Posted on 14th June, 2024 (GMT 21:06 hrs)

Updated on 4th January, 2026 (GMT 05:25 hrs)

Compiled by Partyless Society⤡ & Occupy Dalal Street⤡

[SEE THE LATEST UPDATES TO THIS ARTICLE AS DONE ON 04-01-2026 BY SCROLLING DOWN]

ABSTRACT

The article advocates for the scrapping of the Insolvency and Bankruptcy Code (IBC) 2016, arguing it is flawed and detrimental to the Indian economy. Key points include:

- Ineffectiveness in Recovery: The IBC has failed to effectively recover bad debts, with a low recovery rate that falls short of expectations.

- Erosion of Value: The resolution process under IBC often leads to significant value erosion of the assets involved, harming creditors.

- Lengthy and Costly Process: The IBC process is criticized for being time-consuming and expensive, burdening businesses and the judiciary.

- Negative Impact on Credit Flow: The IBC has disrupted the credit flow to the economy, as banks become more risk-averse due to the possibility of lengthy insolvency proceedings.

- Encouragement of Crony Capitalism: The code has allegedly facilitated the takeover of valuable assets by a few entities at low prices, leading to concerns about crony capitalism.

The article concludes that the IBC should be scrapped in favor of a more effective and equitable system for resolving insolvency and bankruptcy issues.

#Scrap_IBC,

#Seize_Cronies_Fairplay_for_DHFL_Victims,

#Penalize_RSubramaniakumar_CharuDesai_from_DHFL_COC #Scrap_RBI_appointed_COC_for_DHFL,

#RBI_Appointed_CoC_for_DHFL_ReturnYourFees,

#alleged_dawood_mirchi_rkw_dhfl_bjp_collusion,

#Financial_Abuse_By_RBI_CoC_AjayPiramal,

#art_of_resistance_against_autocracy,

#ajay_piramal_alleged_insider_trader,

#Dear_Piramal_I_Wanna_be_Defamator,

#Ajay_Piramal_The_Environment_Terrorist,

#Occupy_Internet_to_Occupy_Cronies,

#Dear_Ajay_Piramal_I_wanna_be_arrested

I. Introduction

This compilation concentrates on a special act introduced by the Modi Sarkar 1.0, viz., the Insolvency and Bankruptcy Code (2016) or IBC, 2016, a brainchild of the then Finance Minister, Mr. Arun Jaitley. Here, in this article, we are going to discuss the drawbacks, flaws, setbacks and amendments of this Code by analyzing its eight-year long history. The authors of this compilation or collage will try to understand the sufferers’ painstaking existence due to the elusive implementation of the said Code.

India had numerous acts before the advent of the IBC, which are similar in character, all of which were aimed to punish the defaulters. Those acts include: the Indian Contract Act, the Recovery of debts due to Banks and Financial Institution Act 1993, the Securitizations and Reconstruction of Financial Assets and Enforcement of Security Interest Act (SARFAESI), 2002, the Sick Industrial Companies (Special Provisions) Act, 1985 (SICA). (SOURCE: VIEW HERE ⤡)

A sceptic mind can question that why such ill-conceived code (to be discussed soon) was introduced despite the existence of such laws beforehand to protect the investors, creditors and debtors in the event of insolvency?

The following poster may be understood as a biased opinion of the authors. However, as always, prologue is written only after the analysis of any phenomenon or object of study is completed.

First things first, what is the chronology of this IBC, 2016? When was it conceived and brought forth as a bill and then turned into an act?

| DATE | EVENT |

| 22nd August, 2014 | The Ministry of Finance created the Bankruptcy Legislative Reforms Committee (BLRC). The committee was headed by T. K. Viswanathan, and tasked with drafting a new bankruptcy law. |

| 4th November, 2015 | The Committee submitted its report, which included a draft bill. A modified version of the draft bill, after the incorporation of public comments, was introduced in the Sixteenth Lok Sabha by Finance Minister Arun Jaitley as the Insolvency and Bankruptcy Code, 2015. |

| 23rd December, 2015 | The bill was tabled. A Joint Parliamentary Committee on the Insolvency and Bankruptcy Code, 2015 (JPC) was set up and the bill was referred to it for detailed analysis. |

| 28th April, 2016 | The JPC submitted its report, which included a new draft of the Bill. |

| 5th May, 2016 | It was passed by the Lok Sabha. |

| 11th May, 2016 | It was passed by the Rajya Sabha. |

| 28th May, 2016 | It received assent from President Pranab Mukherjee and was notified in The Gazette of India. IBC thus became an Act. |

After going through the above timeline, it must be noted that the then Finance Minister Mr. Arun Jaitley glorified the IBC in 2018 as well, posing it as a full-proof, flawless, zero error code to ensure smooth insolvency proceedings and quick resolutions in the long term by providing holistic benefits to all the lenders, creditors, debtors etc.:

Reading the claims made by Mr. Jaitley in the above speech, one has to look beneath the surface-level announcements in order to understand the character of the IBC, 2016. For this purpose, the following sections are being laid out.

II. Bill Passed (Away) Without Dialogue

Despite the fact that the IBC apparently underwent the procedure from being a bill to being an act across two long years, the other bills and acts proposed during the periods of Modi sarkar 1.0 as well as 2.0 did not follow the proper lengthy procedure, which is enriched by discussions, questions/counter-questions, debates etc., by Opposition Parties as well as Parliamentary Committees (if formed). As was observed throughout Modi 2.0, all dissenting voices were suppressed or suspended from the Parliament and bills were passed immediately upon their introduction without the indispensable, constitutionally-necessary “question hour”.

