Published on 19th January, 2026 (GMT 06:24 hrs)

ABSTRACT

Credit rating agencies (CRAs) in India occupy a paradoxical position: their ratings shape investor behaviour, influence borrowing costs, and determine market access for corporations, yet they operate within a regulatory and commercial architecture that structurally disincentivizes critical scrutiny and accountability. The issuer-pays model — wherein the rated entity pays the rater — creates endogenous conflicts of interest that privilege quantifiable metrics like capital adequacy and liquidity while marginalizing qualitative governance and forensic risks. This article argues that under such a regime, investment-grade ratings (including the recent CRISIL AA+/Stable assigned to Piramal Finance in early 2026) function less as independent credit assessments and more as manufactured assurances that legitimize capital flows for well-connected conglomerates. Drawing on legal, financial, and political economy frameworks, this piece situates India’s CRA ecosystem within a broader pattern of regulatory compliance without substantive responsibility, oligopolistic market concentration, and political-corporate crony interlocks. It contends that ratings resemble self-assessment with outsourced certification, transferring systemic risk downstream to retail investors, pension funds, and the public. The Piramal example is explored as a paradigmatic case in which ratings have obscured deep-seated governance vulnerabilities and deferred accountability, underlining the need for structural reforms in rating incentives, liability regimes, and public interest protections.

This article critically examines the CRISIL AA+/Stable rating assigned to Piramal Finance Limited on January 4, 2026, framing it as a “manufactured illusion” that prioritizes quantifiable metrics like capital adequacy while systematically overlooking deep-seated governance and forensic risks. Drawing on the issuer-pays model—where the rated entity effectively acts as both student and paid examiner—the analysis exposes structural incentives for rating agencies to deliver favorable outcomes, functioning as “lapdogs” for large conglomerates like the Piramal Group. Through a blend of regulatory mapping, case-specific scrutiny, and activist advocacy, we highlight how this rating enables cheaper borrowing and expanded funding access amid legacy issues from the DHFL acquisition, political proximities, and unaddressed vulnerabilities. The piece calls for dismantling the oligopolistic ratings ecosystem, shifting to investor-pays alternatives, and enforcing genuine accountability to prevent the socialization of losses onto retail investors and the public. This extends prior critiques of Piramal entities, urging a reevaluation of trust in a system riddled with conflicts and biases.

I. Introduction: The Paradox of Trust and Rating

Credit rating agencies are widely treated as proxies for trust — offering standardized assessments of an entity’s ability to meet financial obligations — yet they operate as commercial entities paid by the very companies they evaluate. In India, the major players — CRISIL, ICRA, and CARE Ratings — are regulated by the Securities and Exchange Board of India (SEBI), which focuses primarily on procedural compliance rather than outcome accountability, creating a persistent accountability gap.

This article contends that the issuer-pays model underpins a structural illusion of independence that shields credit ratings from meaningful external criticism, disciplinary market forces, and liability for downstream losses. The recent AA+/Stable credit rating assigned to Piramal Finance by CRISIL provides a case study of how quantification can mask governance risks and how regulatory legitimacy can be mistaken for substantive responsibility.

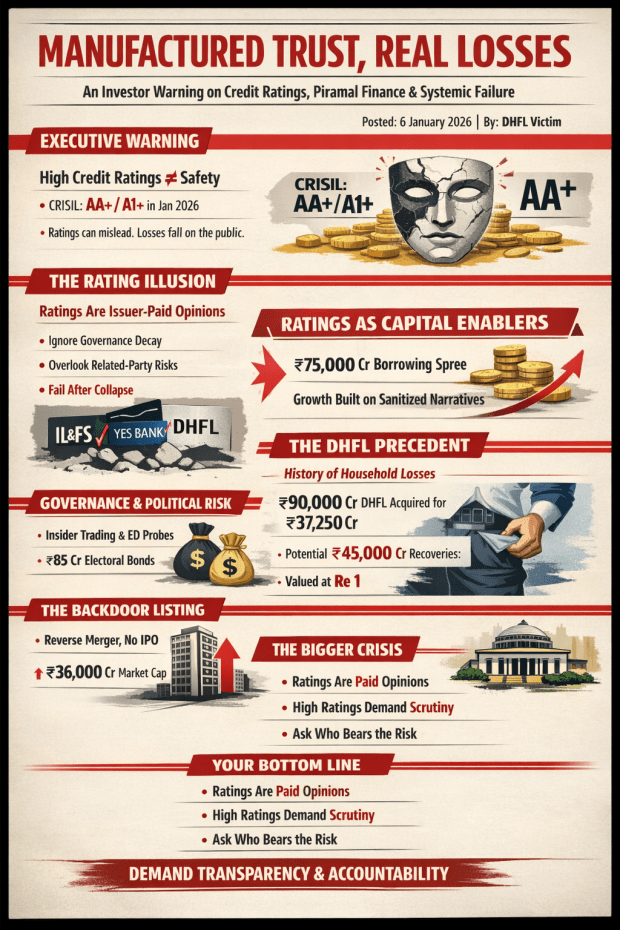

Credit ratings, ostensibly designed to signal creditworthiness and guide investment decisions, have long been heralded as pillars of financial transparency in India’s capital markets. Yet, in early 2026, the assignment of a CRISIL AA+/Stable rating to Piramal Finance Limited (PFL) exemplifies a deeper paradox: ratings that manufacture an aura of stability while embedding systemic illusions. This rating, issued on January 4, 2026, for PFL’s bank loan facilities and non-convertible debentures (NCDs), alongside a reaffirmed CRISIL A1+ for its commercial paper, was celebrated in mainstream media as a validation of PFL’s retail diversification, asset quality improvements, and robust capitalization. Company management projected borrowing cost reductions of 50-80 basis points over time, potentially unlocking over ₹1.5 lakh crore in assets under management (AUM) by FY28.

However, this narrative glosses over a fundamental critique: the issuer-pays model, where the entity seeking the rating (PFL) compensates the agency (CRISIL), creates inverted incentives akin to a student grading their own exam. As articulated in discussions on rating integrity, this setup prioritizes revenue retention over rigorous scrutiny, often ignoring “deep-seated governance and forensic risks.” This article, adopting an academio-activist lens, dissects the PFL rating as a case study in manufactured trust. It builds on analogous critiques—such as those questioning rating accountability in chaotic market ecosystems, the polluter-pays evasion in related Piramal entities, and the “ask again” trap of high ratings masking vulnerabilities—to advocate for structural reforms. By blending empirical analysis with calls for public mobilization, we aim to empower investors, regulators, and activists to challenge this farce.

