Posted on 25th February, 2026 (GMT 05:39 hrs)

ABSTRACT

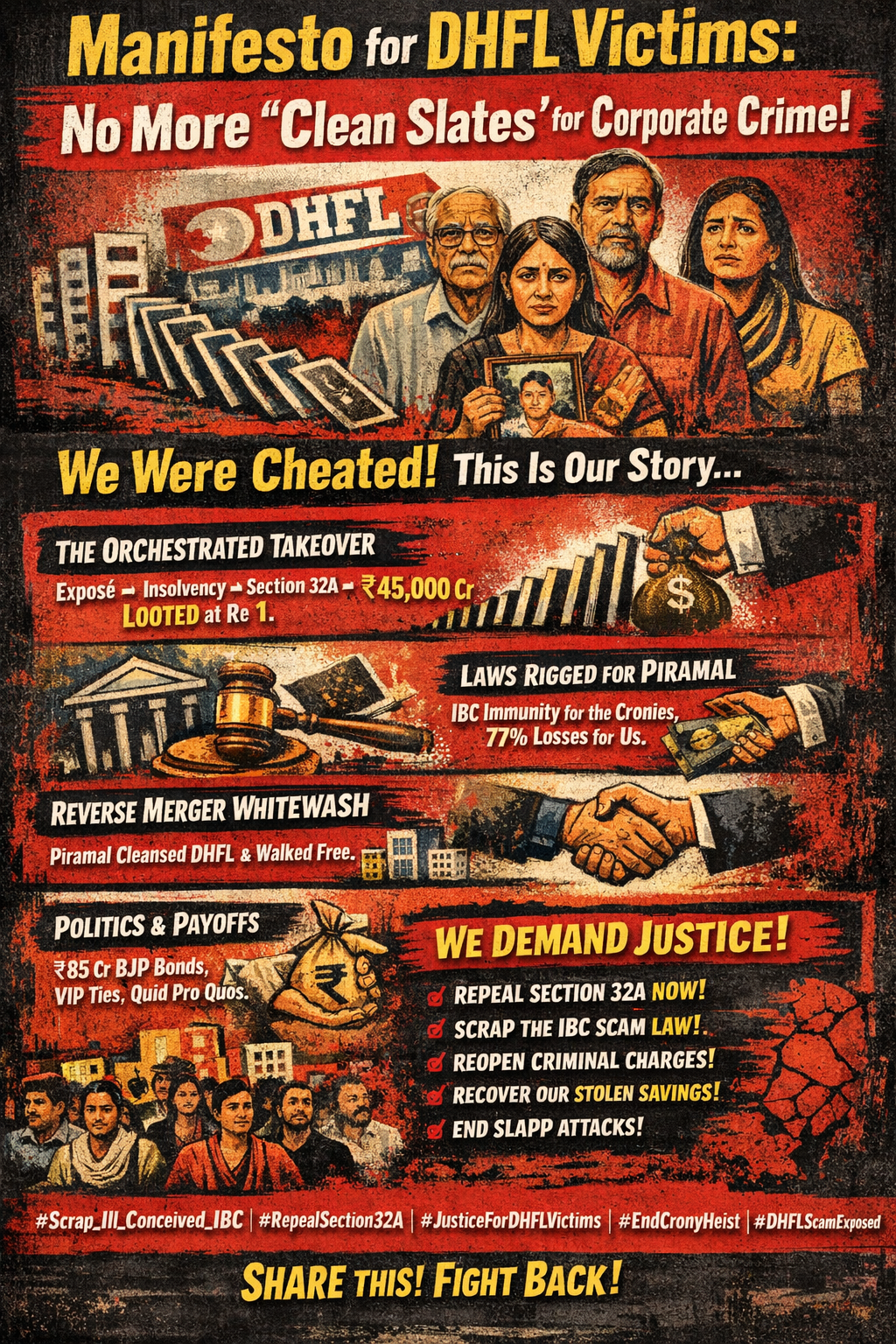

This pamphlet is a fact-based cry from over 2.5 lakh DHFL depositors who lost life savings in massive 54–77% haircuts. It chronicles how India’s first AAA-rated NBFC — a sound ₹91,000+ crore housing finance company — was deliberately dismantled under the IBC: starting with Ajay Piramal’s “shock” warning (28 Jan 2019) followed by the Cobrapost exposé (29 Jan 2019), RBI supersession (20 Nov 2019), CIRP admission (3 Dec 2019), mid-process insertion of Section 32A immunity (28 Dec 2019), ignored full-repayment proposals, a Re 1 giveaway of ₹45,000 crore Section 66 recoveries, judicial overrides culminating in Supreme Court approval (1 Apr 2025), reverse mergers to sanitize legacy, and PMLA discharge of the corporate debtor (2 Feb 2026) under Section 32A — while Piramal Finance now thrives (AUM ₹96,690 crore up 23% YoY, PAT up 162%). Highlighting statutory contradictions, CoC bias allegations, and a documented political-corporate nexus, it demands repeal of Section 32A, scrapping the IBC, restitution, and an end to SLAPP suits — framing the DHFL case as engineered crony sanitisation, not genuine resolution.

LEGAL DISCLAIMER: This manifesto is compiled entirely from publicly available facts, official court judgments, regulatory filings, government notifications, Election Commission data, and credible media reports. It presents a chronological sequence of verifiable events, statutory provisions, and judicial outcomes without making unsubstantiated personal allegations of criminality, secret plots, or defamation against any individual or entity. All statements are either direct quotations, accurate summaries of public records, or fair comment on matters of significant public interest affecting lakhs of depositors. Readers are encouraged to independently verify every detail through official sources. This is not a conspiracy theory but an exercise of free speech under Article 19(1)(a) of the Indian Constitution to highlight documented patterns, contradictions in law, and outcomes in the DHFL resolution process for awareness and advocacy.

In Continuation With

We, the 2.5 lakh+ betrayed depositors, retirees, widows, pensioners and middle-class families — this is our story, connected dot by dot, correlation by correlation.

DHFL was not a Ponzi scheme, or a chit fund. It was India’s first AAA-rated NBFC ever pushed into the ill-conceived, incoherent IBC — a sound housing finance company with over ₹91,000 crore in assets, serving millions. Yet it was deliberately taken apart, scrubbed clean of criminal liability for the “forthcoming” “successful” bidder, and handed over at a massive discount. What happened to us was unprecedented — and the sequence is too precise to be coincidence.

