Posted on 19th June 2021

Updated on 13h July, 2026 (GMT 10:59 hrs)

ABSTRACT

The white paper on DHFL (Dewan Housing Finance Corporation Ltd) details allegations of financial misconduct, including fraudulent loans, political connections, and regulatory oversight failures. It explores the diversion of funds by DHFL executives to politically connected entities and accuses regulatory bodies like SEBI and RBI of inadequate action. The paper calls for accountability and transparency from Indian financial institutions, emphasizing the urgent need for reforms to prevent similar scandals

DISCLAIMER: The allegations and claims outlined in this article are subject to ongoing judicial review and investigation, with many issues remaining sub judice. Readers should refrain from forming definitive conclusions due to the absence of conclusive evidence. OBMA has always mindfully used cautious and legally accurate language, employing terms such as “alleged,” “reported,” “possible,” and “supposed” when discussing matters related to Mr. Ajay Piramal and other business figures. We encourage readers to maintain an open-minded, critical, and independent perspective to foster a just and equitable society, challenging structurally induced constraints.

1. Dewan Housing Finance Corporation Ltd. (henceforth DHFL) is a deposit-taking Housing Finance NBFC regulated by the National Housing Bank (NHB) headquartered in Mumbai with branches in major cities across India. DHFL was established (11 April 1984) to enable access to economical housing finance to the lower and middle income groups in semi-urban and rural parts of India. DHFL is the second housing finance company to be established in the country. The company also leases commercial and residential premises. DHFL is among the 50 biggest financial companies in India. [Source: Wikipedia⤡]

2. Everything was fine for the DHFL before a report published by a News Portal:

DEWAN HOUSING FINANCE CORPORATION LIMITED- THE ANATOMY OF INDIA’S BIGGEST FINANCIAL SCAM VIEW HERE ⤡ (As reported on 29th January, 2019 ©The Cobra Post)

Just before that day, the supposed future “owner” of the DHFL declared this:

Be prepared for one or two major shocks in NBFC sector: Piramal VIEW HERE ⤡ (As reported on 28th January, 2019©The Hindu)

Is it a just “Post hoc ergo propter hoc”? Or, was it totally predetermined by the cronies?

DHFL filed a response with the Bombay Stock Exchange saying the allegations raised by Cobrapost were untrue. DHFL also rebutted these allegations in a hosted investors / analysts conference and clarified that the ₹ 31,000 crore loans mentioned in the allegation consist of its project loan portfolio. Also the company tried to clarify that the advances commented by Cobrapost should be 21,000 Crores and not 31,000 crores.

3. Following the Cobrapost allegations, Indian Credit Rating Agencies reaffirmed their high safety rating for the financial instruments issued by DHFL. Even after the emergence of serious allegations of misconduct against its business, the Indian credit rating agencies continued to issue high safety ratings for the DHFL financial products, but, on 6 June 2019, DHFL defaulted on its debt repayment, resulting in a debt rating downgrade, immediately wiping out 16% of the value from its stock price. At the time, the fall in DHFL stock price was an all year low. This rapid decline in stock price resulted in a loss of investor confidence. [Source: Wikipedia⤡] Rating agencies downgrade DHFL to default status VIEW HERE ⤡ (As reported on 9th June, 2019 ©The Indian Express)

A BOLT FROM THE BLUE FOR THE DHFL CREDITORS! The Honourable High Court of Bombay in the case of Reliance Nippon Life Insurance v/s DHFL passed an order on September 30, 2019 and October 10, 2019 restraining DHFL from making payments to any of its secured/unsecured creditors, including the payments to any fixed deposit holders. Till this verdict, all the FD and NCD Holders of DHFL were getting their dues as per schedule. For more information on this Bombay High Court verdict, visit the following link: Stopped payment to creditors following Bombay High Court orders: DHFL VIEW HERE⤡ (As reported on 4th November, 2019 ©Business Standard)

What Cobrapost could do thorough their sting operation, why the rating agencies, governmental vigilant authorities including the Reserve Bank of India, National Housing Bank etc. could not? They (including Credit Rating Agencies) should be respondents in the legal cases.

4. It is to be noted that the 2019 Indian general election was held in seven phases from 11 April to 19 May 2019 to constitute the 17th Lok Sabha. The votes were counted and the result declared on 23 May. The DHFL Scam happened just after that.

5. Cobrapost also raised allegations of political donations worth crores of rupees, in violation of Section 182 of Companies Act, 2013 for political donations or political charity or otherwise terror funding.

For details cf. Alleged Dawood-Mirchi-RKW-DHFL-BJP Collusion⤡ (Here, in this document, apart from Dawood-Mirchi-RKW-DHFL-BJP Collusion, PM Care Fund Scam, Electoral bond scam are also mentioned)

The ruling party is associated with the “terrorist dons” or the so-called “underworld”, viz., Dawood Ibrahim and his close associate Iqbal Mirchi, who are again related to Dewan Housing Finance Corporation Limited and its associate RKW Developers Private Limited (Dheeraj Realty).

“Why did BJP receive crores in donation from a company accused of buying properties of Iqbal Mirchi? Is this not ‘treason’ Mr. Amit Shah?” Upping the attack, the Congress tweeted, “As it turns out, the ‘Modi Bond of Corruption’ ⤡ extends to terror funding companies as well. Companies associated with Iqbal Mirchi have donated crore of rupees to BJP. PM Modi and Amit Shah must answer on these treasonous acts.” In the case of DHFL scam, the ruling party has played the “dog in manger” policy.

BJP received donation from company being probed for ‘terror funding’ by ED VIEW HERE ⤡ (As reported on Nov 22, 2019 ©The National Herald)

The India Congress Party alleged that . Gift BJP Rs 20 cr, get ‘return gift’ worth Rs 31K cr: Congress on fraud by DHFL VIEW HERE ⤡ (As reported on 30 January, 2019, ©Millennium Post). May we believe Congress’ allegation?

In response to this serious allegation, the BJP has not

(a) filed a Defamation case against all these media houses, who reported such collusion;

(b) banned all these above newspapers, who had reported such false allegations against the BJP.

The legal implications of such unsolicited collusion/nexus among BJP, Dawood-Mirchi, RKW developers and the DHFL must be noted. We are citing the following Sections from the IPC:

Sections 121⤡ (abetting waging of war, against the Government of India), 126 ⤡ (Committing depredation on territories of Power at peace with the Government of India);

130⤡ (aiding escape of, rescuing or harbouring such prisoner: or attempts to rescue any such prisoner, or harbours or conceals any such prisoner who has escaped from lawful custody, or offers or attempts to offer any resistance to the recapture of such prisoner shall be punished with imprisonment for life, or with imprisonment of either description for a term which may extend to ten years, and shall also be liable to fine.)