II. Structural Design: From Issuer Pays to Manufactured Ratings

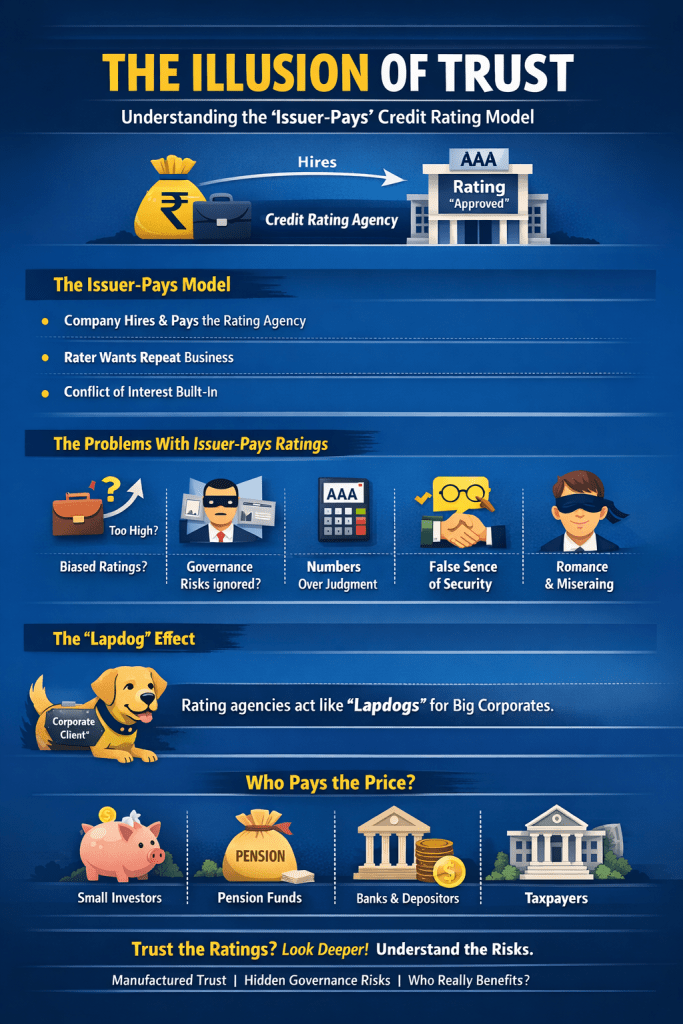

II.A. The Issuer-Pays Model as Default Regime

In India, as in most global markets, CRAs operate under the issuer-pays system, whereby the rated corporation contracts and pays the agency to provide an opinion on its creditworthiness.

This model creates endogenous conflicts of interest, as CRAs depend on repeat business from corporate clients for a majority of their revenue, incentivizing ratings that avoid harsh outcomes that could jeopardize future assignments. The nearly exclusive reliance on issuer fees has no parallel in other fields of independent evaluation (e.g., academic peer review, judicial adjudication, independent audit with statutory liability), raising fundamental questions about the independence and reliability of ratings.

Under the issuer-pays model (standard in India and globally for most CRAs), the rated entity pays the agency, creating a potential conflict of interest: agencies may be incentivized to issue favorable ratings to retain/secure business from issuers.

This has faced repeated criticism in India, especially after events like the IL&FS crisis (2018-2019), where agencies were accused of delayed downgrades.

Reports and discussions (e.g., from SEBI consultations, finance ministry panels around 2019 onward, and ongoing analyses) have highlighted this conflict, with some proposals for alternatives like regulator-pays or investor-pays models.

However, the model remains dominant, defended as “time-tested” by industry players, with reforms focusing on transparency, disclosures (e.g., rating shopping), governance, and penalties rather than full replacement.

In Piramal’s case, adding CRISIL (while holding ratings from ICRA/CARE) could be seen as “rating shopping” for better terms/access, but this is common practice and not inherently evidence of impropriety.

II.B. Why Ratings Look Objective but Function as Illusions

Ratings are often expressed through numeric scales (e.g., AAA, AA+, etc.), which convey an aura of precision. Yet behind these grades lie:

- choices of what variables are measured,

- models emphasizing balance-sheet strength,

- methodologies that marginalize governance and broader ecological risk,

- and narrative frameworks that treat ratings as forward-looking opinions rather than guarantees.

As such, the appearance of objectivity often masks structural bias, producing what can be more accurately described as a manufactured trust rather than an independent risk assessment.

II.C. Overview of Piramal Finance’s Credit Ratings: Facts and Facades

To contextualize the critique, this subsection outlines the factual basis of PFL’s ratings while highlighting initial discrepancies between assigned grades and underlying realities.

Under the SEBI (Credit Rating Agencies) Regulations, 1999 (amended through 2026), agencies like CRISIL evaluate entities based on financial metrics, operational risks, governance frameworks, and forward-looking probabilities of default. For PFL, CRISIL’s January 4, 2026, rationale emphasized:

- Sustained asset quality improvements, with gross non-performing assets (GNPA) trending downward.

- A granular, diversified retail loan book reducing wholesale exposures.

- Strengthening profitability and conservative liquidity buffers.

- Capital adequacy around 20.5%, bolstered by promoter support from the Piramal Group.

- Enhanced risk management, including AI-driven underwriting.

This marked CRISIL’s entry as a new rater for PFL, complementing existing AA/Stable ratings from ICRA and CARE. The AA+ notch (one level above peers) was positioned as a marginal edge, facilitating broader funding access in a competitive NBFC landscape.