It started long before the insolvency began.

A. On 28 January 2019, Ajay Piramal stood in a public forum and said: “Be prepared for one or two major shocks in the NBFC sector.”

B. The very next day, 29 January 2019, Cobrapost published its explosive sting: “Anatomy of India’s Biggest Financial Scam,” accusing DHFL promoters of siphoning over ₹31,000 crore through shell companies, dubious loans, and alleged political donations (including to the BJP) and even terror-funding links.

The exposé triggered panic, downgrades, and scrutiny that never stopped. The man who “predicted” the shock became the one who walked away with the sanitized company.

C. Fast-forward to late 2019. On 20 November 2019, the RBI superseded DHFL’s board amid serious fraud allegations and governance concerns.

D. Just 13 days later, on 3 December 2019, the NCLT admitted DHFL into Corporate Insolvency Resolution Process (CIRP) — making it the first major financial services provider to enter insolvency under the newly notified IBC framework for Financial Service Providers (FSPs). Remarkably, only 25 days after CIRP commencement, on 28 December 2019, the government promulgated the Insolvency and Bankruptcy Code (Amendment) Ordinance, 2019, inserting Section 32A into the IBC with immediate effect. This new provision introduced the “clean slate” immunity, protecting the corporate debtor (and its new management) from prosecution or liability for offences committed before the CIRP commencement, provided the approved resolution plan results in a genuine change in management or control to unrelated persons.

E. The Amendment Act later received presidential assent on 13 March 2020, but Parliament ensured the “clean-slate” immunity under Section 32A applied retrospectively from the ordinance date itself — i.e., deemed to have come into force from 28 December 2019 — thereby covering ongoing resolution processes like DHFL’s that had begun shortly before the Ordinance.

The CIRP had already started. Claims were still being invited. The Committee of Creditors was forming. And then — mid-process — Parliament drops a provision that wipes out all corporate criminal liability for pre-CIRP offences once a new, unrelated management (Piramal!) takes over. This was not reform. This was calendar-engineered immunity, timed to activate exactly when DHFL needed it most for a politically acceptable buyer.

