Posted on 5th January, 2026 (GMT 04:36 hrs)

Updated on 21th January, 2026 (GMT 20:32 hrs)

ABSTRACT

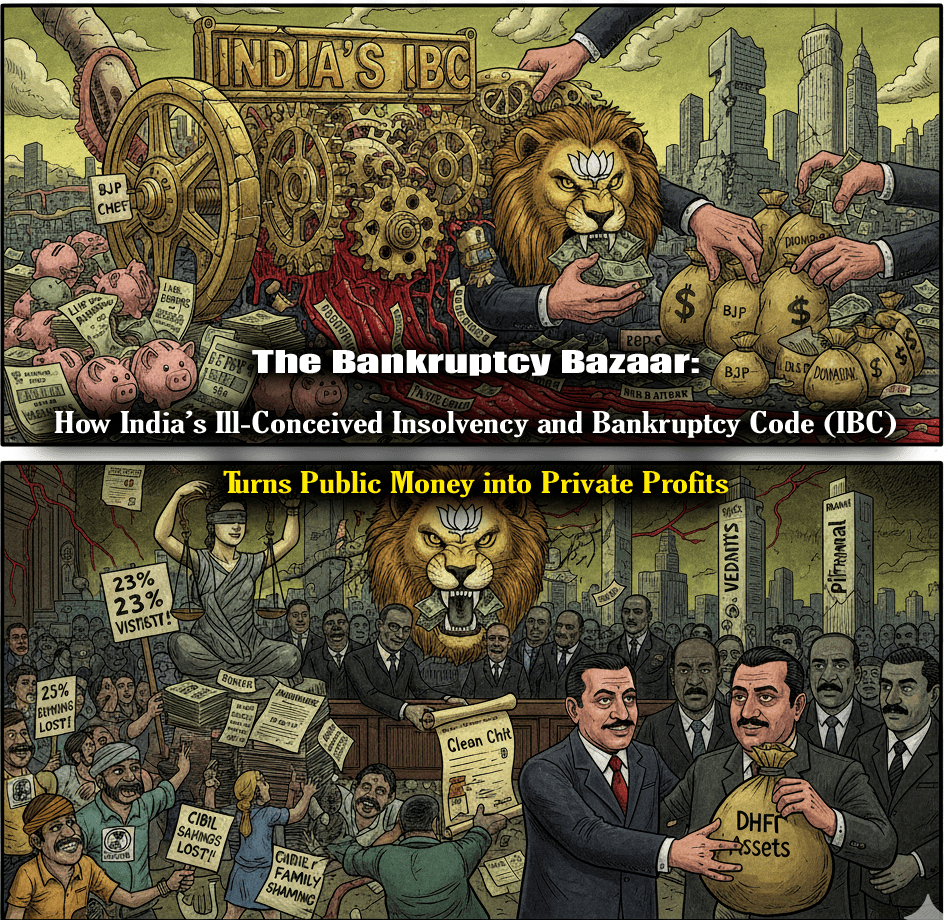

This article delivers a comprehensive indictment of India’s Insolvency and Bankruptcy Code (IBC), 2016, exposing it as a structurally predatory regime that facilitates crony expropriation rather than genuine resolution. Through doctrinal analysis, tribunal data, and emblematic case studies—Videocon, Aircel, Essar Steel, Bhushan Power, Reliance Communications, and most starkly DHFL—it demonstrates how time-bound resolution is a legal fiction, recoveries are abysmally low, avoidance provisions are systematically neutralised, and fraud is laundered through procedural finality. The DHFL case emerges as the perfect crime scene: mass dispossession of 2.5 lakh retail savers, assignment of vast avoidance recoveries at notional value to the acquirer, and judicial deference that extinguished constitutional claims. Situated within a wider political economy of crony capitalism and opaque political funding, the IBC is shown not as a failed reform but as rule by plunder—an insolvency regime that has gone rogue.

In Continuation With

0. Introduction

India’s Insolvency and Bankruptcy Code (IBC)—enacted in 2016 amid grandiose promises of swift debt resolution, value preservation, and economic revival—has instead revealed itself as a chronically amended, internally conflicted, and functionally degraded legal regime that systematically fails to deliver on its core objectives. Far from cleansing the rot of non-performing assets (NPAs), the Code has evolved into a juridical apparatus of elite expropriation, enabling the organised transfer of public wealth into private hands while shielding billionaire defaulters and their political patrons from accountability.

