Posted on 1st April, 2026 (GMT 01:29 hrs)

ABSTRACT

The Indian rupee, far from a stable symbol of sovereignty, has become a theatre of illusion, confusion, and quiet violence—where citizens struggle to recognize notes and coins, multiple designs of the same denomination coexist, and fragile post-2016 currency circulates at high fiscal (₹6,372.8 crore in FY 2024–25) and ecological cost. Tracing a lineage from Muhammad bin Tughlaq’s failed token currency to demonetisation and the fleeting ₹2000 note, this critique reveals a recurring pattern of top-down monetary experiments that burden the public while failing to ensure stability or inclusion. The rupee’s steady depreciation against the US dollar (crossing ₹91 in 2025) reflects deeper global asymmetries masked by PPP metrics, exposing ongoing value extraction from the Global South. Drawing on Marx’s Grundrisse, the analysis frames money as a fetish form that conceals labour and ecological relations behind abstract price, whether in physical currency or digital alternatives. Ultimately, neither reform nor technology can resolve these contradictions; emancipation requires transcending the money-form itself toward a reciprocal, ecological, and post-capitalist society—where value is lived rather than priced, and the rupee is recognized not just as broken, but as a symptom of a deeper civilisational illusion.

I. Introduction: The Everyday Violence of Money

In 2018, at Delhi International Airport, I handed a crisp ₹500 note to the prepaid cab collector, only to have it thrust back with contempt: “Sir, yeh ₹500 nahi, ₹50 hai.” A few months later, a medical shopkeeper angrily discarded a coin into the dustbin, explaining that a customer had given him a 50-paise coin which he had mistaken for ₹5. Not long after, an elderly kirana store owner painstakingly scrutinised every coin I offered, muttering in frustration, “Bahut confusion hai… purane aur naye coins ek jaise lagte hain.”

These seemingly trivial episodes reveal a deeper systemic failure: the Indian rupee has become a daily theatre of illusion, confusion, and quiet violence. Post-2016 Mahatma Gandhi New Series notes are thinner, smoother, and far more fragile than their predecessors. Multiple designs for the same denomination (₹10, ₹20, ₹50, ₹100) circulate simultaneously, while coins of ₹1, ₹2, ₹5, and ₹10 often defy quick visual or tactile recognition. The resulting erosion of trust and usability hits senior citizens, the visually challenged, and small traders hardest. This confusion is compounded by massive fiscal waste — ₹6,372.8 crore spent on security printing in FY 2024–25 alone — and significant ecological burdens from cotton-based paper and metal coins.

Such heterogeneity is not accidental but stems from a cost-driven design philosophy that prioritises short-term printing efficiency and ATM compatibility over durability and accessibility. Older notes and coins remain legal tender indefinitely, creating a chaotic layered economy of differing sizes, colours, thicknesses, and feels for identical face values. The short-lived ₹2000 note, rushed in after the 2016 demonetisation and quietly withdrawn in 2023, exemplifies this pattern of hasty, top-down monetary engineering that ultimately burdens the public.

These failures echo a distant precedent: in 1329–1332, Sultan Muhammad bin Tughlaq’s disastrous experiment of equating copper tokens with silver tankas collapsed amid counterfeiting and inflation, forcing massive redemption costs. Seven centuries later, the 2016 demonetisation repeated the same hubris, inflicting hardship on ordinary citizens while achieving little lasting stability.

At root, these episodes expose the Marxian truth articulated in the Grundrisse: money functions as a fetish that reduces a bottle of cold drink from its concrete use-value to the abstract price of Rs. 50, equating the unequal while concealing the living labour and ecological relations embedded in it. Whether in confusing physical currency, rapidly wearing tactile marks, easily removable indelible ink, or the energy-intensive illusions of cryptocurrencies, the money-form itself alienates and deceives.

This booklet is therefore not merely a critique of Indian currency design or policy failures. It is a polemic against the money-form as such. Incremental reforms — better notes, polymer substrates, or digital rupees — cannot resolve its inherent contradictions. True emancipation lies in transcending the money-form altogether, toward a moneyless society grounded in systemic reciprocity and ecological regeneration, where goods are distributed according to need rather than price, and labour becomes life’s prime want instead of wage slavery. Only by seeing through this civilisational illusion can we imagine an economy that truly serves human needs rather than perpetuating alienation.

II. Illusional Optics of Indian Currency: Maya?

The Indian rupee does not present itself to the eye as a single, stable signifier of value. Instead, it appears as a proliferating ensemble of images — shifting colours, varying sizes, multiple designs, evolving security features, and co-existing old and new variants of the very same denomination. What should be a clear, unambiguous medium of exchange reveals itself as a visual and tactile labyrinth. A ₹10 note from 2010 looks markedly different from one printed in 2024; a ₹2 coin minted in the 1990s feels and appears distinct from its 2020s counterpart, yet both circulate legally side by side. This is not mere aesthetic evolution but the optics of illusion — a deliberate or cumulative fragmentation that undermines immediate recognition and erodes public trust.

In Indian philosophical terms, one might call this Maya — the veil of appearances that conceals a deeper, more unstable reality. The rupee’s surface multiplicity masks the underlying fragility, fiscal inefficiency, and structural confusion documented earlier. What the citizen encounters daily is not a coherent national currency but a heterogeneous archive of competing visual regimes: pre- and post-2016 Mahatma Gandhi Series notes, older and newer coin designs, commemorative issues, and subtle variations in paper thickness, ink composition, and tactile markers. The same denomination wears many faces, and those faces frequently deceive.

This section examines the illusional optics of the Indian rupee in detail. It maps the bewildering variety of images and forms that circulate simultaneously, analyses how this heterogeneity generates cognitive and perceptual burdens — especially for senior citizens and the visually challenged — and demonstrates how the illusion of multiplicity serves to conceal deeper contradictions: massive fiscal waste, ecological costs, reduced durability, and the persistent failure of accessibility. What appears as rich visual diversity is, upon closer inspection, a symptom of policy inertia, incremental design choices, and the absence of a unified, enduring visual grammar for the nation’s money.

Building on the personal episodes recounted earlier — the airport deception, the discarded coin, and the elderly vendor’s meticulous scrutiny — the following pages offer a systematic anatomy of this optical illusion. By laying bare the heterogeneous images of the rupee, we expose how the money-form itself, in its Indian avatar, functions not as a transparent medium but as a site of perceptual instability and everyday alienation. The rupee’s Maya is not accidental; it is structurally produced. Only by seeing through it can we begin to imagine a currency — or a post-currency world — that no longer depends on such illusions.

Take 1: Fragmented Sign-ifiers: Co-existing Designs of the One Rupee Coin

Take 2: The Many Faces of the Two Rupee Coin

Take 3: One Rupee System, Many Appearances: ₹5 and 50 Paise Coin Variations

Take 4: Rs. 10 Coins and Two Kinds of Paper Notes

Rs. 10 coins have at least 14 legal-tender varieties (bimetallic with different edge designs, symbols, and commemorative motifs). Paper notes mainly follow the Mahatma Gandhi series (orange-to-brownish colour); minor variations exist due to printing years and security updates.

A) Rs. 10 coins (various designs):

B) Rs. 10 Notes (co-existing)

