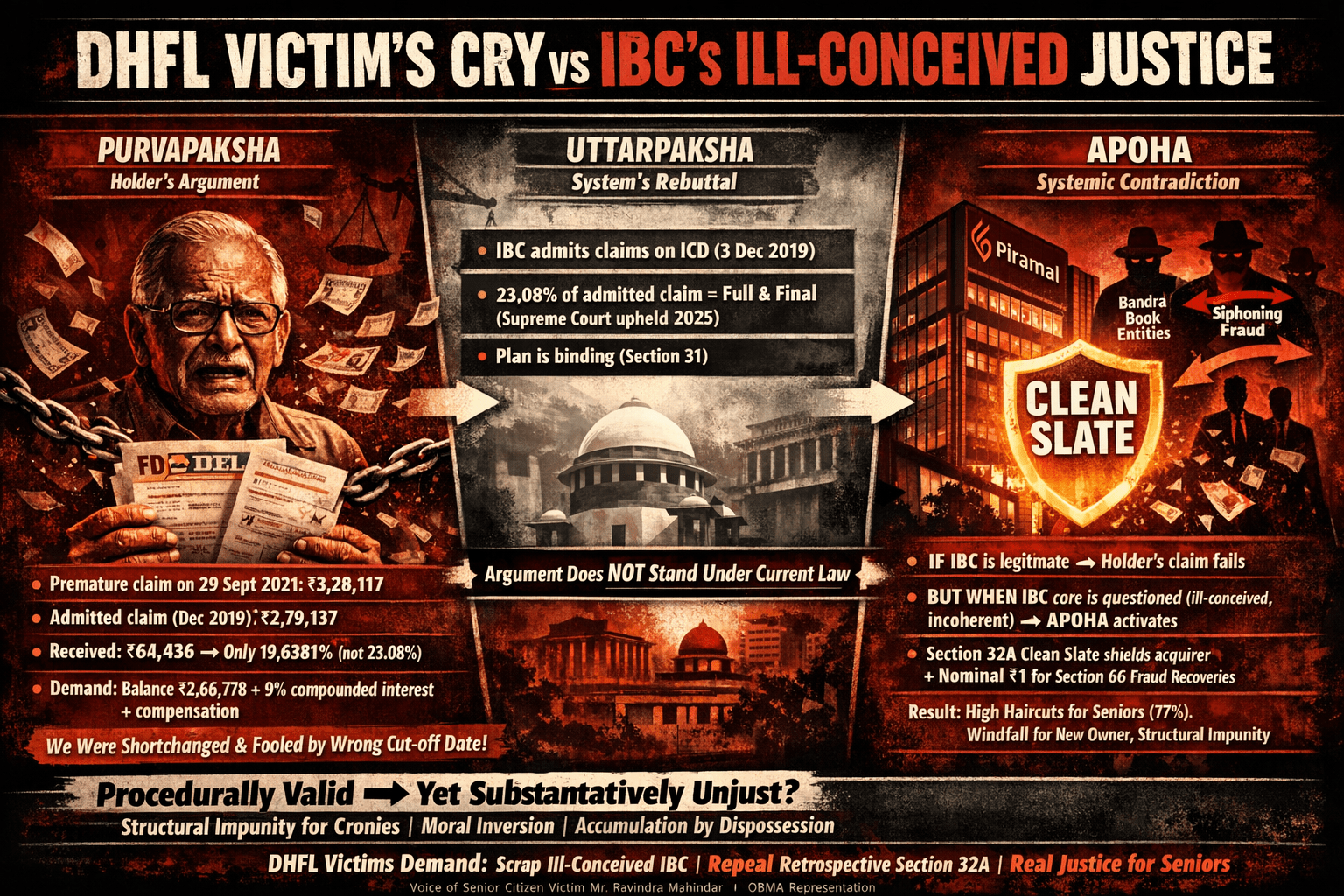

This article examines a senior DHFL fixed deposit holder’s grievance against the 23.08% recovery under the Piramal resolution plan. In Purvapaksha, Mr. Ravindra Mahidhar, the senior citizen FD Holder in question, argues that using the December 2019 cut-off instead of the 29 September 2021 payment date shortchanged him, recalculating his claim at ₹3,28,117 (versus the admitted ₹2,79,137) and receiving only 19.64% instead of 23.08%. Uttarpaksha rebuts that under IBC rules, claims are fixed at the Insolvency Commencement Date, the payment matches the approved plan, and the Supreme Court (2025) upheld it as binding and final. Apoha then probes the deeper paradox: while the individual claim fails if IBC is accepted as legitimate, questioning the IBC’s core as an ill-conceived and incoherent law reveals structural contradictions — particularly between Section 32A’s clean slate immunity and Section 66’s fraud recovery provisions — raising concerns of systemic unfairness, moral hazard, and crony sanitisation for retail victims.

Category Archives: Activities

Our current activities concentrate on the case of Dewan Housing Finance Corporation Limited (DHFL), India. While exploring and investigating this particular case, we have found that India’s crony ruling party, gangsters, banksters as well as religious gurus and institutions are involved in the same. Therefore, to break such collusion, we have decided to deploy an “all out attack” on the existing paradigm of neoliberal market economy as well as market fundamentalism. ***DISCLAIMER: We have collected all the data from available sources on the internet as given on the official portals of media houses, websites and institutions and organizations. We are not first-hand reporters and hence, we are not liable for any inadvertent error or value-loaded statements made on those portals. All propositions have to be viewed as descriptive assertions on the given point of concern.***

Predetermined “Democracy”: Why the 2026 West Bengal Assembly Election Stands Rigged—and Must Be Boycotted!

Ahead of the 2026 West Bengal Assembly elections, nearly 91 lakh voters — almost one in eight — have been deleted through the Special Intensive Revision (SIR), with independent reports showing Muslims disproportionately targeted in opposition strongholds, mirroring a nationwide BJP playbook of communal disenfranchisement. This purge is compounded by engineered bogus additions via bulk Form-6 applications, money-muscle power including pre-poll cash and freebies distribution, and opaque EVM vulnerabilities, all allegedly enabled by a captured Election Commission and passive Supreme Court. The piece argues that these three layers constitute institutional “vote dacoity” turning elections into a managed authoritarian spectacle, and calls for a total boycott of the polls, aggressive use of NOTA, Right to Recall, and proportional representation as the only moral response to reclaim genuine democracy.