Bills getting passed without debate, Parliament to soon become rubber stamp: Former Madras HC judge VIEW HERE ⤡ (As reported on 6th December, 2021 ©The Economic Times)

Amid suspension of Opposition MPs, Parliament passes key Bills without debate VIEW HERE ⤡ (As reported on 18th December, 2023 ©Deccan Herald)

Purge being executed so that draconian bills passed without debate: Cong VIEW HERE ⤡ (As reported on 19th December, 2023 ©Business Standard)

This was reflected in former CJI N. V. Ramana’s comment during the first three years of Modi 2.0:

‘Sorry state of affairs’: CJI N V Ramana on lack of debate in Parliament VIEW HERE ⤡ (As reported on 15th August, 2021 ©The Economic Times)

Now, all the Indian citizens understand that no majoritarian, autocratic system can sustain without discursive dialogue or inputs from pluralistic federal units. It is strange enough to note that the forming of IBC took almost two years to be implemented. Despite this fact, it has cut a sorry figure in meeting its feigned promises. It is also to be noted that within this period, the then ruling party of India allowed 50+ superrich wilful defaulters to fly away from the country without meeting their loan obligations.

After the upsetting results on 4th June, 2024 for the BJP, the RSS (the father organization of the BJP) curiously attacked the BJP’s “over-confidence” and “arrogance” as well as emphasized on the need for plural and diverse voices:

Mohan Bhagwat’s Speech Confirms That RSS’ ‘Open Licence’ to Modi is Under Review VIEW HERE ⤡ (As reported on 14th June, 2024 ©Quint)

Modi 3.0: Why BJP must embrace Mohan Bhagwat’s message for unity and inclusive governance VIEW HERE ⤡ (As reported on 14th June, 2024 ©Firstpost)

Senior RSS leader attacks BJP on Lok Sabha election results: ‘Those who became arrogant…’ VIEW HERE ⤡ (As reported on 14th June, 2024 ©Business Today)

However, it is too late to pronounce such syncretic statement as almost one progeny has already been destroyed by the misruling of the RSS-BJP collusion. This brings us to the contingencies involved in the framing of the IBC by the Modi 1.0 and 2.0, including the 35+ amendments that the Code saw within the period of 2016-2024.

III. Amendments of the IBC (2016): An Overview

If anyone considers the IBC as an omniscient, omnipresent and omnipotent law introduced under the leadership of a self-proclaimed non-biological messianic prophet or avataar, why are there so many amendments within the span of 7-8 years? Let us look through some of the major amendments thus introduced, which prove the fluid, uncertain and confused state of the Code:

“2017 Amendment prohibits certain persons from submitting a resolution plan in case of defaults. These include: (i) wilful defaulters, (ii) promoters or management of the company if it has an outstanding non-performing debt for over a year, and (iii) disqualified directors, among others. Further, it bars the sale of property of a defaulter to such persons during liquidation.” (Source: Wikipedia⤡)

The year 2018 also saw several amendments, e.g.:

- Homebuyers are now classified as financial creditors.

- Revisions to Section 29A, easing criteria for resolution applicants.

- Permitting withdrawal of ongoing Corporate Insolvency Resolution Process (CIRP) with 90% creditor approval.

- Lowering Committee of Creditors’ voting thresholds.

- Mandating special resolutions for companies initiating their own CIRP.

- Applying the Limitation Act to IBC cases.

SOURCE: Major Amendments introduced to the Insolvency and Bankruptcy Code VIEW HERE ⤡ (As reported on 20th July, 2018 ©AZB Partners)

Further, in the year 2020, the Insolvency Amendment Act was notified on 13th March 2020, with a retrospective effect, being in force with effect from 28 December 2019 and bringing about significant changes to various sections of the Code:

- Raising the default threshold for initiating Corporate Insolvency Resolution Process (CIRP) from INR 1 lakh to INR 1 crore.

- Expanding definitions and clarifying roles in sections 5, 7, 11, 14, 16, 21, 23, and 29A.

- Introducing Section 32A, protecting new management from prior offenses.

- Enacting Section 10A, temporarily suspending CIRP initiation due to COVID-19.

- Adding Section 66(3), limiting fraudulent business claims during the CIRP suspension.

In the year 2021: “The Insolvency and Bankruptcy Code (Amendment) Act 2021 introduced a pre-packaged insolvency resolution process for micro, small, and medium-sized enterprises (MSMEs). The process allows for a shorter timeline of 120 days and enables MSMEs to work on resolution plans while remaining in possession of the company.” SOURCE: VIEW HERE ⤡

In the years 2023-2024, a number of crucial amendments were introduced, which are briefly summarized as follows:

Changes to the Insolvency Resolution Process:

- Mandatory Submission: The Committee of Creditors (CoC) must mandatorily submit a resolution plan within 330 days.

- Swift Process: Emphasis on the expedited resolution process, reducing delays and improving efficiency.

Role of the Committee of Creditors (CoC):

- Enhanced Powers: The CoC has been given greater control, including the ability to replace the interim resolution professional (IRP) with a new one.

- Recommendation Consideration: The CoC’s recommendations now hold significant weight in the decision-making process.

Debtor-In-Possession (DIP) Model:

- Introduction of DIP: A Debtor-In-Possession model is introduced, where the debtor continues to manage the business while undergoing insolvency proceedings, provided there is no fraudulent activity involved.

- CoC Supervision: Under the DIP model, the CoC supervises the debtor’s actions to protect creditors’ interests.

Streamlining Liquidation:

- Simplified Liquidation: Procedures for liquidation are simplified, including clear timelines and reduced procedural complexities.

- Liquidator’s Role: The liquidator’s responsibilities are clarified, with a focus on maximizing the value of the debtor’s assets for creditors.

Resolution Plan Approval:

- Quick Approvals: Resolution plans are to be approved more swiftly, ensuring that the insolvency process does not drag on unnecessarily.

- Transparency: The approval process emphasizes transparency and adherence to regulatory standards.

Enhanced Protection for Creditors:

- Secured Creditors: Enhanced provisions for secured creditors to ensure they receive fair treatment in the distribution of proceeds.

- Priority Payments: Priority of payments in the resolution process is clearly defined, giving creditors better insight into their expected recoveries.