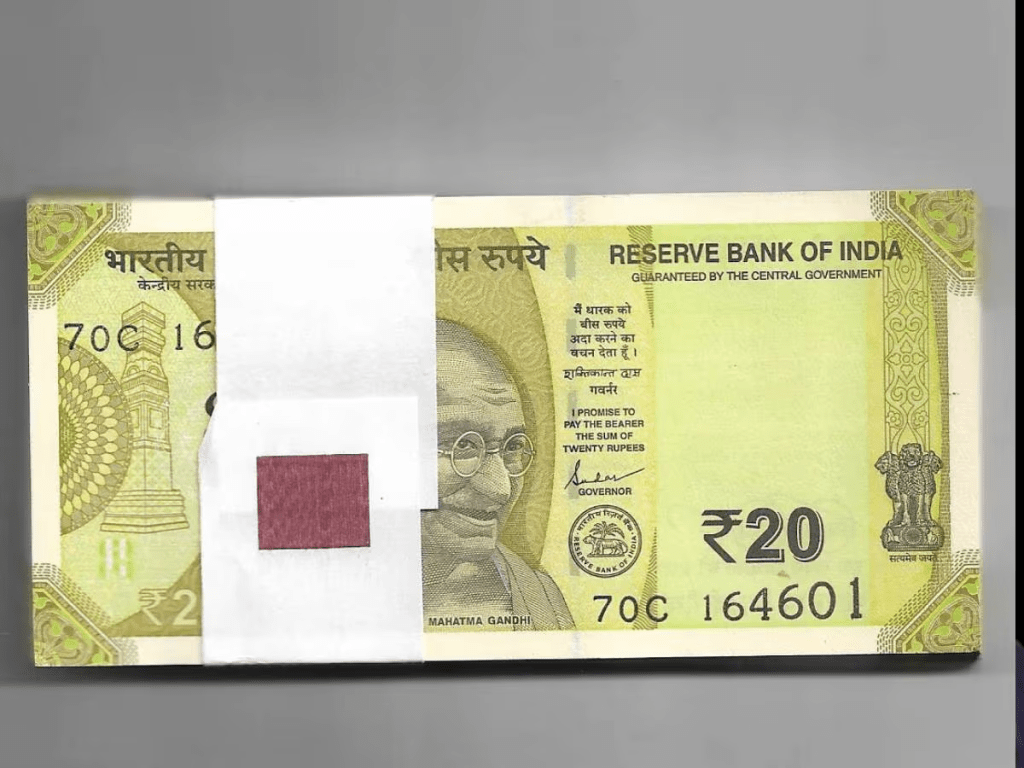

Take 5: Rs. 20 Coins and Two Kinds of Paper Notes

Rs. 20 coins are newer (introduced recently; 12-sided or bimetallic designs, some commemorative). Paper notes have two main types in circulation: older reddish designs and the updated 2019+ greenish-yellow version with enhanced features.

A) Rs. 20 coins:

B) Rs. 20 paper notes (co-existing):

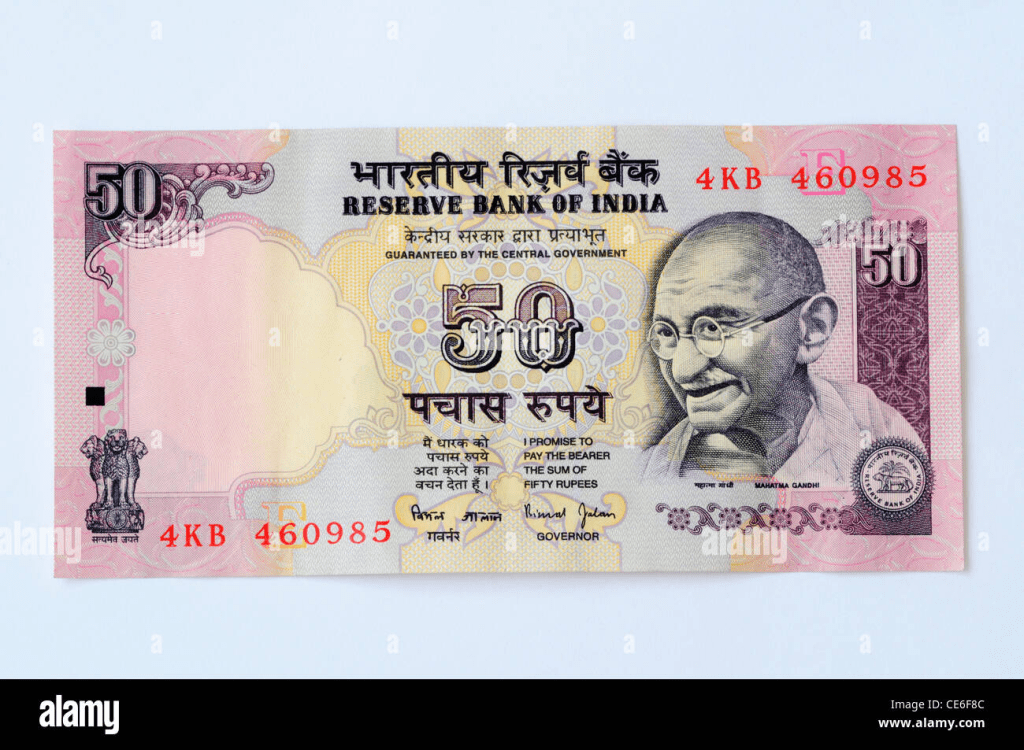

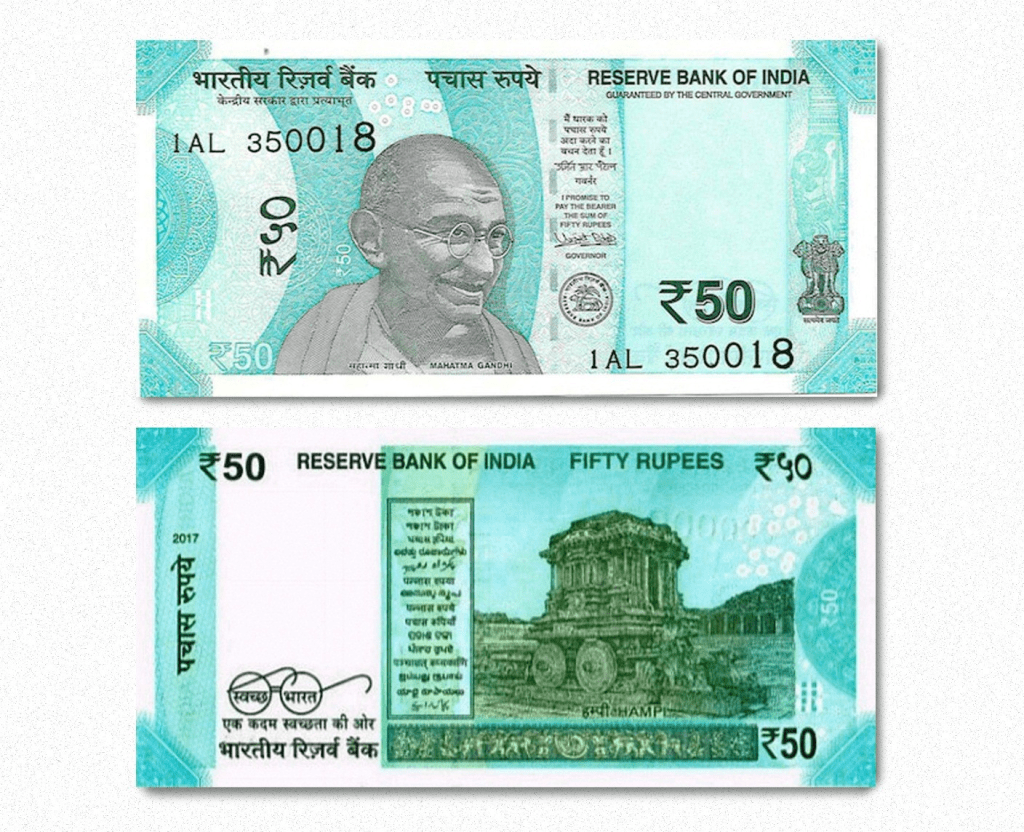

Take 6: Two Types of Rs. 50 notes

Current Mahatma Gandhi series (pink) with variations in reverse motifs (e.g., older vs. 2017 Hampi-themed) co-exist.