The rest followed like clockwork. Competing bidder Oaktree Capital repeatedly accused the CoC of bias, procedural irregularities, lack of transparency, and undue preference for Piramal’s plan — even threatening legal action. The Wadhawan brothers made repeated full-repayment proposals during CIRP — offers to repay every creditor in full through restructuring or infusions. These were summarily ignored, never seriously evaluated, and public depositors (holding nearly 65% CoC voting share) were never even shown the full details. Instead, the plan assigned a notional value of just Re 1 to avoidance transactions (fraudulent and wrongful trading recoveries under Section 66) estimated at ₹45,000 crore in forensic audits. That massive upside went straight to Piramal as the Successful Resolution Applicant — while we, the retail depositors and NCD holders, absorbed 54–77% haircuts on our life savings.

F. In an order on 19 May 2021, the NCLT had expressed concerns over the exclusion of ex-promoters’ settlement proposals, and asked the CoC to reconsider their repayment plan.

G. However, the CoC-Piramal group rushed to the NCLAT and got this order stayed within a few days on 25 May 2021.

H. On 7 June 2021, the NCLT approved the Piramal resolution plan, incorporating the Re 1 valuation for Section 66 recoveries as part of the Committee of Creditors’ commercial wisdom.

I. On 27 January 2022, the NCLAT went further by setting aside the portion of the plan that allowed Piramal to appropriate the Section 66 recoveries, describing the arrangement as discriminatory, irregular and illegal, and directing the CoC to reconsider so that such benefits could flow to creditors.

J. However, the Supreme Court, in its judgment headed by BJP’s favoured Justice Bela Trivedi (reports say so!) dated 1 April 2025, upheld the entire plan — including the Re 1 valuation and overall structure — as a valid exercise of commercial wisdom, effectively overturning the NCLAT’s intervention.

K. To further amplify the “clean slate” effect and legally distance the new entity from DHFL’s tainted legacy, Piramal executed a reverse merger: Piramal Capital & Housing Finance Limited (PCHFL) merged into DHFL effective 30 September 2021 (as stipulated in the approved resolution plan), with DHFL as the surviving entity, which was then immediately renamed Piramal Capital & Housing Finance Limited (later rebranded as Piramal Finance).

This corporate technique allowed the combined entity to inherit DHFL’s valuable assets, branch network, and loan book while creating a fresh legal identity that helped disown or minimize continuity with past liabilities. In 2025, another reverse merger absorbed the listed parent, Piramal Enterprises Limited, into Piramal Finance, further streamlining the structure and embedding the gains.

L. On 2 February 2026, the Mumbai Special PMLA Court discharged Piramal Finance (formerly DHFL) from the entire ₹5,050 crore money-laundering case, explicitly citing Section 32A as the overriding immunity provision. The corporate debtor walked free of all liability, while the individuals (including the Wadhawan brothers) remain accused and prosecutable.

| Date | Event | Key Details / Source Context |

|---|---|---|

| 28 January 2019 | Ajay Piramal’s public statement | “Be prepared for one or two major shocks in the NBFC sector” (reported in public forums and activist compilations; widely cited in DHFL-related discussions). |

| 29 January 2019 | Cobrapost exposé published | “Anatomy of India’s Biggest Financial Scam” — accused DHFL promoters of siphoning over ₹31,000 crore via shell companies, dubious loans, alleged political donations (including to BJP), and terror-funding links. Triggered market panic and scrutiny. |

| 20 November 2019 | RBI supersedes DHFL board | RBI invokes powers under RBI Act due to governance concerns and defaults; appoints R. Subramaniakumar as Administrator. |

| 3 December 2019 | NCLT admits DHFL for CIRP | First major financial services provider under FSP Rules; insolvency commencement date set as 3 Dec 2019; moratorium imposed. |

| 28 December 2019 | IBC Amendment Ordinance promulgated, inserting Section 32A | Immediate effect; provides “clean slate” immunity for corporate debtor from pre-CIRP offences post-resolution plan approval and management change. (Just 25 days after CIRP admission.) |

| 13 March 2020 | IBC (Amendment) Act, 2020 receives presidential assent | Replaces the December 2019 Ordinance; formalizes Section 32A into law with retrospective effect (deemed to come into force from 28 December 2019), ensuring “clean slate” immunity applied to ongoing CIRPs like DHFL’s. |