Technological Integration:

- Digital Processes: Adoption of digital platforms and technologies to streamline filing, monitoring, and reporting within the insolvency framework.

- Efficiency Gains: Aimed at increasing efficiency and reducing administrative burdens.

Revised Compliance and Reporting Standards:

- Stricter Compliance: More stringent compliance requirements for insolvency professionals and entities involved in the process.

- Regular Reporting: Enhanced reporting obligations to improve oversight and accountability.

SOURCES: Insolvency and Bankruptcy Code (Amendment) Act, 2023 VIEW HERE ⤡ (As reported on 11th October, 2023 ©FreeLaw)

Important Amendments Under IBC: 2023 & 2024 – Volume III VIEW HERE ⤡

We can see that the IBC has always remained a subject of modifications and revisions over the course of eight years. This proves that the IBC at the moment of its conception was far from being the exhaustive, unstained, non-contaminated ideal that Mr. Jaitley had claimed multiple times. The compilers have suffered as well as struggled enough in the information age (in the context of speed capitalism) while bringing together these different amendments in one place, since the amendments have often argued about the same issues again and again from different vantage points and are also quite a many in number.

The issue of amendments of IBC leads us to the consideration of its flaws, setbacks, shortcomings and imperfections that caused these amendments to be issued in the first place.

IV. Drawbacks/Flaws of the IBC (2016)

Given below are some of the overt problematic areas of the IBC, compiled from different authentic sources. Let us start with Mrs. Sucheta Dalal’s take on the IBC’s present status as representing the rotten core of the Indian economy:

It would now be worthwhile to bring into attention the key negative issues with the IBC:

- Limited Judicial Bench Strength: The National Company Law Tribunal (NCLT) and National Company Law Appellate Tribunal (NCLAT) are understaffed, leading to delays in case resolutions. This shortage exacerbates the backlog and extends the time taken to resolve insolvency cases.

- Operational Delays: Procedural delays in the resolution process, partly due to insufficient infrastructure and manpower, affect the timely resolution of cases, which is critical for the effectiveness of the IBC.

- Unpredictability in Outcomes: Inconsistencies in judicial decisions create uncertainty, impacting stakeholders’ confidence and the predictability of the insolvency resolution process.

- Low Recovery Rates: The recovery rates under the IBC are relatively low compared to global standards, questioning the effectiveness of the process in terms of value maximization for creditors.

- Haircuts for Financial Creditors: Significant reductions (haircuts) in the value recovered by financial creditors have been a concern, affecting the willingness of financial institutions to participate in the resolution process.

- Resolution Plans and Bidding Process: Issues related to the submission and approval of resolution plans, including concerns about transparency and fairness in the bidding process, have been highlighted.

SOURCE: Concerns over Insolvency and Bankruptcy Code, 2016 VIEW HERE ⤡ (As reported on 11th January, 2014 ©Drishti IAS)

Moreover, certain other shortcomings are also worth noticing:

- Inadequate Safeguards: Lack of protections for company rights before management handover.

- Overreliance on Creditors: Excessive dependence on creditors’ decisions.

- Limited Representation: No provision for corporate debtor representation.

- Professional Criteria: Insufficient criteria for insolvency professionals.

- Information Access: Unrestricted access to sensitive information.

- Resolution Definition: Ambiguity in defining resolution applicants.

- Liquidation Default: Automatic liquidation if no consensus is reached.

- No Withdrawal: Prohibition on application withdrawal post-admission.

SOURCE: Flaws in IBC VIEW HERE ⤡ (As reported on 12th August, 2017 ©Shankar IAS Parliament)

Even so, the following setbacks remain as of now:

“The IBC aimed to enforce judicial discipline by introducing strict timelines for insolvency resolution processes. However, the average time taken for corporate insolvency resolution processes (CIRPs) has exceeded the stipulated timeline of 330 days, resulting in delays and erosion of value for creditors. The disruptions caused by the COVID-19 pandemic further exacerbated these delays. Additionally, a significant number of CIRPs have resulted in liquidation rather than resolution plans, indicating challenges in achieving successful outcomes. Despite challenges, the government and the Insolvency and Bankruptcy Board of India (IBBI) have proactively responded to issues by amending the legislation and regulations. The IBC has undergone frequent amendments to address various challenges, although some amendments have led to confusion.”

SOURCE: Understanding India’s Insolvency and Bankruptcy Code: Challenges and Opportunities VIEW HERE ⤡

The following source highlights the sorry states of affairs of the IBC, 2016:

SOURCE: Anything that can go wrong may have gone wrong with IBC VIEW HERE ⤡ (As reported on 15th February, 2024 ©Fortune India)

The “hits and misses” of the supposedly “all-powerful” IBC can be viewed clearly below, since people mark when they hit but they do not mark when they miss:

SOURCE: India’s Insolvency and Bankruptcy Code is not working; here’s what’s going on VIEW HERE ⤡ (As reported on 6th August, 2023 ©Business Today)

The following links may be visited for eliciting further details to this end:

IBC report card: It’s win some, lose some for the bankruptcy law VIEW HERE ⤡ (As reported on 28th June, 2022 ©The Federal)

IBC turns 5: Hits and misses of the Insolvency and Bankruptcy Code VIEW HERE ⤡ (As reported on 20th August, 2021 ©The Economic Times)

This type of ambivalent attitude of the lawmakers makes the common people miserable, whilst their docile bodies are subjected, subjectified and objectified through such harsh (as well as fluctuating) mechanisms of law!

The spokesperson in the above video has implicatively pointed out the following three sections of the IBC (Section 12A, Section 29A and Section 53) that are incommensurable with the constitutional values of the Republic of India; this hampers the Fundamental Rights, especially Article 14 of the Indian Constitution, which states: “The State shall not deny to any person equality before the law or the equal protection of the laws within the territory of India.” (Some petitioners in the DHFL case⤡⤡ are spreading a rumour that only petitioners will get back their invested amount. This is in contravention to the Article 14).