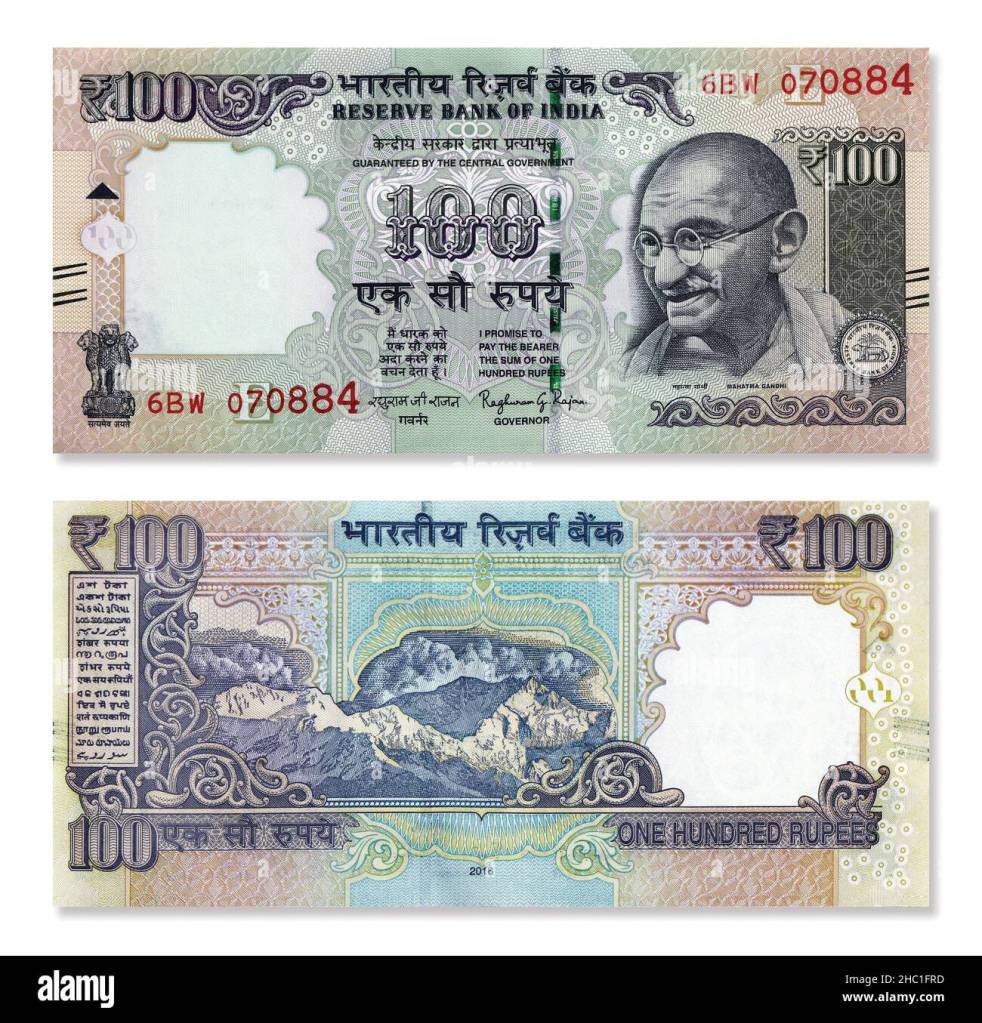

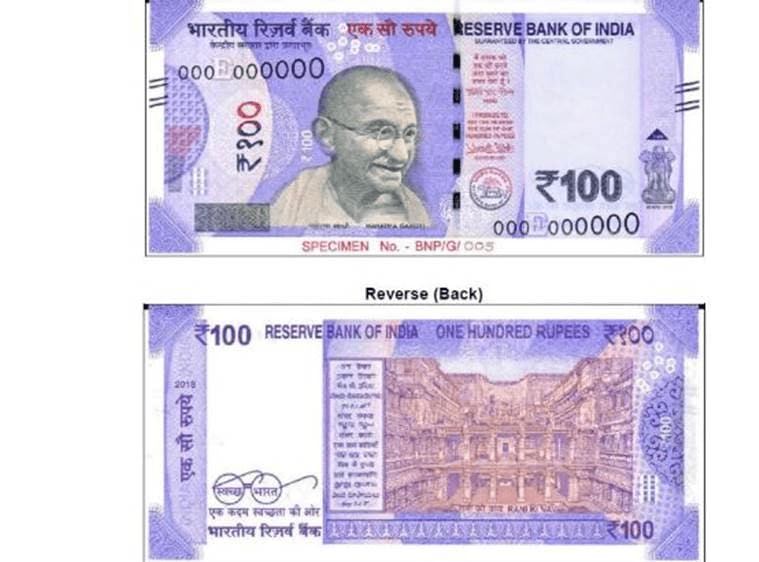

Take 7: Two Types of Rs. 100 notes (Coexisting)

Mahatma Gandhi series (purple/lavender) with design and security updates across printing years; older and newer variants circulate together.

All images show genuine circulating or legal-tender examples. Older designs still remain valid unless officially withdrawn, thereby adding to the confusion.

III. Everyday Perceptual Confusion: The Burden of Heterogeneous Currency on Senior Citizens and the Visually Challenged

The contemporary Indian currency system, administered by the Reserve Bank of India, presents a paradox: while it aspires to inclusivity through features like the Mahatma Gandhi portrait and incremental accessibility additions, its visual heterogeneity across denominations and series produces significant confusion among users—most acutely for senior citizens and visually challenged persons. This confusion is not incidental; it is structurally embedded in the coexistence of multiple designs, evolving iconography, and inconsistent sensory cues. What should be a seamless medium of exchange instead functions as a fragmented visual and tactile puzzle, forcing millions to navigate daily transactions with heightened cognitive effort and risk of error.

A. Structural Origins of Currency Heterogeneity

(a) Coexistence of Multiple Series

India’s monetary system continues to permit the simultaneous circulation of pre-2016 Mahatma Gandhi Series notes, post-2016 Mahatma Gandhi New Series notes, and a wide array of older and newer coin designs. Unlike the Eurozone or the United States, which enforce phased withdrawal of older variants, India grants indefinite legal tender status to legacy designs. As a result, identical denominations differ markedly in size, colour intensity, reverse imagery (monuments, heritage sites, or abstract motifs), typography, security features, and even subtle details such as inset letters and governor signatures.

In 2025–2026, this layered visual economy remains evident: older Mahatma Gandhi Series notes (pre-2016) still circulate alongside newer ones; within the New Series itself, batches with varying inset letters and updated signatures coexist; and coins minted over the past two decades — including pre-2011 designs, the 2011–2019 series, and recent Azadi Ka Amrit Mahotsav (AKAM) variants — appear side by side in everyday transactions. A ₹10 note or coin from 2010 can thus look and feel strikingly different from its 2024–2025 counterpart, yet both remain fully legal tender, making denomination recognition context-dependent rather than absolute.

(b) Incremental Design Philosophy

The Reserve Bank of India’s approach has remained incremental and additive rather than radical and standardised. New features — such as the ₹ symbol, enhanced security threads, tactile marks, or updated heritage motifs — are layered onto existing templates without retiring prior variants. This produces “denominational ambiguity”: while the face value is legally stable, perceptual identification is unstable. Users must rely on comparative memory rather than instant recognition, turning a simple transaction into an exercise in visual and cognitive effort.

B. Cognitive and Perceptual Burdens

(a) Visual Similarity Across Denominations

Several denominations share overlapping visual cues that erode quick differentiation. ₹10 and ₹20 notes have historically occupied similar warm colour palettes in the orange-red spectrum, while ₹50 and ₹100 notes differ only subtly — one pinkish, the other lavender — without strong brightness or contrast gradients. Coins in the ₹1, ₹2, and ₹5 range frequently converge in metallic tone (silver-grey or bi-metallic) and near-identical physical diameters.

For users with reduced visual acuity due to aging, cataracts, or macular degeneration, these distinctions collapse into perceptual equivalence. What appears as “a small brownish coin” or “a reddish note” no longer reliably signals value. In practice, this leads to frequent misidentification: shopkeepers accepting a ₹10 note as ₹20, customers handing over ₹5 coins believing they are ₹2, and senior citizens overpaying or receiving incorrect change because the notes or coins “look almost the same.”

(b) Memory Load and Recognition Failure

Currency recognition depends on learned associations (colour → value), size heuristics, and tactile familiarity. Frequent redesigns and the coexistence of multiple variants disrupt these mental models, resulting in recognition latency, higher error rates, and increased dependence on external validation (asking others, using phone apps, or seeking assistance). For senior citizens — many experiencing age-related cognitive slowing or mild decline — everyday cash transactions become sources of anxiety and potential financial loss.

(c) Breakdown of Tactile Hierarchy

Although newer notes include raised printing and identification marks, these features wear quickly, vary in placement across series, and offer limited differentiation. Coins lack a consistent tactile taxonomy: shape variations (e.g., polygonal ₹2 or 12-sided ₹20) are not uniformly applied, and edge patterns remain insufficiently distinct. Touch-based identification is therefore unreliable, especially for the visually impaired, who cannot fallback on visual cues.

C. Accessibility Deficits for Visually Challenged Users

(a) Partial Compliance with Inclusive Design

While some efforts exist — such as tactile marks on newer notes — they fall short of universal design principles. There is no consistent tactile coding system across all notes and coins, inadequate contrast ratios in older variants, and limited integration of assistive technologies (e.g., NFC or standardised audio cues). Legacy currency thus remains largely inaccessible, creating a two-tier system that favours users of the newest issues.

