Posted on 10th April, 2026 (GMT 06:44 hrs)

ABSTRACT

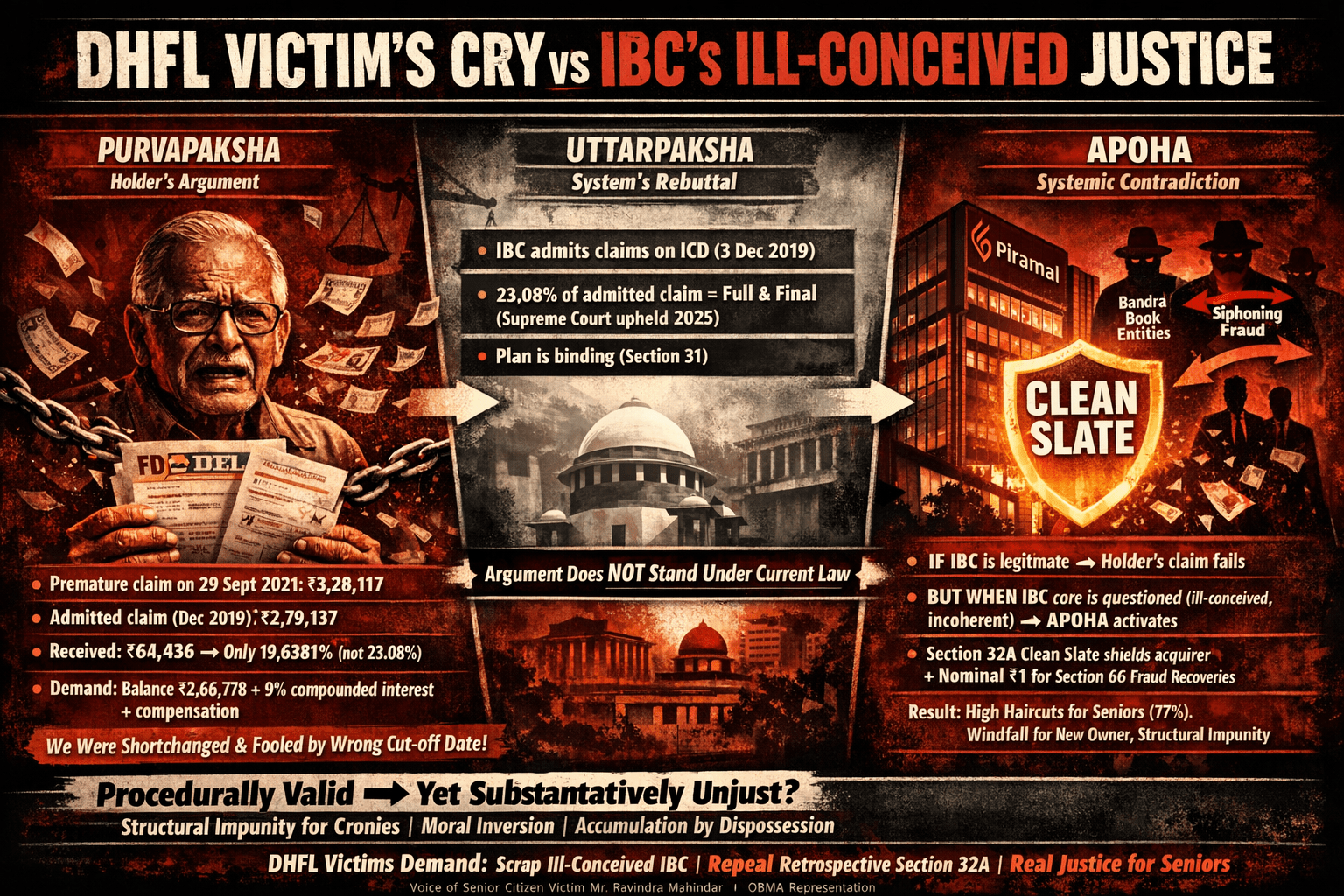

This article examines a senior DHFL fixed deposit holder’s grievance against the 23.08% recovery under the Piramal resolution plan. In Purvapaksha, Mr. Ravindra Mahidhar, the senior citizen FD Holder in question, argues that using the December 2019 cut-off instead of the 29 September 2021 payment date shortchanged him, recalculating his claim at ₹3,28,117 (versus the admitted ₹2,79,137) and receiving only 19.64% instead of 23.08%. Uttarpaksha rebuts that under IBC rules, claims are fixed at the Insolvency Commencement Date, the payment matches the approved plan, and the Supreme Court (2025) upheld it as binding and final. Apoha then probes the deeper paradox: while the individual claim fails if IBC is accepted as legitimate, questioning the IBC’s core as an ill-conceived and incoherent law reveals structural contradictions — particularly between Section 32A’s clean slate immunity and Section 66’s fraud recovery provisions — raising concerns of systemic unfairness, moral hazard, and crony sanitisation for retail victims.