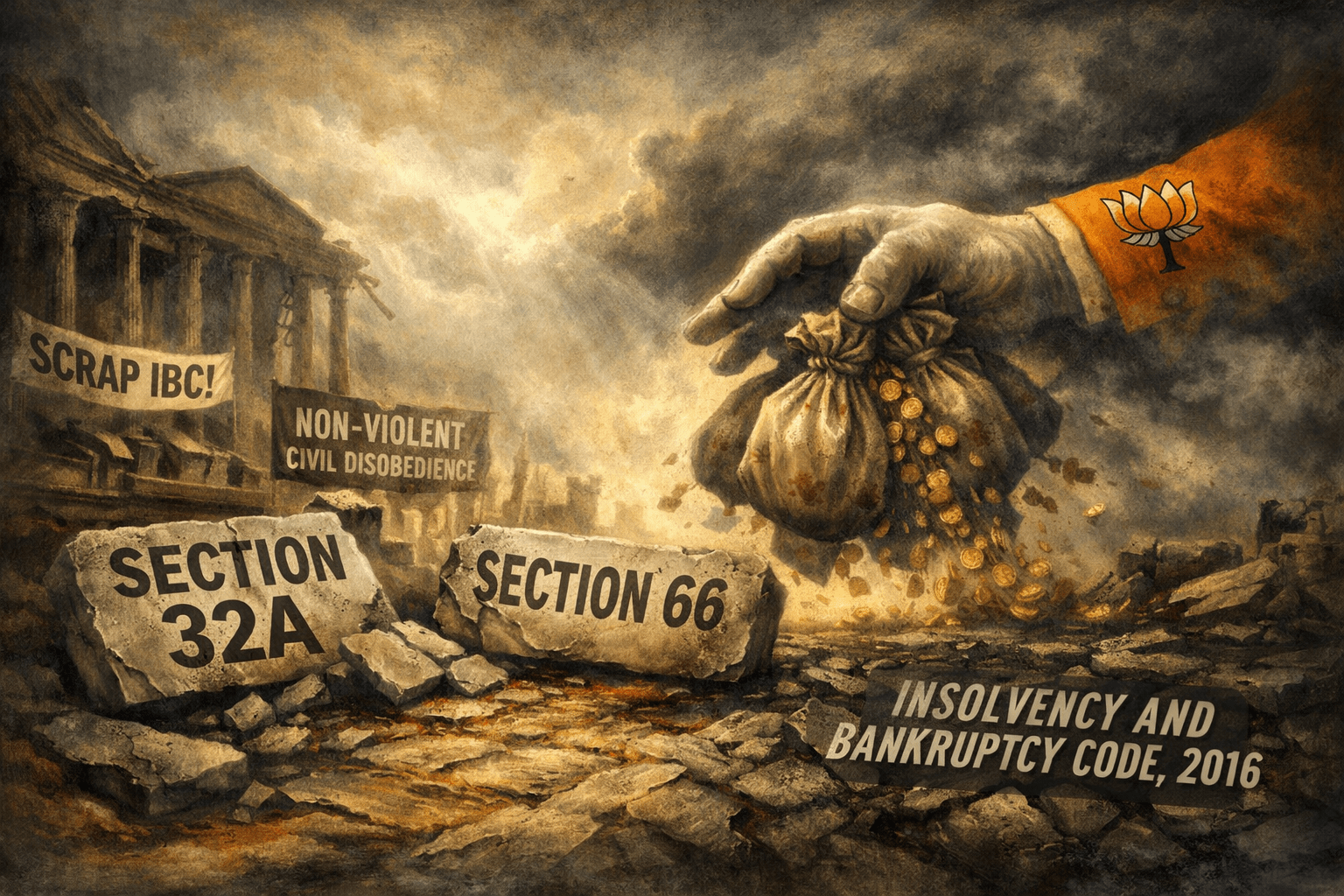

Scrap IBC Now: How Section 32A Buried Section 66 | The DHFL Case (Video)

In the DHFL insolvency — India’s first major NBFC case under the IBC — over 2.5 lakh retail depositors, including pensioners and widows, suffered heavy haircuts of 54–77% on their life savings. Yet the company emerged spotless in Piramal’s hands, fully discharged from a ₹5,050 crore PMLA case in February 2026 under Section 32A of the IBC. Inserted retrospectively via ordinance on 28 December 2019 — just 25 days after DHFL entered CIRP — this “clean slate” provision granted the new owner complete immunity from past offences, even as ₹45,000 crore in alleged fraud recoveries were valued at one rupee. Like Valmiki’s Ramayana, which existed before Rama’s birth and reconfigured reality itself, Section 32A rewrote corporate accountability after the fact (POST-FACTO), turning a law meant to protect creditors into a sophisticated mechanism that socialised losses and privatised gains for cronies like Piramal. The DHFL case stands as a stark example of how retrospective legislation can erase liability while ordinary citizens bear the burden.

Who Owns the Crisis? Indian Banking from Nationalization to Crony Regime

Posted on 1st April, 2026 (GMT 07:50 hrs) ABSTRACT This article traces the historical transformation of Indian banking from postcolonial state-led social banking to the contemporary regime of what it terms “resolution capitalism,” foregrounding the shifting configurations of power, distribution, and knowledge. Beginning with the pre-1969 era of private concentration and systemic fragility, it examinesContinue reading “Who Owns the Crisis? Indian Banking from Nationalization to Crony Regime”

Pressing Repeat: A Tragi-Comedy of DHFL Ruin, Viraha, and Satyagraha through Dilemma