The Prevention of Terrorism Act, 2002 (15 of 2002) ⤡ and Terrorist and Disruptive Activities (Prevention) Act⤡.

If all these above are believed to be true, the laws go against the ruling party, but not against the Government of India. A Criminal Case may be filed against the BJP. The respondent will be Jagat Prakash Nadda, The President of the Bharatiya Janta Party, Village – Vijaypur, P. O.- Auhar, Tehsil – Jhandutta, District – Bilaspur, Himachal Pradesh Tel. – 01978-259005 Present Address:7-B, Motilal Nehru Marg, New Delhi. Before this, we demand the CBI enquiry on this issue.

According to our conclusive perception (we may be wrong), due to the huge terror funding or otherwise political charity, the business tycoons are bound to become preys of fraudulent transactions to compensate their loss.

6. Some transparency activists are whispering that there is one-to-one correspondence between ruling party’s astronomically increasing assets and abrupt bankruptcies.

For more details with statistical evidences cf. Consequences Of Crony And Monopoly Capitalism In India⤡.

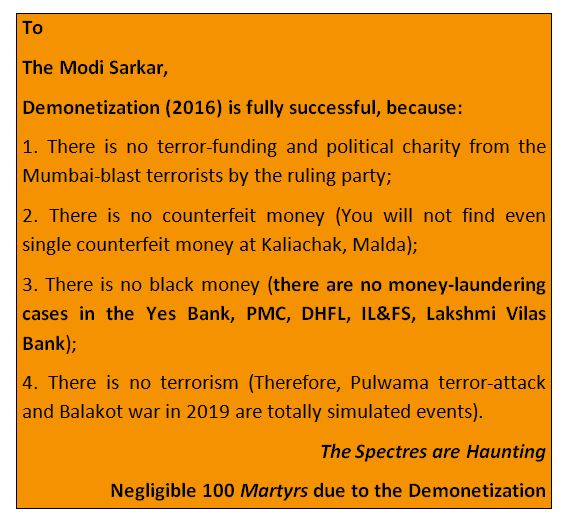

The situation is bleak and we are living within a sick society. (cf. India Wounded: A Bird’s Eye View VIEW HERE ⤡)! A Guru And A Tycoon Feel India’s Endless Bank Salvage Pain VIEW HERE ⤡ (As reported on Jan 13, 2021 © The Economic Times). The cronies are probably working against common persons. Our humble questions are: What is the role of the ruling party here? Is the BJP getting “terror funding” or otherwise “political charity” (euphemism!? Orwellian Newspeak?) from the business tycoons via so-called “underworld” or shadow economic zone by depriving the citizens (yet to be proven by the tiresome process of NPR-NRC-CAA!!!⤡⤡)of Indian Republic???

7. Taking cue from the point 6, we are awfully scared to see the abrupt bankruptcies within the span of last three years. The IL&FS, Dewan Housing Finance Corporation (DHFL), Punjab and Maharashtra Cooperative Bank (PMC), Yes Bank, Lakshmi Vilas Bank (LVB) have collapsed and many other smaller banks in India which are confronting higher risks of collapsing due to rising bad loans (as well as money-laundering) despite the fact of existence of too many governmental vigilant agencies including Income Tax Department.

Bad banks: LVB’s collapse marks 5th financial institution’s failure in less than 3 years. VIEW HERE ⤡ (As reported on 20th November, 2020 ©India Today)

8. Why there are so much bad loans? The answer is quite simple: present government is favouring superrich wilful defaulters! PSU Banks Technically Write Off Over Rs 68,000 Cr Loans, Choksi Among 50 Top Wilful Defaulters: RTI VIEW HERE⤡⤡ (As reported on 28th April 2020 ©CNBC TV18 )

It was predicted by the scroll on the 2nd November, 2018:

We are citing an excerpt from this report:

“One reason for the inflexibility in the insolvency proceedings, said a former Union finance secretary who did not want to be identified, is the government’s fear that it would be seen as being soft on corruption. “It sees even bad loans as fraud,” he said. This is why the government is taking measures such as “extinguishing shareholdings” – that is, getting rid of the promoters of all defaulting companies.” (emphasis added)

We are emphasizing on this word “inflexibility”, though we perceive arbitrary flexibility in the governance. Same measure has not been taken in all the cases of above-mentioned collapsed banks, e.g., only the DHFL has been taken under the newly-introduced IBC. What’s about other banks? The deployment of different laws and codes for the same problem is self-contradictory.

9. At present, most of the listed Companies holding Public Deposits in one form or another are getting defaulted, bankrupted and facing rapid insolvencies. It has been observed that the ‘Loss Reporting’ begins only after they are completely exposed by the fourth pillar of democracy, viz., mass media. Until that the Auditor of that respective company remains in sleeping mode. It is well surprising that even 100% of the net worth has been eroded but the Auditor is signing the Balance Sheet with the remarks “True & Fair View” and a “going concern”. It is only after the bomb get blasted that Auditor comes to know, “Oh no, it’s a Loss Balance Sheet!”

It is embarrassing to note that such a deviation in the Assets of the Company is not known to the Auditors, and yet they are misguiding the public at large and ‘dishonestly’ conducting their profession. If an Auditor claims that it is not a wilful mistake and s/he is unaware of such erosion in Assets, we are sorry to say that in this case his/her competency to act as an Auditor need to be reviewed. A serious action should be taken against such Auditors so that a message is crystal clear to the chartered Accountant Association:

“That Audit means confirming/certifying the Books of Accounts based on which the Funds are being raised and misconduct should lead to pecuniary penalty in form of repaying to the sufferer either by the ICAI as an regulatory body or the member himself.”

Regarding such anomalies, we have informed (14th March, 2021) The President, Institute of Chartered Accountants, India, ICAI Bhawan, Indraprastha Marg, Post Box no: 7100 New Delhi – 110 002. Cf. Reliance On The Sanctity Of Audited Balance Sheet And Safeguarding The Country’s Financial Ecosystem VIEW HERE ⤡ There is no response till date. They must also be respondents in the legal case.