I. Introduction

Taking cue from classical South Asian philosophical traditions, arguments could be articulated through three distinct yet interrelated stages: pūrvapakṣa—the rigorous presentation of the aggrieved or opposing position in its strongest form; uttarapakṣa—the critical rebuttal or khaṇḍana of that position alongside the systematic establishment of a counter-claim; and, moving beyond conventional forms of such “dialectics”, Apoha—not merely as stark exclusion, but as the residual space of unresolved tension that persists beyond both assertion and refutation, gesturing toward what escapes final closure.

This article applies that framework to a passionate representation received from Mr. Ravindra Mahidhar, a widowed senior citizen, DHFL fixed deposit victim, and also an ardent supporter of our OBMA initiatives.

In simple terms, the article first presents Mr. Mahidhar’s strong grievance — he believes he was shortchanged because the company used the wrong cut-off date and paid him far less than he feels he deserved. It then gives the official reply from the system (banks, Piramal, and courts), which says the payment was correct and “final” under the law. Finally, it explores the bigger question: even if the rules were followed correctly in this case, is the entire IBC system itself fair, or does it systematically disadvantage ordinary depositors like senior citizens while favouring politically associated big companies? Who makes the rules?

The law exists for the people, not the people for the law.

II. Pūrvapakṣa: The FD Holder’s Argument – “We Were Shortchanged on the True Claim Amount”

A former fixed deposit (FD) holder of Dewan Housing Finance Corporation Ltd. (DHFL) named Mr. Ravindra Mahidhar, whose two FDs had a combined original maturity value of approximately ₹3,31,214, strongly disputes the resolution process under the Piramal Capital & Housing Finance Ltd. plan. He argues that RBI, the Committee of Creditors (CoC), and other stakeholders misled FD holders, the National Company Law Tribunal (NCLT), and the National Company Law Appellate Tribunal (NCLAT) by treating the payment of 23.08% of the “admitted/claimed amount” as full and final settlement.

His core objection is the cut-off date used for calculating the admitted claim. The CoC/admitted claim used a date around 10 December 2019 (close to the insolvency commencement date of 3 December 2019), whereas he insists the actual payment date of 29 September 2021 should have been used. This, he says, artificially lowered his admitted claim and resulted in a much smaller payout.

Mr. Mahidhar’s Claim Calculations

For his two FDs:

(A) First FD

- Principal: ₹1,20,000 (deposited 12 July 2018)

- ROI: 8.9% p.a.

- Original maturity: 12 November 2021 (40 months)

- Maturity amount: ₹1,59,574

- Less interest for 44 days (premature closure on 29 Sept 2021): ₹1,287

- Premature amount on 29 Sept 2021: ₹1,58,287

(B) Second FD

- Principal: ₹1,30,551 (deposited 21 November 2018)

- ROI: 9.55% p.a.

- Original maturity: 21 December 2021 (approx. 36–37 months)

- Maturity amount: ₹1,71,674

- Less interest for 53 days: ₹1,810

- Premature amount on 29 Sept 2021: ₹1,69,830

Total premature/realisable value on payment date (29 Sept 2021): ₹1,58,287 + ₹1,69,830 = ₹3,28,117 (he rounds it to ₹3,28,127 in some places).

However, the official admitted claim shown in his online status was only ₹2,79,137 (based on the 2019 cut-off).

