Posted on 7th February, 2026 (GMT 02:58 hrs)

ABSTRACT

This article examines the structural relationship between global banking institutions and large emerging-market conglomerates through a dual case analysis of Standard Chartered Bank and the Piramal Group between 2012 and 2026. Drawing on regulatory enforcement actions, insolvency proceedings, capital-market transactions, and litigation outcomes, the paper argues that recurrent compliance failures in global banking and aggressive corporate restructuring in emerging markets are not independent phenomena but mutually reinforcing processes. The analysis demonstrates how persistent anti-money laundering lapses, sanctions violations, and settlement-driven regulation in global banks coexist with—and indirectly enable—high-leverage expansion, legal insulation, and accountability dilution within domestic conglomerates. By situating the Standard Chartered–Piramal relationship within the broader context of regulatory arbitrage, insolvency-enabled legal finality, and transnational risk transfer, the article shows how contemporary financial law increasingly prioritizes resolution, liquidity, and market confidence over distributive justice and creditor accountability. The findings contribute to critical debates on global financial governance by revealing how legality itself has become a primary instrument for organizing, rather than constraining, financial risk.

1. Global Finance, Legal Finality, and the Normalization of Risk

The global financial landscape in the mid-2020s is marked by a convergence of geopolitical instability, deepening financialization, and increasingly sophisticated forms of economic wrongdoing. Rather than manifesting as episodic crises, these dynamics have coalesced into what is often described as a polycrisis—a condition in which systemic risk is continuously reproduced through legal, institutional, and market mechanisms. At the center of this configuration stand systemically important financial institutions (SIFIs) and their evolving relationships with large, diversified corporate groups operating in emerging markets.

Global banks continue to serve as the principal arteries of cross-border capital flows, underwriting sovereign debt, structuring corporate finance, and intermediating investment into jurisdictions characterized by regulatory complexity and uneven enforcement. Yet the same institutions have repeatedly been implicated in large-scale failures of anti-money laundering controls, sanctions compliance, market integrity, and disclosure obligations. Enforcement responses, particularly since the global financial crisis, have increasingly relied on fines, deferred prosecution agreements, and negotiated settlements—mechanisms that preserve institutional continuity while normalizing compliance failure as a manageable cost of business.

Parallel to this evolution in global banking has been the rise of powerful emerging-market conglomerates whose growth strategies are anchored in leverage, acquisition-driven expansion, and legal restructuring. In India, the Piramal Group exemplifies this trajectory. Over the past two decades, the group has transformed from a manufacturing-oriented enterprise into a dominant presence in pharmaceuticals and financial services. This transformation, however, has unfolded alongside persistent regulatory scrutiny, insider-trading settlements, environmental penalties, and—most notably—the acquisition of Dewan Housing Finance Corporation Ltd (DHFL) through India’s Insolvency and Bankruptcy Code (IBC).

The DHFL resolution represents a watershed moment in India’s insolvency jurisprudence. By affirming the primacy of resolution finality and granting corporate immunity for pre-resolution offences, the Supreme Court’s interpretation of the IBC has effectively severed financial recovery from accountability. For acquiring entities, this legal architecture converts distressed assets, contested liabilities, and even fraudulent legacy transactions into legally cleansed instruments of future value. For creditors—particularly retail investors and deposit holders—the same architecture has resulted in irreversible loss and extinguished claims.

This article argues that the relationship between Standard Chartered Bank and the Piramal Group must be understood within this broader institutional landscape. Standard Chartered’s role as a lead financier, arranger, and market signaler for Piramal entities is not merely transactional. It reflects a deeper alignment between global banking practices shaped by settlement-driven regulation and domestic conglomerate strategies enabled by insolvency-based legal insulation. Together, these dynamics produce a system in which risk is not eliminated but redistributed—across jurisdictions, balance sheets, and social classes.

The central claim of this paper is that contemporary financial governance increasingly operates through legal closure rather than substantive accountability. Compliance failures are resolved, not corrected; insolvency finalizes disputes, not responsibility; and capital markets reward legal certainty even when underlying governance risks persist. By tracing the regulatory histories of Standard Chartered and the corporate evolution of the Piramal Group, and by examining the financial and legal ties between them, this article seeks to illuminate how global finance today organizes impunity through law itself.

The paper proceeds as follows. Section 2 examines Standard Chartered Bank’s regulatory and compliance history, highlighting recurring patterns of sanctions violations, AML failures, and market misconduct. Section 3 analyzes the Piramal Group’s corporate governance record, financial restructuring, and the legal consequences of the DHFL acquisition. Section 4 maps the financial, strategic, and philanthropic dimensions of the Standard Chartered–Piramal relationship, situating it within a framework of regulatory arbitrage and transnational risk transfer. The conclusion synthesizes these findings to reflect on the broader implications for financial law, creditor justice, and democratic accountability.