10. On 24 March 2021, CBI filed a new suit against DHFL and its promoters Kapil Wadhawan and Dheeraj Wadhawan, wherein the latter were accused of siphoning off the welfare subsidy fund of Pradhan Mantri Awas Yojana by creating 260,000 fake home loan accounts under the same scheme under the guise of a non-existent branch. The suit says, fake loans were granted worth Rs. 14,046 crore of which 11,755.79 crore were routed to shell corporations and citing these loans, subsidy amounts were claimed under Pradhan Mantri Awas Yojana. [Source: Wikipedia⤡] Thus, the much proclaimed Aadhaar-PAN link with any types of banking transactions has been proven to be failed, if DHFL scam is believed to be true!

A failure of scrutiny: DHFL fraud shows limitations of Aadhaar in plugging leakages. VIEW HERE ⤡ (As reported on 26th March, 2021 © DAILY 2 DAILY NEWS)

DHFL money trail vanishes in Modi’s ‘digital’ India! (VIEW HERE ⤡ (As reported on 30th October, 2019 © The National Herald)

Not only that, it also shows the failure of the much proclaimed Demonetization drive (2016). This sarcastic tweet may be noted:

The conclusive question is: Either the government must admit their failure in executing the PAN-Aadhaar link or must admit that the above-mentioned events had not been happened. In this disjunctive proposition, a case of destructive dilemma (modus tollens), one cannot escape through the horns of the dilemma by undermining that premise.

11. What is the role of the Brand Ambassador, Mr. Shah Rukh Khan, of the DHFL here? May he be treated under the Consumer Protection Act, 2019⤡ for “False and Misleading Advertisements” by violating the rights of consumers? We have approached him also, cf. LET’S DO IT: HITCHHIKING FOR ZAKAT FOR THE AILING FD AND NCD- HOLDERS OF THE DHFL: A LETTER TO SHAH RUKH KHAN, THE DHFL BRAND AMBASSADOR (24/04/2021) ⤡

12. DHFL, was referred to the IBC on 22 November 2019, the RBI appointed a Committee of Creditors (COC) by giving special powers to RBI. DHFL was being run by an Administrator appointed by the RBI. Repayments to FD holders have been stopped and FD holders have been clubbed together with banks and other big lenders in the Resolution Process by the RBI-appointed Administrator. The FD and NCD holders, are waiting for repayment of their monies since then. In the mean time, the RBI has approved the Resolution Plan (18th February, 2021, see the following attachment), which has deprived themselves of their dues.

DHFL RESOLUTION PLAN – PIRAMAL VIEW HERE ⤡

In this regard, we wish to cite the NCLT order on the DHFL-case ⤡ [IA 2431 of 2020 in CP (IB) 4258/MB/C-II/2019 Under Section 60 (5), 227 (2), 239 of the Insolvency and Bankruptcy Code, 2016] points 16-19 and 84-89.

As pointed in point 16 a scathing remark that “…it (The COC) has not considered the same (Mr. Kapil Wadhawan’s Resolution Proposal) on its merits or with its commercial wisdom.” One can understand the position of the DHFL-COC being the pet of the RBI and the Government. However, what is puzzling is that Catalyst Trusteeship Limited holds 52.13% (cf. point 69 of the NCLT Order, as per the DHFL-COC’s RP meetings) of the total voting power in the COC though FD and NCD holders hold more than 65% according to the NCLT Order (cf. Point 87: “…the proposal is not made available to FD, NCD holders who constitute more than 65% of vote share of members of COC”).

The answer my friend, is blowin’ in the wind…

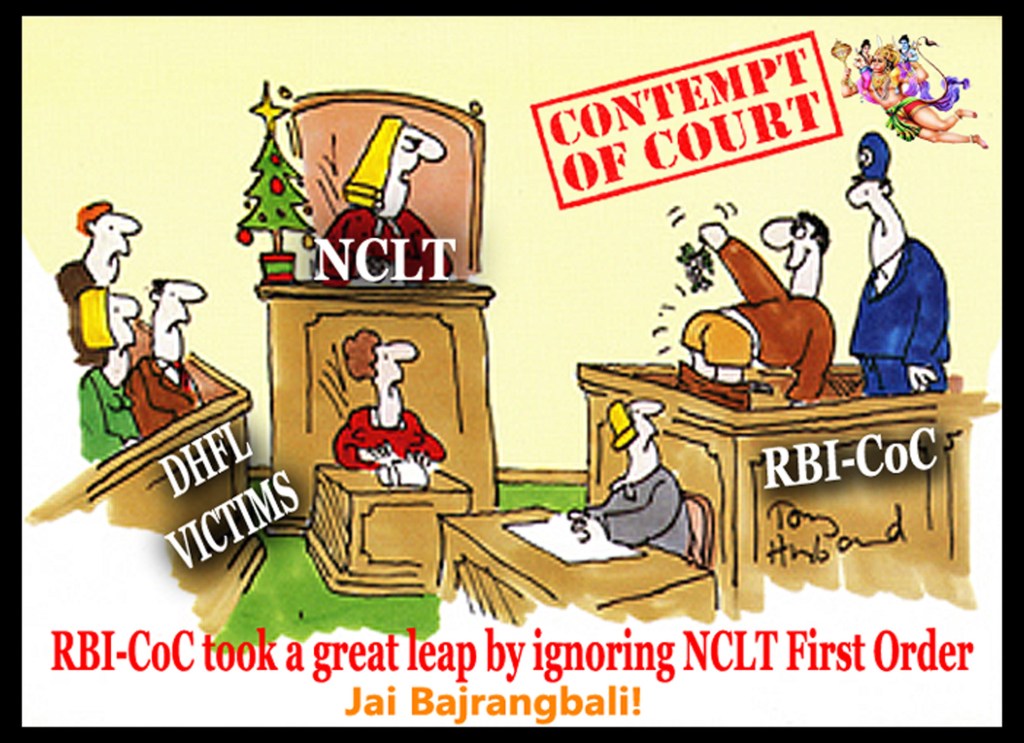

We appreciate (???) the speed in which the RBI-appointed COC for DHFL has moved to the NCLAT⤡ to nullify the previous NCLT order (19/05/2021), without answering the latter within the NCLT-prescribed ten day-span. It is a proof for their (along with the Union Bank, commanding merely 4.04% voting share in the DHFL-COC; cf. Point 55, aforementioned NCLT Order) efficiency as professionals. Peculiarly enough, the date of the order is not mentioned after their signatures in the NCLAT order Company Appeal [(AT) (Insolvency) No. 370 of 2021]. Perhaps due to the speed capitalist hurried emergency, Justice A.I.S. Cheema, The Officiating Chairperson and Mr. V.P. Singh, Member (Technical) of the NCLAT have forgotten to mention the mandatory date after their signatures. The case was heard on 25/05/2021 as it is mentioned at the beginning of the said document.