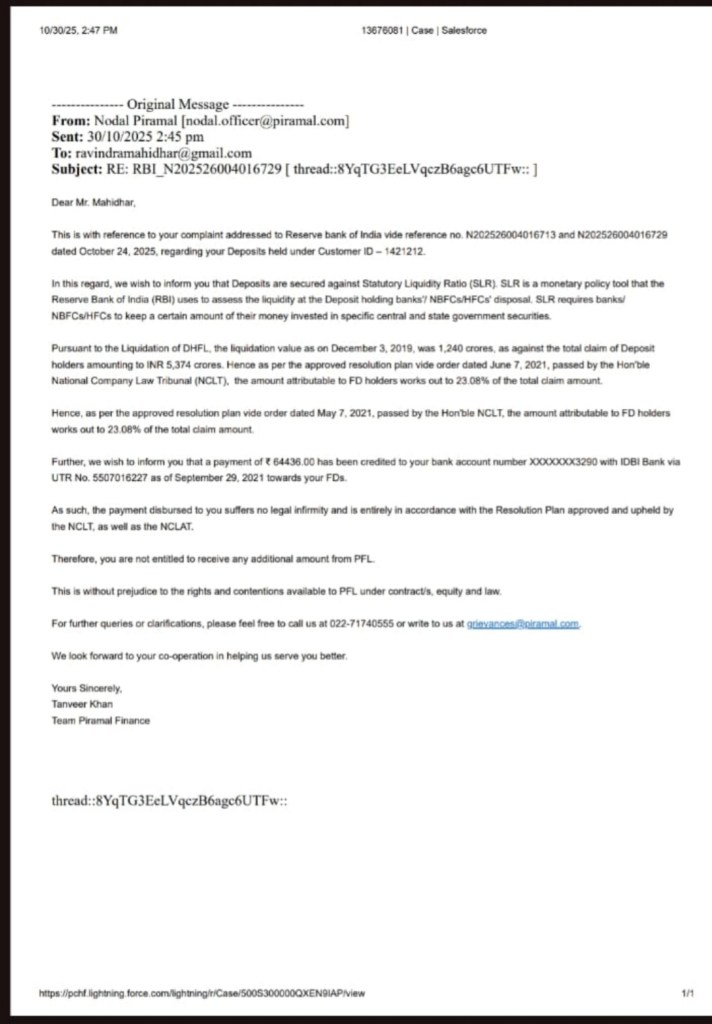

He received ₹64,436 on 29 September 2021 (via IDBI Bank).

His Percentage and Balance Calculations

- Against his recalculated claim of ₹3,28,117, the received amount works out to only 19.6381% (not the advertised 23.08%).

- Balance due: ₹2,66,778 (approx. 80.36% still outstanding).

- Against original maturity value (₹3,31,214), the recovery is even lower in his view.

He further demands:

- The unpaid balance of ₹2,66,778 plus overdue interest accrued after 29 September 2021.

- Compounded interest at 9% p.a. (half-yearly) from 29 Sept 2021 to 28 March 2026, which he calculates would take the due amount to around ₹3,96,458, plus further interest till actual payment date.

- Additional justified compensation for the delay, mental agony, and alleged misguidance by authorities.

Implication drawn by the holder: The entire 23.08% recovery mechanism is flawed and unfair because it ignored the time value of money and the actual amount due on the payment date. He believes stakeholders were “totally misguided/fooled,” and he is entitled to the balance plus interest and compensation. The payment, in his eyes, does not represent full and final settlement.

III. Uttarpakṣa: The Rebuttal (?) by the “System”

While the FD holder’s frustration is understandable—many retail depositors suffered significant haircuts—the legal and procedural framework under the Insolvency and Bankruptcy Code (IBC), 2016 does not support his recalculations or demand for additional amounts. The resolution plan was approved by the CoC (with overwhelming majority), by NCLT on 7 June 2021, and ultimately upheld by the Supreme Court in April 2025. Here is a clear, point-by-point rebuttal:

- Correct Cut-off Date for Claim Admission

Under IBC, claims are admitted based on the Insolvency Commencement Date (ICD) — 3 December 2019 for DHFL. The public announcement invited claims by mid-December 2019. Interest accrual is generally frozen or limited post-ICD due to the moratorium under Section 14.

Using the “actual payment date” (29 Sept 2021) or adjusting for premature closure interest as of 2021 would amount to allowing post-CIRP interest, which the approved plan and IBC do not permit for this class of creditors. The CoC and Administrator verified claims against the company’s books as on the ICD. Courts have consistently refused to reopen individual claim admissions on this basis. - 23.08% Was of the Admitted Claim — Not Maturity or Premature Value

The Piramal plan explicitly provided 23.08% of the admitted claim amount in cash as full and final settlement for FD holders (treated as dissenting financial creditors).

Total admitted claims of FD holders: approximately ₹5,374–5,375 crore.

Total payout to the class: approximately ₹1,240–1,243 crore (exactly 23.08%).

In this holder’s case, if the admitted claim was ₹2,79,137, then 23.08% comes to roughly ₹64,436 — which precisely matches what he received.

The “19.64%” figure appears only when he substitutes his higher self-calculated premature/maturity value. The plan never used maturity value or 2021 premature value as the base. Original contract terms (maturity amounts, premature interest) were overridden by the binding resolution plan. - The Plan Provided Full and Final Settlement — No Further Interest or Compensation

The approved plan treated the cash payout as extinguishing the entire FD liability. It did not provide for ongoing interest post-payment or any additional “overdue” amounts after 2021.

Section 31 of the IBC makes a court-approved resolution plan binding on all stakeholders, including dissenting creditors. Post-2021 demands for compounded interest at 9% or “justified compensation” contradict the finality of the plan. - RBI/NHB Provisions Do Not Override IBC

The holder implicitly relies on regulatory expectations of full repayment of deposits. However, the Supreme Court (in its April 2025 judgment) explicitly clarified that neither the RBI Act, 1934 nor the National Housing Bank Act, 1987 mandates full repayment of deposits in an insolvency resolution scenario. These laws allow repayment of the deposit “or part thereof.”