(b) Dependence on External Technologies

Visually impaired users are often pushed toward mobile recognition apps or third-party tools. This introduces new barriers: technological dependency, privacy concerns when scanning financial instruments, and digital inequality, as not everyone possesses a smartphone or the required literacy.

D. Socio-Economic Consequences of Currency Confusion

(a) Increased Vulnerability to Exploitation

The persistent ambiguity exposes users — particularly senior citizens — to accidental mispayment, under- or over-change, and opportunistic exploitation by vendors who capitalise on hesitation. This erodes personal autonomy and dignity in routine transactions.

(b) Erosion of Monetary Trust

When citizens cannot reliably identify their own currency, trust shifts from the money itself to intermediaries. This subtly undermines public confidence in the monetary system as a credible and inclusive institution of the state.

E. The Semiotics of Currency: When Symbols Fail

Currency functions as a semiotic system — a visual language of value. In India, this language has become polyphonic yet incoherent, with multiple “dialects” (pre- and post-2016 series, commemorative and AKAM coin variants) coexisting without a dominant grammar. The result is semiotic overload: excessive variation obscures the core meaning (face value), turning the rupee into a source of interpretive labour rather than a transparent medium.

F. Toward a Normative Framework for Reform

(a) Visual Standardization: Adopt a strict “one denomination, one dominant colour family” policy with clear size gradation and elimination of overlapping palettes.

(b) Robust Tactile Encoding: Introduce unique, durable edge patterns for coins and standardised, wear-resistant tactile markers on notes, placed consistently across all series.

(c) Phased Withdrawal of Legacy Designs: Enforce time-bound, non-disruptive withdrawal of older variants, supported by nationwide awareness campaigns.

(d) Assistive Integration: Embed optional machine-readable markers (e.g., standardised codes readable by dedicated apps) that augment, rather than replace, inherent accessibility.

G. De-sign of Indian Currency: Trivial Inconvenience or Systemic Accessibility Failure?

The confusion generated by India’s heterogeneous currency is not a minor inconvenience — it is a systemic accessibility failure rooted in design fragmentation and policy inertia. By allowing multiple visual regimes (old and new notes, diverse coin motifs from different decades, and even recent AKAM variants) to coexist without unifying logic, the system imposes disproportionate cognitive, perceptual, and emotional burdens on its most vulnerable users.

For a currency to be truly inclusive, recognition must be immediate, unambiguous, and independent of external aid. Until this clarity is achieved, the Indian rupee will continue to function not only as a medium of exchange but also as a daily site of uncertainty, alienation, and quiet exclusion for millions of senior citizens and visually challenged persons.

IV. Rigorous, Data-Backed Breakdown of Taxpayer Expenditure on Indian Currency

The contemporary Indian currency system — managed by the Reserve Bank of India (RBI) for notes and the Ministry of Finance (via SPMCIL) for coins — entails a substantial annual fiscal commitment ultimately borne by the public. While seigniorage generates implicit profits for the state, the upfront costs of printing, minting, logistics, and frequent replacement represent real public expenditure. Below is a precise analysis based primarily on the RBI Annual Report 2024-25 and corroborated official sources.

A. Institutional Structure

- Paper Notes: Printed exclusively under RBI authority through Bharatiya Reserve Bank Note Mudran Pvt. Ltd. (BRBNMPL, presses at Mysuru and Salboni) and Security Printing and Minting Corporation of India Ltd. (SPMCIL). Costs are borne by the RBI from its balance sheet and recovered through seigniorage, with surplus profits transferred to the government.

- Coins: Minted by the Government of India at four India Government Mints (Mumbai, Kolkata, Hyderabad, Noida) operated by SPMCIL. Costs are directly funded through the Union Budget via the Consolidated Fund of India — explicit taxpayer expenditure.

B. Total Annual Expenditure (FY 2024-25)

- Security Printing (Notes): ₹6,372.8 crore, a 24.9% increase from ₹5,101.4 crore in FY 2023-24. This reflects higher indent amid 5.6% volume growth and 6% value growth in banknotes in circulation.

- Coins: Exact minting costs are not separately itemised in recent reports but form part of SPMCIL operations. In FY 2023-24, SPMCIL supplied ~1,205.64 million circulation coins; the coin component remains structurally loss-making at lower denominations. Combined notes + coins expenditure has historically hovered around ₹6,700–₹6,725 crore.

Context on Circulation (as of early 2026): Currency in Circulation (CiC) reached a record ~₹40 lakh crore by January 2026 (up 11.1% YoY). Notes dominate at 98.99% of total currency value, coins at 0.98%, and the digital rupee (e₹) at a negligible 0.03%. Despite explosive digital growth — with monthly UPI transactions reaching ~₹28 lakh crore (roughly 70% of total CiC in a single month) — physical cash continues to expand in absolute terms while its share of GDP has declined to ~11.2%. This highlights a dual-track economy: cash persists for store-of-value, small retail, and rural transactions, while digital handles a rising proportion of everyday payments.

C. Denomination-Wise Printing Costs (Paper Notes)

Approximate per-note costs (derived from RBI data, RTIs, and consistent industry references):

| Denomination | Printing Cost per Note (₹) | Key Cost Drivers |

|---|---|---|

| ₹10 | 0.96 | Basic security features |

| ₹20 | 0.95 | Basic security features |

| ₹50 | 1.13 | Moderate ink/complexity |

| ₹100 | 1.77 | Enhanced security threads |

| ₹200 | 2.37 | Higher paper/ink quality |

| ₹500 | 2.29 | Advanced features (dominant) |

Key Observations: Lower-denomination notes (₹10–₹50) drive disproportionate reprinting due to short lifespans and high transaction volume (₹10 notes alone account for ~16.4% of note volume). The ₹500 note dominates circulation (~86% by value, 40.9% by volume as of March 2025). RBI has ceased printing ₹2, ₹5, and ₹2,000 notes.

D. Coin Minting Costs

Per-coin costs (based on RTI data from Hyderabad Mint, adjusted for inflation; still used as baseline in 2024-25 discussions):

| Coin | Minting Cost (₹) | Economic Reality |

|---|---|---|

| ₹1 | 1.11 | Loss-making (net loss ~11 paise) |

| ₹2 | 1.28 | Thin margin |

| ₹5 | 3.69 | Viable |

| ₹10 | 5.54 | Efficient |

Critical Insight: ₹1 and ₹2 coins cost more than their face value to produce — a direct fiscal loss absorbed by taxpayers. Although coins last 20+ years, low-denomination production remains structurally unprofitable. SPMCIL supplied ~1,205 million coins in FY 2023-24, with modest growth in 2024-25.

E. Hidden and Structural Costs

Beyond direct printing/minting, significant burdens arise from:

- Material costs (cotton-linen paper, special security inks, metal alloys).

- Security features (micro-text, holograms, threads).

- Logistics, handling, transport to currency chests, and destruction of soiled notes.

- Frequent replacement of fragile low-denomination notes.

Heterogeneity Amplifies Waste: The coexistence of pre-2016 and post-2016 Mahatma Gandhi Series notes, along with multiple coin variants (including recent AKAM issues), requires new plates, inks, and parallel logistics. This incremental design philosophy — layering features without retiring legacy variants — duplicates effort and inflates costs without improving usability.

F. Seigniorage vs. Real Public Burden

Seigniorage remains high (e.g., a ₹500 note costing ~₹2.29 yields massive implicit profit). However, frequent redesigns, replacement cycles for low-denomination notes, and loss-making coins create genuine fiscal drag. Note printing costs surged ~59% from FY 2021 to FY 2024-25, outpacing the ~36% growth in note supply — a clear signal of structural inefficiency.

G. Dual Fiscal Paradox and Socio-Economic Implications

India’s currency system reveals two paradoxes:

- Paper notes are extremely cheap per unit relative to face value, yet aggregate costs are high due to massive volume and rapid wear of low-denomination notes.

- Coins are structurally inefficient at lower denominations yet remain essential for retail cash transactions in a predominantly physical economy (notes + coins still form the overwhelming bulk of CiC at ~₹40 lakh crore).

This fragmentation — old and new variants circulating indefinitely — not only drains taxpayer resources but also exacerbates accessibility failures for senior citizens and the visually challenged, forcing reliance on intermediaries or apps and eroding monetary trust.

H. Recommendations

- Enforce “One Denomination = One Dominant Visual/Tactile Signature” with strict colour/size standards and phased withdrawal of legacy designs.