2. Standard Chartered Bank: A Recurrent Pattern of Regulatory Failure, Financial Crime Exposure, and High-Risk Capital Practices

Standard Chartered Bank (SCB) occupies a distinctive position in global finance: formally regulated within the United Kingdom’s prudential framework, yet structurally oriented toward emerging markets with historically weak enforcement regimes. This positioning has repeatedly exposed the bank to large-scale regulatory failures, particularly in the domains of anti–money laundering (AML), sanctions compliance, market integrity, and transparency toward investors. Rather than isolated lapses, these episodes reveal a persistent governance deficit embedded in the bank’s operational and risk-management architecture.

2.1 Systemic AML and Sanctions Violations

Standard Chartered has a documented history of systemic breaches of international sanctions and AML protocols spanning more than two decades. Between 2001 and 2014, the bank twice admitted to violating United States sanctions against Iran, Sudan, Syria, and Myanmar. Regulatory findings established that SCB engaged in deliberate transaction “cloaking,” stripping identifying information from payment messages in order to conceal the involvement of sanctioned Iranian entities. These practices were not episodic misconduct by rogue employees but reflected institution-wide process failures that persisted across jurisdictions and management cycles.

In 2012 and again in 2019, the bank paid combined penalties exceeding USD 1.7 billion to U.S. and UK regulators for sanctions breaches and systemic AML failures. Enforcement actions emphasized not merely technical non-compliance but a sustained inability—or unwillingness—to remediate known control deficiencies despite repeated regulatory warnings.

UK regulators subsequently reinforced this assessment. In April 2019, the Financial Conduct Authority (FCA) imposed a £102.2 million fine for “serious and sustained shortcomings” in AML controls. Regulatory findings included extreme lapses such as the opening of an account funded by £500,000 in physical cash delivered in a suitcase, underscoring the absence of basic due diligence and escalation safeguards. In December 2021, the Prudential Regulation Authority (PRA) levied an additional £46.55 million penalty for failures in regulatory reporting and lack of candour regarding liquidity errors occurring between 2018 and 2019.

Taken together, these sanctions suggest a recurring compliance pathology: risk identification is subordinated to revenue imperatives, while remediation is treated as a post-hoc regulatory cost rather than a core governance obligation.

2.2 Allegations of Terrorism Financing Exposure

More recent litigation has intensified scrutiny of Standard Chartered’s historic transaction flows. Court filings in June 2024 alleged that the bank processed over USD 100 billion in transactions between 2008 and 2013 involving entities linked to designated terrorist organisations, including Hezbollah, Hamas, and al-Qaeda. While the bank disputes these allegations, expert analyses submitted in court identified approximately USD 9.6 billion in foreign exchange transactions allegedly connected to designated terror-linked entities.

Even if ultimate judicial findings remain contested, the scale and duration of the alleged exposures point to structural weaknesses in correspondent banking oversight, customer risk classification, and sanctions screening during a period in which global counter-terror financing standards were already well established.

2.3 Exposure to Global Financial Crime Scandals

Standard Chartered has also been implicated in major international financial crime controversies beyond sanctions violations. In July 2025, the bank faced a USD 2.7 billion lawsuit relating to its alleged role in facilitating the movement and concealment of funds misappropriated from Malaysia’s sovereign wealth fund, 1MDB, between 2009 and 2013. The litigation alleges failures in transaction monitoring, beneficial ownership verification, and escalation of suspicious activity—failures strikingly consistent with patterns identified in earlier enforcement actions.

In December 2025, the bank reached a £1.5 billion civil settlement in the United Kingdom with institutional investors, resolving claims that it had inadequately disclosed historic financial crime risks and regulatory exposures. This settlement is significant not merely for its size, but because it reframes compliance failures as a form of investor deception, linking AML misconduct directly to capital market accountability.

2.4 Market Manipulation and Non-Traditional Risk Activities

Beyond AML and sanctions, Standard Chartered’s record includes repeated involvement in market integrity violations and high-risk industrial financing. In November 2023, South Africa’s Competition Commission fined the bank R42.7 million for manipulating the USD/ZAR exchange rate between 2007 and 2013. The bank admitted to coordinating bids and spot prices, reinforcing concerns about cultural tolerance for benchmark manipulation across global trading desks.

