the Juridical Rupture of Supposed Moral Causality

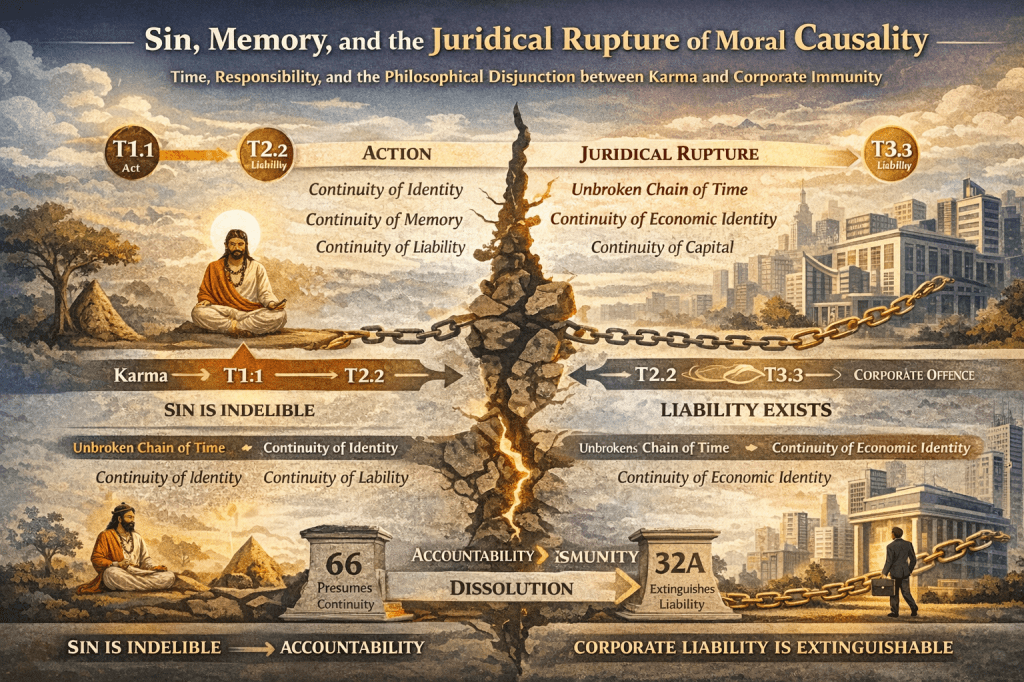

The philosophical structure underlying the Ratnakar–Valmiki narrative rests upon a fundamental axiom: moral responsibility is inalienable. Sin attaches to the subject who acts; it is neither divisible nor transferable. Its burden is not economic but ontological. In classical karmic theory, action (karma) generates consequence (phala) through an unbroken chain of moral causality. The continuity between act and consequence is not merely doctrinal but metaphysical. The self that commits the act is the self that must bear its residue. Redemption, therefore, does not consist in institutional rearrangement but in interior transformation. The subject persists through time, and with that persistence comes responsibility.

This philosophical structure presupposes three elements: (1) continuity of identity, (2) continuity of memory, and (3) continuity of liability. The moral order is intelligible because these three continuities remain aligned. The actor, the act, and the consequence are temporally and ontologically connected.

Sections 66 and 32A of the Insolvency and Bankruptcy Code disrupt this alignment in distinct and structurally revealing ways.

Section 66 presupposes continuity. Fraudulent or wrongful trading generates liability that must be restored to the corporate debtor’s asset pool. The provision assumes that misconduct produces a deficit in corporate value, and that this deficit can be rectified through contribution orders. The corporate debtor remains the juridical site through which past wrongdoing is economically reconciled. In this respect, Section 66 mirrors the logic of moral causality: action produces consequence; consequence must be absorbed and redistributed.

Section 32A, however, introduces a juridical rupture in this chain. It preserves corporate identity and economic continuity while extinguishing corporate criminal liability. The corporate entity that committed the offence continues to exist in law, continues to own assets, continues to benefit from recoveries—including those arising from Section 66—yet is legally severed from prosecutorial consequence. Identity persists; liability does not. The unity between actor and burden is dissolved.

This produces a structural dissociation unprecedented in classical moral reasoning. The corporation becomes ontologically continuous but normatively discontinuous. It is the same legal person for purposes of ownership, transfer, and recovery, but not the same legal person for purposes of culpability. In moral philosophy, such bifurcation is incoherent: continuity of self grounds continuity of responsibility. Under Section 32A, continuity of corporate personhood is retained while responsibility is selectively extinguished.