In this darkly comic, self-reflexive monologue, a financially devastated DHFL victim—robbed of her life savings and hounded by a 100-crore SLAPP suit under an undeclared emergency—chronicles her solitary existence through obsessive loops of Rabindrasangeet. Trapped between paralyzing fear and compulsive repetition, she navigates aesthetic intimate separation anxiety (biraha), confronts the absence of any divine or human companion, and mercilessly dissects the selective “divine intervention” granted to the powerful while she receives only silence. Weaving Tagore’s melodies, Sudhindranath Dutta’s merciless “Ostrich,” Socrates’ Euthyphro Dilemma, Nietzsche’s amor fati, and Gandhi’s faith in truth, she transforms personal malady into a weapon of creative resistance. Refusing fatalism or piety, she reclaims the pharmakon of crisis, turning her suffering into non-violent digital satyagraha against the state-corporate apparatus. The result is a haunting, non-conclusive testament: a lone whistleblower who, though penniless and abandoned, continues to press “send” — pressing repeat no longer as surrender, but as quiet, unrelenting war.

A DHFL Victim’s Anonymous Letter — and the YouTube “Dislike” Campaign

This post presents an anonymous testimony from a DHFL depositor, documenting the lived human cost of India’s crony-capitalist financial regime. Through a raw account of loss, dispossession, and psychological distress following the DHFL collapse and subsequent resolution process, the letter foregrounds how institutional decisions, regulatory opacity, and political–corporate entanglements translate into everyday suffering for ordinary citizens. At the same time, it traces a shift from despair to resistance, as the victim transforms personal trauma into acts of digital dissent and collective voice. By reproducing the testimony in both transliterated Hindi and English, this piece seeks not only to archive a voice often erased in financial discourse but also to situate it within broader critiques of the “money-signifier” as a structuring force that shapes visibility, accountability, and justice in contemporary India.

Opaque by Design: The DHFL “Resolution” and Institutional Evasion — An Open Letter to the Reserve Bank of India (RBI)

The DHFL insolvency resolution under the Insolvency and Bankruptcy Code (IBC), 2016, stands as a stark exemplar of systemic opacity, regulatory evasion, and alleged crony favoritism in India’s financial ecosystem. Initiated by the Reserve Bank of India (RBI) in November 2019 through the supersession of the DHFL Board and referral to the National Company Law Tribunal (NCLT), the Corporate Insolvency Resolution Process (CIRP) culminated in the approval of Ajay Piramal’s resolution plan by the Committee of Creditors (CoC), the NCLT (June 2021), and ultimately the Supreme Court (April 1, 2025), which upheld the plan—including the appropriation of avoidance recoveries by the successful resolution applicant—while reaffirming the primacy of the CoC’s “commercial wisdom.” The case has drawn sustained scrutiny from approximately 2.5 lakh retail fixed-deposit and NCD holders, who suffered severe haircuts (recovering around 23% of admitted claims), amid allegations of undervaluation, procedural irregularities, premature occupation by the acquirer, and the dilution of fraud-avoidance mechanisms under Sections 32A and 66 of the IBC. Persistent Right to Information (RTI) applications—filed notably by activists associated with “Once in a Blue Moon Academia”—seeking itemized disclosure of the RBI-appointed CoC’s total expenditures (including professional fees, litigation costs, and deductions from the resolution pool) have been met with uniform institutional denial, with the RBI repeatedly claiming it “has no information” and bears no responsibility to maintain or interpret such records, while the Insolvency and Bankruptcy Board of India (IBBI) and the Comptroller and Auditor General (CAG) have similarly deflected or transferred queries. This refusal to disclose even basic expenditure details—despite the RBI’s direct role in constituting the CoC—fuels concerns about a deliberate “will to hide,” potentially masking inflated costs borne by depositors, quid pro quo arrangements linked to political financing, and preferential treatment for well-connected acquirers. Critics increasingly frame the DHFL case as a “test case” for the IBC regime, wherein small savers became unwitting “guinea pigs” in a system dominated by institutional creditors, marginalizing retail stakeholders and entrenching judicial deference to CoC decisions—even in the face of documented NCLAT findings of irregularities. This analysis argues that the DHFL resolution reveals deeper structural flaws in India’s insolvency framework: the transformation of statutory immunity into structural impunity, the erosion of transparency obligations under the RTI Act, and the prioritization of private gain over public accountability. Absent independent investigation and full disclosure, the episode risks eroding trust in regulatory institutions and reinforcing perceptions of oligarchic capture under the guise of financial reform, making urgent rectification of the persistent opacity surrounding CoC expenditures essential to restoring legitimacy to the IBC process and securing justice for affected depositors.