Historically, the bank’s risk appetite has also been shaped by its colonial-commercial origins. Founded in 1853 under royal charter, its predecessor institutions were deeply embedded in imperial trade networks dealing in cotton, indigo, tea, and opium-linked markets across Asia. While historical continuity should not be overstated, this legacy contextualizes a longstanding orientation toward extractive and commodity-driven capital flows in weakly regulated environments.

In the contemporary period, this orientation manifested in aggressive lending to volatile industrial sectors. Notably, Standard Chartered incurred substantial losses through exposure to the midstream diamond industry, ultimately announcing in 2016 its exit from the sector. As of 2017, the bank reportedly carried approximately USD 1.7 billion in unpaid diamond-related debt. Earlier, in 1994, its Asian investment banking arm was temporarily banned from underwriting IPOs in Hong Kong after illegally supporting post-issue share prices—an early signal of governance weaknesses in capital market conduct.

2.5 Synthesis: Governance Failure as Structural Condition

The cumulative record suggests that Standard Chartered’s regulatory violations are not anomalous deviations from an otherwise sound governance model. Rather, they point to a structural condition in which compliance is treated as negotiable, geographically uneven, and ultimately subordinate to growth in high-margin, high-risk markets. Penalties, settlements, and deferred prosecution agreements function less as deterrents than as recurring costs of doing business.

This pattern is analytically significant for examining the bank’s relationships with large conglomerates operating in regulatory gray zones. The persistence of AML failures, sanctions breaches, and disclosure deficiencies raises critical questions about counterparty due diligence, reputational risk transfer, and the normalization of legal risk within elite financial networks—questions that become especially salient when assessing Standard Chartered’s engagements with corporate groups such as the Piramal conglomerate.

Summary of Major Penalties

| Year | Authority | Fine/Settlement | Primary Violation |

|---|---|---|---|

| 2012 | US Regulators (DFS/DOJ) | $667 Million | Hiding Iranian transactions & sanctions breaches |

| 2019 | US & UK Authorities | $1.1 Billion | Systemic AML and sanctions failures |

| 2021 | PRA (UK) | £46.55 Million | Regulatory reporting and liquidity transparency |

| 2023 | Competition Comm. (SA) | R42.7 Million | USD/ZAR currency pair manipulation |

| 2025 | Civil Settlement (UK) | £1.5 Billion | Investor claims regarding financial crime disclosure |

3. The Piramal Group: Corporate Restructuring, Regulatory Tensions, Market Valuation, and Post-DHFL Legal Status

The Piramal Group, led by billionaire Ajay Piramal, has undergone rapid corporate transformation across pharmaceuticals and financial services, accompanied by repeated regulatory scrutiny and contested insolvency outcomes. This section evaluates the group through three interlinked dimensions: regulatory–legal exposure, distributional consequences of the DHFL resolution, and post-restructuring financial metrics, situating market valuation alongside governance risk.

3.1 Regulatory Scrutiny and Market Conduct

The group’s compliance history reveals recurring weaknesses in information governance, disclosure discipline, and internal controls relating to price-sensitive information.

Table 3.1: Key Regulatory and Legal Actions Involving the Piramal Group

| Year | Entity / Individual | Regulator / Court | Issue | Outcome |

|---|---|---|---|---|

| 2016 | Promoter Family (Piramal Group) | SEBI | Mishandling of Unpublished Price Sensitive Information (UPSI) during Abbott India divestment | Indicted by SEBI; partial relief granted later by SAT |

| 2021–24 | Piramal Capital & Housing Finance (MD & spouse) | SEBI | Insider trading involving trades in parent company shares | ₹43.55 crore settlement (no admission of guilt) |

| 2024 | Piramal Pharma Ltd | National Green Tribunal (NGT) | Non-disclosure of Digwal plant shutdown due to pollution violations | ₹8.32 crore environmental penalty |

| 2025 | DHFL (post-acquisition) | Supreme Court of India | Allocation of avoidance transaction recoveries | Resolution plan upheld; recoveries accrue to Piramal |

| 2026 | DHFL (corporate entity) | Special PMLA Court | Money-laundering prosecution | Corporate entity discharged under IBC immunity |

Analytical implication:

The regulatory record reflects not episodic misconduct but recurrent correction by enforcement agencies, often resolved through settlements rather than adjudication. This pattern mirrors a broader Indian trend where economic scale and systemic relevance coexist with attenuated punitive outcomes.

3.2 The DHFL Acquisition: Distributional Effects and Legal Finality

The ₹34,250 crore acquisition of DHFL under the Insolvency and Bankruptcy Code (IBC) stands as the most consequential—and contested—transaction in the group’s recent history.