Crucially, Section 238 of the IBC has overriding effect over other laws. The Court held that the distribution mechanism in the plan (including the 23.08% for FD holders) was fair, compliant with IBC, and did not violate regulatory provisions. Appeals by FD holders on this ground were dismissed. - Commercial Wisdom of CoC and Judicial Deference

The CoC (representing financial creditors) exercised its commercial wisdom in approving the distribution, including the treatment of FD holders. Courts, including the Supreme Court, give wide deference to this wisdom and do not interfere unless there is clear perversity or violation of law.

Proposals to increase FD recovery to ~40% (to match some secured creditors) were considered but not carried through by majority vote. A higher payout was not mandated.

FD holders (as a class) were represented through an authorised representative in the CoC; individual dissent does not override the class decision. - Implementation and Finality

Payments were disbursed starting September 2021 exactly as per the plan (cash credits with UTR details), and Piramal’s communication correctly stated there was “no legal infirmity” and no entitlement to additional amounts.

The Supreme Court in 2025 upheld the entire plan, dismissed FD/NCD holder appeals, and affirmed that the distribution was in accordance with IBC. No further claims survive.

Below is the response received by Mr. Mahidhar from the Piramal Nodal Office, which appears to be a standard copy-paste reply, similar to what we have received previously:

IV. Apoha: Can We Challenge the Sacrosanct Nature of CoC-under-IBC Decisions?

Even when an individual DHFL FD holder’s specific recalculations and arguments do not hold if and only if we accept the IBC and its CoC-driven CIRP as legitimate and binding, a broader systemic “apoha” becomes operative the moment we begin to problematize, question, and critique the very foundations of the IBC itself — viewing it as poorly conceived, heavily amended, and internally incoherent legislation, with the DHFL scenario serving as a test case to legitimize and justify the IBC.

In the Indian philosophical sense of an apparent uncontradictory contradiction that invites deeper inquiry, this apoha persists as the everyday-level chatter of unease, unresolved tensions, and not-so-quite discontent among affected stakeholders.

Is the IBC-CoC framework genuinely fool-proof and impervious to significant scrutiny? Or do its profound internal inconsistencies — especially the dynamic interaction between Section 32A (offering clean slate immunity to the corporate debtor after resolution) and Section 66 (pertaining to actions for fraudulent or wrongful trading) — expose underlying structural contradictions? These contradictions may challenge the substantive justification for the treatment of retail FD holders, even if such treatment is procedurally (and seemingly) validated by specific courts.

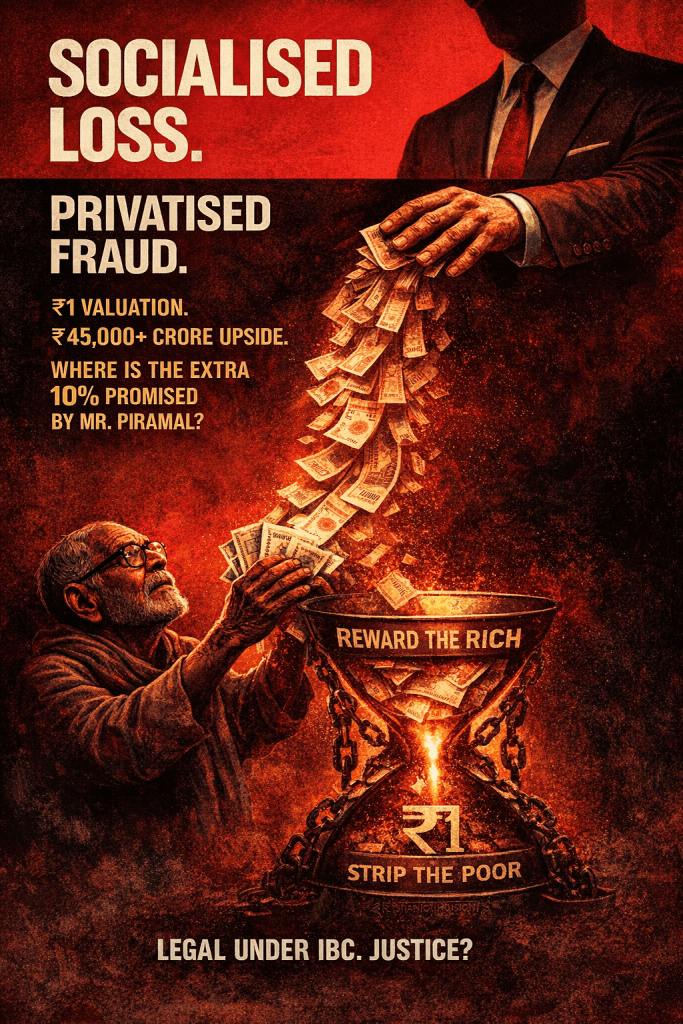

The Core Paradox: Section 66 empowers the resolution professional to pursue recoveries where business was carried on with intent to defraud creditors or for fraudulent purposes (or wrongful trading by directors who knew insolvency was imminent but failed to minimize losses). In DHFL, forensic audits flagged massive irregularities, including fictitious loans routed through “Bandra Book Entities,” with siphoning/diversion estimates ranging from ₹14,046 crore (as on June 30, 2019) to broader figures of ₹45,000+ crore across avoidance and Section 66 applications. The intent is restorative and deterrent — to claw back value for the creditor estate and hold wrongdoers accountable.