One may find “Error in jurisdiction vs. Excessive Jurisdiction” VIEW HERE ⤡ (As reported on 17th July, 2020 ©Law Street India) on the part of NCLT (second order) and NCLAT . Though there are precedents, where fixed deposit holders were relieved from their miseries by the NCLAT itself.

NCLAT : Defaulting company liable to repay FDR amount alongwith interest to its deposit holders VIEW HERE ⤡ (As reported on 25th Feb 2020 ©TaxGuru)

13. We have smelt the rat in the CoC, especially in the anomalies in the behaviours of the RBI-appointed DHFL Administrator Mr. R. Subramaniakumar and Ms. Charu Sandeep Desai, Authorized Representative of the Fixed Deposit Holders. We have mentioned all these in a letter to The Honourable President, The Republic of Indiadated 24th March, 2021: Smelling The Rat In The DHFL-COC Resolution Process⤡ with evidences. Again, we have dispatched our grievances to the President, Republic of India, regarding the same matter on 2nd June, 2021, PLEASE COMPOSE AN OBITUARY FOR THE RBI-APPOINTED COMMITTEE OF CREDITORS (COC) FOR THE DHFL⤡

Our questions were simple enough:

“It is being circulated in the media that only the highest bidding price will be distributed among the lenders/investors/creditors’ dues/investments. In that case:

a) Will the distribution of lenders’/ investors’/creditors dues (especially FDs) only be on the basis of the buying price of the bidders?

Or

b) Will it also involve the working capital, revenue generation or otherwise profits, monthly income, recovery of loans, and the overall assets of the DHFL? Will it not follow the waterfall mechanism in case of FD holders’ (may be deferred) repayment? What will be the net sales, income from operations, other operating income per annum, the profit, overall assets of DHFL, a running company?

In the case of FD holders, will not all these variables (Question b) be considered for full payment (with interest) of their investments?

We are in big trouble with agony/anguish/anxiety. Kindly remove our confusion regarding the repayment of our dues.”

Our questions are still to be answered. Are they (RBI-appointed DHFL Administrator Mr. R. Subramaniakumar and Ms. Charu Sandeep Desai, Authorized Representative of the Fixed Deposit Holders) not subservient to All India Services (Conduct) Rules, 1968. 9 or the Section 107⤡, Section 201⤡, Section 505⤡ of the Indian Penal Code (IPC). The allegations were mentioned in the above mentioned letters to the President.

Even the Standing Committee of the Parliament of India questioned the credibility of the CoC.

Standing Committee on Finance raps IBC over unsustainable haircuts, says 13,000 cases worth Rs 9 lakh crore pending VIEW HERE ⤡ (As reported on August 03 2021, ©Moneycontrol)

immediately after the Parliamentary Standing Committee’s report the the corporate affairs ministry is working with the finance ministry, RBI and the Indian Banks’ Association on the conduct of the committee of creditors (CoC) under the insolvency resolution process.

IBC: Govt. working with RBI on CoC’s conduct VIEW HERE ⤡ (As reported on 27th August ©The Hindu, PTI)

14. Therefore, we have to check the audit of the company, in which we are totally illiterate. Therefore we are citing others’ opinions, collected from different web platforms:

Opinion-1:

According to the DHFL-COC RP, the overall distribution of the assets, bidding price, profits and gains are as follows (as calculated by Mr. Ashok Khemka, IAS, in his Tweet⤡, 16/01/2021):

| WILL THIS BE A RESOLUTION SCAM? | |

| BOOK VALUE OF THE ASSETS | 93, 700 CR |

| FRAUD APPLICATION U/S BEFORE NCLT | 33, 000 CR |

| BIDDER’S VALUE | 32, 250 CR |

| WHITHER GOES THE BALANCE? | 28, 450 CR? |

| WHO LOSES? | |

| FINANCIAL CREDITORS | 55, 000 CR |

| SHAREHOLDERS | 6, 300 CR |

| STATUROY DUES | 88 CR |

| OPERATIONAL CREDITORS | 70 CR |

| TOTAL | 61, 458 CR |

| WHO GAINS? | |

| ADVISORS | 130 CR |

| EARLIER DHFL PROMOTERS | ??? |

| NEW OWNERS | ??? |

| TOTAL | 61, 458 CR |

| ABOVE FIGURES ARE ESTIMATES |

The total auditing report is way too opaque.

Opinion -2:

“If 91000cr home loan is lent @ 13% (avg), what will be yearly EMI collected?

It is 11830cr which is 985cr per month.

In last 1.5 years since November, 2019, DHFL EMI collected so far is 16000cr/18months which means 888cr per month.

Shortage is 985 – 888= 96cr

NPA/siphoned money can be calculated reversely from shortfall in EMI amount assuming the same average 13% = 96cr*12months=1152cr*100/13= 8861cr

So 91000 – 8861cr = 82138cr is the actual present value of DHFL.

Collected EMI speaks itself for the actual value of DHFL..

It is definitely not 36000cr!!!

Liquidation value stands at 47000cr!!

8861cr is missing in books.

Which should likely be the siphoned money using Bandra books.

Surprisingly Wadhawan is saying he will pay this 9000cr upfront as cash to retail and pay all others with 100% by running the company as it is generating income from EMI today and pay back 100% to banks, NCD, MFs , institutional investors etc in next 6 to 7 years..

Logically it is achievable.”

Opinion-3:

“I would like to share with you that prior to finalization of DHFL resolution plan, I had seen a video in which it was told that Piramal’ s offer does not include the RECOVERY amount (which will be recovered from Wadhwan Brothers in future by seizing their assets) for distribution to FD holders and will straight away owned by Piramal group which means Piramal have purchased Rs. 94000 Cr. DHFL Property just by paying 34000 Cr LESS –>RECOVERY AMOUNT (MAY BE Rs. 30000 Cr = ONLY Rs. 4000 CRORES. All this proves that CoC members including Ms. Charu Sandeep Desai have also manipulated the deal and CHEATED ALL OF US FOR EARNING THEIR SHARE IN NET PROFIT OF Rs. 90000 CRORES.”

Opinion-4:

“Total amount of FD is around 5300 crores and amount of retail fd holders is around 2200 crores and the remaining are institutions,1800 crores of pf money of UPPSL will be paid by govt of Uttar Pradesh, SLR maintained with NHB is around 1300 crores plus just 1000 crores is required to pay retail FD-holders in full the accrued interest after 3rd December, 2019.”