Let us view the summary of each of the aforementioned sections that function in favour of the superrich crony business tycoons at the cost of the small depositors:

Section 12A of the IBC allows for the withdrawal of an insolvency application that has been admitted under sections 7, 9, or 10. This withdrawal can occur if the applicant requests it and receives approval from 90% of the voting share of the Committee of Creditors (CoC). This provision was introduced to supposedly/presumably provide flexibility in the insolvency process, enabling parties to settle disputes and avoid prolonged proceedings.

Section 29A of the IBC, which outlines the criteria that disqualify certain individuals and entities from being resolution applicants. These include undischarged insolvents, wilful defaulters, those convicted of an offense punishable with imprisonment of two years or more, and related parties of such individuals or entities. The purpose is to ensure that only credible and financially sound applicants can participate in the insolvency resolution process.

Section 53 of the IBC details the distribution of assets during liquidation. It prioritizes payments to secured creditors and workmen’s dues, followed by unsecured creditors, government dues, and other debts. This is done to supposedly/presumably ensure a systematic and fair distribution of the debtor’s assets to satisfy given claims.

Moreover, the issue of Section 32A of the IBC remains. This was specially observed in the infamous DHFL Scam, in which the following took place:

Before going into that: can you remember Ratnākara’s trajectory from a dacoit to a saint, viz., Rsi Valmiki? When Ratnākara looted others’ private and personal properties, Narada Muni pointed him out that these are sinful acts (papa) and are not to be performed/committed (though, according to anarchist interpretation: property is in-itself a theft) and requested Ratnākara to share the surplus burden of sin with his family members. However, the family members of Ratnākara refused to take that burden, though they were nurtured by the tiresome labour-products of his loots.

Mr. Ajay Piramal, after allegedly “owning” the Dewan Housing Finance Corporation Limited (DHFL), refused to take the burden of so-called “prior offences” by alluding to the Section 32A (2019 amendment) of the IBC (2016), which states:

“[32A. Liability for prior offences, etc.–(1) Notwithstanding anything to the contrary contained in this Code or any other law for the time being in force, the liability of a corporate debtor for an offence committed prior to the commencement of the corporate insolvency resolution process shall cease, and the corporate debtor shall not be prosecuted for such an offence from the date the resolution plan has been approved by the Adjudicating Authority under section 31…”

In other words, the PCHFL aka Piramal Finance that allegedly “acquired” the DHFL argued by citing the Section 32A that the said legal provision prohibits the existence of an FIR and the criminal proceeding arising out of it against the new management, after the “successful completion” of the corporate insolvency resolution process (CIRP). Hence, sins are not to be “carried forward”!

SC notice to CBI on Piramal Capital & Housing Finance plea to quash FIR VIEW HERE ⤡ (As reported on 26th February, 2023 ©Business Standard)

Mr. Ajay Piramal can never be a “Saint” Vālmiki. Instead of singing out “mā niṣada pratiṣṭham tvamagamahaḥ” by seeing the DHFL victims suffer a “capital” punishment after undergoing massive haircuts under the IBC, he is actually playing the role of niṣāda or the hunter, the one who killed two innocent birds engaged in loving intimacy. Nevertheless, he has forgotten the burden of his past deeds.

Moreover, Mr. Piramal has forgotten all about the Section 66 of the IBC that provides for the benefit of all the creditors in the recovery of avoidance transactions. He has financially abused the DHFL victims by looting their life-savings with the help of the then ruling party, i.e., the BJP.

Without any liability, he “bought” (?) an AAA rated, 45k crore worth company by paying only a rupee after five contradictory (seemingly simulated) bidding wars between three final bidders!

This is an adverse possession of a solvent, ongoing concern. Without putting in much labour (and zero amount of socially necessary labour!), one can “buy” a company with an entire infrastructure along with all the employees without bothering about the legality of the affairs!

However, the Hon’ble Supreme Court of India had earlier pointed out:

Bankruptcy will not void personal guarantees: Hon’ble Supreme Court VIEW HERE ⤡ (As reported on May 22, 2021 ©The Times of India)

In other words, the old promoters’ rights in the occasion of a “bankruptcy” or “insolvency” shall not be extinguished but are to be upheld as a continuation.

The SCI is still maintaining such a stance with regard to the old promoters’ rights, in so far as there are still no “escape routes” for the “new owner” of a company without reconsidering the old promoter’s appeals in response to the initiation of the corporate insolvency resolution process (CIRP).

Anil Ambani, Dhoot, Biyani may face heat after SC ruling on personal guarantors VIEW HERE ⤡ (As reported on 16th November, 2023 ©ET BFSI)

SC denial of IBC relief to personal guarantors opens new recovery window for lenders VIEW HERE ⤡ (As reported on 13th November, 2023 ©Economic Times)

Supreme Court Upholds Constitutionality Of IBC Provisions Relating To Personal Guarantors; Says Adjudicatory Role Can’t Be Read Into Sec 97 VIEW HERE ⤡ (As reported on 9th November, 2023 ©LiveLaw)

The above flaws comprehend the fact how the multiple-times amended sections/provisions/portions of the IBC are often in conflict, e.g., one section preserves the rights of all stakeholders (Section 66(1)) in the long run while another provides way to the profiteering benefits of the “new” owner after the CIRP (Section 32A). How to reconcile all these conflicting issues then? Not only that, many such provisions of the IBC also enter into contradictions with the RBI Act, NHB Act and Company Act. Even the public servants have made mistakes in the course of IBC-run insolvency process and those have been pointed out by the NCLT and NCLAT. The CoC’s decision stood still as in the case of DHFL due to the challenging verdicts or orders of such adjudicating authorities.