Yet the approved Piramal plan (overall value ~₹37,250 crore) ascribed a notional value of just ₹1 to potential Section 66 recoveries and explicitly allowed the successful resolution applicant (SRA — Piramal) to appropriate any future proceeds from them. Recoveries from other avoidance transactions (Sections 43, 45, 50 etc.) were directed to the CoC.

Notably, during the bidding process Piramal had publicly promised an additional 10% over and above whatever the CoC decided for FD holders, but this sweetener did not materialise in the final approved plan; FD holders ultimately received only the base 23.08%.

This allocation process unfolded against the backdrop of two key orders that were effectively sidelined in the final outcome. The NCLT order dated 19 May 2021 (in IA No. 2431 of 2020 filed by erstwhile director/promoter Kapil Wadhawan) directed the Administrator to place the ex-promoters’ “second settlement proposal” — which claimed significantly higher value realisation for creditors — before the CoC for consideration, decision, and voting, and to inform the outcome within 10 days. The order invoked the Adjudicating Authority’s powers under Section 60(5)(c) of the IBC and Rule 11 of the NCLT Rules, 2016, emphasising the need to explore better value maximisation amid the serious fraud allegations and the peculiar composition of DHFL’s creditors. However, the Administrator and CoC (represented by Union Bank of India) immediately challenged the order before the NCLAT, which granted a stay on 25 May 2021.

The CoC did not place the proposal before it for substantive consideration or voting as directed. The NCLT thereafter approved the Piramal resolution plan on 7 June 2021 (subject to certain observations), allowing the process to proceed without compliance with the earlier directive on the alternative settlement proposal.

The NCLAT order dated 27 January 2022 (in Company Appeal (AT) (Ins) Nos. 454-455, 750 of 2021 and connected matters, including appeals by 63 Moons Technologies Ltd.) explicitly addressed the treatment of recoveries. It set aside the clause in the resolution plan that permitted the SRA (Piramal) to appropriate recoveries from Section 66 applications and directed that the resolution plan be sent back to the CoC for reconsideration on this aspect. The tribunal highlighted material irregularities in the CIRP process, the treatment of fraudulent-trading recoveries (which, under Section 66, are meant to benefit the creditor estate), and questioned whether the CoC’s commercial wisdom had been exercised in full alignment with the IBC’s restorative objectives in fraud cases.

The Supreme Court in its 1st April 2025 judgment set aside the NCLAT’s interference, holding that the allocation was a legitimate “commercial bargain” and part of the CoC’s wisdom, not open to judicial tinkering absent clear perversity. The Court distinguished Section 66 (conduct-based, penal in nature) from pure asset-restorative avoidance actions under Chapter III, allowing contractual flexibility. It directed NCLT to decide the applications separately, with Section 66 recoveries going to the SRA and others to the CoC. However, the NCLT has not visibly responded to the same even after a year!

Section 32A Amplifies the Tension: Section 32A was introduced through an ordinance promulgated on 28 December 2019 — just 25 days after DHFL’s Corporate Insolvency Resolution Process (CIRP) began on 3 December 2019. The provision was later enacted into law in March 2020 and explicitly given retrospective effect from the date of the ordinance itself. Once a resolution plan is approved by the Adjudicating Authority and there is a change in management/control to a party not involved in the earlier misconduct, Section 32A grants the corporate debtor near-absolute immunity from prosecution, attachments, or any liabilities for offences committed prior to the commencement of CIRP.

One could describe this as enabling a “corporate metamorphosis of liability” — the entity retains its legal identity, assets, and economic continuity (including potential upside from Section 66 recoveries), yet is severed from past criminal responsibility. The result is a profound internal incoherence: the IBC formally acknowledges fraud through Section 66 and avoidance tools, yet systematically “launders” corporate-level accountability via Section 32A, shielding the resurrected entity (and its assets) while alleged siphoned value (or future recoveries) can flow to the acquirer rather than fully compensating defrauded creditors. In DHFL, this facilitated what some call an “engineered legal coup,” sanitising a tainted entity for the new owner.