- Introduce durable, standardised tactile encoding and optional embedded assistive markers (e.g., QR/NFC).

- Publish full denomination-wise costs annually and incentivise digital substitution for low-denomination production.

- Create a transparent “Currency Modernisation Fund” to ring-fence coin losses with sunset clauses.

The ₹6,372.8 crore+ spent annually on currency production is not abstract economics — it is a rights and governance issue. Every extra crore wasted on duplicative printing due to heterogeneity is a rupee denied to welfare or infrastructure. Until visual/tactile unity is achieved, the Indian rupee will remain both fiscally wasteful and socially discriminatory. A truly inclusive currency must be immediately recognizable by all citizens, not just the sighted and digitally literate.

V. The Lifecycle of the Obliviated ₹2000 Banknote: A Case Study

The ₹2000 banknote — rushed into existence in November 2016 and quietly withdrawn from circulation in May 2023 — stands as a damning testament to the Reserve Bank of India’s and the Government’s pattern of reckless, top-down monetary engineering. Born in the panic of demonetisation and discarded after a mere seven years, this short-lived denomination exemplifies policy flip-flopping, institutional opacity, and the quiet socialisation of public costs. What was touted as a pragmatic solution became yet another expensive experiment imposed on citizens, with the real burden ultimately falling on taxpayers while the state hid behind seigniorage rhetoric and legal technicalities.

A. Birth: Panic-Driven Remediation (2016)

The ₹2000 note was introduced on 10 November 2016 under Section 24(1) of the RBI Act, 1934, just two days after the catastrophic demonetisation of ₹500 and ₹1,000 notes that wiped out ~86% of currency in circulation. The official rationale was “rapid remonetisation” to ease the acute cash crunch caused by the government’s own reckless decision.

Higher denomination notes allowed the printing presses to inject value faster with fewer physical units. At an approximate printing cost of ₹3.54–4.58 per note, the cost per ₹1,000 of value was lower than for smaller denominations, delivering massive seigniorage windfall to the RBI. Yet this “efficiency” was illusory — a desperate patch for a self-inflicted wound. The note was never designed for long-term use; it was explicitly a temporary bridge, revealing the ad-hoc nature of the entire exercise.

B. Death: Quiet Obsolescence and the “Clean Note” Facade (2023)

In May 2023, the RBI announced the withdrawal of the ₹2000 note from active circulation — not formal demonetisation, but a calibrated retirement. By early 2026, over 98.4% of the notes (valued at ~₹3.56 lakh crore at the time of announcement) had returned, leaving negligible circulation.

The reasons cited were telling: retail rejection due to change-making difficulties, widespread hoarding rather than transactional use, and the completion of remonetisation. The RBI wrapped the decision in the respectable cloak of its “Clean Note Policy,” claiming the note had simply reached the end of its 4–5-year lifespan. In reality, the ₹2000 note had become a symbol of policy failure — introduced in haste, largely unused in daily commerce, and abandoned once it outlived its narrow utility.

C. The Cost Question: Legal Fiction vs Substantive Public Burden

Under Sections 22 and 24 of the RBI Act, 1934, the RBI formally bears the printing costs on its balance sheet. Seigniorage (face value minus production cost) flows back to the government as surplus transfers under Section 47. Coins are directly funded through the Consolidated Fund of India, but notes enjoy convenient “off-budget” treatment.

This distinction is largely cosmetic. Every rupee spent on printing, logistics, collection, verification, transportation, and destruction of soiled ₹2000 notes ultimately reduces the RBI’s surplus transferred to the government — meaning the burden is indirectly borne by taxpayers. The Supreme Court’s 2023 demonetisation judgment upheld procedural powers but offered no meaningful scrutiny of these diffused fiscal costs, allowing the state to continue such experiments with impunity.

D. Economic Paradox and Wasted Resources

The ₹2000 note embodied a grotesque paradox: cheap and efficient to print, yet almost useless in circulation. It became a hoarding instrument for the informal economy and black money rather than a medium of exchange. Its introduction triggered a massive spike in security printing expenditure (₹7,965 crore in FY 2016-17, a 133% jump), while its withdrawal contributed to sustained high replacement costs in later years.

Data Table 1: ₹2000 Notes in Circulation

| Year (as on 31 March) | Volume (crore pieces) | Value (₹ crore) |

|---|---|---|

| 2017 | 329 | 6,57,063 |

| 2018 | 336 | 6,72,642 |

| 2019 | 329 | 6,58,199 |

| 2020 | 274 | 5,47,952 |

| 2021 | 245 | 4,90,195 |

| 2022 | 214 | 4,28,394 |

| 2023 | 181 | 3,62,220 |

| May 2023 | ~178 | 3,56,000 |

(98.4%+ returned by early 2026, with residual circulation barely ₹5,500–5,900 crore.)

Data Table 2: RBI Security Printing Expenditure Trend (₹ crore)

| FY | Total Printing Cost | % Change (YoY) | Context |

|---|---|---|---|

| 2020-21 | ~4,000 | — | Post-peak stabilisation |

| 2023-24 | 5,101.4 | — | Withdrawal phase begins |

| 2024-25 | 6,372.8 | +24.9% | Replacement printing surge |

E. Critical Evaluation: A Textbook Case of Policy Arbitrariness

The ₹2000 episode is not prudent monetary management — it is fiscal roulette played with public resources. Introduced overnight as a panicked “bridge,” it was discarded seven years later under vague bureaucratic rhetoric. The state celebrated seigniorage gains while concealing the full lifecycle costs: printing, hoarding, idle circulation, collection, destruction, and replacement printing of other denominations.

This mirrors the broader tragedy of the 2016 demonetisation — a massive, poorly planned shock that caused enormous economic disruption, productivity losses, and indirect costs running into lakhs of crores, all while ordinary citizens bore the brunt. The ₹2000 note was both a symptom and a driver of that fiasco. Its lifecycle reveals the same dangerous pattern: short policy horizons, design without longevity, incremental chaos, and costs quietly socialised onto citizens without transparency or accountability.

F. The Tragedy and the Demand for Radical Reform

The ₹2000 note was a monetary instrument born of crisis and retired by redundancy — a cautionary tale of how top-down engineering burdens the public while delivering little lasting benefit. Its costs, though formally booked by the RBI, ultimately drain the Consolidated Fund and constrain public spending.

Until the RBI and Government are forced to publish full, granular, denomination-wise lifecycle cost accounting and conduct mandatory “Currency Lifecycle Impact Assessments,” such wasteful experiments will continue. The rupee does not belong to the RBI’s experimental laboratory or to transient policymakers — it belongs to the people. Enough with these costly illusions of monetary sovereignty. The ₹2000 saga exposes the deeper civilisational Maya: a currency system that claims efficiency while repeatedly extracting public resources through opaque, arbitrary, and ultimately futile interventions.

AN OPEN LETTER TO MODIJI: THE HORNS OF THE DEMONETIZATION DILEMMA

VI. Historical Parallels: Tughlaq’s Currency Experiment (1329–1332) and the 2016 Demonetization – Two Grand Monetary Failures

The short, disastrous life of the ₹2000 note did not emerge in a historical vacuum. Its sudden birth in November 2016 and equally sudden withdrawal in 2023 eerily echo one of medieval India’s most notorious monetary disasters: the token currency experiment of Muhammad bin Tughlaq (r. 1325–1351).

In 1329–1330, facing a depleted treasury after costly military campaigns and grandiose public works, Sultan Tughlaq ordered the mass minting of copper and brass coins. These low-intrinsic-value tokens were declared legal tender at par with the silver tanka — the empire’s established high-value currency. The stated aims sounded visionary: expand the money supply without the expense of precious metals, stimulate trade and agriculture, and finance imperial ambitions. Mints were established across the realm, and the sultan himself allegedly supervised designs to prevent forgery.

The policy imploded within two to three years. Because the copper tokens had negligible intrinsic value, counterfeiters flooded the market with near-identical coins produced in homes and workshops. Inflation exploded, trade collapsed, and public trust evaporated. Peasants and merchants hoarded silver and gold, refusing the new tokens. Contemporary chroniclers Ibn Battuta and Ziauddin Barani documented widespread misery: farmers could not sell their produce, soldiers went unpaid, and the treasury was swamped with worthless copper. By 1332–1333, Tughlaq was forced to withdraw the entire token currency and redeem both genuine and fake coins in silver at ruinous cost to the royal exchequer. Indian historiography has rightly condemned this as the archetype of well-intentioned but catastrophically executed top-down monetary engineering — a classic case of royal hubris meeting economic reality.