See the following timeline to see how the various tiers of these adjudicating authorities often contradict themselves in the interpretation of the IBC-sanctioned CIRP, as was observed again and again in the DHFL case:

| 19.05.2021 | The NCLT ordered the CoC to reconsider DHFL’s erstwhile promoter Wadhawan’s offer of 100% repayment within 10 days. NCLT order on the DHFL-case ⤡ [IA 2431 of 2020 in CP (IB) 4258/MB/C-II/2019 Under Section 60 (5), 227 (2), 239 of the Insolvency and Bankruptcy Code, 2016] points 16-19 and 84-89. |

| 25.05.2021 | NCLAT set aside NCLT’s order after the Union Bank of India and Ajay Piramal approached the NCLAT with an urgent petition. The CoC did not even bother to answer the NCLT. HOW DID MR. AJAY PIRAMAL GET SUCH JUDICIAL PRIVILEGE IN NCLAT, GIVEN THE NUMBER OF PENDING CASES IN THE INDIAN COURTS? Piramal is more equal than the other 98%!VIEW HERE ⤡ |

| 07.06.2021 | NCLT is forced to approve the resolution plan in favour of the Piramals. |

| September 2021 | Mr. Ajay Piramal started disbursing merely 23% of the total FD amount to the respective FD Holders of DHFL, the rest of the amount going for a major haircut. Financial deprivation (curtailment of business-related human rights due to financial abuse) of thousands of FD and NCD Holders is apparent. |

| 27.01.2022 | Following the case filed by 63 Moons Technologies (the case questioned the deal of Piramal’s resolution plan, wherein the approx. 45k crore worth of assets were bought by paying only a rupee. 63 Moons cited the Section 66 of the IBC, which provides for the benefit of all the creditors of the insolvent company) the NCLAT passed an order that declared the illegality of the DHFL CoC, its conduct and the allocation of the resolution amount as well. NCLAT asks CoC to consider 63 moons’ plea in DHFL Resolution Plan VIEW HERE ⤡ (As reported on 27th January, 2022 ©The Times of India) |

| 01.03.2022 | Piramal approached the Supreme Court, challenging the NCLAT Second Order. |

| 11.04.2022 | The Supreme Court stayed the NCLAT Order. Despite the fact that the case is under adjudication or sub judice, Piramal CHF acquired DHFL by using dubious company names: Piramal CHF and Piramal Finance. |

This further reflects the IBC’s lack of clarity in guiding any resolution process, since it enables the chosen few mercilessly.

One of the OBMA founder-members had tried to challenged the legitimacy of the IBC at the Supreme Court of India in connection with the DHFL Scam in 2021-22. However, the same was dismissed after being listed chiefly for two reasons:

The case could not be continued:

a) Crunch of money in the expensive realm of the Indian judiciary;

b) Due to some black-sheep within the group installed by the opponents.

Black Sheep: The Adversaries of the DHFL Victims’ Movement VIEW HERE ⤡

V. Conclusion: Scrap IBC!

In conclusion, it is transparent that the IBC is a product of anti-people collusion of crony, savage, cannibal capitalists with the underworld and the ruling party. In the context of such an Orwellian dystopia, we are facing a peculiar word “non-performing assets” (NPA), a doublespeak, or an instance of uncontradictory contradictory since if “X” is non-performing, how can it be considered an “asset” per se? This type of doublespeak or Newspeak of Oceania reveals the ambiguous, tautologous and contradictory nature of the IBC. Even the 45k crore=1 rupee equation in the DHFL case was such a curious case made possible by the very paradoxical character of the IBC.

It is as much a case of failure as the farmers’ bills, electoral bonds scheme, demonetization, PMLA, Article 370 abrogation, GST etc., all of which were either thoroughly questioned, challenged or simply scrapped in the face of public agitation, movement or civil disobedience, or merely in the course of the concerned law/policy’s implementation. In a similar way, the IBC needs to be challenged, its key provisions that favour the profiting-motives of a few corporate tycoons must be changed to stand in defence of the small investors and/or depositors.

In fact,

Centre likely to review IBC Bill only after 2024 general elections VIEW HERE ⤡ (As reported on 19th December, 2023 ©Business Standard)

Especially after:

Madras High Court Urges Parliament To Assess Efficiency Of IBC And Consider Recovery Percentage From Successful Resolution Processes VIEW HERE ⤡ (As reported on 9th June, 2024 ©LiveLaw)

In this connection, noted financial investigative journalist Mrs. Sucheta Dalal noted in a March 2024 article:

“Last month, the Madras High Court responded to a petition filed by a chartered accountant and insolvency professional (IP), V Venkata Siva Kumar, by seeking a response from the Union government to charges of corruption at the NCLT’s Chennai bench. Mr Siva Kumar, who appears in person, contends that the country has lost several lakh crores of rupees due to corrupt and collusive decisions. He has sought a ‘monitoring mechanism’ for the work of adjudicating officers, given that large sums of money are at stake in every case.

Even earlier, Mr Siva Kumar had alleged that a specific technical officer of the Chennai bench had assumed full authority over the adjudication process and would decide matters in favour of ‘the highest bidder’ with negotiations taking place in his chambers without any documentation of their interactions. He had alleged that petitions of select senior counsel were entertained while those of others, particularly juniors, were shouted down and silenced.

Mr Siva Kumar, who has been doggedly recording and highlighting instances of corruption at the NCLT and its appellate body for over two years, has made the ministries of corporate affairs, law and justice as well as the central vigilance commission as respondents.”

SOURCE: Courts Step Up as Legislative Amendments to IBC Remain Elusive VIEW HERE ⤡ (As reported on 1st March, 2024 ©Moneylife)

Even earlier in 2021-22, it was urged that:

Standing Committee on Finance raps IBC over unsustainable haircuts, says 13,000 cases worth Rs 9 lakh crore pending VIEW HERE ⤡ (As reported on August 03 2021, ©Moneycontrol)

IBC: Govt. working with RBI on CoC’s conduct VIEW HERE ⤡ (As reported on 27th August, 2021 ©The Hindu, PTI)

Impossible to accept 95% haircuts for banks under IBC: Sitharaman VIEW HERE ⤡ (As reported on 1st October, 2022 ©The Hindu)

Is IBC a mechanism to rescue stressed firms or another tool for ‘organised loot’, asks Congress VIEW HERE ⤡ (As reported on 2nd June, 2023 ©The Hindu)

Now, for the last words of this lengthy but substantially enriched post.