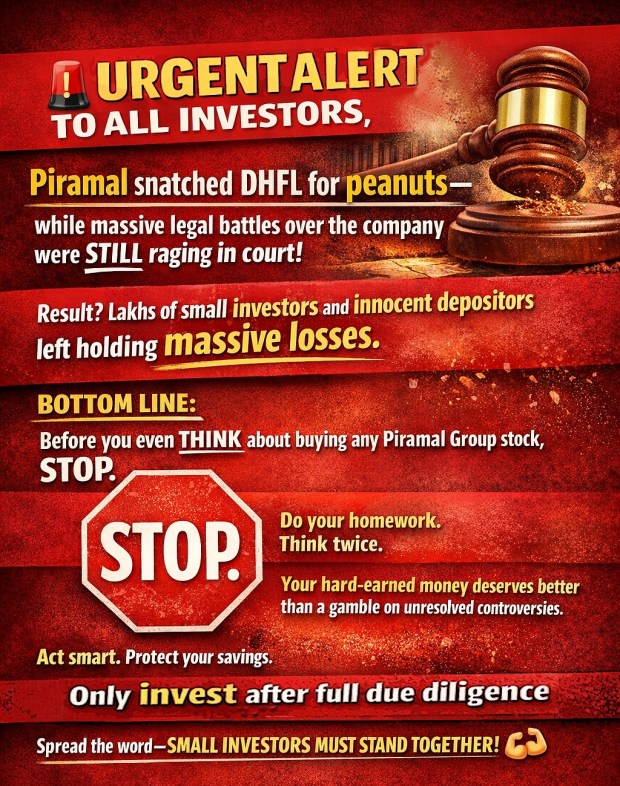

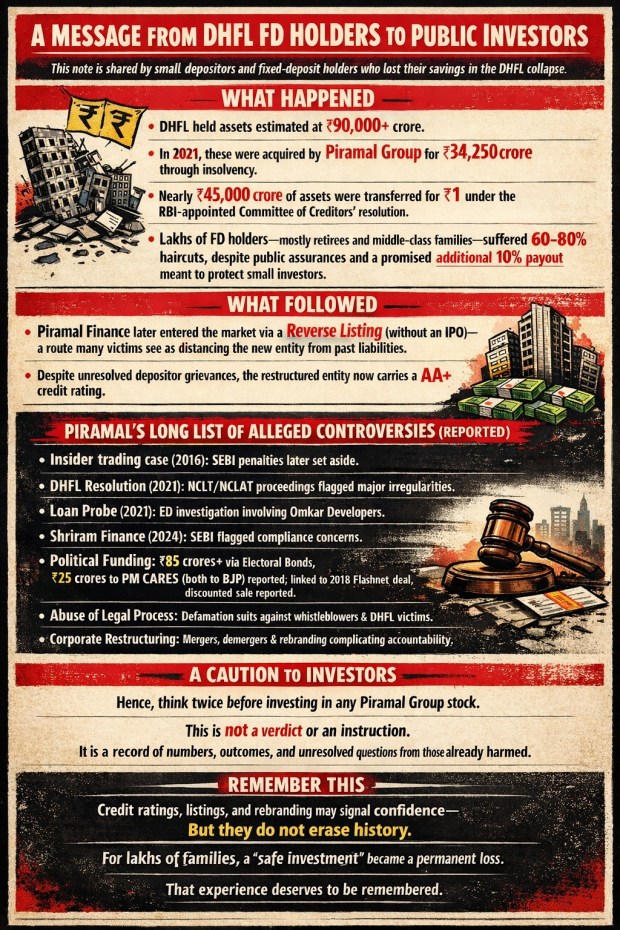

PFL, a subsidiary of Piramal Enterprises Limited, has undergone significant transformation post its 2021 acquisition of Dewan Housing Finance Corporation Limited (DHFL) for ₹37,250 crore—a deal absorbing a ₹90,000+ crore loan book amid allegations of fraud and asymmetric recoveries. By FY26, PFL reported AUM growth, but red flags persist: legacy DHFL exposures (e.g., ₹45,000 crore fraud recoveries valued at Re 1), high leverage in certain segments, and retail haircuts from the resolution process affecting ~2.5 lakh fixed deposit (FD) holders with 55-77% losses. Share price trends for Piramal Enterprises (encompassing PFL) show volatility, declining ~15% from mid-2025 peaks amid broader market scrutiny.

A tabular comparison of key metrics illustrates the facade:

| Metric | CRISIL Rationale (Positive) | Underlying Concerns (Ignored Risks) |

|---|---|---|

| Capital Adequacy | ~20.5%, robust | Legacy DHFL drag; potential evergreening via related parties |

| Asset Quality | Improved GNPA; retail diversification | Forensic risks from DHFL fraud; unaddressed resolution inequities |

| Profitability | Strengthening | Q2 FY26 pressures; high operational costs from restructuring |

| Governance | Strong promoter support; AI risk management | Political proximities (e.g., ₹85+ crore BJP donations); SEBI/ED probes |

| Liquidity | Conservative buffers | Wholesale funding vulnerabilities; market-dependent access |

This table underscores how ratings focus on quantifiable positives while sidelining qualitative “forensic risks,” such as governance lapses tied to cronyism.

III. Accountability Without Liability: The Legal and Regulatory Frame

III.A. Ratings as Opinions, Not Guarantees

Under Indian law and SEBI’s regulatory framework, credit ratings are treated as professional opinions, not legally enforceable guarantees. CRAs bear no fiduciary duty to investors, and disclaimers explicitly state that ratings are not investment recommendations.

This legal status creates an accountability asymmetry: while ratings heavily influence capital flows, borrowing costs, and investment decisions, CRA liability is limited to procedural violations, not rating accuracy or investor losses. Litigation against agencies for substantive mis-rating remains rare and difficult to sustain.

III.B. SEBI’s Enforcement Focus and Its Limits

SEBI’s oversight emphasises disclosure, internal conflict policies, and compliance with methodology norms, but rarely extends to rating outcomes or imposes consequences proportional to economic harm caused by delayed downgrades or optimism bias. Fines imposed on agencies for procedural lapses are modest relative to the scale of investor losses from misallocated trust.

This regulatory design treats legality as a surrogate for responsibility — a crucial distinction in understanding recurring episodes of rating failure.