Expose IBC’s Dirty Secret, Resist the Structural Impunity for Cronies!

This dossier argues that the Insolvency and Bankruptcy Code, 2016 has evolved from a reform tool into a system of impunity, exemplified by the Dewan Housing Finance Corporation Ltd collapse, where depositors suffered massive losses while Section 32A IBC erased corporate liability for the “new owner” Mr. Ajay Piramal; highlighting repeated amendments and creditor dominance, it calls for repeal—especially of Section 32A in relation to its contradictory relationship to Section 66—and urges non-violent resistance inspired by Gandhiji to restore accountability.

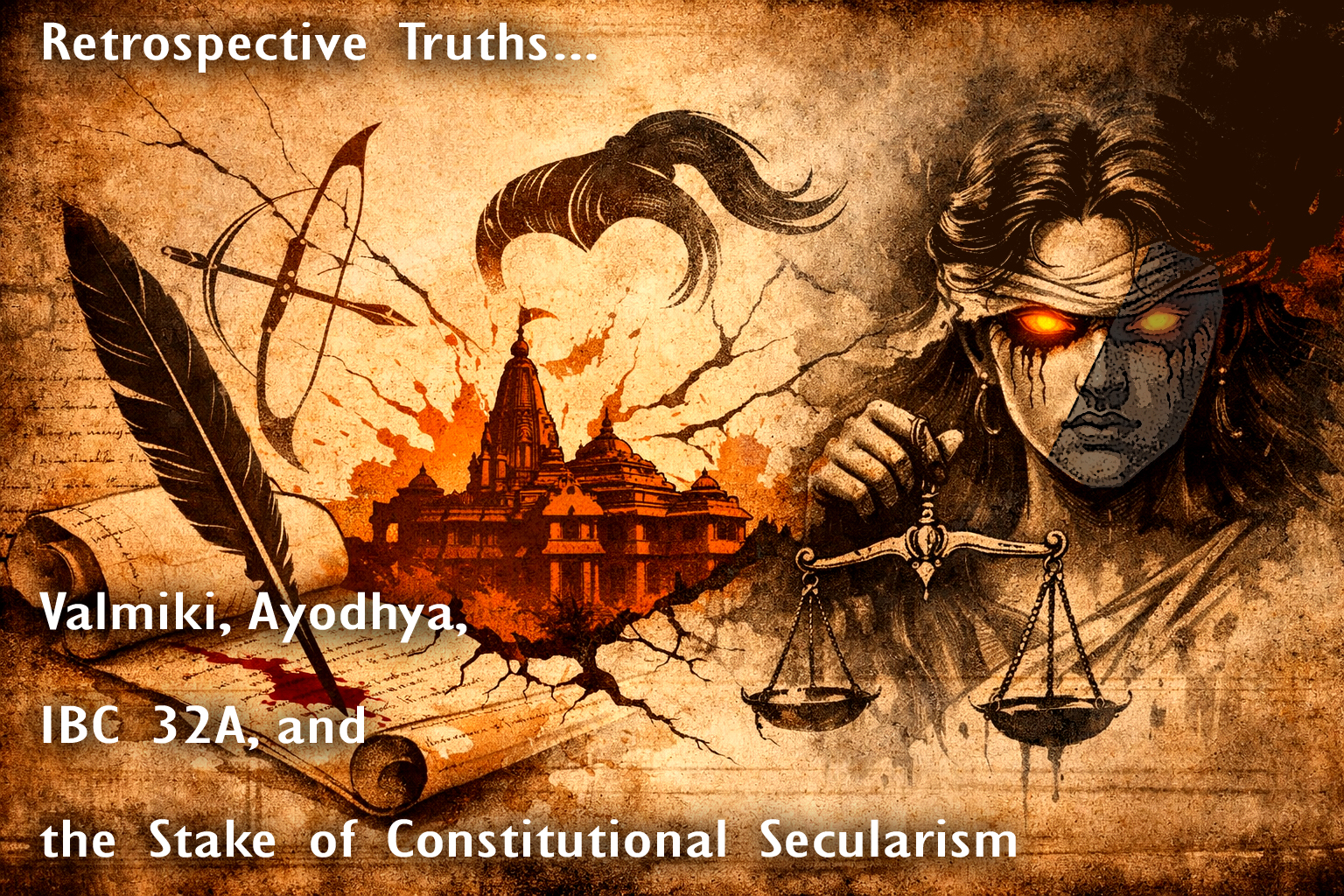

Retrospective Truths: Valmiki, Ayodhya, IBC 32A, and the Stake of Constitutional Secularism

This short article explores a striking parallel between poetic creation and state-sanctioned reality-making in contemporary India. Drawing from Rabindranath Tagore’s poetic dialogue with Narada in the context of Valmiki’s Ramayana—where the poet’s imaginative mind-realm is declared Rama’s truer birthplace than historical Ayodhya—the discussion extends to two landmark institutional acts: the Supreme Court’s 2019 Ayodhya verdict (with Justice D.Y. Chandrachud’s later confession of seeking divine guidance) and Section 32A of the Insolvency and Bankruptcy Code (IBC), which retrospectively absolves corporate debtors of pre-insolvency offences upon plan approval, as vividly illustrated in the DHFL-Piramal takeover. Both instances represent exercises in retrospective ontological surgery: the poet erases or reconfigures the past through fiction for ecstatic delight (jouissance), while the judiciary and legislature do so through unsigned judgments infused with faith-based inspiration and statutory “clean-slate” mechanisms that shield economic continuity at the expense of accountability. The article argues that such sovereign rewritings—whether sacralising faith in a title suit or engineering corporate rebirth—breach the thick wall of separation between powers, subordinate evidence-based adjudication to revelation or expediency, and inflict profound injury on constitutional secularism. By collapsing the distinction between objective historical/legal truth and creatively decreed higher