Seven centuries later, the 8 November 2016 demonetisation of ₹500 and ₹1,000 notes — which extinguished ~86% of currency in circulation — followed immediately by the emergency introduction of the ₹2000 note, replayed the same tragic script with uncanny precision.

Striking Parallels

- Suddenness and centralised fiat: Tughlaq’s decree was issued by royal command; the 2016 decision was taken by the Union Cabinet on RBI recommendation with minimal public or parliamentary debate. Both bypassed the gradualism and preparation essential for any successful monetary change.

- Mismatch between ambition and capacity: Tughlaq underestimated counterfeiters’ ingenuity; the 2016 exercise grossly underestimated India’s overwhelmingly cash-dependent economy, the limited capacity of printing presses, and the deep rural–urban digital divide. The result in both cases was prolonged cash starvation and acute disruption of daily life.

- Massive public hardship disguised as reform: Ordinary citizens bore the heaviest burden. Tughlaq’s subjects faced famine-like conditions in parts of the empire; post-2016 India witnessed long queues, lost wages, disrupted supply chains, spikes in distress, and an estimated 1.5 million job losses in the informal sector.

- Fiscal opacity and ultimate cost to the public: Tughlaq drained his treasury by redeeming worthless copper in silver; in 2016–17, RBI security printing expenditure surged 133% to ₹7,965 crore, while the government’s dividend from the RBI collapsed by nearly ₹35,000 crore in a single year. Both experiments transferred enormous costs onto the public purse while policymakers claimed visionary success.

- Symbolic legacy of failure: Tughlaq’s copper tokens became synonymous with royal folly; the ₹2000 note, introduced as a temporary bridge, was quietly retired after seven years, having largely functioned as a hoarding tool rather than a circulating medium.

Statisticized Failure of the 2016 Demonetisation The 2016 exercise stands exposed as an unmitigated disaster by its own official metrics. Of the ₹15.44 lakh crore in demonetised notes, 99.3% (₹15.31 lakh crore) returned to the banking system, rendering the primary goal of flushing out black money a spectacular failure. Instead of taxing undeclared wealth, the policy largely enabled money laundering through banks, with only a minuscule fraction (~0.7%) not returned.

Economically, the shock was severe: GDP growth dipped by an estimated 1–2 percentage points in the affected quarters (with some independent estimates, using night-light data, suggesting up to 2.5% contraction in the immediate term). Industrial production and consumer durable sales fell sharply (by ~30% in some segments), informal-sector employment suffered massive losses, and the labour force participation rate dropped dramatically. Far from curbing black money, counterfeit notes, or terror financing in any meaningful way, the move delivered widespread hardship while currency in circulation eventually surpassed pre-demonetisation levels.

Neither experiment achieved its stated objectives — Tughlaq failed to create a stable expanded money supply, and 2016 failed spectacularly to eliminate black money — yet both left behind deep institutional distrust and economic scars.

The ₹2000 note episode is therefore not an isolated modern blunder but the latest iteration of a recurring Indian tragedy: grandiose monetary experiments imposed from above, executed with shocking disregard for ground realities, and ultimately paid for by ordinary citizens. From Tughlaq’s copper tankas forced upon a sceptical populace to the 2016 demonetisation and its short-lived ₹2000 offspring, the same fatal flaw persists — the arrogant belief that state fiat can instantly reshape the monetary system without regard for trust, circulation patterns, or everyday usability.

This historical continuity exposes the deeper civilisational illusion at the heart of Indian currency management: repeated sacrifices of long-term durability, accessibility, and fiscal prudence at the altar of short-term political expediency and administrative hubris. Until this dangerous pattern is broken — through genuine transparency, standardised durable design, rigorous public consultation, and an end to ad-hoc experimentation — the rupee will continue to function not as a reliable medium of exchange, but as a recurring site of policy-induced confusion, waste, and quiet violence against the very people it claims to serve.

VII. The Perceived Fragility of New Indian Banknotes

The widespread observation that post-2016 Mahatma Gandhi New Series notes feel thinner, smoother, and markedly more fragile than the older Mahatma Gandhi Series is shared by countless users across India. Many report that these notes crease easily, tear at the edges, soil rapidly, and lose their characteristic crisp crackle far sooner than their predecessors, particularly in lower denominations that see frequent handling.

This perception is not mere nostalgia. It raises important questions about material durability, design priorities, and the real-world performance of currency issued by the Reserve Bank of India.

A. Material Reality

Indian banknotes are printed on a high-grade security substrate made of 100% cotton fibre (often a cotton-linen rag blend). This material is chosen for its strength, printability, and ability to incorporate advanced security features such as watermarks, security threads, and micro-printing. Grammage typically ranges between 82–90 GSM, with thickness around 100–110 microns. Technically, this remains premium security paper, not low-quality pulp.

B. Why New Notes Feel More Fragile

The sense of reduced robustness stems from deliberate design changes introduced in the Mahatma Gandhi New Series:

- Reduced thickness and grammage to improve processing efficiency, ATM compatibility, and lower material usage.

- Smoother surface finishes and updated ink formulations that enhance visual appeal and security but create a less grippy, more easily soiled surface.

- Smaller overall dimensions compared to older notes, which concentrates mechanical stress on a reduced area and increases vulnerability to folding and edge wear.

- India’s tropical climate — high humidity, heat, and frequent sweat-laden handling — accelerates degradation of the moisture-absorbent cotton substrate.

These changes make lower-denomination notes especially prone to rapid deterioration under normal circulation conditions.

C. Lifecycle Evidence

Banking practice and RBI observations confirm that lower-denomination notes now require replacement more frequently due to soiling and physical damage. Even if the base material meets high-security standards, real-world durability under Indian usage patterns has visibly declined.

D. Policy Design Tension

The current approach reflects a clear trade-off between competing objectives:

| Objective | Design Choice | Consequence |

|---|---|---|

| Cost and processing efficiency | Thinner GSM, smaller size | Reduced tear resistance |

| Enhanced security | Smoother coatings, new inks | Faster soiling and loss of tactile feel |

| Machine compatibility | Optimised dimensions | Lower structural strength |

E. Comparative Perspective: Polymer Alternatives

Many countries have successfully transitioned to polymer (plastic) substrates for superior durability. Australia, the pioneer since 1988, reports polymer notes lasting up to four times longer than cotton-paper equivalents. The United Kingdom and Canada have seen lifespans extended 2.5–5 times, with significant reductions in replacement rates and long-term costs. Polymer offers excellent resistance to moisture, dirt, folding stress, and temperature extremes — advantages particularly relevant in India’s humid conditions.

India conducted limited field trials of ₹10 polymer notes between 2014 and 2018 in selected cities, but has not scaled adoption. As of 2026, the country continues to rely entirely on cotton-based notes, forgoing the proven longevity and efficiency gains demonstrated elsewhere.

F. Policy Critique

The perceived and functional fragility of newer notes is not an accident — it is the predictable result of incremental, cost-driven design choices that favour short-term savings and processing efficiency over long-term robustness. This creates unnecessary “currency churn,” where notes degrade faster than technically necessary, forcing repeated production cycles.

A full shift toward durable polymer or significantly enhanced cotton substrates would deliver measurable improvements in lifespan and performance. Continuing with the present approach reflects policy inertia rather than optimal stewardship of a public good.

G. Legal and Rights Perspective

Under the Rights of Persons with Disabilities Act, 2016, the RBI has a duty to ensure currency design supports accessibility. Rapid wear of tactile features on newer notes undermines this obligation. The Delhi High Court in September 2025 explicitly directed the RBI to address accessibility concerns in note design, reinforcing that systemic flaws affecting usability violate constitutional guarantees of equality and dignity.

H. The Core Paradox

Indian banknotes remain premium security substrates in technical terms. However, post-2016 design shifts have produced notes that feel — and perform — less resilient in everyday Indian conditions. This paradox highlights a deeper tension: a currency engineered for security features and machine efficiency at the expense of human usability and material endurance.

Reform is essential. Transparent lifecycle assessments, mandatory durability standards, and serious consideration of polymer substrates are needed to ensure the rupee serves its users effectively rather than burdening them with prematurely degraded notes. Durability and practical usability must become core obligations of public currency design, not secondary considerations.