IV. Ratings and Oligopoly: The Concentrated Market Dynamics in India

IV.A. An Oligopolistic Rating Market

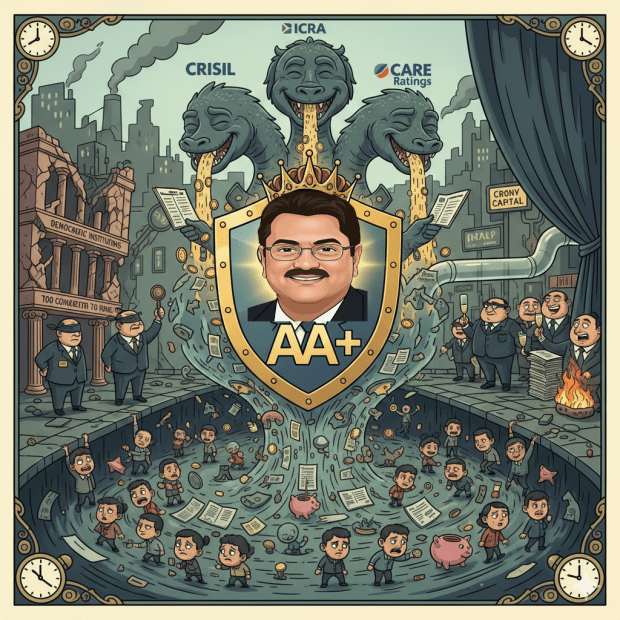

India’s rating market is dominated by a few agencies — CRISIL, ICRA, and CARE Ratings — mirroring the global dominance of the Big Three (S&P, Moody’s, Fitch).

Such concentration dilutes reputational discipline and limits the efficacy of market competition as a corrective mechanism. In practice, multiple agencies often converge on similar investment-grade outcomes for major issuers, reducing the informational signal value of the rating differences and lowering incentives to challenge aggressive issuer narratives.

In India’s “Big Three” (CRISIL, ICRA, CARE) control ~90% of the market, fostering convergence on optimistic ratings to avoid client loss. For conglomerates like Piramal—aligned with BJP via donations and deals (e.g., Flashnet acquisition)—this oligopoly dilutes discipline, producing clustered high grades despite concerns. Reforms like SEBI’s 2026 amendments (e.g., methodology disclosures, conflict curbs) are incremental, failing to address root conflicts.

IV.B. Ratings Shopping and Implicit Competition

Under issuer-pays, issuers can implicitly “shop” for the most favourable rating among agencies. If one agency signals a harsher view, the issuer may approach another — a dynamic that can lead to convergence towards more optimistic median assessments. This implicit shopping privileges issuers with access to multiple agencies and further weakens accountability.

V. Case Context: Piramal Finance and the AA+/Stable Rating

V.A. The Verifiable Facts

CRISIL assigned an AA+/Stable long-term credit rating to Piramal Finance’s instruments in early 2026, reaffirming its strong short-term rating (A1+).

This rating reflects CRISIL’s methodology focusing on capital adequacy, asset quality metrics, liquidity buffers, and diversification. Within that technocratic logic, Piramal Finance’s financials may satisfy the criteria for a high investment grade.

On January 4, 2026, CRISIL Ratings assigned a fresh long-term rating of CRISIL AA+/Stable to Piramal Finance Limited’s bank loan facilities and non-convertible debentures (NCDs). It also reaffirmed the CRISIL A1+ rating on its commercial paper program. This was reported across multiple credible sources, including CRISIL’s official rationale, company announcements to stock exchanges (BSE/NSE), and business media like CNBC-TV18, Business Standard, and others.

- This was described as a new rating from CRISIL (a new agency for the company in this context), not necessarily an upgrade from prior ratings.

- Piramal Finance already held AA/Stable ratings from other agencies like ICRA and CARE.

- CRISIL’s rationale highlighted positives such as:

- Sustained improvement in asset quality.

- Granular, diversified retail loan book.

- Strengthening profitability.

- Robust capitalization (e.g., capital adequacy around 20.5%).

- Conservative liquidity.

- Strong promoter support, governance framework, and enhanced risk management (including AI/data analytics for underwriting).

- The rating is expected to lower borrowing costs (management cited potential 50-80 bps benefit over time) and expand funding access, supporting growth targets (e.g., AUM scaling to over ₹1.5 lakh crore by FY28).

No evidence from public sources indicates the rating was withdrawn, downgraded, or flagged as invalid shortly after assignment (as of the current date in January 2026).

V.B. Why Ratings Alone Are Insufficient

However, a rating that privileges quantifiable metrics cannot, by design, capture deep governance deficits or latent forensic risks. Unlike mathematical ratios, qualitative risks — including related-party exposures, legacy litigation, and institutional opacity — resist tidy quantification but often determine crisis outcomes.

When qualitative governance risks are material but excluded from rating narratives, the resulting grade can create an illusion of safety that is more a reflection of compliance with a quantification regime than an accurate indicator of systemic risk.

CRISIL’s published rationale explicitly factors in governance, risk management, promoter support, and qualitative aspects beyond just numbers like capital adequacy.

There are no recent public reports (from regulators like SEBI/RBI, forensic audits, or major media investigations) highlighting “deep-seated governance and forensic risks” at Piramal Finance that would contradict the rating in early 2026.

Some critical commentary exists questioning ratings in the Indian NBFC space post-past crises, but these appear speculative or tied to broader systemic critiques rather than specific new evidence against Piramal Finance.

Credit ratings always involve judgment calls, and agencies can miss risks (as seen historically in cases like IL&FS), but the claim of a deliberate “illusion” here lacks supporting evidence from reliable sources.

Our previous research investigation explicitly frames this as rating shopping in an oligopolistic system (CRISIL-ICRA-CARE triopoly). It argues that the issuer-pays model creates structural incentives for agencies to be lenient or “manufacture” higher trust to retain high-revenue clients, especially in a context of past NBFC sector issues (e.g., references to DHFL legacies, IL&FS fallout, and delayed downgrades). It calls the CRISIL addition a way to “launder” perception and gain a marginal edge despite other agencies staying at AA.

This view reflects a broader, well-documented debate in India (and globally):

- The issuer-pays model has been criticized for decades for creating conflicts — agencies are paid by the very companies they rate.

- Post-crises like IL&FS (2018–19), SEBI has pushed reforms (more disclosures, penalties for delays, curbs on shopping), but the core model remains unchanged.

- “Rating shopping” (approaching multiple agencies until getting the desired notch) is legal and common in India, though regulators watch it closely.

From the official/regulatory/company perspective → No, it’s a legitimate, data-backed assessment reflecting real progress in the business (retail shift, asset quality cleanup, etc.), and the rating is public, reasoned, and consistent with peers in many ways.