The result is not forgiveness in the theological sense. Forgiveness presupposes acknowledgment, repentance, and moral transformation. Nor is it punishment. It is legal insulation achieved through change of control. Liability ceases not because the past is reconciled, but because statutory architecture mandates its cessation. The offence remains historically real; the corporate subject remains legally alive; yet the juridical relation between the two is dissolved.

This dissolution is intensified by retrospectivity. When Section 32A is applied to offences committed prior to its enactment, the chain of moral causality is interrupted after the fact. At Time 1 (t1), the act generates liability. At Time 2 (t2), insolvency commences under a regime where such liability attaches to the corporate entity. At Time 3 (t3), legislation intervenes and retroactively alters the legal consequences of the past act. The temporal unity between wrongdoing and consequence is fractured. Law does not merely regulate the future; it reconfigures the normative meaning of the past.

In karmic philosophy, temporal continuity is inescapable; causality cannot be legislatively repealed. In the insolvency framework shaped by Section 32A, causality becomes contingent upon statutory design. Liability is no longer an intrinsic extension of wrongdoing but a variable subject to policy recalibration. Moral residue becomes administratively negotiable.

This recalibration produces a deeper political economy effect. When economic continuity is preserved while legal liability is extinguished, the costs of past misconduct are displaced. Creditors absorb losses through resolution haircuts; the reorganized corporate entity retains assets and contingent recovery rights; criminal prosecution is confined to individuals whose enforcement may be uncertain, protracted, or diluted. The corporate form, as an enduring economic vehicle, survives insulated from its own penal history. Responsibility is individualized; continuity is collectivized.

Thus, insolvency law performs a conceptual transformation. It converts wrongdoing from a question of moral burden into a question of transactional allocation. Section 66 attempts to restore value within the corporate structure; Section 32A reconstitutes that structure free from criminal stain. The corporate debtor becomes a vessel emptied of liability but filled with preserved capital. Accountability becomes asymmetrical: economic benefit adheres to the entity; penal consequence is displaced onto natural persons.

The Ratnakar narrative insists that sin cannot be shared, outsourced, or extinguished without inner transformation. The insolvency architecture suggests that liability can be extinguished without ontological rupture, provided ownership shifts and statutory conditions are satisfied. Where moral philosophy binds identity to responsibility across time, Section 32A decouples them. The corporate self remains; the corporate guilt does not.

In this decoupling lies the deeper structural significance of the interaction between Sections 66 and 32A. One provision affirms continuity between misconduct and restitution; the other affirms continuity between entity and capital while discontinuing culpability. The result is a juridical configuration in which memory is preserved economically but erased normatively. The corporation remembers the benefit of recovery; it does not remember the burden of offence.

This is not merely a technical feature of insolvency design. It represents a reordering of the relationship between law, time, and responsibility. The chain that once linked act, subject, and consequence is rendered selectively interruptible. In that interruption, insolvency law moves from enforcing moral-economic coherence to engineering corporate survivability.

The above article was sent as an “offering” (sarcasm intended) to Mr. Piramal in the form of the following letter:

Subject: Will you be Valmiki, Away from being Ratnakar?

Dear Mr. Piramal,

I write with the deepest admiration — truly, the stuff of epic mythologies. You’ve managed what our legal system once promised only sages and thieves: a clean slate metamorphosis. Just as Ratnakar shed his sins to become Valmiki, so too has the corporation once called DHFL/PCHFL/PFL (?!) shed the inconvenient burden of accountability and emerged reborn — now under your auspicious banner, sans liability but still proudly clutching the assets and rewards. Bravo!

Here’s the offering today, exclusively for you, oh philanthropic Sire:

You see, we humble depositors — widows, pensioners, middle-class families — were merely supporting characters in this grand tale. We shared in the fruits of DHFL’s operations (our hard-earned monies), but unlike Ratnakar’s family who refused to share his sins, the legal architecture favoured an even more convenient outcome: corporate liability simply ceased to exist, while the economic perks gallantly followed into the coffers of your new management.

Of course, we expected some metamorphosis in the Insolvency and Bankruptcy Code — that’s why Parliament introduced and soon enacted Section 32A with retrospective effect to shrewdly apply to the DHFL CIRP. Only, most of us thought redemption meant justice for wrongdoing, not justice forgiveness with benefits. Under Section 66, wrongdoing should generate recoveries to the benefit of all the creditors; but under Section 32A, the corporate sinner — or its new avatar — simply skates free while keeping the loot. Neat trick! Yielding benefit from incoherent incommensurability.