Opinion-5:

“In the Bombay High Court has proved the DHFL is solvent. So, the Bombay High Court allowed for paying 800cr per month for securitization. ⤡

In the NCLT, the RBI is trying to prove it is insolvent. ⤡ ⤡

It is the highest level of contradiction.

Amidst this, the company is swiftly running its business (as evident from the above box, too), i.e., it is very much a solvent ongoing concern as they are lending 500cr per month for home loans and they are also earning from their previous loans.

DHFL only needs slight restructuring, not haircuts for all public depositors.

The Banks have additional tools to recover the dues; whereas we, the public depositors and NCD holders, have no such avenue. Thus it is a double advantage to the Piramal Enterprises. They will take their pound of flesh from the RP. Clearly it is a very sinister move on the part of the RBI.

Government should not deliberately sell DHFL to the Piramal Enterprises. It can appoint a committee of experienced retired bankers (not like the present RBI-appointed DHFL Administrator) and let the DHFL run after slightly restructuring it so that all classes of creditors and lenders get back their 100% principle amount with interest. Though we are not interested in the choice of the owner for this ongoing solvent company, we only wish to get back our hard-earned public money in full along with due compensation for infringing our fundamental human rights due to financial abuse.”

All the above opinions, if believed to be true, could/might prove that the DHFL is a ongoing concern and it is handed over to Mr. Ajay Piramal in pre-determined way in a throw way prices by imposing huge haircut on the creditors and investors as it is expected in the context of crony and monopoly capitalist⤡ plutocratic regime [cf. India Is No Longer a Democracy but an ‘Electoral Autocracy’: Swedish Institute ⤡ (As reported on 11th March 2021, © The Wire), The Freedom House also dropped India from the list of “Free Countries” in its annual report entitled “Democracy under Siege” VIEW HERE ⤡. India is now only ‘partly free’ under Modi, says report ⤡ (As reported on 3rd March, 2021 © BBC News)].

The selling of the DHFL to a reportedly non-listed company, viz., Piramal Capital & Housing Finance, by reverse-merger is the suspicious one. The ruling party’s partial efforts for selling the ongoing company at a throw-away price (at 75% discount)—or as a free gift to the father of the damaad of a favoured business tycoon. We are using the word damaad instead of son-in-law by taking cue from our Hon. Madam FM, when she was targeting Mrs. Sonia Gandhi’s son-in-law: ‘Not working for damaads‘: FM Nirmala Sitharaman fires back at Congress over ‘crony capitalists’ jibe⤡ ( as reported on Feb 12, 2021 ©Times Now.news.com)

In response to such usage of regarding kinship term, we cannot but help to remember the beginning of ostentatious display of Ambani-Piramal family-bond.

Isha Ambani and Anand Piramal wedding : world’s most expensive wedding card ! VIEW HERE ⤡

Opinion-6

A. RS. 8994.54 Lakh worth Fresh LOAN distributed in just 2 months (during Feb21 Rs.3230.22 Lakh & during March 21 Rs. 5764.32 Lakh).

B. Collection/Recovery from borrowers-

Total Rs. 10640.08 crores as detailed below:

February 20. Rs.1457 crores

September 20. Rs. 1195.07 crores

October 20 Rs.1218.23 crores

November 20 Rs. 1267.95 crores

December 20 Rs. 1327.94 crores

January 21 Rs. 1334.59 crores

February 21 Rs. 1438.28 crores

March 21 Rs. 1401.02 crores

On one hand, they have stopped repayments to FD holders showing reasons of INSOLVENCY (as if DHFL is DEAD) & on other hand they are continuing their business WHICH IS TOTALLY UNJUSTIFIED.

During current pandemic Covid19 scenario when situation is worsening day after day and badly effecting lower/middle class people including senior citizens like me, all sources of income is totally STOPPED and there is huge increase in medical expenses (victimized by hospitals through straight away looting by hospitals, house hold essential items viz. Groceries etc.)

21-07-2021

Opinion-7

The cat is out of the bag, when Moneylife has briefly summarized the discrepancies of the whole audit:

DHFL Resolution: Piramals Profit Plentifully, Pittance for the Rest! VIEW HERE ⤡ (As reported on 1st October, 2021 ©Moneylife)

15. Moreover, there are questions over the bidding process also. It is found that Oaktree Capital emerges highest bidder for Dewan Housing Finance. VIEW HERE ⤡ (As reported on 14th December, 2020 ©The Mint)

DHFL resolution bid: A guru and a tycoon feel India’s endless bank salvage pain VIEW HERE ⤡ (As reported on 13th January, 2021©The Mint) [ Kindly note that after “sweetening” the bidding price, “Oaktree’s Jan. 6 letter to creditors says their vote will ‘define the reputation‘ of India’s bankruptcy code in global markets. But international standing will be a byproduct of a fair, rules-based bidding process that holds up to domestic legal scrutiny and minimizes contagion risk. With Indian banks’ exposure to shadow financiers increasing, it’s critical to establish a template that can be used for swift resolution in the future. ]

DHFL bids: Oaktree mulls legal action ‘seeing’ creditors’ ‘bias’ towards Piramal’s offer VIEW HERE ⤡ (As reported on 3rd January, 2021© The Hindu Business Line )

15A. TRANSPARENCY CONCERNS IN THE CoC-LED PROCESS: A CLOSER LOOK

We must pause here and ask: was the DHFL CIRP — the first deposit-taking financial institution ever resolved under the Code — actually transparent, or only performatively so?

In February 2020, 24 parties expressed interest in DHFL. By late 2020 this had shrunk to four: Oaktree Capital, Piramal (through PCHFL), the Adani Group, and Hong Kong’s SC Lowy. THEN THE TWIST: Adani — despite having originally proposed only for parts of the business — submitted an unsolicited bid for the WHOLE company AFTER the 9 November 2020 deadline had already closed. Oaktree, Piramal and SC Lowy jointly wrote to the CoC asking that this post-deadline bid be rejected as a breach of process. What did the CoC do? It reopened bidding and invited fresh plans. SC Lowy walked away immediately, citing unfair treatment. A bidders’ letter to the CoC and RBI put it plainly: bidders need confidence the process is “fair, transparent and reliable… both in perception and fact.” We ask: WHY WAS THE FIELD ALLOWED TO NARROW FROM 24 TO 4 TO EFFECTIVELY 2 THROUGH REPEATED DEADLINE EXTENSIONS AND A POST-DEADLINE BID?