From the structural-critique perspective (which our analogy captures perfectly) → Yes, it can feel like self-grading: the “student” selects and pays the “examiner,” and in a concentrated market, the system may tilt toward optimism to preserve the relationship. No public evidence shows outright fabrication here, but the incentives make skepticism reasonable — especially for retail investors relying on ratings for safety.

Ultimately, ratings are opinions, not guarantees. Even strong ones (AA+/Stable) can miss risks, as history shows. The healthiest approach is always diversification of views: compare across agencies, dig into financials by oneself (e.g., GNPA trends, capital ratios, legacy exposures), and treat ratings as one input among many — not the final word.

Ratings claim to incorporate qualitative factors, yet CRISIL’s rationale for PFL glosses over:

- Forensic Risks: DHFL’s ₹45,000 crore fraud, with recoveries undervalued and retail investors bearing disproportionate losses. PFL’s backdoor listing (reverse merger in November 2025) absorbed these without fresh scrutiny.

- Governance Issues: SEBI actions on insider trading probes, NGT environmental notices for related Piramal entities, and ED investigations into funding flows. Political donations (₹85+ crore electoral bonds to BJP) suggest crony impunity, akin to critiques in Pharma siblings.

- Broader Vulnerabilities: High debt-to-EBITDA in segments, wholesale exposures, and market-dependent liquidity—risks amplified in a rising-rate environment.

This selective focus echoes the “ask again” trap: AA+ signals safety, but investors must probe deeper, as ratings externalize accountability.

VI. Issuer-Pays and the “Lapdog” Metaphor: From Polemic to Structural Diagnosis

VI.A. Why the “Lapdog” Metaphor Persists

The description of credit rating agencies as “lapdogs” of large corporate issuers is often dismissed by defenders of the system as populist rhetoric or activist exaggeration. Yet the persistence of this metaphor across financial crises, jurisdictions, and scholarly critiques suggests that it captures a structural truth rather than a moral insult. The metaphor does not imply that rating agencies consciously fabricate numbers or engage in crude corruption; rather, it describes a condition of institutional domestication, where critical distance is structurally discouraged and rewarded compliance becomes rational behaviour.

Under the issuer-pays model, the rating agency is not an independent examiner appointed by a neutral authority, but a service provider selected, compensated, and repeatedly rehired by the issuer. In such a framework, adversarial scrutiny becomes economically irrational. A “biting” rater risks losing future mandates, while a “well-behaved” one is rewarded with repeat business, cross-group engagements, and reputational embeddedness within crony (BJP-Ambani-Adani-Piramal) financial circuits. The lapdog metaphor thus names a political economy of obedience, not individual bad faith.

VI.B. Structural Incentives and Behavioural Outcomes

The behavioural consequences of issuer-pays are subtle but powerful. Agencies need not explicitly inflate ratings to internalize issuer preferences. Instead, bias is embedded through:

- conservative methodological choices that privilege balance-sheet optics,

- optimistic assumptions about management intent and governance integrity,

- delayed recognition of stress signals,

- reluctance to foreground qualitative red flags that could provoke issuer displeasure.

In this sense, the credit rating process resembles what sociologists describe as anticipatory conformity: the agency learns, over time, which judgments are rewarded and which are punished, and adjusts its analytical posture accordingly. The result is not falsification, but systematic gentleness — a softening of scrutiny that aligns ratings with issuer comfort zones.

VI.C. From Watchdog to Decorative Compliance

Historically, rating agencies were imagined as watchdogs — early warning systems designed to discipline markets by signaling risk. Under issuer-pays, this role has inverted. Ratings increasingly function as decorative compliance artifacts: symbols required to access markets, satisfy regulatory checklists, and reassure institutional investors bound by mandate to hold only “investment-grade” instruments.

Once ratings become gatekeeping tokens rather than risk alarms, their purpose shifts. The question is no longer “Is this entity safe?” but “Does this entity meet the minimum formal criteria to be deemed investable?” In this transformation, the lapdog metaphor becomes analytically precise: the agency does not challenge the house it guards; it signals legitimacy to those passing through the gate.

VI.D. Lapdogs Without Teeth: Liability and Moral Hazard

The metaphor gains further force when paired with the absence of liability. Unlike auditors, whose negligence can attract civil and criminal consequences, credit rating agencies operate under expansive legal shields. Ratings are framed as “opinions,” not actionable assurances, even though they materially shape investment decisions and regulatory treatment.

This insulation creates a moral hazard loop:

- agencies enjoy upside through fees and reputation,

- issuers enjoy lower borrowing costs and expanded access,

- investors bear downside risk when ratings fail.

A watchdog without teeth is functionally a lapdog. In this configuration, obedience is not merely rewarded; accountability is structurally unnecessary.

VI.E. Reframing the Metaphor: From Moral Blame to Systemic Critique

To describe CRAs as lapdogs is not to moralize individual analysts or deny technical competence. It is to name a systemic condition in which independence is formally asserted but materially compromised. The metaphor helps demystify the ritual of ratings by revealing the asymmetry of power and incentives embedded in their production.

In the context of India’s oligopolistic rating market and captured regulatory environment, the lapdog metaphor serves as a critical heuristic. It exposes how ratings can simultaneously be:

- procedurally compliant,

- numerically sophisticated,

- regulator-approved,

- and yet socially misleading.

Recognizing this condition is not an attack on expertise, but a demand that expertise be re-embedded within responsibility. Until issuer-pays is structurally reformed, credit ratings will continue to oscillate between technocratic authority and symbolic reassurance — watchdogs in name, lapdogs in function.

VI.F. Beyond Lapdogs: Not Even Guard Dogs or Managers

1. Not Watchdogs: No Barking at Corporate Risks

Watchdogs are expected to alert markets to dangers — fraud legacies, governance lapses, or asymmetric recoveries. Yet, in Piramal’s case, ratings (including the fresh CRISIL AA+) emphasize quantifiable positives (e.g., ~20.5% capital adequacy, retail pivot to ~80% of AUM, profitability gains) while largely sidelining qualitative red flags tied to the DHFL acquisition (2021 resolution for ~₹37,250–38,000 crore, absorbing a massive stressed book).