What presents itself as reform is, in reality, managed insolvency: a predatory framework that enforces illusory timelines, delivers abysmal recoveries, imposes staggering haircuts on creditors—predominantly public-sector banks laden with taxpayer funds—and launders fraud through procedural finality. This is not policy failure. It is design functioning as intended.

I. A Code Permanently Under Repair—And Permanently Broken

Amendment as Admission of Failure

Since its enactment, the IBC has been subjected to continuous, piecemeal amendments, each marketed as a corrective but cumulatively producing doctrinal incoherence and institutional confusion. These amendments do not arise from a consistent jurisprudential vision; they are reactive, ad hoc, and often contradictory—designed to plug visible leaks without addressing foundational flaws.

By 2025, amendments and proposed bills had begun redefining core concepts such as “security interest”, effectively stripping statutory creditors—tax authorities, provident fund bodies, municipal corporations, environmental regulators—of secured status. This relegation pushes public-interest claims down the recovery waterfall, weakening long-standing legal protections for workers, retirees, and civic institutions, while privileging financial creditors and resolution applicants. These changes, reported critically in The Sunday Guardian, reflect not reform but re-engineering of priorities in favour of concentrated financial power.

The result is a statute that is heavily amended yet never fundamentally rebalanced—a patchwork law whose internal logic collapses under its own revisions.

II. The Myth Of Time-Bound Resolution

Timelines as Legal Fiction

The IBC’s ideological cornerstone—the promise of time-bound resolution—has collapsed in practice. The original 180-day deadline (extendable to 330 days) exists largely on paper. Tribunal data consistently shows that average Corporate Insolvency Resolution Process (CIRP) durations exceed statutory limits by a factor of two or more, with many cases dragging on for 700+ days.

As reported by Moneylife and acknowledged by the Parliamentary Standing Committee on Finance, procedural ambiguity, judicial vacancies, and endless litigation have hollowed out the Code’s temporal discipline. These delays are not incidental; they systematically erode enterprise value, depress recoveries, and incentivise liquidation over resolution—often after assets have been stripped and litigated into worthlessness.

By 2025, 77% of cases breached the 270-day limit, rendering the Code’s timelines performative rather than enforceable.

III. Recoveries That Mock The Promise Of Value Maximisation

Haircuts as the Norm, Not the Exception

Despite nearly a decade of operation and repeated amendments, recovery rates under the IBC remain dismal and volatile:

- As of September 2025, recoveries from successful resolution plans averaged ~32% of admitted claims, implying 68% haircuts as the norm (Mint).

- In several recent quarters, recoveries fell to ~25%, underscoring structural fragility (Financial Express).

- Overall realizations have declined from ~43% in 2019 to today’s depths, despite official claims of improvement.

The regime’s favourite success metric—recoveries as a percentage of liquidation value (often touted as 170%)—is a statistical sleight of hand, resting on manipulated and depressed valuations. This accounting alchemy obscures the reality: massive destruction of creditor value, particularly of public money.

IV. Avoidance Provisions: The Code’s Greatest Fraud

Fraud Recovery Designed to Fail

Sections 43–51 and 66–67 of the IBC—meant to claw back preferential, undervalued, and fraudulent transactions—are the Code’s most damning failure. In theory, they target pre-insolvency siphoning. In practice, they are rendered toothless by:

- Under-resourced and conflicted insolvency professionals

- Creditor committees obsessed with quick exits over forensic accountability

- Judicial deference that treats fraud recovery as collateral rather than central

Promoters routinely siphon thousands of crores into shell entities and family trusts pre-CIRP, then repurchase assets via proxies at fire-sale prices. Non-cooperation attracts no meaningful penalty. Avoidance claims are routinely parked, under-valued, or assigned notional ₹1 values, only to accrue exclusively to the successful resolution applicant post-approval.

Pending avoidance claims today rival total IBC recoveries, yet they are structurally excluded from benefiting victims or public creditors. Worse, IBC orders increasingly grant “clean chits” that invoke res judicata, stymieing parallel fraud investigations under RBI, ED, or PMLA frameworks.

V. Case Studies: This Is The Blueprint

The IBC’s outcomes are not aberrations; they are patterned results:

- Videocon Group: ₹60,000+ crore default resolved for ₹2,962 crore by Twin Star (Vedanta affiliate)—a 95–96% haircut.

- Aircel: ₹58,670 crore claims yielded ₹6,630 crore—89% wiped out, largely deferred.

- Essar Steel: ₹49,000 crore claims resolved at ₹42,000 crore—hailed as success only after Supreme Court intervention, masking prolonged value erosion.