Then came the vote. Between 30 December 2020 and 15 January 2021, ~77,000 FD holders — disproportionately senior citizens — voted electronically on the resolution plan. EVERY SINGLE ONE OF THEM VOTED AGAINST IT. They were overridden anyway: voting power tracks debt value, not headcount, so the plan passed with ~94% approval carried entirely by secured banks. But look at HOW they were made to vote: no option on the ballot allowed voting for full repayment; no paper or assisted alternative existed for elderly voters, many of whom hit technical failures and simply couldn’t vote at all; nothing could be downloaded, printed, or retained; and to this day NO ballot record, audit log, or class-wise turnout has ever been published. WE ASK: WOULD THIS PROCESS PASS MUSTER FOR A MUNICIPAL BY-ELECTION IN INDIA? The reply is NO.

And who paid for all this? The Authorised Representatives — including the FD holders’ own AR — draw a statutory ₹25,000 PER MEETING, paid out of CIRP costs, which come out of DHFL’s OWN ESTATE. Nineteen CoC meetings are recorded by the time of plan approval. In other words: THE VICTIMS SUBSIDISED THE MACHINERY THAT IMPOSED THEIR OWN HAIRCUT.

What about the promises made to win depositor goodwill? Oaktree dangled ₹300 crore extra for FD holders (structured through a subsidiary sale that, as a foreign entity, it faced real legal obstacles executing). Piramal promised ₹150 crore plus a 10% top-up, calling it “an attempt to share in the pain of those most affected.” SBI Capital Markets — the Administrator’s own advisors — valued Piramal’s offer at ₹150 crore and OAKTREE’S AT ZERO. What actually landed? ₹1,241 crore against ₹5,375 crore in admitted claims — 23%. The “10% top-up” was 10% of an already-gutted base, not of the original claims. “Sharing the pain” turned into a ~77% loss for depositors who had already voted no.

Can anyone actually examine how this happened? NO. The “commercial wisdom” doctrine bars tribunals from reviewing CoC decisions on the merits. CoC banks claim fiduciary exemption from the RTI Act. The Administrator says the RTI Act doesn’t apply to the corporate debtor. Minutes, evaluation matrices, SBI Caps scoring, ballots, e-voting logs — MOSTLY UNPUBLISHED, still. (Separately vindicating this pattern: the ₹1 valuation given to ₹45,000+ crore in fraud-recovery claims, challenged by 63 Moons Technologies as unjust enrichment, was ultimately remitted by the Supreme Court in April 2025 — the objectors were right to smell a rat.)

IS THIS SURPRISING, GIVEN WHERE INDIA STANDS ON EVERY INDEPENDENT TRANSPARENCY MEASURE? Transparency International’s Corruption Perceptions Index: India peaked at 41/100 in 2019 (the year DHFL’s CIRP began), fell to 38 by 2024, recovering only marginally to 39 in the latest Index — still below 2019, still well under the 50-point line TI treats as a serious systemic problem. Reporters Without Borders’ Press Freedom Index: India fell from 140th (2014) to as low as 161st (2023), sitting at 157th in 2026 — “very serious” throughout. V-Dem reclassified India an “electoral autocracy” in 2021; Freedom House downgraded it from “Free” to “Partly Free” the same year; the EIU’s Democracy Index shows the same slide into “flawed democracy” territory. WE ARE NOT CITING THESE TO PROVE THIS CASE — we cite them because a depositor class demanding transparency from a CoC in 2020–2026 was demanding it from a system whose OWN measured capacity for transparency was falling at the same time.

16. The proposed course of action would be where the FD Holders demand that the Insolvency and Bankruptcy (Insolvency and Liquidation Proceedings of Financial Service Providers and Application to Adjudicating Authority) Rules, 2019 and Notification bearing No. S.O 4139 (E) dated 18.11.2019 passed by the Central Government should be declared arbitrary, illegal, unjust and against public interest, thereby violating Articles 14, 19, 21, 26, 29 and 30 of the Constitution of India and Reserve Bank of India Act, 1934. Reserve Bank of India should be directed to undertake the revival/ restructuring of Dewan Housing Finance Corporation Ltd, as was done in the case in exercise of powers conferred under Section 45 (1) of the Banking Regulation Act, 1949. Reserve Bank of India should undertake the resolution of Dewan Housing Finance Corporation Ltd. in public interest, in terms of Sections 45-MBA and 45-QA of the Reserve Bank of India Act, 1934. FD Holders should also challenge the resolution plan approved by the CoC and seeking that the Hon‟ble Court scrap the plan in full or at least partly, allowing the fixed depositors to be paid in full, as thousands of common people have invested their incomes and monies with the Corporate Debtor as way of fixed deposits.

17. THE CHEKOVIAN TURN: WADHAWAN MOVES SC, WANTS LENDERS TO CONSIDER BID FOR THE DHFL

“The erstwhile promoter submitted that his proposal being “in public interest” would result in 100% payment of the liabilities of the secured creditors as well as other creditors like deposit holders, etc, whereas Piramal Capital and Housing Finance’s RP is resulting in an overall huge loss of more than Rs 53,000 crore to the nationalised banks and small depositors.

This “shows a complete misuse and subversion of the insolvency process of taking over a valuable company having an asset base of approximately over `68,000 crore for a discount of approximately Rs 37,000 crore,” the appeal stated.

Stating that his offer is 150% higher than the offer made by the successful resolution applicant, Wadhawan said that he was constrained to make the settlement proposal prior to the voting in view of abysmal bids being received for DHFL providing for a haircut of more than 60% to the creditors.

According to the appeal, “DHFL currently has a cash reserve of Rs 16,000 crore in addition to retail assets (i.e. loans given to small homebuyers) of approximately Rs 30,000 crore which are yielding interest at the rate of 10% and investments of approximately Rs 3,000-4,000 crore.”

Besides, the corporate debtor has a wholesale book (i.e. loans given to builders for development of project loans against property, etc) in excess of Rs 27,000 crore, it said, adding that despite the value available in DHFL, the lenders were offering the company to Piramal “on a platter at a huge discount”.”

SOURCE: Wadhawan moves SC, wants lenders to consider bid for DHFL VIEW HERE⤡ (As reported on June 02, 2021 ©The Financial Express)

Further, with the recent SC judgement regarding validity of invoking personal guarantees of promoters in IBC. We are emphasizing on this verdict: Bankruptcy will not void personal guarantees: Supreme Court VIEW HERE ⤡ (As reported on May 22, 2021 ©The Times of India)

18. The victims of the DHFL Scam are sandwiched due to clashes or the incommensurability among the RBI act, the NHB Act, Companies act and the newly introduced IBC.

Section 29 of the NHB Act safeguards repayments to public depositors by any Housing Finance Company to continue its business. DHFL is very much a going concern and doing business even now.