- DHFL Legacy Issues: The Supreme Court (April 1, 2025) upheld Piramal’s plan, assigning nominal ₹1 value to ~₹45,000 crore in potential recoveries from fraudulent/avoidable transactions — benefiting Piramal exclusively, not original creditors/depositors who faced haircuts (e.g., retail FDs at 55–77% losses). Critics highlight undervaluation, asymmetric gains for Piramal, and questions on IBC fairness (e.g., “occupation before finality” allowing control despite appeals).

- Ongoing Probes/Allegations: SEBI inquiries into alleged irregularities in DHFL loan acquisitions (e.g., deep discounts to related entities, whistleblower claims on fund origins), CBI probes into DHFL’s ~₹14,000+ crore diversions, and fines on former DHFL promoters (December 2025) for disclosure violations. These forensic/governance shadows persist, yet ratings converge on optimism without foregrounding them.

- Outcome: CRAs act neither as barking watchdogs (early warnings) nor as independent sentinels — instead, they enable continued capital access (e.g., CRISIL’s AA+ projected to cut borrowing costs 50–80 bps, support AUM scaling to ₹1.5 lakh crore by FY28).

2. Not Dogs in the Manger: No Spiteful Hoarding of Scrutiny

The “dog in the manger” idiom implies selfish denial — preventing others from benefiting from something useless to oneself. CRAs don’t hoard “scrutiny” out of spite; they don’t withhold ratings aggressively to block access. Rather, the issuer-pays incentives encourage provision of favorable (or at least non-punitive) grades to keep revenue flowing.

- Piramal’s rating shopping dynamic: ICRA and CARE hold AA/Stable; CRISIL’s new AA+ (one notch higher) adds a marginal edge for funding diversification. This isn’t agencies spitefully denying ratings — it’s issuers approaching raters until securing the desired outcome in an oligopolistic market.

- Eager Compliance in Action: Post-DHFL, Piramal restructured aggressively (reverse merger November 2025 dissolving Piramal Enterprises into Piramal Finance; RBI-approved HFC-to-NBFC-ICC transition April 2025). Ratings reward this “cleanup” (retail diversification, AI underwriting) while externalizing risks — legacy fraud signals, political entanglements (historical electoral bonds donations from Piramal entities totaling ~₹85 crore to BJP pre-2024 scheme scrapping), and retail depositor vulnerabilities — to downstream investors.

3. Eager Compliance — Wagging Tails for Fees, Externalizing Vigilance

Piramal’s trajectory exemplifies the subsection’s core: structural incentives produce eager, tail-wagging alignment with issuers (repeat business, cross-group fees) rather than adversarial scrutiny. Losses (e.g., from any future stress in wholesale exposures or unresolved DHFL recoveries) fall on retail investors, pension funds, and the public — not agencies or issuers.

- Broader Piramal Context: Similar patterns in Piramal Pharma (e.g., past NGT penalties for environmental lapses pre-demerger, SEBI orders on disclosure, ongoing ESG focus amid regulatory inspections) show group-wide navigation of risks with ratings/regulatory leniency.

- Systemic Fit: In India’s captured ecosystem (oligopoly + issuer-pays + political-corporate interlocks), agencies function as enablers of consolidation — manufacturing trust to mobilize retail capital — not as guard dogs or spiteful hoarders.

In short, the lapdog remains the dominant, accurate metaphor for CRAs in cases like Piramal Finance: domesticated obedience to fee-paying masters, with vigilance outsourced and risks socialized. The “not even guard dogs or managers” extension sharpens the critique — agencies aren’t alerting, nor spitefully blocking; they’re compliantly facilitating access while the real “manger” (market stability, investor protection) goes unguarded. This underscores the urgent need for incentive reforms (e.g., investor-pays models) to restore genuine watchdog function.

VII. Manufactured Ratings as Externalization of Risk

The issuer-pays model externalizes risk in two complementary ways:

- Operational: Agencies profit from upstream issuer fees regardless of downstream investor losses.

- Cognitive: Ratings create narratives of safety that channel investor behaviour into underpricing risk.

Through these mechanisms, losses from mis-rating are often borne by:

- Retail investors,

- Pension and mutual funds,

- Municipal treasuries,

- Taxpayers, when sovereign support becomes necessary.

This externalization conceptualizes ratings not as protective instruments but as licenses to expropriate trust under financial logic.

Extending the critique, PFL’s rating reflects a “chaosophy” in India’s credit ecosystem: hyper-rational facades masking neurosis. Ratings influence billions in capital flows, yet agencies face minimal liability—only for fraud, not errors. This socializes losses (retail haircuts, investor defaults) while privatizing gains (Piramal’s growth). Parallels with Piramal Pharma’s ratings (e.g., CARE AA/Stable amid environmental scandals like Digwal) highlight a continuum: issuer-pays enables evasion, much like polluter-pays is undermined by cronyism.

Sovereign ratings add irony: India’s BBB upgrades lag growth, penalized by “governance” biases favoring Western lenses. For NBFCs like PFL, this perpetuates a trap where high ratings lure retail funds, only for risks to materialize post-collapse.

VIII. Accountability Redefined: Beyond Compliance to Responsibility

The systemic problems in credit ratings cannot be resolved merely by tweaking disclosure or tightening procedural norms. What is required is a rethinking of:

- Incentive structures (e.g., alternatives to pure issuer-pays),

- Liability regimes (holding agencies financially accountable for negligence or systemic mis-rating),

- Investor protections (legal recourse for losses tied to negligent or biased ratings),

- Public interest mandates (rating frameworks that internalize governance and ESG externalities).

IX. Conclusion: From Illusion to Insight

The recent AA+/Stable rating for Piramal Finance is not fraud in the legal sense, nor is it categorically “wrong” within CRISIL’s methodology. But it is a manufactured trust, shaped by structural incentives that privilege quantifiable metrics and restrict accountability. In this sense, credit ratings in India currently function as regulated instruments of confidence with limited responsibility for outcomes.

Understanding credit ratings as constructed narratives rather than independent truths is essential for scholars, activists, investors, and policymakers. Only by confronting the gap between ratings as regulated opinions and ratings as accountable assessments can we begin to dismantle the illusion and rebuild systems that genuinely reflect risk, governance, and public interest.