Retail fixed-deposit holders reportedly recovered approximately 23% of their claims, while secured and institutional creditors achieved materially higher recoveries. Central to the controversy was the treatment of nearly ₹45,000 crore in suspected fraudulent and avoidance transactions, valued at a token ₹1 in the resolution plan.

The Supreme Court’s April 2025 judgment conclusively affirmed that:

- Avoidance-related recoveries belong to the resolution applicant.

- Creditors possess no residual claim once the plan is approved.

- Regulatory statutes (RBI Act, NHB Act) override equitable redistribution arguments.

This ruling has now closed most investor appeals, consolidating legal finality while intensifying normative critiques of IBC-enabled wealth transfer.

3.3 Post-Resolution Financial Metrics and Market Valuation

Following aggressive restructuring and consolidation, the Piramal Group has sought to reposition itself as a diversified, publicly disciplined conglomerate. However, post-listing financial indicators point to elevated leverage and operating stress, particularly within financial services.

Table 3.2: Selected Financial Metrics and Market Indicators (FY25–FY26)

| Entity | Indicator | Latest Reported Value | Interpretation |

|---|---|---|---|

| Piramal Finance Ltd | Market Capitalisation (listing phase) | ~₹30,000 crore | Strong debut valuation despite high leverage |

| Piramal Finance Ltd | Net Debt-to-Equity Ratio | ~7.13 | Indicates aggressive balance-sheet leverage |

| Piramal Finance Ltd | Gross NPA (GNPA) | ~2.8% | Moderated but flagged as “key monitorable” |

| Piramal Pharma Ltd | Q2 FY26 Net Profit/Loss | –₹99.2 crore | Continued operating losses |

| Piramal Pharma Ltd | Q2 FY26 Revenue Growth | –8.8% YoY | Demand and margin pressures |

| Piramal Pharma Ltd | EBITDA Change | –44% YoY | Sharp profitability compression |

| DHFL (resolved entity) | Retail FD recovery rate | ~23% | Severe distributional asymmetry |

Analytical implication:

The contrast between robust market capitalisation and fragile operating fundamentals suggests that valuation optimism is driven more by structural consolidation and legal closure than by balance-sheet resilience or governance reform.

3.4 Governance Strategy and Organisational Culture

Critics argue that the Piramal Group’s frequent mergers, demergers, and rebrandings function as a form of corporate risk partitioning, allowing legacy liabilities—financial, regulatory, and reputational—to be isolated within restructured entities. Parallel to this, employee-reported workplace issues—hierarchical “sir culture,” abrupt layoffs, and internal opacity—raise questions about internal accountability ecosystems that mirror external governance patterns.

Taken together, all the tables demonstrate a critical paradox:

legal finality and market confidence have advanced faster than accountability and financial robustness. This disjuncture provides the analytical hinge for examining how global banks—such as Standard Chartered—interface with Indian conglomerates operating within legally insulated, highly leveraged, and regulatorily corrected environments.

3.5. Regulatory Arbitrage, IBC-Enabled Impunity, and Transnational Risk Transfer

The interaction between global banks and large domestic conglomerates in emerging markets is best understood not as a series of bilateral transactions, but as a systemic architecture of risk circulation. In the case of Standard Chartered Bank and the Piramal Group, three interlocking mechanisms are analytically salient: regulatory arbitrage, IBC-enabled impunity, and transnational risk transfer. Together, they illuminate how legal compliance, financial stability, and accountability become unevenly distributed across jurisdictions and stakeholder classes.

4.6. Regulatory Arbitrage as Structural Strategy

Regulatory arbitrage refers to the strategic exploitation of differences in legal, supervisory, and enforcement regimes across jurisdictions. Standard Chartered’s historical pattern of sanctions breaches and AML failures demonstrates how globally active banks often operate in regulatory gradients, concentrating high-risk activities in jurisdictions where enforcement is slower, fragmented, or negotiable.

India’s financial regulatory environment—characterised by ex post settlements, limited criminal enforcement, and prolonged appellate processes—has increasingly functioned as a permissive node within this global gradient. For multinational banks, partnerships with well-connected domestic conglomerates provide:

- local regulatory insulation,

- reputational buffering through “national champion” narratives, and

- reduced enforcement asymmetry relative to Western jurisdictions.

The Piramal Group, operating across pharmaceuticals and financial services, fits this profile of a jurisdictionally embedded counterparty: large enough to be systemically relevant, diversified enough to absorb regulatory shocks, and legally sophisticated enough to convert compliance failures into negotiated settlements.

Regulatory arbitrage here is not illegal per se; it is institutionalized, operating through lawful settlements, consent orders, and tribunal relief rather than outright evasion. The result is a normalized tolerance for governance risk, priced into transactions rather than eliminated.