| 19 May 2021 | The NCLT ordered the CoC to reconsider DHFL’s erstwhile promoter Wadhawan’s offer of 100% repayment within 10 days. | [IA 2431 of 2020 in CP (IB) 4258/MB/C-II/2019 Under Section 60 (5), 227 (2), 239 of the Insolvency and Bankruptcy Code, 2016] points 16-19 and 84-89. |

| 25 May 2021 | NCLAT set aside NCLT’s order after the Union Bank of India and Ajay Piramal approached the NCLAT with an urgent petition. | The CoC did not even bother to answer the NCLT. |

| 7 June 2021 | NCLT approves Piramal resolution plan | Incorporates Re 1 valuation for Section 66 recoveries as CoC’s commercial wisdom. |

| 27 January 2022 | NCLAT sets aside part of plan re: Section 66 recoveries | Described arrangement as discriminatory/irregular/illegal; directed CoC reconsideration so benefits flow to creditors. |

| 30 September 2021 | Reverse merger effective (PCHFL into DHFL) | DHFL survives as entity, renamed Piramal Capital & Housing Finance Ltd (later Piramal Finance); amplifies clean slate by creating fresh legal identity to distance from legacy liabilities. |

| 1 April 2025 | Supreme Court upholds entire plan | Judgment (authored by Justice Bela M. Trivedi) validates Re 1 valuation and structure as commercial wisdom; overturns NCLAT on key aspects. |

| 2 February 2026 | Mumbai Special PMLA Court discharges Piramal Finance (ex-DHFL) | From ₹5,050 crore money-laundering case; explicitly cites Section 32A as overriding immunity; corporate debtor free, individuals (Wadhawans) remain prosecutable. |

This outcome perfectly exposed the fatal internal contradiction at the heart of the IBC: Section 66 explicitly states that recoveries from fraudulent or wrongful trading must benefit all creditors and be directed “to the assets of the corporate debtor” for their general benefit. Yet Section 32A’s clean-slate immunity was used to override this statutory mandate, allowing the new owner to pocket the entire upside.

The Code itself contains no provision that automatically funnels Section 66 recoveries to the Successful Resolution Applicant — the loophole lies in the fact that allocation is left entirely “open to interpretation” through the approved resolution plan, rubber-stamped under the cloak of the CoC’s “commercial wisdom” and Section 31. The NCLAT had seen through this on 27 January 2022, calling the Re 1 giveaway discriminatory and illegal and ordering the benefits to go back to creditors. But the Supreme Court in its 1 April 2025 judgment ultimately sided with Piramal, sanctifying the token Re 1 valuation and handing the entire speculative ₹45,000 crore windfall to the acquirer.

Today, Piramal Finance proudly reports an AUM of ₹96,690 crore (up 23% YoY), 9M FY26 PAT of ₹1,004 crore (up 162% YoY), and a fresh CRISIL AA+ rating — all achieved on the foundation of our massive 54–77% haircuts and a ₹45,000 crore windfall from avoidance recoveries valued at just Re 1. Public losses were socialized; private gains were fully privatized.

The nexus is impossible to ignore. Piramal Group entities donated ₹85–98 crore to the BJP via electoral bonds (including tranches from loss-making companies). Ajay Piramal is samdhi to Mukesh Ambani. There was the 2014 Flashnet deal — buying a near-dormant company linked to Piyush Goyal at a 1,000% premium. ₹25 crore donated to PM CARES. Repeated closed-door meetings with the Prime Minister. The pattern screams quid pro quo: political funding and proximity in exchange for a distressed AAA-rated asset delivered pristine, with every criminal overhang erased.

When we speak out democratically, Ajay Piramal’s lawyers at DSK Legal respond not with dialogue but with SLAPP (defamation) suits — targeting victims, activists, and OBMA members since 2023. Litigation becomes intimidation. Courtrooms become instruments of exhaustion. Dissent is reframed as “defamation.”

And when we turned to constitutional methods — filing RTIs to the Supreme Court of India, Reserve Bank of India, Insolvency and Bankruptcy Board of India, Ministry of Corporate Affairs, Department of Financial Services, and the Comptroller and Auditor General of India — asking simple, democratic questions:

Where are the Committee of Creditors (CoC) audits?

Where are the voting records?

Where are the minutes of meetings?