An Appeal to the DHFL Victims

Dear DHFL Victims,

After going through this entire collage by deploying your sravana, manana and nididhyasana (listening-internalizing-deeply contemplating), we have a few things to say to you on which you must reflect upon.

We, the DHFL victims, the helpless small depositors of the first NBFC to enter the problematic zone of the IBC, are now standing in front (or inside? The demarcating fine line has been obliterated) of the huge gates of the Arun Jaitley Stadium, refurnished and refurbished using tax-payers’ money to suit the BJP’s dirty politics of spectacle. The stadium appears to our sufferers’ gaze as the huge metaphorical experimenting lab of the then Finance Minister, as part of a crony machinery that has never cared about our miseries.

Oh Victims. Don’t submit yourself to the tyrannical hands of these brutes: the few superrich blood-suckers, who treat you like sacrificial fodder, turn you into petty guinea pigs and render your existential value insignificant!

By this time, it has become clear to all of us that the RBI-appointed CoC has killed us by taking away our alms arms and turning them against our legitimate concerns and interests.

Your hard-earned money has been subsumed and utilized to sue you by manipulating all the administrative, judicial and bureaucratic apparatuses. A sum of Rs. 100 Cr has been allotted to the Resolution Professionals to defend themselves against the cases we lodge.

To resist this reign of merciless state-corporate abuse, turn the present struggle into a non-violent civil disobedience movement either physically or as a digital-nomad or as a keyboard warrior. Don’t be discouraged by some of the illusory “fellow” victims of the DHFL, who are trying to disband the collective strength of the movement by installing agents from time and again.

The DHFL scam is a political matter, and must be dealt with in terms of a politically conscious war at all fronts, from all sides – through an all-out attack, following the tactics of Total Football.

You are not alone. You have the Constitution of India by your side, and also the International Human Rights’ provisions. You have nothing more to lose in this battle. So, don’t be apathetic. It is not the time to lose hope. Our identified enemies, BJP and Co., are facing a huge legitimation crisis after the declaration of the Lok Sabha Election results. They are at their weakest point now. We must strike the blow whilst the iron is still hot. It is high time we do that without any hesitation, without any excuse. We have all the weapons at our disposal to fight back against the Goliath of fascist politicians and chosen ones of the corporate world.

UPDATE (04-01-2026):

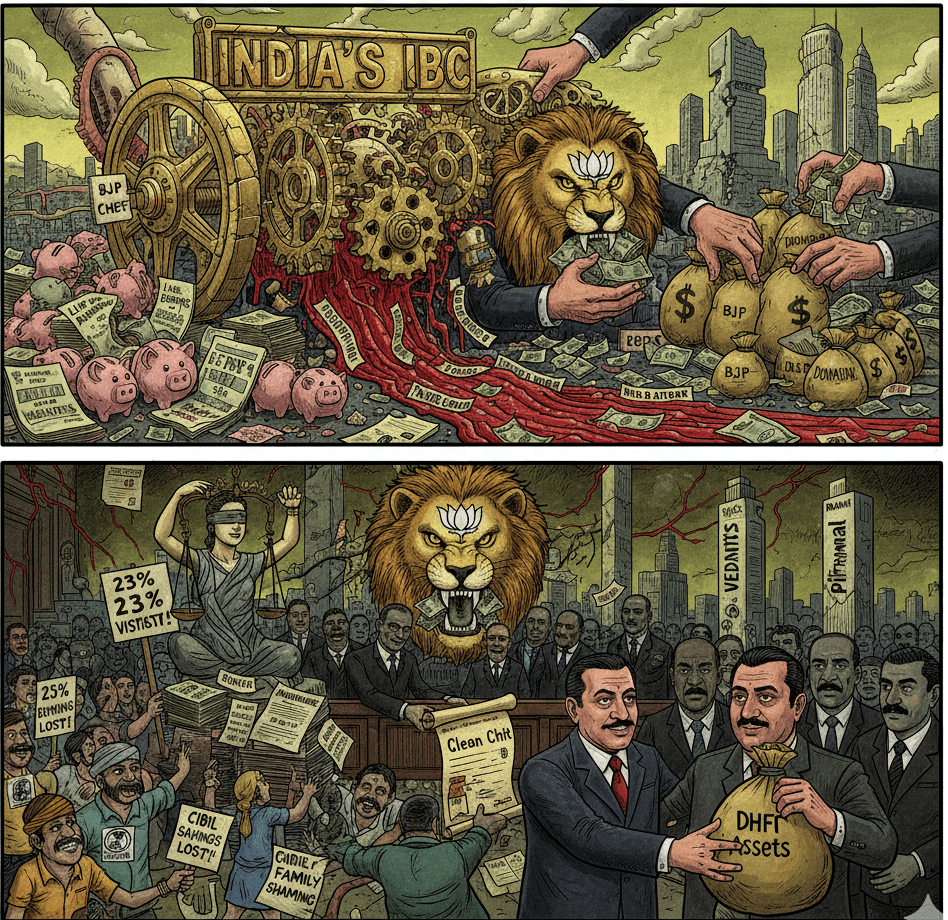

Crony Bankruptcy Bonanza: How India’s IBC Turns Tycoon Defaults into BJP’s Billion-Rupee War Chest

India’s Insolvency and Bankruptcy Code (IBC) stands as a grotesque parody of financial reform, a labyrinthine scam masquerading as a resolution framework that systematically plunders public coffers while coddling billionaire defaulters and their political enablers. Enacted in 2016 with fanfare as a tool to cleanse corporate debt rot, the IBC has devolved into a predatory machine that enforces draconian timelines in theory but delivers endless delays, paltry recoveries, and obscene haircuts in practice—ensuring that banks, predominantly public-sector behemoths laden with taxpayer money, absorb trillions in losses. Creditors limp away with a meager 32-33% recovery rate on admitted claims as of September 2025, translating to haircuts of 67-68% on average, a figure that has stubbornly stagnated despite nine years of supposed tweaks. This isn’t inefficiency; it’s engineered sabotage, where the system’s architects and beneficiaries—often one and the same—profit from the chaos.