3.7. IBC-Enabled Impunity and the “Clean Slate” Doctrine

India’s Insolvency and Bankruptcy Code (IBC) was designed to resolve distressed assets efficiently and restore productive capacity. However, judicial interpretation—most notably in the DHFL resolution—has expanded the doctrine of the “clean slate” into a mechanism that detaches financial recovery from accountability.

The Supreme Court’s affirmation that avoidance transaction recoveries accrue exclusively to the resolution applicant crystallizes a profound shift:

- past fraud becomes a monetizable asset for the acquirer,

- creditors are extinguished as moral claimants once the plan is approved, and

- corporate entities gain de facto immunity from prosecution for pre-resolution offences.

This jurisprudence produces what may be termed IBC-enabled impunity: a legally sanctioned condition in which scale, timing, and procedural compliance outweigh substantive justice. While individual liability is theoretically preserved, in practice it is fragmented across investigative agencies and diluted by time, jurisdictional complexity, and evidentiary decay.

For acquiring entities such as Piramal Capital & Housing Finance, the IBC thus functions not merely as a resolution mechanism, but as a risk-laundering device—converting toxic assets and contested liabilities into legally cleansed balance-sheet entries.

3.8. Transnational Risk Transfer: From Global Banks to Domestic Stakeholders

Transnational risk transfer describes the process by which financial, legal, and reputational risks are displaced across borders and institutional layers. In this architecture:

- global banks externalize enforcement risk by operating through domestic intermediaries,

- domestic conglomerates absorb balance-sheet and reputational volatility, and

- retail investors, depositors, and informal stakeholders bear the ultimate losses.

Standard Chartered’s historical exposure to AML failures, sanctions violations, and investor litigation has heightened its sensitivity to reputational and compliance risk in Western jurisdictions. Engagements in emerging markets, therefore, increasingly prioritize legal insulation over prudential caution. This often takes the form of:

- structured lending,

- consortium participation,

- risk-shared financing, or

- arm’s-length capital market exposure rather than direct ownership.

Within this framework, entities like Piramal Finance act as risk absorbers, domestically anchoring capital flows that would be politically or regulatorily costly for foreign banks to hold directly. When stress materializes—whether through NPAs, insolvency, or regulatory action—the losses are localized, while the originating global institutions remain shielded by contractual distance and jurisdictional complexity.

3.9. The Political Economy of Asymmetric Accountability

What emerges is a system of asymmetric accountability:

- Global banks pay fines but retain licenses and market access.

- Large conglomerates consolidate assets through legal restructuring.

- Retail investors and small creditors experience irreversible loss.

This asymmetry is sustained by a convergence of:

- settlement-driven regulation,

- insolvency law prioritizing resolution speed over distributive justice, and

- capital markets that reward legal finality more than ethical clarity.

The Standard Chartered–Piramal constellation thus exemplifies a broader transformation in contemporary capitalism: risk is no longer eliminated, only displaced—across borders, balance sheets, and social classes.

This framework allows the paper to move beyond firm-specific critique toward a systemic diagnosis of financial governance in the Global South. The following conclusion synthesizes these findings to question whether contemporary financial law, as presently structured, resolves crises—or merely redistributes their consequences.

4. The Standard Chartered–Piramal Relationship: Financial Intermediation, Strategic Alignment, and Social Capital

Standard Chartered Bank (SCB) maintains a multi-layered relationship with the Piramal Group that extends beyond conventional lender–borrower dynamics. The relationship spans large-scale debt financing, capital market intermediation, and social-impact partnerships, positioning SCB as both a critical financial enabler and a reputational stakeholder in the Piramal Group’s post-restructuring trajectory. This section maps these linkages and situates them within the broader political economy of transnational banking and domestic conglomerate consolidation.

4.1 Financial Relationship and Funding Architecture

Standard Chartered has consistently functioned as a lead institutional financier to Piramal Group entities, particularly in periods of balance-sheet expansion and strategic repositioning. Its role has not been confined to passive lending but has often involved structuring, underwriting, and syndication, indicating a deeper alignment with the group’s capital strategy.