In DHFL’s case, retail FD holders (part of the ~₹5,375 crore admitted claims for the class) bore ~77% haircuts, recovering only ~23% in cash. Secured financial creditors generally fared better. The acquirer gained a cleansed entity with potential upside from any Section 66 successes (speculative though they may be), while public trust in deposit safety eroded. Broader IBC data reinforces the pattern: cumulative recoveries reached ~₹4.1 lakh crore by late 2025, but average recovery rates hovered around 31–33% of admitted claims (implying 67–69% haircuts), with rates dipping as low as 20% in some quarters and liquidation outcomes remaining dismal (often 5–7%). High haircuts have persisted, raising questions about genuine value maximisation versus distress sales or negotiated outcomes favouring select bidders.

These orders (NCLT 19/05/2021 directing reconsideration of a potentially superior settlement and NCLAT 27/01/2022 directing reconsideration of the Section 66 allocation clause) underscore the core paradox: while the IBC formally acknowledges and equips mechanisms to address fraud through Section 66 and avoidance tools, the practical implementation in DHFL allowed the negotiated plan — with its nominal valuation and SRA appropriation of fraud recoveries — to prevail. The swift stay on the NCLT directive, non-compliance with its direction, and the later reversal of NCLAT’s modifications reinforced the primacy of CoC commercial wisdom, even as retail FD holders bore heavy haircuts. The acquirer gained a cleansed entity with potential upside from any Section 66 successes, while public trust in deposit safety eroded. This sequence has been cited by affected stakeholders as emblematic of how statutory intent can be subordinated to transactional finality.

The Insolvency and Bankruptcy Code (IBC), far from being a neutral technocratic instrument for “value maximisation” and “timely resolution,” has crystallised into one of the most sophisticated mechanisms of accumulation by dispossession in contemporary India. Nowhere is this more grotesquely visible than in the DHFL resolution, where the presupposed supremacy of the CoC’s “commercial wisdom” — repeatedly sanctified by the Supreme Court, most emphatically in its April 2025 ruling — functions as juridical cover for a brazen transfer of public and retail suffering into private windfall for connected capital.

A. Socialisation of Losses, Privatisation of Fraud Upside: The Moral Inversion Perfected

Retail fixed deposit holders — overwhelmingly elderly citizens whose life savings were parked in what was once marketed as a safe housing finance vehicle — were forced to swallow haircuts that bordered on expropriation. Meanwhile, the Strategic Resolution Applicant (SRA), Ajay Piramal, secured potential recoveries from massive fraudulent and avoidable transactions (forensic estimates running into tens of thousands of crores) at a nominal valuation of ₹1.

This is not mere commercial negotiation; it is institutionalised moral inversion. The IBC’s Section 53 waterfall and the CoC’s majority vote (often dominated by public sector banks eager for quicker recapitalisation-backed exits) formally comply with the letter of the law while enabling the socialisation of fraud costs (borne by taxpayers via bank recapitalisation and by retail savers via near-total wipeout) and the privatisation of fraud upside (captured by the new owner). The Supreme Court’s 2025 endorsement of this allocation effectively legalised a form of resolution capitalism in which the fruits of corporate looting are gifted to the acquirer under the pious banner of “clean slate” and “expeditious revival.”

Market discourse and victim forums rightly describe this as juridical architecture of structural impunity — a system that probes fraud performatively (through forensic audits and Section 66 applications) only to hand its monetisable remains to the very entity that benefits from extinguishing accountability.

B. Crony Collusion and Political Nexus: Piramal-BJP Architecture of Capture

The DHFL saga cannot be understood without naming the reported nexus between Ajay Piramal and the ruling BJP dispensation. Allegations of quid pro quo — ranging from substantial electoral bond contributions by Piramal Group entities to the BJP, the controversial Flashnet transaction involving a BJP minister, and Piramal’s uncanny prescience about an impending NBFC sector “shock” just before DHFL’s collapse — point to a deeper political-corporate collusion.

The CoC, effectively steered under RBI oversight in this case, displayed a clear preference for Piramal’s bid despite competing proposals that allegedly offered better terms for retail creditors. Opaque deliberations, alleged bidder favouritism, and the sidelining of higher payout proposals for FD holders reinforce the perception of institutional capture. The authorised representative mechanism for retail classes provided only performative voice, binding individuals to majority decisions that systematically marginalised the most vulnerable.

This is crony capitalism 2.0: not crude licence-permit raj, but a sophisticated electoral-autocratic insolvency regime where proximity to political power translates into preferential access to distressed public assets at fire-sale (or even sub-fire-sale) valuations, insulated by statutory immunity.

C. Performative Anti-Fraud Provisions and Legalised Corporate Amnesia

Section 32A of the IBC — applied retrospectively and expansively in the DHFL matter — has neutered the deterrent potential of Sections 66 and 67 while granting near-blanket immunity from prior offences, including overlapping proceedings under PMLA. The corporate debtor emerges cleansed (“corporate amnesia” made statutory), even as forensic trails of diversion running into thousands of crores are effectively neutralised for the new owners.