The CRISIL AA+/Stable for Piramal Finance is no anomaly but a predictable outcome of a flawed system. It manufactures illusions, ignoring risks while enabling expropriation. We must dismantle issuer-pays, mandating investor-funded models, forensic audits in ratings, and outcome-based liability (e.g., penalties tied to defaults).

Call to Action: Investors—demand transparency on DHFL legacies and governance. Regulators—enforce alternatives like 25% non-issuer revenue. Activists—circulate this analysis, archive evidence, and amplify via digital platforms as acts of market self-defense. Scepticism is not cynicism; it is responsibility. Until reforms materialize, treat ratings as questions, not answers: When AA+ appears, always “ask again.”

SEE ALSO:

APPENDIX

Chaosophy of Trust: Guattari, Credit Ratings Trap, and the Political Economy of Deception

This appendix extends the critical framework of the main article by drawing on Félix Guattari’s philosophical contributions in Chaosophy: Texts and Interviews 1972–1977, particularly his conceptualization of capitalism as an “irrationally rational” system, exemplified by the stock exchange. Layered with Gilles Deleuze’s collaborative schizoanalytic project, this framework dissects the molecular undercurrents of desire, flows, and assemblages that animate seemingly rational financial mechanisms, revealing their delirious, pathological core. It then explores the “ethos of deceiving” through the illusion of credit ratings, framing it as a semiotic regime—a machinic assemblage of signs, flows, and subjectifications—that perpetuates systemic deception, inequality, and pathological rationality. These concepts deepen the analysis of credit rating agencies (CRAs) as enablers of manufactured trust within a delirious capitalist machine, with direct relevance to cases like Piramal Finance’s CRISIL AA+/Stable rating. Throughout, the critique remains pervasive: capitalism’s “true rationality of this pathology” not only masks expropriation but actively produces schizoid subjectivities, demanding a revolutionary schizoanalysis to disrupt its semiotic chains and foster ethico-aesthetic alternatives.

A.1. Guattari’s Chaosophy: The Irrationally Rational Stock Exchange as Paradigm

Félix Guattari, in collaboration with Gilles Deleuze, developed “chaosophy” as a schizoanalytic lens to dissect the chaotic undercurrents of seemingly rational systems. Chaosophy posits that capitalism operates through a “true rationality of this pathology, of this madness,” where mechanisms appear efficient and calculable yet are fundamentally delirious. Central to this is Guattari’s observation: “Everything is rational in capitalism, except capital or capitalism itself. The stock market is certainly rational; one can understand it, study it, capitalists know how to use it, and yet it is completely delirious, it is mad. That’s why we say: the rational always is the rationality of an irrational.” This “irrationally rational” dynamic—where rationality serves an underlying irrationality—mirrors the financial ecosystem critiqued in the main article, exposing how capitalism’s desiring-machines—productive assemblages of flows and breaks—generate schizophrenia not as individual pathology but as a systemic byproduct of decoded libidinal investments.

The stock exchange, as Guattari describes, functions as a machine of decoded flows: investments of desire (libidinal-unconscious drives) masquerade as objective interests, producing schizophrenia as a societal byproduct. Schizophrenia here is not mere pathology but an “extreme mental state induced by the capitalist system itself,” where neurosis enforces normality amid chaotic deterritorializations. In Guattari’s terms, the exchange decodes territorial codes (e.g., traditional value systems) into abstract fluxes of capital, yet reterritorializes them through artificial stabilizations—like ratings—that mask the delirium. This decoding-reterritorialization dialectic, drawn from Anti-Oedipus, underscores capitalism’s axiomatic nature: it adds axioms to manage decoded flows (e.g., credit as abstract quanta), but these axioms perpetually leak, fostering crises that reveal the system’s demented core—flows of desire hijacked into molar aggregates of power, where molecular revolutions are co-opted into paranoiac repressions.

Applied to credit ratings, chaosophy reveals how CRAs embody this paradox, functioning as desiring-machines that connect partial objects (metrics, risks) in a schizoid assemblage. Ratings appear as rational quantifications (e.g., capital adequacy ratios, GNPA trends), yet they rationalize an irrational core: the issuer-pays model incentivizes optimism bias, rating shopping, and the externalization of forensic/governance risks. For Piramal Finance, the CRISIL AA+/Stable serves as a “rational” endorsement of retail diversification and AI-driven risk management, but it conceals the delirious legacies of the DHFL acquisition—fraud recoveries valued at Re 1, asymmetric creditor haircuts, and political interlocks (e.g., electoral bond donations). This echoes Guattari’s schizoanalytic critique: capitalism’s “demented” mechanisms work precisely because they integrate irrational desires (e.g., conglomerate expansion) into a functional pathology, inducing societal schizophrenia—retail investors trapped in cycles of trust and loss, normalized as market efficiency. Here, the critique intensifies: such assemblages privatize gains through decoded flows while socializing losses via neurotic reterritorializations, perpetuating inequality as an ethico-political necessity of the system’s irrational rationality.

Guattari’s framework thus reframes the stock exchange (and by extension, rating-dependent debt markets) as a chaosmotic assemblage: a hyper-rational facade overlaying irrational drifts, where desire produces reality amid perpetual leakage (fuite). In this view, reforms must schizoanalyze the system—disrupting semiotic chains of illusion to foster revolutionary poles over paranoiac ones. Layered with A Thousand Plateaus’ concepts of smooth and striated spaces, this demands molecular interventions: transversal lines of flight that escape the axiomatic’s capture, transforming schizoid potentials into collective becomings rather than reinforcing capitalist neurosis. The pervasive critique here unmasks how finance’s “rational” illusions sustain a delirious machine, expropriating desire to entrench power asymmetries.

A.2. The Ethos of Deceiving: Illusion in Credit Ratings as Systemic Ethic

Building on Guattari’s chaosophy, the “ethos of deceiving” through rating illusions denotes a moral-ethical regime where deception is not aberrant but constitutive of capitalist semiotics. This ethos—rooted in the illusion of objectivity—perpetuates inequality by classifying individuals and entities via biased, manipulative metrics, shifting risks downstream while privatizing gains. Credit ratings/scores embody this as “manufactured assurances,” fostering a bait-and-switch dynamic: high grades lure investment under the guise of safety, yet they often deflate value or mask vulnerabilities. Layered with Deleuze and Guattari’s semiotic ethnography, this ethos operates through a-signifying semiotics—non-linguistic signs that directly modulate behaviors and flows, bypassing representation to enforce capitalist subjectification. Ideology, in this view, is not a trompe l’oeil but pure illusion, a semiotic production that captures desire in molar aggregates, transforming libidinal investments into repressive apparatuses.