Public FD holders are not lenders and they should not be clubbed with banks and financial creditors in the resolution process under the IBC. There is no precedence of such clubbing of FD holders of an NBFC.

IBC, or any Act, is meant to prevent any activity which is against public interest. Small public depositors would like to lose their life savings due to the newly introduced IBC, which otherwise is safeguarded by the prevailing NHB Act.

Despite the fact that IBC⤡ is a “one step solution” for financial disputes, in reality, its validity is also challenged. Many sufferers are asking a crucial question: Is IBC an investor-friendly code or an escape route for the wilful defaulters?

The amendments (2020) of IBC mandated a minimum of 100 home buyers to come together to file an insolvency application in the National Company Law Tribunal (NCLT) to trigger the IBC against a defaulting developer.

SC upholds validity of IBC Amendment Act, 2020 VIEW HERE ⤡(As reported on January 19, 2021) © Business Line

Supreme Court upholds validity of Insolvency and Bankruptcy Code (Amendment) Act, 2020 VIEW HERE ⤡ (As reported on 19 Jan, 2021) ©Bar and Bench

Supreme Court Upholds Sections 3, 4 & 10 of IBC Amendment Act 2020 VIEW HERE ⤡ (As reported on 19 Jan 2021) ©Live Law

The Supreme Court upheld amendments in the Insolvency and Bankruptcy Code that prescribe that at least 100 allottees from the same real estate project should support the initiation of corporate insolvency resolution process in the National Company Law Tribunal against their property developer.

A three-judge Bench led by Justice Rohinton F. Nariman found in their 474-page judgment, based on petitions filed by allottees of real estate projects and money lenders who finance such property endeavours, said

“The connection with the same real estate project is crucial to the determination of the critical mass… If it is to embrace the total number of allottees of all projects, which a promoter of a real estate project may be having, in one sense, it will make the task of the applicant himself, more cumbersome. It becomes a sword, which will cut both ways. This is for the reason that the complaints, relating to different projects, may be different.”

“Prescribing a time limit in regard to pending applications, cannot be, per se, described as arbitrary; as otherwise, it would be an endless and uncertain procedure. The applications would remain part of the docket and also become a Damocles Sword⤡ overhanging the debtor and the other stakeholders with deleterious consequences also qua the objects of the Code.”

The Chekhovian turn of the story regarding the amendments of the IBC, the apex court said “the law came as a bolt from the blue”. This small remark is more than enough for challenging the validity of the IBC. It has prompted SC to invoke Art. 142⤡.

New bankruptcy law caused disagreements between Prime Minister Narendra Modi’s government and the RBI.

There are more discontents on this new code. I am citing here only two of them:

Urgency to fix India’s bankruptcy code⤡ (As reported on 28 Dec 2020) ©The Mint

IBC mechanism needs structural changes to expedite faster resolution of companies⤡ (As reported on Jan 27, 2021) © The Economic Times

Even Urjit Patel, former Reserve Bank of India Governor had a dispute with the government, especially with the PM as the rift centered around a February 2018 circular issued by the RBI, which forced banks to immediately classify borrowers as defaulters when they delayed repayments, and which barred defaulting company founders from trying to buy back their firms during insolvency auctions. In a book released Friday, Patel — who headed the RBI between September 2016 and his unexpected resignation in December 2018 — said the government seemed to lose enthusiasm for the legislation in the middle of the year he left the central bank.

Mr. Patel wrote,

“Instead of buttressing and future-proofing the gains thus far, an atmosphere to go easy on the pedal ensued,….Until then, for the most part, the finance minister and I were on the same page, with frequent conversations on enhancing the landmark legislation’s operational efficiency.”

(Cited from the ©Financial Express)

Ex-RBI chief Urjit Patel says insolvency rules caused rift with government. VIEW HERE ⤡ (As reported on July 24, 2020) ©Financial Express

19. As per the current consideration of the DHFL-COC (17th June, 2020) after the second NCLT order, the Indian Army Group is getting repayment in full where as the other small investors, i.e., FD Holders, are only getting 40% of their total due amount. Is not this type of partial treatment characteristic to an exclusive society (a la Jock Young VIEW HERE TWEET ⤡) built on discriminatory privileges?

Article 14 of the Constitution of India (as part of the inalienable “Right to Equality”, Fundamental Rights) provides for equality before the law or equal protection of the laws within India. It states: “The State shall not deny to any person equality before the law or the equal protection of the laws within the territory of India.” Therefore, the above decision of the DHFL-COC violates the underlying egalitarian provisions of the Constitution of India by providing relative importance to a certain group above another. Where is the much-cherished distributive justice (iustitia distributiva) in this case? Therefore, we demand the restoration of our justiciable fundamental rights, which are being infringed, through judicial intervention.

20. After the forceful, impulsive and illegal disbursement of 23% of the principal amount to the DHFL FD Holders by Mr. Ajay Piramal on 29th-30th September, 2021:

WHO IS PIRAMAL?

WHO IS AJAY PIRAMAL?VIEW HERE ⤡

Father of a damad of a favoured business tycoon?

An allegedly savage capitalist?

A non-entity, non-MNC, whose company is not even listed?

a. Piramal, though the so-called “successful bidder” according to lowest quasi-judicial body+ the RBI-appointed CoC & a father of a damad of a business tycoon, preferred by the ruling party (bribing? Political charity? Terror funding?), Piramal is reportedly performing illegal activities despite pending sub judice cases.

b. The de facto “owner” (?self-proclaimed?) of the DHFL is also part of our case as they are also mentioned as the respondents. His “claim” as an owner of the DHFL binds him to be a party in our case.

Kindly note that the recent SC judgement regarding validity of invoking personal guarantees of promoters in IBC. We are emphasizing on this verdict: Bankruptcy will not void personal guarantees: Supreme Court (As reported on May 22, 2021 ©The Times of India)

c. The greatest alleged mistake he had done was that, when the RBI-appointed CoC approached the NCLAT, the lower quasi judicial body, he, a non-entity, accompanied the CoC & the Union Bank of India without answering the legitimate questions raised by the NCLT (lowest quasi judicial body) first order (our weapon–in 84 page-verdict, everything was revealed) that was rejected without any arguments. That appears to be an instance of the “contempt of the court”.

Hence, this is possible only within the realm of a thoroughly plutocratic regime run by the cronies. Resist that regime by non-violent all-out-attack along with the judicial means!