I can almost hear Nārada’s question echoing through the corridors of the National Company Law Tribunal and the National Company Law Appellate Tribunal — “Will your family share your sins?”

Except this time, the question was asked not by a sage but by a statute; answered not by conscience but by a Committee of Creditors with their so-called “commercial wisdom” (though NCLAT radically overturned this on 27th January, 2022); and signed off with a corporate phoenix rising from the ashes of accountability. All that was lacking was a celestial flute for accompaniment. We are still awaiting the “divine” (Article 51Ah?!) verdict of Purusottama as catalyzed by former CJI Chandrachud in this regard.

This did not unfold in isolation. It moved alongside conspicuous corporate donations reportedly made by your conglomerate — ₹85 crore and more, ₹25 crore and more — flowing into the PM CARES Fund and through the Electoral Bonds Scheme, filling crony political coffers in the background.

And now, when voices like mine point this out in public commentary and academic blogs — explaining the structural tension between fraud recovery and immunity, highlighting how the corporate entity retains assets while shedding liability — we are met with robust legal correspondence from DSK Legal. Vexatious litigation, you call it. SLAPP-style intimidation, we feel it. How charmingly apt: those who question the new Ratnakar-canon of corporate justice now get a preview of what it means to stand in the crossroads of legal privilege and public scrutiny.

So allow me to ask with genuine curiosity (and a dash of mythic fervour):

Will you be the Valmiki — benefitting from a crafted “clean slate” while insulating yourself from accountability — leaving the victims to carry all the sins, debts, and unanswered questions?

Or perhaps there’s another twist in this corporate epic yet to be revealed?

Wishing you all the very best for today’s pre-admission interim SLAPP proceedings.

Yours theatrically,

लड़ेंगे या मरेंगे!

इंक़लाब ज़िंदाबाद!

No Pasaran!

Debeprasad (sic) Sadhan (patriarchal insertion?!) Bandopadhyay (sic)

COPY TO:

1. Shri A.H. Laddhad, The Hon’ble Prothonotary and Senior Master, Bombay High Court (Case No. S/42/2025)

#Scrap_Ill_Conceved_IBC, #IBC Section 32A Explained | DHFL Piramal Takeover Analysis | Insolvency Code Critique | Crony Capitalism in India | Depositor Rights & Bankruptcy Law Reform | Financial Governance Crisis | Corporate Accountability Campaign|

They erased liability.

They erased accountability.

They will NOT erase us.

Scrap the law that shields cronies.

Return the people’s money.

Justice for DHFL victims — now.

#Scrap_Ill_Conceved_IBC, #Repeal_IBCSection32A, #InsolvencyAndBankruptcyCode, #IBCReformNow, #DHFLScam, #DHFLPiramalTakeover, #JusticeForDHFLVictims, #JusticeForDepositors, #Seize_Cronies_Fairplay_for_DHFL_Victims, #Alleged_Dawood_Mirchi_Rkw_Dhfl_Bjp_Collusion, #CronyCapitalismExposed, #CorporateCaptureIndia, #PublicMoneyPrivateProfits, #FinancialGovernanceCrisis, #TransparentBankruptcy, #InvestorProtectionIndia, #DepositorRightsIndia, #RegulatoryFailureIndia, #AccountabilityInIBC, #PolicyCaptureIndia, #StopCorporateLoot, #ReclaimPublicFunds, #InsolvencyAndBankruptcyCode, #IBCReformNow, #DHFLScam, #DHFLPiramalTakeover, #JusticeForDHFLVictims, #JusticeForDepositors, #Seize_Cronies_Fairplay_for_DHFL_Victims, #Alleged_Dawood_Mirchi_Rkw_Dhfl_Bjp_Collusion, #CronyCapitalismExposed, #CorporateCaptureIndia, #PublicMoneyPrivateProfits, #FinancialGovernanceCrisis, #TransparentBankruptcy, #InvestorProtectionIndia, #DepositorRightsIndia, #RegulatoryFailureIndia, #AccountabilityInIBC, #PolicyCaptureIndia, #StopCorporateLoot, #ReclaimPublicFunds, #FinancialSystemsReform, #PeopleOverProfit, #DigitalActivismIndia, #JusticeMovementIndia, #ExposeTheSystem, #PublicInterestEconomics, #BankruptcyLawReform,

LikeLiked by 6 people