- Bhushan Power & Steel: ₹19,700 crore JSW bid annulled by the Supreme Court in 2025 for fraud concealment—after years of creditor limbo, ending in liquidation.

- Reliance Communications (Anil Ambani): ~₹40,000 crore default, negligible recovery.

- Balajee Ingot India: 99% haircut proposal rejected under Section 65—an anomaly in an ocean of impunity.

- DHFL: ₹90,000+ crore fraud-tainted collapse; over 2.5 lakh FD and NCD holders—predominantly elderly, middle-class savers—expropriated. Resolved under IBC in 2021 by Piramal Group for ~₹34,250 crore, translating into massive haircuts for retail creditors, extinguishment of contractual rights, and effective wealth transfer from public savers to a crony corporate acquirer.

Despite documented diversion, forensic audit flags, and CBI-ED prosecutions, NCLT-NCLAT’s observations about dubious-opaque-expropriative resolution process and plan, retail victims were denied standing, hearings, and parity, rendering the process a jurisprudence of dispossession, not resolution.

Liquidations now outpace resolutions, especially in real estate, where haircuts routinely hit 80–90%. Forensic audits remain superficial, tribunals overwhelmed, and 2025 amendments—group insolvency, faster auctions—remain cosmetic.

Vi. The Political Economy: IBC And The BJP Funding Loop

This insolvency architecture dovetails seamlessly with India’s contemporary crony-capitalist order. Corporates absolved through IBC haircuts re-emerge as political donors, recycling windfalls into party coffers that then preserve the very loopholes that enriched them.

The BJP’s finances illustrate this symbiosis:

- Party funds ballooned from ₹780 crore (2014) to ₹9,000+ crore (2024).

- Cash reserves rose tenfold to ₹7,000 crore.

- Donations in 2024–25 surged to ₹6,088–6,654 crore, capturing ~85% of major party inflows.

- Trusts like Prudent channelled 75% of ₹2,720 crore (since 2013) to the BJP.

The quid pro quo is unmistakable:

- Tata Group: ₹758 crore donation post ₹44,000 crore semiconductor subsidies.

- Megha Engineering: Donations followed mega contracts like Zojila Tunnel.

- Vedanta (Anil Agarwal): Donations amid mining clearances, post-Videocon grab.

- Aditya Birla: ₹100 crore before Vodafone Idea bailout.

- Piramal Group: massive chunk donations to the BJP through electoral bonds, PM CARES and involvement in Flashnet scam in association with BJP Union Minister Piyush Goyal.

- Loss-making firms donating hundreds of crores.

- ED/IT-raided entities timing gifts suspiciously.

IBC haircuts free capital; donations buy protection; protection sustains the system.

VII. DHFL: The Perfect Crime Scene

For the 2.5 lakh+ victims of DHFL—mostly elderly FD and NCD holders—the IBC’s violence is not abstract. It is personal ruin.

DHFL was transferred to Ajay Piramal’s group for ₹37,250 crore (effectively ~₹34,250 crore) against ₹87,000 crore admitted claims. FD holders received 23% recovery—₹1,241 crore against ₹5,375 crore dues.

Promoters Kapil and Dheeraj Wadhawan allegedly siphoned billions pre-insolvency. Yet avoidance recoveries—estimated at ₹45,000–47,000 crore—were assigned a notional ₹1 value, accruing solely to Piramal post-approval. RBI and NHB safeguards were overridden. “Commercial wisdom” crushed equity.

The Supreme Court’s April 2025 ruling rubber-stamped this outcome, overturning NCLAT scrutiny even as the Wadhawans secured bail in parallel fraud cases.

VIII. Laundering Fraud, Terror Funding Taints, And Political Money

DHFL’s resolution also launders deeper criminal and political taints:

- ED probes since 2019 link the Wadhawans to Dawood Ibrahim’s network via Iqbal Mirchi, involving ₹2,200 crore in suspect transactions.

- Kapil Wadhawan’s 2020 arrest in the Mirchi PMLA case and ED attachments in Dubai remain unresolved.

- DHFL and associates allegedly donated ₹27.5 crore to BJP as per Cobrapost’s 2019 expose.

- RKW Developers (Wadhawan-linked) donated ₹10 crore.

- Piramal Group donated ₹85 crore via electoral bonds, amid the earlier Flashnet scandal involving a Piyush Goyal-linked firm acquired at a 1,000× premium for ₹48 crore.

The IBC thus functions as a legal laundering machine, cleansing financial crime into corporate respectability.