Table 4.1: Major Financial Transactions between Standard Chartered Bank and the Piramal Group

| Year | Transaction Type | Amount | Role of Standard Chartered | Piramal Entity |

|---|---|---|---|---|

| 2016 | Commercial real estate loan | ₹700 crore | Lead lender | Piramal Agastya (Mumbai project) |

| 2019 | Non-Convertible Debentures (NCDs) | ₹1,500 crore | Sole / major institutional investor | Piramal Enterprises Ltd |

| 2021 | Leveraged buyout financing | $355 million | Lead arranger (consortium) | Piramal Glass |

| 2024 | Syndicated social loan | $100 million | Sole Underwriter, Mandated Lead Arranger & Social Loan Coordinator | Piramal Finance |

| 2024 | Sustainability bond (international) | $300 million | Joint Global Coordinator & Bookrunner | Piramal Finance |

Analytical significance:

The concentration of roles—underwriter, arranger, coordinator, and bookrunner—suggests a relationship built on trust in governance representations, risk-sharing mechanisms, and confidence in regulatory closure, particularly in the post-DHFL period.

4.2 Capital Markets Intermediation and Risk Signalling

Standard Chartered’s participation in Piramal Finance’s debut international sustainability bond and maiden syndicated social loan is especially significant. These instruments rely heavily on:

- ESG-linked credibility,

- representations of end-use compliance, and

- assurances of internal monitoring and disclosure.

In this sense, the relationship is reciprocal:

- Piramal gains global capital access and legitimacy,

- SCB gains exposure to high-yield emerging-market assets structured within ESG-labelled frameworks.

4.3 Strategic Overlaps and Institutional Structure

While Standard Chartered does not hold equity stakes in Piramal Group companies, the two entities operate within overlapping institutional and sectoral ecosystems:

- Piramal Finance holds a 50% stake in Pramerica Life Insurance, while Standard Chartered maintains a long-standing global bancassurance partnership with Prudential plc (Pramerica’s joint-venture partner).

- Though these arrangements are not operationally merged, they indicate convergent institutional networks in insurance, finance, and risk distribution.

Additionally, SCB’s participation in the leveraged buyout financing of Piramal Glass illustrates its willingness to support highly leveraged industrial acquisitions, aligning with the group’s expansion-through-finance model rather than organic capital accumulation.

4.4 Philanthropo-Capitalist Collaboration and Social Capital Formation

Beyond commercial finance, Standard Chartered and the Piramal Group collaborate in philanthropic and CSR-linked initiatives, most notably through water and healthcare programmes.

By acting as Social Loan Coordinator and Global Bookrunner, SCB effectively signals Piramal Finance’s investability to international capital markets. This signalling function carries reputational implications, particularly given SCB’s own history of regulatory enforcement in AML, sanctions, and disclosure failures.

Key initiatives include:

- Piramal Sarvajal, a decentralised water-delivery model providing safe drinking water to over 0.5 million people daily across 123 villages and 25 schools in seven Indian states.

- Joint projects with the Enable Health Society aimed at reducing medical expenditure through improved water quality and hygiene practices in rural communities.

These collaborations serve a dual function:

- Delivering measurable social outcomes in under-served regions.

- Generating social legitimacy and reputational buffering for both entities amid heightened scrutiny of financial practices.

From an analytical standpoint, CSR partnerships function as a form of social capital intermediation, complementing financial intermediation by stabilising public perception and stakeholder trust.