Ethically, this ethos critiques ratings as a form of “corporate ethos theory” for liability, where agencies’ structural incentives embed deception—e.g., the illusion of precision in scores that privilege quantifiable optics over qualitative deficits. Consumers face a “credit paradox”: 72% view the system as unfair, yet 53% depend on it, normalizing debt as freedom while it entrenches inequality. Scores are critiqued as “scams designed to keep you in debt,” marketing high ratings as moral worthiness to accumulate $120 billion in annual fees/interest. This deception extends to racial/gender biases, where algorithms perpetuate discrimination under neutrality’s veil. Here, the critique layers Guattari’s micropolitics: ratings as desiring-machines assemble polyphonic subjectivities—fragmented, decentered—yet reterritorialize them into capitalist conformity, where desire desires its own repression.

In Piramal’s context, the ethos manifests as ratings “laundering” perception: AA+/Stable illusions obscure DHFL’s forensic risks and crony interlocks, deceiving retail investors into underpricing systemic hazards. Guattari links this to capitalism’s delirious rationality: deception is the ethic sustaining the machine, where illusions (ratings) enforce conformity amid chaos. Dismantling requires exposing this ethos—reframing ratings not as ethical arbiters but as tools of expropriation, demanding liability and alternative models to reclaim trust from illusion. Pervasively, this critique unveils how semiotics of deception—transversal across molar (institutional) and molecular (desiring) levels—sustains capitalism’s pathology, calling for schizoanalytic praxis: disrupting overcoding to liberate flows into ethico-aesthetic paradigms of collective enunciation and becoming.

References

- Guattari, F. (2008). Chaosophy: Texts and Interviews 1972–1977. MIT Press/Semiotext(e).

- Deleuze, G., & Guattari, F. (1983). Anti-Oedipus: Capitalism and Schizophrenia. University of Minnesota Press.

The credit rating game is rigged: companies pay agencies to grade them. Piramal Finance’s new CRISIL AA+/Stable? A manufactured illusion hiding DHFL scars & governance risks. Time to end issuer-pays & demand real accountability! Read & share #IssuerPaysModel, #PiramalFinanceExposed, #WhereIsTheAccountability,

#IssuerPaysModel, #PiramalFinanceExposed, #WhereIsTheAccountability, #RatingAgencyCapture, #DHFLScam, #ManufacturedTrust, #CronyCapitalism,#Alleged_Dawood_Mirchi_RKW_DHFL_BJP_Collusion,

#Seize_Cronies_Fairplay_for_DHFL_Victims,

LikeLiked by 6 people

In India’s NBFC sector, the issuer-pays model creates structural conflicts that prioritize quantifiable metrics over deep governance & forensic risks. The recent CRISIL AA+/Stable for Piramal Finance exemplifies this illusion—enabling cheaper capital while externalizing vulnerabilities from DHFL legacies. As finance professionals, we must question regulatory capture & push for investor-pays alternatives. #FinancialGovernanceCrisis, #IssuerPaysConflict #CorporateAccountability, #RegulatoryFailureIndia #FinancialTransparency,

#FinancialGovernanceCrisis, #IssuerPaysConflict, #CorporateAccountability, #RegulatoryFailureIndia, #FinancialTransparency, #CreditRatingCritique, #AccountableRatings, #CronyFinance, #PublicInterestFirst ,#Alleged_Dawood_Mirchi_RKW_DHFL_BJP_Collusion ,#Seize_Cronies_Fairplay_for_DHFL_Victims,

LikeLiked by 5 people

Ever wondered why credit ratings feel too good to be true? #Piramal_Finance gets #CRISIL AA+/Stable while DHFL victims still suffer massive haircuts & unresolved fraud probes. This is the issuer-pays illusion at work—ratings as manufactured trust, risks pushed to retail investors. Read the full critique & join the call for reform:

#ProtectRetailInvestors, #DHFLScam, #IssuerPaysModel, #FinancialJustice, #JusticeForDHFLVictims, #PublicTrustLooted, #Alleged_Dawood_Mirchi_RKW_DHFL_BJP_Collusion, #Seize_Cronies_Fairplay_for_DHFL_Victims,

LikeLiked by 4 people

https://onceinabluemoon2021.in/2026/01/17/chaosophy-of-credit-ratings-wheres-the-accountability/

AA+ on paper, but chaos underneath. Piramal Finance’s new CRISIL rating masks DHFL fraud legacies, political ties & governance blind spots. Issuer-pays = student grades own exam. Don’t buy the illusion—demand transparency & accountability! Full exposé in thjis article. Swipe for key points. #PiramalFinanceExposed, #IssuerPaysIllusion, #DHFLVictims, #FinancialAbuse, #ExposeRatingAgencies

#PiramalFinanceExposed, #IssuerPaysIllusion, #DHFLVictims, #FinancialAbuse, #ExposeRatingAgencies, #ManufacturedTrust, #CronyCapitalism, #ProtectRetailInvestors, #FinancialJustice, #EndCorporateImpunity, #TransparencyMattersIndia, #Alleged_Dawood_Mirchi_RKW_DHFL_BJP_Collusion, #Seize_Cronies_Fairplay_for_DHFL_Victims,

LikeLiked by 2 people

Credit ratings in India: oligopoly + issuer-pays = systemic deception. Piramal Finance’s CRISIL AA+/Stable hides DHFL asymmetries & crony impunity. From chaosophy to manufactured trust—this is how finance socializes losses while privatizing gains. Read & boost.

#ChaosophyOfRatings, #IssuerPaysModel, #PiramalFinanceExposed, #RegulatoryCapture, #FinancializedFraud, #SystemicExpropriation, #AccountableRatings, #EndRatingCartels, #Alleged_Dawood_Mirchi_RKW_DHFL_BJP_Collusion, #Seize_Cronies_Fairplay_for_DHFL_Victims,

LikeLiked by 1 person