VIII. Barriers to Polymer Banknote Adoption in India

The growing perception of fragility in post-2016 cotton-based Indian banknotes naturally directs attention toward polymer (synthetic plastic) substrates as a proven alternative. Countries such as Australia (since 1988), the United Kingdom, Canada, and New Zealand have successfully adopted polymer notes, achieving 2.5–4 times longer lifespans, superior tear and water resistance, cleaner circulation, and significantly lower long-term replacement costs. India itself conducted limited ₹10 polymer note trials in five climatically diverse cities — Kochi, Mysuru, Jaipur, Bhubaneswar, and Shimla — between 2012 and 2017. However, the project was effectively shelved by 2022 and remains dormant as of 2026, with no full-scale rollout despite occasional expressions of intent.

The following analysis examines the multi-dimensional barriers that have blocked adoption, based on RBI and government disclosures, trial outcomes, and expert assessments. These barriers are substantial but reflect a complex mix of technical, economic, infrastructural, and institutional challenges rather than outright impossibility.

(a) Climatic and Technical Durability Barriers (India-Specific)

India’s tropical and sub-tropical conditions — extreme heat exceeding 45°C, monsoon humidity above 80%, dust, and heavy sweat-laden handling — create unique risks for polymer. Bankers and RBI sources have repeatedly cited concerns that polymer substrates can deform, melt, or become brittle under prolonged high temperatures, unlike cotton-linen paper which is more tolerant in short-term exposure. Reports from trials in hotter and drier cities such as Jaipur and Shimla highlighted potential warping or damage, raising fears that compromised polymer notes would complicate public exchange at banks and erode public trust. Additionally, polymer requires precise temperature-controlled storage and handling during printing and distribution — a significant challenge across India’s decentralised mints and currency chests.

(b) Massive Infrastructure and Conversion Costs

Transitioning to polymer would demand wholesale upgrades. Printing presses at BRBNMPL (Mysuru and Salboni) and SPMCIL facilities would need retrofitting or replacement to handle polymer-specific inks, substrates, and security features such as clear windows. ATMs, note-sorting machines, and verification equipment across more than 1.5 lakh bank branches and over 2 lakh ATMs would require recalibration or outright replacement — an exercise estimated in thousands of crores. The supply chain would also need overhaul, with reliance on imported biaxially oriented polypropylene (BOPP) substrates from specialised global suppliers. Although initial per-note production cost is 1.5–2 times higher than cotton, the one-time transition cost is widely cited as the biggest deterrent, far exceeding current annual printing budgets.

(c) Economic and Fiscal Trade-offs

Short-term fiscal pain versus long-term gain creates strong policy hesitation. RBI operates under cost-efficiency mandates, and the immediate burden of polymer conversion would hit its balance sheet upfront, potentially reducing seigniorage transfers to the government. Replacement savings (estimated at 70%+ fewer reprints for low-denomination notes) would materialise only over 4–7 years — well beyond typical policy and budgetary horizons. Environmental considerations add another layer: while polymer production has a higher initial carbon footprint, the net reduction in destroyed notes could favour it long-term. However, the upfront commitment remains politically and fiscally unattractive.

(d) Public Acceptance and Socio-Cultural Barriers

Cotton notes carry a deeply familiar “crackle” and tactile feel ingrained in public memory. Polymer feels smoother, lighter, and distinctly “plastic-like,” which could trigger initial confusion or rejection, particularly among rural users and those accustomed to traditional haptic cues. Trial feedback highlighted concerns about “different handling” and doubts regarding authenticity verification without the familiar paper texture. In a still largely cash-reliant economy, any perceived change in “feel” risks social pushback, heightened fraud perceptions, or hoarding of old cotton notes.

(e) Operational and Security Challenges

Existing verification devices calibrated for cotton would need new protocols for polymer. A prolonged hybrid circulation period (cotton alongside polymer) could increase confusion and temporary forgery risks. Logistics would also change: polymer’s lighter weight aids transport but demands different storage conditions to prevent static or heat damage.

(f) Policy and Institutional Inertia

The RBI’s longstanding preference for incremental improvements to cotton-based notes — adding brighter inks and better coatings rather than radical change — reflects deep risk aversion. The absence of a statutory mandate or dedicated “Currency Modernisation Fund” for polymer adoption further entrenches inertia. The shift toward digital payments (UPI and e-rupee pilots) has additionally deprioritised investment in physical currency durability. As of 2026, the RBI continues to invest in enhancing traditional cotton notes rather than committing to polymer.

Comparative Barrier Summary Table

| Barrier Category | Severity in India | Key Examples/Evidence | Mitigation Potential |

|---|---|---|---|

| Climatic/Technical | High | Heat deformation concerns; trial failures | Climate-specific polymer variants |

| Infrastructure/Capex | Very High | Press & ATM retrofits (thousands of crores) | Phased rollout starting with low denominations |

| Economic/Fiscal | High | Upfront cost vs delayed savings | Long-term lifecycle budgeting |

| Public Acceptance | Medium-High | Change in “feel”; rural/senior resistance | Nationwide awareness campaigns |

| Operational/Security | Medium | Machine recalibration; hybrid circulation risks | Parallel testing with existing stock |

| Policy Inertia | High | Shelved since 2022; digital shift priority | RPwD Act litigation or parliamentary push |

(g) Ecological Costs of Polymer

While polymer notes promise longer lifespans and reduced replacement cycles, their production relies on fossil-fuel-derived biaxially oriented polypropylene (BOPP), entailing a significantly higher upfront carbon footprint, energy consumption, and fossil resource depletion compared to cotton-paper manufacturing. Concerns include potential microplastic pollution at end-of-life, especially in a country like India with limited advanced recycling infrastructure and high plastic waste burden. Although some life-cycle assessments show net environmental gains over time due to fewer reprints, the front-loaded impacts — higher greenhouse gas emissions during raw material extraction and substrate production — remain a serious drawback in India’s context of tropical conditions and underdeveloped closed-loop recycling systems.

Critical Evaluation: These barriers are real, yet largely addressable through a carefully phased and targeted approach — for instance, beginning with low-denomination polymer notes in high-circulation urban and semi-urban areas, as attempted in the earlier trials. The continued reliance on a fragile cotton system, despite its clear limitations in Indian conditions, represents not technical inevitability but a conscious policy choice. Short-term fiscal caution and institutional inertia continue to outweigh long-term efficiency, durability, and inclusion gains.

Without decisive action, India will persist in subsidising a high-churn, rapidly degrading cotton-based currency while forgoing global best practices that have delivered measurable benefits elsewhere. Polymer is not a perfect solution, but the stubborn maintenance of the status quo is a demonstrable failure of vision in durability, cost management, and public service. The time for meaningful modernisation has long passed.

IX. Dollar Imperialism and the Depletion of the Rupee – The External Face of Monetary Fetishism

While the Indian rupee struggles with internal contradictions — fragile notes, confusing coins, fiscal waste, and accessibility failures — its deepest vulnerability lies in its subordinate relationship with the US dollar. The sustained depreciation of the INR against the USD is not a neutral market fluctuation; it is a structural expression of dollar imperialism — the global monetary hierarchy in which the dollar functions as the de facto world reserve currency, enforcing unequal exchange and systematically transferring value from the Global South to the United States.

As of December 2025, the rupee breached the psychologically significant ₹90 mark and hit an all-time low of approximately ₹91.14 by 16 December. This means that more than 91 rupees were required to purchase what one rupee could buy against the dollar in earlier decades. The long-term trajectory is stark: from roughly ₹22 per dollar in the early 1990s to over ₹91 by late 2025 and to ₹94 by March 2026— a depreciation of more than 300 per cent in three decades.

Table: Long-Term Depreciation of the Indian Rupee Against the US Dollar (1990–March 2026)

| Year / Period | Average / End-of-Period Rate (₹ per 1 USD) | Depreciation from 1990 Base (%) | Key Context |

|---|---|---|---|

| 1990 (Early 1990s) | 17.5 | — | Pre-liberalisation era |

| 2000 | 44.9 | +157% | Post-1991 economic reforms |

| 2010 | 45.7 | +161% | Global financial crisis aftermath |

| 2020 | 74.3 | +325% | COVID-19 pandemic impact |

| 2024 (Annual average) | 83.7 | +378% | Post-pandemic recovery |

| December 2025 | 91.14 | +421% | All-time low amid FPI outflows & US tariffs |

| March 2026 (End of FY 2025-26) | ~94.83 | +442% | Record weakness; worst fiscal year drop in over a decade |

A. Key Drivers of Rupee Depletion (Late 2025 – Early 2026)

Several interlocking factors accelerated this slide:

- Massive Foreign Portfolio Investor (FPI) Outflows: In 2025 alone, foreign investors pulled out over ₹1.59 lakh crore from Indian equities, creating intense demand for dollars to repatriate profits and directly weakening the rupee.