Where are the expenditure details?

Where is the documentary trail of accountability?

The response was denial, evasion, or silence.

Thus the pattern stands exposed:

When we speak — they sue.

When we ask — they refuse. Auditors do not know their own audits!

This is not merely a legal battle. It is a struggle over whether public institutions will answer citizens — or shield concentrated power behind procedural opacity.

This was never spontaneous market correction. It was a meticulously sequenced handover: Expose first → scandal escalates → insolvency triggered → immunity legislated mid-stream → competing bids sidelined → full-repayment paths blocked → ₹45,000 crore upside gifted at Re 1 → toxic asset sanitized and gifted to the politically favoured acquirer.

We, the victims, demand:

- Immediate and full repeal of Section 32A — nullify its retrospective effect.

- Scrap the entire ill-conceived IBC — it has become the greatest tool of middle-class dispossession since Independence.

- Reopen criminal accountability for the corporate debtor on pre-CIRP offences.

- Full transparency: forensic review of ignored full-repayment proposals, CoC bias, and the Re 1 giveaway.

- Restitution for depositors — claw back the windfall and compensate those who lost life savings.

- End SLAPP intimidation — protect free speech for victims exposing public-interest wrongs.

We will not remain silent. We see every dot. We connect every correlation. DHFL was the test case. We were the collateral. But our resistance will not stop.

#Scrap_Ill_Conceived_IBC, #RepealSection32A, #JusticeForDHFLVictims, #EndCronyHeist, #DHFLScamExposed, #Scrap_Ill_Conceved_IBC, #IBCSection32A, #InsolvencyAndBankruptcyCode, #IBCReformNow, #DHFLScam, #DHFLPiramalTakeover, #JusticeForDHFLVictims, #JusticeForDepositors, #Seize_Cronies_Fairplay_for_DHFL_Victims, #alleged_dawood_mirchi_rkw_dhfl_bjp_collusion, #CronyCapitalismExposed, #CorporateCaptureIndia, #PublicMoneyPrivateProfits, #FinancialGovernanceCrisis, #TransparentBankruptcy, #InvestorProtectionIndia, #DepositorRightsIndia, #RegulatoryFailureIndia, #AccountabilityInIBC, #PolicyCaptureIndia, #StopCorporateLoot, #ReclaimPublicFunds, #FinancialSystemsReform, #PeopleOverProfit, #DigitalActivismIndia, #JusticeMovementIndia, #ExposeTheSystem, #PublicInterestEconomics, #BankruptcyLawReform, #OBMA, Occupy_Internet_to_Occupy_Cronies,

Share this manifesto. Print it. Post it. Flood the internet. The clean slate was engineered for them, the top 2% in utter disregard for the other 98%. Our fight is for justice — relentless, united, and unafraid.

See Also:

Section 32A vs Section 66 of the Ill-Conceived IBC

IBC Section 32A Explained | DHFL Piramal Takeover Analysis | Insolvency Code Critique | Crony Capitalism in India | Depositor Rights & Bankruptcy Law Reform | Financial Governance Crisis | Corporate Accountability Campaign|

They erased liability.

They erased accountability.

They will NOT erase us.

Scrap the law that shields cronies.

Return the people’s money.

Justice for DHFL victims — now.

#Scrap_Ill_Conceved_IBC, #IBCSection32A, #InsolvencyAndBankruptcyCode, #IBCReformNow, #DHFLScam, #DHFLPiramalTakeover, #JusticeForDHFLVictims, #JusticeForDepositors, #Seize_Cronies_Fairplay_for_DHFL_Victims, #Alleged_Dawood_Mirchi_Rkw_Dhfl_Bjp_Collusion, #CronyCapitalismExposed, #CorporateCaptureIndia, #PublicMoneyPrivateProfits, #FinancialGovernanceCrisis, #TransparentBankruptcy, #InvestorProtectionIndia, #DepositorRightsIndia, #RegulatoryFailureIndia, #AccountabilityInIBC, #PolicyCaptureIndia, #StopCorporateLoot, #ReclaimPublicFunds, #FinancialSystemsReform, #PeopleOverProfit, #DigitalActivismIndia, #JusticeMovementIndia, #ExposeTheSystem, #PublicInterestEconomics, #BankruptcyLawReform,

LikeLiked by 5 people