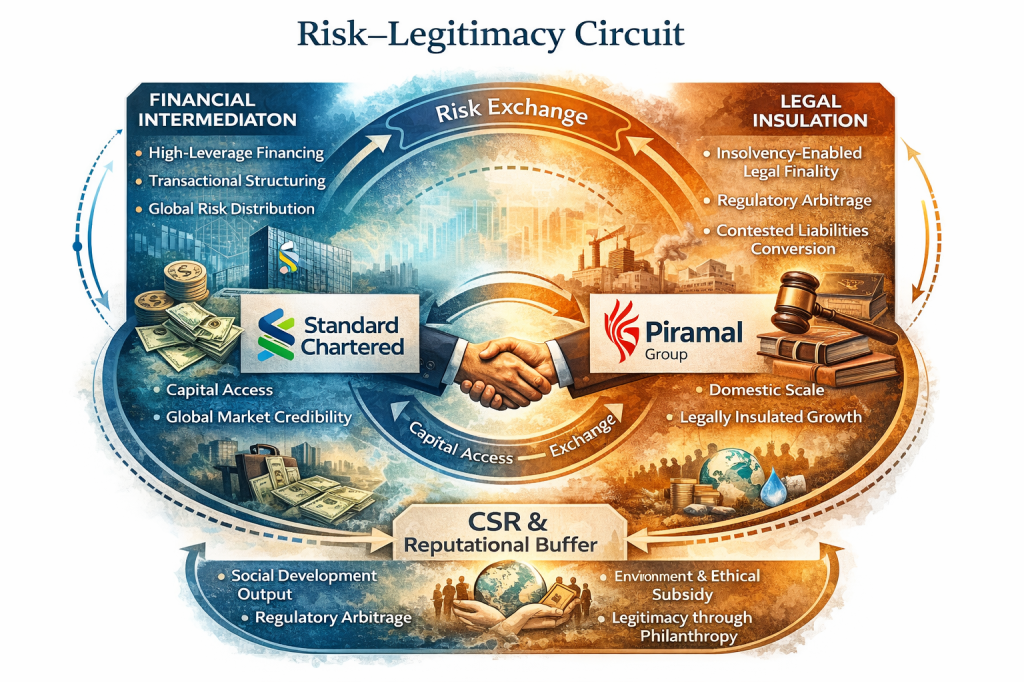

4.5. Synthesis: Relationship as Risk–Legitimacy Exchange

The Standard Chartered–Piramal relationship can thus be conceptualised as a risk–legitimacy exchange:

- Standard Chartered provides capital access, international market credibility, and transaction structuring expertise.

- The Piramal Group offers scale, domestic embeddedness, and legally insulated growth opportunities within India’s regulatory framework.

This relationship operates within the conditions identified earlier—regulatory arbitrage, insolvency-enabled legal finality, and transnational risk transfer—where financial exposure is carefully structured, accountability is jurisdictionally fragmented, and losses are socially asymmetrical.

By embedding global banking capital within domestically consolidated conglomerates, relationships such as that between Standard Chartered and the Piramal Group illuminate how financial power today travels through mased legality rather than legality constraining power. The concluding section will assess what this implies for democratic accountability, creditor justice, and the future architecture of financial regulation in emerging markets.

The relationship between Standard Chartered Bank and the Piramal Group can be understood as a complex circuit of financial risk and reputational legitimacy. Standard Chartered provides capital access, international market credibility, and transaction structuring expertise, while the Piramal Group supplies scale, domestic embeddedness, and legally insulated growth opportunities. Together, they operate within a transnational environment where regulatory arbitrage, insolvency-enabled legal finality, and global capital flows facilitate risk redistribution across jurisdictions and balance sheets.

Crucially, this risk–legitimacy circuit extends beyond conventional financial intermediation to CSR and social-impact initiatives. The Piramal Sarvajal programme exemplifies how corporate philanthropy and high-visibility CSR partnerships with Standard Chartered function as reputational instruments: they signal social responsibility to international and domestic stakeholders, while also potentially obscuring environmental and ethical critiques, such as those raised by water activist Rajendra Singh regarding water commodification, aquifer stress, and the displacement of community-led water governance.

Thus, CSR visibility reinforces the legitimacy of high-risk financial engagements, while simultaneously generating social outputs that are measurable but potentially misaligned with sustainable, bottom-up governance. In this sense, philanthropy functions as a dual instrument: it provides social benefit, but also buffers reputational and legal risk, complementing the capital and transactional roles that Standard Chartered fulfills in supporting Piramal’s corporate expansion.

By integrating environmental, social, and financial dimensions, the relationship illustrates how legality, market credibility, and CSR converge to organize and redistribute risk without necessarily imposing substantive accountability. CSR, like high-stakes financing and legal finality, becomes part of a systemic infrastructure that enables growth while simultaneously insulating the actors involved from social, environmental, and creditor consequences.

5. Financial Closure Without Accountability

This paper has examined the relationship between Standard Chartered Bank and the Piramal Group not as an aberrant convergence of two controversial institutions, but as a structurally legible configuration of contemporary finance. The evidence presented across regulatory histories, insolvency outcomes, and transnational financing arrangements suggests that what is at stake is not misconduct in isolation, but a reproducible institutional pattern.

Standard Chartered’s long record of sanctions violations, AML failures, market manipulation penalties, and investor litigation situates it within a global banking environment where enforcement increasingly operates through fines, settlements, and negotiated compliance rather than exclusion or disqualification. These mechanisms, while formally punitive, have proven compatible with continued expansion into emerging markets through legally insulated intermediaries.

The Piramal Group’s trajectory—marked by aggressive restructuring, regulatory settlements, and the legally finalised acquisition of DHFL—illustrates how domestic conglomerates function as risk absorbers and consolidators within this architecture. Insolvency law, particularly as interpreted under the IBC, has enabled the conversion of contested liabilities and fraudulent legacy transactions into assets of future value, while simultaneously extinguishing creditor claims and foreclosing avenues of collective redress.

The relationship between the two entities thus emerges as a risk–legitimacy circuit: global capital gains access to high-yield markets under the cover of legal finality and ESG-labelled instruments, while domestic capital secures international credibility and liquidity through association with systemically important banks. Accountability, by contrast, becomes fragmented—distributed across jurisdictions, deferred through procedure, and diluted by time.