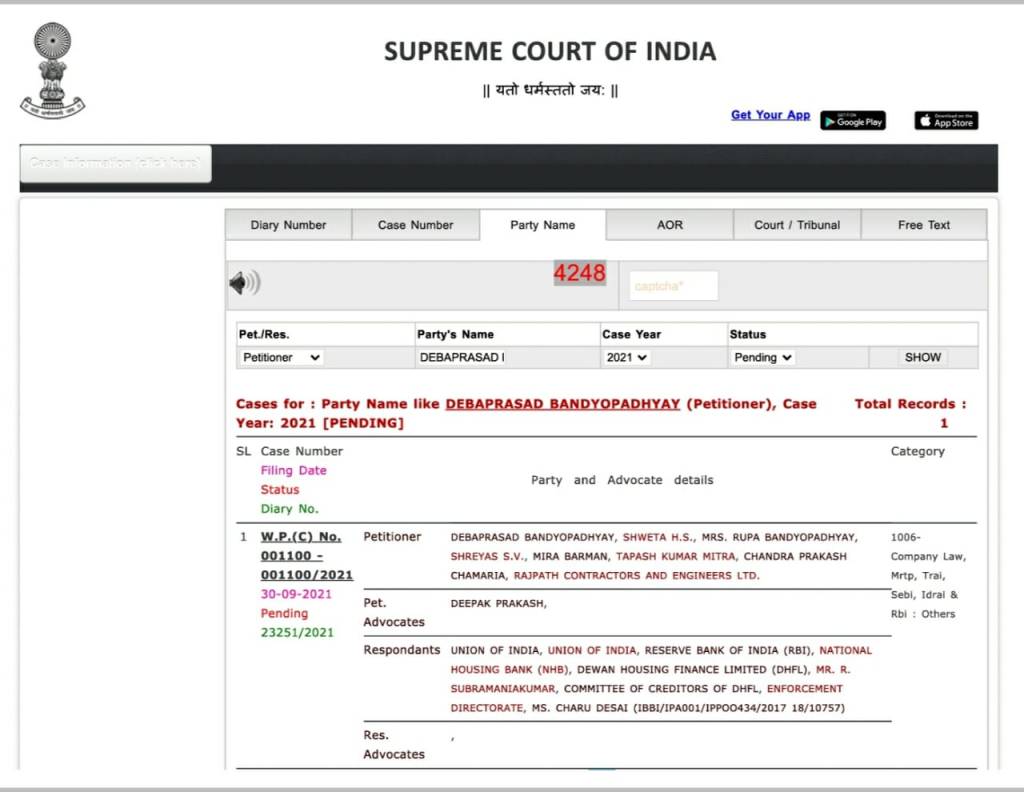

IX. Constitutional Challenge And Judicial Impunity

Recognising the IBC as the first premise of injustice, DHFL victims challenged its constitutional validity under Articles 14 and 21 via W.P.(C) No. 001100/2021 (Diary No. 23251/2021), filed on 30 September 2021 by multiple petitioners including Debaprasad Bandyopadhyay, represented by Advocate Deepak Prakash.

The petition was disposed of without explanation.

Not for lack of merit—but because justice in India is priced beyond victims’ means. In a system of tarikh pe tarikh, insolvency victims are exhausted into silence.

X. Conclusion: This Is Not Reform—It Is Rule By Plunder

The IBC is not a flawed statute in need of tweaks. It is a weaponised legal regime, structurally aligned with oligarchy, hostile to small creditors, and corrosive to constitutional equality.

Without dismantling its core premises—

- absolute deference to “commercial wisdom,”

- avoidance recoveries captured by acquirers,

- political funding loops, and

- judicial abdication—

the IBC will remain institutionalised expropriation masquerading as reform.

What India faces is not an insolvency crisis.

It is an insolvency regime that has gone rogue.

See More: The Avoidance Mechanism under India’s Insolvency Code: A System in Crisis VIEW HERE ⤡ (As reported on 24th December, 2025 ©Moneylife)

Video Courtesy: Ayush Vishwakarma (Source Video VIEW HERE⤡)

SEE ALSO:

This presentation is absolutely correct and based on facts/bitter truth. Dr. Debaprasad BandyopadhyayJi deserves many thanks for providing factual research based presentation.As long as ruling party at centre continues, this game of fooling innocent investors and favouring their beloved business tycoons will continue and I don’t see any improvement or corrective actions will be taken because they have started and continued extorting money from their beloved business tycoons against illegal favours and protection provided by them.

LikeLiked by 4 people