This statutory sanitisation finds its most cynical expression in the choreography of forgetting that followed the resolution. In September 2021, Piramal Capital & Housing Finance Limited (PCHFL) executed a reverse merger into the insolvent Dewan Housing Finance Corporation Limited (DHFL). The tainted shell of DHFL — riddled with allegations of massive fraud and diversion — survived as the legal entity, while PCHFL was absorbed into it. The amalgamated entity was then promptly rechristened Piramal Capital & Housing Finance Limited (PCHFL), effectively burying the DHFL name and its toxic legacy under a fresh Piramal-branded identity. By March 2025, this entity underwent yet another rebranding to Piramal Finance Limited, completing the cosmetic erasure. The sequence culminated in a further restructuring involving the reverse merger of the listed parent Piramal Enterprises Limited (PEL) into this very vehicle, embedding the DHFL-acquired assets deep within a newly configured, “clean” financial architecture.

The choreography reached its logical culmination in February 2026, when a Mumbai Special PMLA Court, on 2 February 2026, discharged Piramal Finance Limited (formerly DHFL) from a ₹5,050 crore money laundering case linked to the Yes Bank-DHFL scam. Citing Section 32A of the IBC and the change in management, the court granted full statutory immunity to the corporate debtor, holding that it could no longer be prosecuted for pre-resolution offences. This ruling not only extinguished the Enforcement Directorate’s proceedings against the entity but also provided judicial affirmation that the “clean slate” doctrine overrides even overlapping PMLA liabilities — a near-perfect execution of legalised oblivion.

This is not organic corporate evolution; it is a meticulously staged architecture of cunning capitalism — successive layers of reverse merging, renaming, rebranding, and now judicial discharge designed to induce collective amnesia. The original sins of DHFL are not confronted or clawed back; they are ritually dissolved through juridical and branding sleight-of-hand. Forensic trails remain on paper, but the public face of the enterprise is repeatedly laundered until the stench of the original fraud becomes untraceable to the casual observer, the regulator, or the retail victim.

Combined with the near-absolute judicial deference to CoC “commercial wisdom” (reaffirmed yet again in 2025), this creates a framework of performative accountability: fraud is acknowledged, investigated, and then monetarily reassigned to the acquirer at token value. The result is not resolution but legalised sanitisation of tainted assets — a process that Parliamentary Standing Committees have repeatedly flagged for excessive haircuts (routinely 60-95%), opaque valuations, and the subordination of enterprise value to distress liquidation logic, yet these concerns remain ritualistically ignored under the dogma of non-interference.

In this theatre of impunity, Section 32A does not merely extinguish liabilities; it enables the systematic rewriting of corporate memory itself. The DHFL-to-PCHFL-to-Piramal Finance sequence, crowned by the February 2026 PMLA discharge, stands as a textbook case of how the IBC’s clean-slate doctrine, when married to strategic branding, reverse mergers, and overriding immunity, produces not revival but institutionalised oblivion — where the fruits of alleged fraud accrue to the connected acquirer while the original victims are left staring at a shiny new logo that no longer bears the name of their loss.

E. Towards Structural Rupture, Not Cosmetic Reform

Mere tinkering — stronger safeguards for retail creditors, better valuation norms, or enhanced transparency in CoC processes — is insufficient. The DHFL case stands as a litmus test exposing the IBC as an ill-conceived instrument that facilitates crony sanitisation of distressed (and sometimes solvent) assets under the guise of insolvency resolution.

The demand must be bolder: repeal or fundamental overhaul of Section 32A (including its retrospective application), reopening of corporate criminal accountability where fraud is established, calibrated dismantling of the absolute clean-slate doctrine (especially where proceeds of crime or public interest are involved), and a serious parliamentary re-examination of whether the current IBC architecture serves collective creditor and societal interests or merely accelerates efficient transfers of control with grossly uneven — and often predatory — distributional outcomes.

Until then, the “commercial wisdom” of the CoC will remain what it has largely become in practice: a juridical euphemism for the predatory convergence of big capital, public bank recapitalisation, and political patronage under the sign of insolvency reform.

The DHFL victims’ prolonged struggle is not merely about individual recoveries. It is about whether India’s financial architecture will continue to legitimise this reverse merger republic of impunity — or whether a deeper democratic and juridical reckoning can still be forced.

V. Conclusion

Ultimately, while the specific FD holder’s letter offers no viable legal reopening of his claim under the existing framework, the apoha reveals that IBC-CoC decisions, though judicially upheld as binding and largely non-justiciable, remain open to legitimate critique on grounds of equity, transparency, internal statutory consistency, moral hazard, and long-term societal trust in the financial system. Efficient resolution was achieved in DHFL, but the lingering chatter persists: at what cost to deposit safety, fraud deterrence, perceived fairness, and public confidence? The presupposed supremacy of CoC commercial wisdom, while pragmatically useful for speed, invites scrutiny when it appears to insulate systemic imbalances and enable structural impunity. Systemic reforms — informed by ongoing reflection on these contradictions, potential amendments, and lessons from high-profile cases like DHFL — may prove more constructive than isolated challenges. The framework continues to evolve through jurisprudence and legislative tweaks; whether it can better balance revival with robust protection for the most vulnerable stakeholders and genuine accountability remains an open, vital, and increasingly urgent inquiry.