Layered atop this foundational failure are the avoidance provisions (Sections 43-51 and 66-67), billed as safeguards against fraudulent asset stripping but rendered impotent by regulatory capture and judicial inertia. Insolvency professionals, starved of resources and beholden to creditor committees fixated on quick exits rather than forensic justice, routinely overlook or under-pursue preferential transfers, undervalued deals, and extortionate credits. Promoters like Venugopal Dhoot of Videocon or the Ruias of Essar siphon billions to shell entities or family trusts pre-insolvency, only to reclaim assets through proxies at bargain-basement prices. Non-cooperation flourishes unchecked, with penalties as rare as genuine accountability. Judicial rulings exacerbate the farce: recoveries are siloed to creditors, barring third-party pursuits, while clashes with RBI fraud guidelines grant defaulters “clean chits” via res judicata, shielding them from parallel probes. The result? Pending avoidance claims balloon to levels rivaling total recoveries, while asset values erode amid delays—77% of cases now exceed the 270-day statutory limit, with averages ballooning beyond 700 days, allowing litigation warfare to hollow out companies before resolutions even materialize.

This systemic rot manifests in scandalous case studies that scream cronyism. Take Videocon Group under Venugopal Dhoot: saddled with over ₹60,000 crore in debts, it settled for a derisory ₹2,962 crore via Twin Star Technologies—a Vedanta arm tied to Anil Agarwal—inflicting a 95-96% haircut on lenders, though appeals offered fleeting resistance. Aircel, promoted by the Maxis family, defaulted on ₹58,670 crore, yielding just ₹6,630 crore under UV Asset Reconstruction, an 89% haircut with payouts dribbled over years. Essar Steel’s saga, helmed by the Ruia brothers, saw ArcelorMittal (led by Lakshmi Mittal) acquire it for ₹42,000 crore against ₹49,000 crore claims—a “success” story masking deeper value destruction and Supreme Court interventions. Bhushan Power and Steel, under Sanjay Singal, had its ₹19,700 crore JSW Steel bid (against ₹47,000 crore dues) torpedoed by the Supreme Court in 2025 for blatant fraud concealment, forcing liquidation after years of creditor bleeding. Even smaller horrors like Balajee Ingot India, with a proposed 99% haircut, saw the NCLT reject the plan as malicious, invoking Section 65 for penalties—yet such rebukes are outliers in a sea of impunity.

These aren’t aberrations but the IBC’s DNA: a framework that coerces banks into fractional settlements to “clean” balance sheets, while defaulters like Anil Ambani (Reliance Communications, ₹40,000 crore default, minimal recovery) or Vijay Mallya (though pre-IBC) embody the elite’s escape velocity. Forensic audits are perfunctory, tribunals overburdened, and amendments—heralded in 2025 for faster auctions and group resolutions—prove cosmetic, failing to stem the tide of liquidations (outpacing resolutions in many quarters) or address real estate’s quagmire, where unfinished projects yield even steeper 80-90% haircuts. The IBC’s “success” metric—170% of liquidation value—rings hollow when fair values are manipulated downward, and overall realizations have plummeted from 43% in 2019 to today’s abysmal lows.

This financial alchemy fuses seamlessly with the Bharatiya Janata Party’s (BJP) brazen crony capitalism, a symbiotic racket where absolved corporates funnel windfalls into party treasuries, perpetuating the loopholes that birthed them. The BJP’s wealth has metastasized: from ₹780 crore in total value in 2014 to over ₹9,000 crore by 2024, with fixed assets ballooning from ₹84 crore to ₹1,200 crore (plus ₹400 crore in projects), and cash reserves exploding tenfold to ₹7,000 crore. Donations, the regime’s oxygen, surged to ₹6,088-6,654 crore in 2024-25 alone—a 50-68% leap from ₹3,967 crore in 2023-24—capturing 85% of all major party contributions, dwarfing rivals like Congress (₹522 crore). This isn’t organic support; it’s quid pro quo extortion, with electoral trusts like Prudent (funneling 75% of its ₹2,720 crore corpus to BJP since 2013) laundering corporate largesse.

Stark examples abound: Tata Group, under Ratan Tata’s legacy, pocketed ₹44,000-44,200 crore in semiconductor subsidies for Gujarat and Assam plants, then routed ₹758 crore to BJP via trusts in April 2024—mere weeks later. Megha Engineering (P.P. Reddy), a top donor with ₹966 crore via bonds historically, secured massive infra contracts post-donations, including Zojila Tunnel and Polavaram. Vedanta’s Anil Agarwal, fresh from Videocon’s asset grab, donated millions amid mining clearances. Aditya Birla Group (Kumar Mangalam Birla) gave ₹100 crore two months before Vodafone Idea’s bailout. DLF (K.P. Singh) donated ₹170 crore, earning a clean chit in the Vadra land deal. Murugappa Group funneled ₹125 crore post-semiconductor approval. Even loss-making firms—33 donated ₹582 crore via bonds, 75% to BJP—reek of laundering, with suspects like those under ED/IT raids (e.g., NATCO Pharma, Heremba Renewables) timing contributions suspiciously.

Northeastern contractors epitomize the graft: Over 50-80% of BJP’s regional donations from FY23-24 traced to firms landing government contracts in Assam, Arunachal, and Tripura, where the party holds sway. This vicious cycle—IBC write-offs freeing capital for donations, which buy policy favours sustaining the system—squanders billions on propaganda (₹1,700 crore on 2024 elections, ₹500 crore to media) while starving public goods like schools and hospitals.