truth, these developments risk transforming the secular Republic into a palimpsest open to majoritarian or crony capture, where Article 51A(h)’s mandate of scientific temper yields to engineered absolution and divine endorsement. Ultimately, while the poet may harmlessly invent birthplaces, when the State borrows that crown, the stake is nothing less than the integrity of constitutional secularism itself.

The Archaeology of Architecture in the Piramal Archipelago

This article examines the ecological contradictions embedded in contemporary corporate development through a critical analysis of four interconnected cases linked to the activities of the Piramal Group. Situated within the broader environmental context of Mumbai—one of the world’s most climate-vulnerable coastal megacities—the study explores how industrial production, urban real-estate expansion, and superrich architectural consumption intersect with fragile ecosystems and emerging climate risks. The first case investigates allegations of groundwater contamination linked to pharmaceutical manufacturing in Digwal village in Telangana, where proceedings before the National Green Tribunal raised concerns about impacts on aquifers and agricultural landscapes. The second examines controversy surrounding a chemical manufacturing facility in Dahej in Gujarat, where the Gujarat Pollution Control Board ordered a plant shutdown after allegations that hazardous industrial waste had been discharged into a canal connected to the Narmada River system. The analysis then turns to Mumbai’s coastal urban landscape, where luxury developments by Piramal Realty illustrate the commodification of waterfront environments marketed through narratives of sustainability and “biophilic living.” Finally, the study examines the sea-facing residence Gulita as a symbolic expression of wealth concentration along a climate-exposed coastline. Drawing on environmental reports, regulatory proceedings, and urban climate research, the article situates these cases within a broader framework of coastal capitalism and urban ecological transformation, arguing that corporate sustainability narratives often coexist with environmental risks displaced onto rural landscapes, industrial waterways, and vulnerable urban coastlines.