APPENDIX: Logical Anatomy of the Dispute – Purvapakṣa, Uttarpakṣa, and the Apoha of IBC “Legitimacy” (?!)

The appendix presents the entire debate in simple logical form. It breaks down Mr. Mahidhar’s argument and the official system’s reply into clear “if-then” statements using basic symbols.

It shows two opposite conclusions:

- Mr. Mahidhar’s side says: “Because my real claim was higher and I received much less, I was shortchanged and misled.”

- The official IBC/system side says: “Because the law clearly says we pay 23.08% of the admitted claim only, and the plan is final and binding, nothing more is due.”

The appendix then highlights the deeper “Apoha” — the bigger contradiction: If we accept the current IBC rules as fair and final, then Mr. Mahidhar is wrong. But if we question whether the IBC law itself is flawed and unjust, then his grievance points to a much larger systemic problem affecting thousands and lakhs of victims. In short, it helps readers see both the specific dispute and the bigger picture debate in a structured way.

Which Symbol Stands for What

| Symbol | Meaning | What it stands for | Example in this case |

|---|---|---|---|

| • | Conjunction (AND) | Both statements are true together | P1 • P2 means P1 AND P2 |

| ⊃ | Implication (IF…THEN) | If the left side is true, then the right side follows | P1 • P2 • P3 • P4 ⊃ C_h means If P1 and P2 and P3 and P4 are true, then C_h follows |

| ~ | Negation (NOT) | The opposite / denial | ~(IBC is legitimate) means It is not the case that IBC is legitimate |

1. Premises

| Premise | Statement |

|---|---|

| P1 | Two FDs had original combined maturity value = ₹3,31,214 |

| P2 | Premature value on actual payment date (29 Sept 2021) = ₹3,28,117 |

| P3 | Officially admitted claim (CoC, Dec 2019 cut-off) = ₹2,79,137 |

| P4 | Amount actually received = ₹64,436 |

| P5 | 23.08% of admitted claim (₹2,79,137) ≈ ₹64,436 |

| P6 | Resolution plan pays 23.08% of admitted claim as full & final settlement for FD holders |

| P7 | IBC admits claims on Insolvency Commencement Date (3 Dec 2019); post-ICD interest generally frozen |

| P8 | Approved resolution plan is binding on all (Section 31 IBC) and overrides other laws (Section 238 IBC) |

2. Holder’s Logical Derivation (Purvapaksa)

Premises: P1 • P2 • P3 • P4

Derivation: ₹64,436 ÷ ₹3,28,117 = 19.6381% (not 23.08%) Balance due = ₹2,66,778 (80.3619%)

Holder’s Conclusion (C_h):

P1 • P2 • P3 • P4 ⊃ C_h

(We were shortchanged & misled)

3. System’s Logical Derivation (Uttarpaksa / Rebuttal)

Premises: P5 • P6 • P7 • P8

Derivation: Payment = 23.08% of admitted claim (correct base) Using 2021 premature value would violate moratorium & IBC rules Plan is court-approved and binding

System’s Conclusion (C_s): P5 • P6 • P7 • P8 ⊃ C_s

(Payment was correct & final)

4. Apoha: The Deeper Systemic Contradiction

Conditional Logic:

- If IBC + CoC process is accepted as legitimate and binding: (P5 • P6 • P7 • P8) ⊃ C_s → Holder’s claim fails (C_h is invalid under current law)

- But if the core of IBC itself is problematized (as ill-conceived, heavily amended, and internally incoherent): → Apoha becomes operative

Apoha Statement: Even though the individual argument fails under existing rules, once we critique the foundational legitimacy of IBC, deep structural paradoxes emerge — especially the tension between Section 32A (clean slate immunity) and Section 66 (fraud recovery).

This creates an uncontradictory contradiction: The process is procedurally valid → yet potentially substantively unjust (high haircuts for retail victims, windfall for acquirer, moral hazard, crony sanitisation).

Final Logical Tension

Holder’s Position: P1 • P2 • P3 • P4 ⊃ C_h (We were shortchanged & misled)

System’s Position: P5 • P6 • P7 • P8 ⊃ C_s (Payment was correct & final)

Apoha (Meta-Level):

(IBC is legitimate) ⊃ C_s is true

~ (IBC is legitimate) ⊃ Apoha activates → Systemic critique is valid

Overall Conclusion: The individual claim fails if IBC is accepted as valid. The systemic critique becomes powerful when the IBC itself is put under scrutiny.