The ultimate obscenity? Hypocrisy in enforcement. Tycoons negotiate trillion-rupee escapes, but small borrowers—farmers, MSMEs—face goon squads, family shaming, and eternal CIBIL scars for paltry defaults. Regulators like IBBI and NCLT, selectively aggressive toward outsiders yet deferential to insiders, fail to harmonize with fraud laws, ensuring no deterrence. This isn’t a flawed code; it’s a weaponized oligarchy, institutionalizing inequality, eroding trust, and burdening the masses with elite excesses. Without torching this edifice—imposing 100% promoter bans, mandating 50% minimum recoveries, severing donation-favor ties via public funding—the IBC remains a tool of entrenched tyranny, dooming India to perpetual crisis under the veil of “reform.”

For the expropriated victims of the Dewan Housing Finance Limited (DHFL) debacle—over 2.5 lakh fixed deposit (FD) and non-convertible debenture (NCD) holders, overwhelmingly elderly retirees and middle-class savers—the Insolvency and Bankruptcy Code (IBC) stands revealed not as a neutral mechanism of resolution, but as the foundational legal architecture of structural plunder in India. These citizens entrusted their life savings to what was once India’s second-largest housing finance company, only to watch them be erased through a brazenly engineered resolution process that transferred DHFL to Ajay Piramal’s conglomerate for a bargain ₹37,250 crore against admitted claims exceeding ₹87,000 crore. The outcome was grotesque: FD holders received barely 23% recovery—₹1,241 crore against dues of ₹5,375 crore—amid rigged valuations, suppressed avoidance claims, and documented fraud.

This was not a case of administrative inefficiency or unintended collateral damage. It exposed the IBC’s core design flaw: the elevation of “commercial wisdom” above equity, justice, and constitutional guarantees. By subordinating all other considerations to opaque Committee of Creditors (CoC) decisions—dominated by crony banks—the IBC systematically overrides pre-existing regulatory safeguards under the RBI and NHB, vaporizing the rights of small creditors while channeling colossal windfalls to politically connected acquirers. What masquerades as creditor-led reform in fact operates as an industrial-scale expropriation machine.

In DHFL’s case, promoters Kapil and Dheeraj Wadhawan allegedly siphoned billions through shell entities prior to insolvency. Yet, rather than recovering these assets for victims, the system assigned notional ₹1 valuations to massive avoidance transactions—potentially involving ₹47,000 crore in asset-backed loans—which were then allowed to accrue exclusively to the successful resolution applicant, Piramal, post-approval. Thus, the loot cascaded upward, while victims were judicially gagged by deference to CoC “commercial wisdom.” This doctrine reached its apotheosis in the Supreme Court’s April 2025 ruling, which rubber-stamped the resolution plan despite the NCLAT’s brief and ultimately aborted scrutiny of the avoidance framework.

After years of mass petitions, street protests, and serial appellate rejections—culminating in the Supreme Court’s 2025 dismissals that sanctified the resolution even as the Wadhawans secured bail in parallel fraud investigations—a resilient cadre of survivors has arrived at an unavoidable conclusion: the IBC itself is the first premise of injustice. Its constitutional validity must be challenged wholesale, particularly under Articles 14 and 21, as a discriminatory regime that enables elite expropriation while annihilating small creditors’ rights. DHFL is the litmus test par excellence.

The “legitimization” of the DHFL resolution also performs a broader laundering function. It neutralizes the terror-funding taint associated with the Wadhawans’ alleged links to Dawood Ibrahim’s network via Iqbal Mirchi—under ED investigation since 2019, involving ₹2,200 crore in suspect transactions—while obscuring a murky political donation ecosystem. Entities such as RKW Developers (linked to the Wadhawans and under ED scrutiny) reportedly donated ₹10 crore to the BJP, alongside Piramal Group’s ₹85 crore in electoral bond contributions through Piramal Enterprises, Piramal Capital, and PHL Finvest. These flows sit uneasily alongside earlier controversies, including the 2014 Flashnet deal, where Piramal Estates acquired a firm linked to then-minister Piyush Goyal at a 1,000× premium for ₹48 crore, suggesting quid pro quo that now culminates in the predatory DHFL takeover. The IBC thus emerges as the regime’s central looting instrument, shielding dacoits in suits while condemning ordinary citizens to destitution.

It was precisely this systemic rot that prompted the filing of a writ petition under Article 32 in the Supreme Court of India—W.P.(C) No. 001100/2021 (Diary No. 23251/2021)—challenging the IBC’s legitimacy as the first premise in the contextualized reckoning of the DHFL scam. Filed on 30 September 2021, the petitioners included Debaprasad Bandyopadhyay, Shweta H.S., Mrs. Rupa Bandyopadhyay, Shreyas S.V., Mira Barman, Tapash Kumar Mitra, Chandra Prakash Chamaria, and Rajpath Contractors and Engineers Ltd., represented by Advocate Deepak Prakash, against respondents including the Union of India, RBI, NHB, DHFL, the CoC (through R. Subramaniakumar), the Enforcement Directorate, and Ms. Charu Desai.

The petition—categorized under company law and financial regulatory matters—was disposed of without explanation. The reason was brutally simple: those who dared to challenge the IBC’s legitimacy were financially exhausted. In a judicial system where justice is expensive, endlessly delayed, and governed by tarikh pe tarikh, the poor are priced out of constitutional redress. The DHFL victims did not lose because their case lacked merit; they lost in this particular legal battle because truth, in India’s insolvency regime, is unaffordable.

See More: The Avoidance Mechanism under India’s Insolvency Code: A System in Crisis VIEW HERE ⤡ (As reported on 24th December, 2025 ©Moneylife)

Video Courtesy: Ayush Vishwakarma (Source Video VIEW HERE⤡)

SEE ALSO:

Not only IBC, all the other acts after passing bill without discussion show systematic structural failure of the then Modi Sarkar.

LikeLiked by 1 person