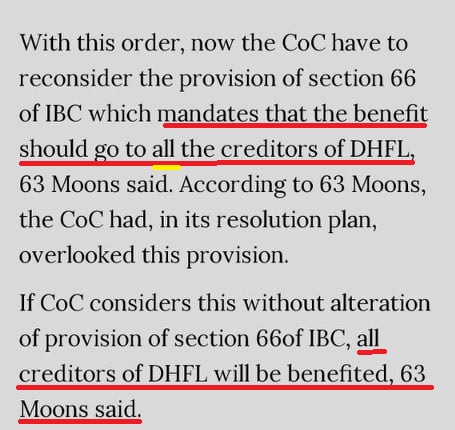

d. On 27/01/2022, the NCLAT ordered the DHFL-CoC to consider 63 moon’s plea and reconsider its resolution plan in favour of Piramal accordingly. The 63 Moons has made its appeal on the basis of Section 66⤡ of the IBC, which, according to the 63 Moons, provides for the “benefit of all the creditors” in the long run. However, this provision was overlooked by the DHFL-CoC due to its fraudulent state of affairs. With this NCLAT order, DHFL Administrator R. Subramaniakumar and Public Depositors’ Representative Charu Sandeep Desai are seriously at stake! The Conduct of the CoC (in general) has also been questioned by the Standing Committee of the Parliament as well.

NCLAT asks CoC to consider 63 moons’ plea in DHFL Resolution Plan VIEW HERE ⤡ (As reported on 27th January, 2022 ©The Times of India)

NCLAT asks CoC to reconsider value of DHFL’s recoverable assets VIEW HERE ⤡ (As reported on 27th January, 2022 ©Moneycontrol)

Furthermore, on 27th January, 2022, the NCLAT pointed out that:

“The National Company Law Appellate Tribunal (NCLAT) set aside the order of the National Company Law Tribunal, Mumbai, which directed the administrator of Dewan Housing Finance Corporation Ltd. (DHFL) to place the second settlement proposal sent by Kapil Wadhawan before the Committee of Creditors (CoC).

The order came on a batch of petitions filed by Union Bank of India (on behalf of the CoC), DHFL’s administrator and Piramal Capital & Housing Finance (successful resolution applicant) challenging NCLT’s order.

While setting aside the NCLT order, a Bench of judicial member M Venugopal and technical members VP Singh and Dr Ashok Kumar Mishra held that “the said exercise was beyond the jurisdiction of the Adjudicating Authority (NCLT) hence unsustainable and liable to be set aside”.

It observed that the directions passed by NCLT came despite the fact that CoC already approved the resolution plan submitted by DHFL by an overwhelming majority and the plan approval application filed by the administrator had been reserved for orders by the Adjudicating Authority.“

NCLAT sets aside NCLT order permitting consideration of Kapil Wadhawan’s settlement proposal VIEW HERE ⤡ (As reported on 31st January, 2022 ©Bar and Bench)

DHFL: NCLAT sets aside order that directed to consider Wadhwan’s 2nd offer VIEW HERE ⤡ (As reported on 31st January, 2022 ©Business Standard)

Certain relevant portions from the said judgment, highlighting the basal “illegality” of the DHFL-CoC and its approved Resolution Plan are cited as follows:

The NCLAT Judgment, passed on 27/01/2022, is being provided as follows in PDF:

Update: The Supreme Court of India has stayed the above NCLAT order on 11th April, 2022.

Supreme Court stays NCLAT order on DHFL case VIEW HERE ⤡ (As reported on 12th April, 2022 ©Financial Express)

UPDATE (01.04.2023):

On 27th March, 2023, the Supreme Court of India dismissed the allegations made by the Enforcement Directorate (ED) and upheld the default bail granted to DHFL’s ex-promoters Kapil Wadhawan and Dheeraj Wadhawan by the Bombay High Court in the Yes Bank-DHFL Money Laundering case. No criminal charges against the Wadhawan brothers have been proved conclusively yet. This has a direct binding on the future outcome of the DHFL case.

Yes Bank-DHFL scam: Supreme Court upholds default bail granted to Kapil, Dheeraj Wadhawan VIEW HERE ⤡ (As reported on 27th March, 2023 ©Economic Times)

21. The present situation also violates United Nations Guiding Principles on Business and Human Rights ⤡ in this context, “Access to remedy for victims of business-related abuses”.

The UNGP declares in terms of its 1st foundational remedy: “States must protect against human rights abuse within their territory and/or jurisdiction by third parties, including business enterprises. This requires taking appropriate steps to prevent, investigate, punish and redress such abuse through effective policies, legislation, regulations and adjudication” , and also that the “States should exercise adequate oversight in order to meet their international human rights obligations when they contract with, or legislate for, business enterprises to provide services that may impact upon the enjoyment of human rights.”

The UNGP also states: “Business enterprises should respect human rights. This means that they should avoid infringing on the human rights of others and should address adverse human rights impacts with which they are involved.” (11th Foundational Principle)

Though, the sad truism is that “International law is the vanishing point of jurisprudence” ⤡, if sovereign government would cut a sorry figure to implement all the above procedures, one, a financially abused person, has to take their recourse to the vanishing point, i.e., parallel international “law” (?) without hampering the sovereignty of the imagined nation state⤡. In doing so, the state must be compelled to fulfil its international human rights obligations.

“The Reserve Bank of India needs to take human rights more seriously and it should meet their human rights responsibilities without compromising the sovereignty of our imagined nation state. It should meet their monetary and financial responsibilities for greening the financial ecosystem (as decided by the 36 central banks and banking supervisors in the Central Bank and Supervisors Network⤡”, July 2019). “Protect, Respect and Remedy⤡” (one of the 31 principles implemented by the United Nations) on the issue of human rights and transnational corporations and other business enterprises.

Cf. Why Central Banks Need to Take Human Rights More Seriously VIEW HERE ⤡ (As reported on 15th July, 2019 ©African Eye Report)

To understand the full scam in Hindi, please view the following video:

DHFL Delisting SCAM|अनकहे राज़⤡

See also: Confession Of A Victim Of Financial Abuses VIEW HERE ⤡

UPDATE (08.04.2024):

After nearly five years, NCLT admits insolvency resolution plea against the erstwhile promoter of DHFL Kapil Wadhawan VIEW HERE ⤡ (As reported on 4th April, 2024 ©The Economic Times). What kind of anachronism is this? How can a so-called already “insolvent” company that has underwent a CIRP be declared insolvent by the lowest-quasi judicial body years after Piramal’s adverse possession of it? If it is “insolvent” in April 2024, how could it have been “insolvent” before that?

178 Comments