What this configuration ultimately reveals is a shift in the function of financial law itself. Law no longer primarily arbitrates responsibility after harm; it increasingly organises the conditions under which harm is rendered legally untraceable. Insolvency, compliance settlements, and ESG frameworks do not eliminate risk or wrongdoing; they reorganise who bears their consequences and who is insulated from them.

In this sense, the Standard Chartered–Piramal relationship is not exceptional. It is emblematic of a broader political economy in which financial closure substitutes for justice, and legality operates less as a constraint on power than as its most reliable instrument.

References

Financial Conduct Authority. (2019, April 9). FCA fines Standard Chartered Bank £102.2 million for poor AML controls. https://www.fca.org.uk/news/press-releases/fca-fines-standard-chartered-bank-102-2-million-poor-aml-controls

Piramal Finance. (2024). Piramal Finance secures $100 Million loan to support social impact projects (Syndicated Social Loan coordinated by Standard Chartered Bank). https://www.piramalenterprises.com/Assets/download/Press-Releases/Piramal%20Finance%20Secures%20$100%20Million%20Loan%20to%20Support%20Social%20Impact%20Projects.pdf

Piramal Finance. (n.d.). Piramal Finance makes a standout debut in International Bond Markets with USD 300 Mn Sustainability Bond. https://www.piramalfinance.com/content/dam/piramalfinance/pdf/press-release/piramalfinance-debuts-in-international-bond-markets-sustainability-bond.pdf

Securities and Exchange Board of India (SEBI). (2024, July). Settlement Order in the matter of Piramal Enterprises Limited. https://www.sebi.gov.in/enforcement/orders/jul-2024/settlement-order-in-the-matter-of-piramal-enterprises-limited_85194.html (Note: Exact July 25 date confirmed in source metadata; focuses on insider trading/UPSI settlement.)

Supreme Court of India. (2025, April 1). Piramal Capital and Housing Finance Limited v. 63 Moons Technologies Limited & Others (2025 INSC 421). https://api.sci.gov.in/supremecourt/2022/5046/5046_2022_9_1501_60698_Judgement_01-Apr-2025.pdf (Note: This judgment upholds key aspects of the DHFL resolution plan under IBC, including treatment of avoidance transactions, legal finality, and CoC commercial wisdom.)

U.S. Department of Justice. (2019, April 9). Standard Chartered Bank admits to illegally processing transactions in violation of Iranian sanctions and agrees to pay more than $1 billion. https://www.justice.gov/archives/opa/pr/standard-chartered-bank-admits-illegally-processing-transactions-violation-iranian-sanctions

U.S. Department of the Treasury, Office of Foreign Assets Control (OFAC). (2012, December 10). Settlement Agreement between the U.S. Department of the Treasury’s Office of Foreign Assets Control and Standard Chartered Bank. https://ofac.treasury.gov/recent-actions/20121210

World Bank. (n.d.). Corporate Governance in Emerging Markets: Why It Matters to Investors—and What They Can Do About It. Open Knowledge Repository. https://openknowledge.worldbank.org/entities/publication/960fb58d-7f31-50cb-bb03-5239cd57b5b4 (Note: Foundational resource; no exact 2025 empirical study found, but this aligns with themes of governance/performance in emerging markets. Recent IFC/World Bank reports expand on similar empirical analyses.)

Exploring how global banks and Indian conglomerates navigate regulatory gaps, insolvency laws, and risk shifting — a deep dive into the Standard Chartered–Piramal relationship and its implications for accountability in finance.

Regulatory arbitrage, IBC-enabled finality & transnational risk transfer in action: Standard Chartered & Piramal Group.

#RegulatoryArbitrage, #InsolvencyRegimes, #RiskTransfer, #StandardChartered, #PiramalGroup, #PiramalFinance, #DHFLResolution, #IBCCleanSlate, #LegalFinality, #FinancialImpunity, #AMLFailures, #SanctionsViolations, #TransnationalRisk, #IndianBanking, #CorporateRestructuring, #SupremeCourtIBC, #SEBIInsiderTrading, #FinancialGovernance, #RiskRedistribution, #EmergingMarketFinance,

#BankruptcyBazaar, #IBCScam, #CronyCapitalismIndia, #DHFLScam, #FinancialJusticeIndia,#PolicyFailureIndia, #CorporateImpunity, #AuditFailure, #Seize_Cronies_Fairplay_for_DHFL_Victims, #Alleged_Dawood_Mirchi_RKW_DHFL_BJP_Collusion,

LikeLike