- US Tariffs and Trade Deadlock: The imposition of up to 50% tariffs on key Indian exports by the United States brought trade negotiations to a standstill, triggering market panic and further pressure on the currency.

- High Import Bill, Especially Oil: India remains heavily dependent on imported crude oil and electronics. Every spike in global commodity prices or rupee weakening inflates the current account deficit, forcing the economy to acquire more dollars.

- Reduced RBI Intervention: Unlike previous episodes of aggressive dollar sales from reserves, the RBI in late 2025 appeared to allow greater flexibility in the exchange rate, prioritising other macroeconomic objectives over short-term stabilisation.

Despite these pressures, the rupee has paradoxically been one of the relatively better-performing emerging-market currencies against the euro and yen, underscoring that its primary nemesis remains the dollar’s structural dominance.

B. Effects on the Indian Economy and People

The depreciation produces deeply contradictory outcomes:

- Import Inflation: The cost of essential imports — petroleum, electronics, fertilisers, and machinery — rises sharply, feeding into higher domestic prices and eroding the purchasing power of ordinary citizens.

- Export Competitiveness: In theory, a weaker rupee makes Indian goods cheaper abroad. In practice, however, tariff barriers and global slowdowns have limited this benefit, while the pain of higher import costs is felt immediately by consumers and industry.

- Increased Debt Burden: For corporations and the government that have borrowed in dollars, repayment becomes significantly more expensive in rupee terms, raising the risk of financial stress.

- Pressure on Foreign Exchange Reserves: The RBI faces constant tension between defending the currency and preserving reserves for genuine crises.

C. Dollar Imperialism: The Global Monetary Hierarchy

At its core, the rupee’s depreciation reflects the enduring architecture of dollar imperialism. Since the collapse of the Bretton Woods system in 1971, the US dollar has maintained its supremacy not through gold convertibility but through its privileged roles in international trade (especially oil — the petrodollar system), debt issuance, and official reserve holdings. The United States enjoys what Valéry Giscard d’Estaing famously called an “exorbitant privilege”: it can run persistent trade deficits, finance them by printing dollars, and force other nations to hold those dollars as reserves.

This hierarchy was aggressively reinforced through the Washington Consensus and the neoliberal globalised order promoted by the World Bank and IMF from the 1980s onwards. Structural adjustment programmes, conditional loans, privatisation drives, and capital account liberalisation were imposed across the Global South under the guise of “reform.” These neo-imperial mechanisms tied peripheral economies ever more tightly to dollar-denominated debt and volatile portfolio flows. Countries like India were compelled to prioritise dollar earnings, maintain high foreign reserves as insurance, and accept IMF-mandated austerity whenever balance-of-payments crises emerged. The result has been heightened vulnerability to US monetary policy shifts, Federal Reserve interest-rate decisions, and geopolitical manoeuvres.

When the Fed raises rates, capital flees emerging markets toward the safety of US Treasuries, depreciating currencies like the rupee. When the US imposes tariffs or sanctions, the resulting uncertainty further weakens peripheral currencies. The dollar thus acts as a hidden extractor of value: every depreciation forces India to export more real goods, services, and embodied labour merely to maintain the same level of dollar reserves.

Marx’s insight in the Grundrisse acquires fresh global relevance here. Money is never neutral; when one nation’s currency becomes the universal equivalent on a planetary scale, it equates the unequal on an international level. The rupee’s depreciation is not merely a bilateral exchange-rate movement — it is the visible symptom of how the dollar-form subordinates other monies, hiding the transfer of real social labour and ecological wealth from the Global South to the imperial centre.

D. The Illegitimacy of Purchasing Power Parity (PPP)

Mainstream economists and institutions such as the IMF and World Bank routinely invoke Purchasing Power Parity (PPP) to argue that, once adjusted, the rupee is not as weak as the nominal rate suggests and that India’s economy ranks higher globally. Such assertions create a comforting illusion of fairness and equivalence. In reality, PPP is deeply illegitimate as a measure of true economic standing or monetary sovereignty for three fundamental reasons.

First, PPP assumes what it needs to prove — that identical baskets of goods should cost the same everywhere once converted at market rates — while ignoring the structural distortions caused by dollar dominance itself. Second, PPP conceals unequal exchange: as the rupee depreciates from ₹22 to over ₹91 per dollar over three decades, Indian workers and exporters must deliver ever-larger quantities of real goods and embodied labour simply to earn the same amount of dollars needed for debt servicing, oil imports, or technology. Third, PPP naturalises dependency by focusing on domestic price levels rather than the global power relations that determine those prices, erasing the historical and ongoing role of dollar seigniorage, IMF conditionalities, Washington Consensus policies, and the weaponisation of the SWIFT system.

PPP thus performs an ideological function: it converts a relation of subordination into a technical, ahistorical comparison, thereby legitimising the continued hegemony of the dollar.

E. Bretton Woods and the Foundations of Dollar Hegemony

The Bretton Woods system (1944) was never a neutral multilateral order but an American-led settlement designed to institutionalise US financial power in the post-war era. Currencies were pegged to the dollar, which itself was convertible to gold at $35 per ounce. The IMF and World Bank were created to enforce stability while serving US strategic interests. The system collapsed dramatically in 1971 with Nixon’s unilateral suspension of dollar-gold convertibility (the Nixon Shock), ushering in the era of floating exchange rates and pure fiat dollar dominance.

The subsequent neoliberal globalised order — enforced through the Washington Consensus — deepened this subordination. Structural adjustment programmes, debt traps, and capital account liberalisation tied peripheral economies ever more tightly to dollar liquidity. India’s post-1991 liberalisation bears the clear imprint of this neo-imperial framework: periodic balance-of-payments crises, reliance on volatile FPI inflows, and repeated pressure to prioritise dollar earnings over domestic needs.

The rupee’s internal failures — fragile notes, confusing coins, wasteful printing cycles, and accessibility deficits — are therefore compounded and ultimately conditioned by this external subordination. Attempts to “strengthen” the rupee through RBI intervention, capital controls, or modest de-dollarisation efforts treat symptoms rather than the structural reality of a world money system still dominated by the dollar.

The depreciation of the rupee against the dollar is not an isolated economic statistic. It is the external face of the same fetish that turns a bottle of cold drink into Rs. 50 and a nation’s labour into dollars that must be perpetually earned and hoarded. Overcoming dollar imperialism, like overcoming the rupee’s internal contradictions, ultimately points toward the same emancipatory horizon: a world in which money itself — whether rupee or dollar — ceases to be the mediator of human and ecological relations.

X. Ecological Hazards of Cotton-Paper vs. Polymer Banknotes: A Balanced Lifecycle Perspective

The debate over polymer banknotes in India is routinely sanitised into questions of durability and cost. That is a deliberate distraction. The real scandal is ecological plunder. Both the RBI’s current cotton-paper notes and any proposed polymer (biaxially oriented polypropylene or BOPP) substrate inflict serious, measurable environmental violence across their full lifecycle — from raw-material extraction and production through circulation, use, and end-of-life disposal. Life-cycle assessments (LCAs) by the Bank of Canada (2011, updated), Bank of England (2013/2017), and Banco de México (2018) are unequivocal: polymer’s 2.5–5× longer lifespan dramatically slashes total impacts by cutting repeated production cycles. Yet neither option is innocent. In India’s tropical, water-stressed, and waste-poor reality, physical currency itself functions as a hidden engine of ecological destruction — a state-sanctioned machine that externalises its costs onto rivers, soil, air, and future generations while the RBI and Government pretend to manage a “sovereign” monetary system.

A. Ecological Hazards of Cotton-Based Paper Banknotes (Current Indian System)

Indian notes are printed on a high-grade 100% cotton substrate (sometimes with linen/rag content). The material is renewable in name only; the system is environmentally voracious and indefensible at scale.

Major hazards include:

- Water-intensive and pesticide-heavy cotton farming: Conventional cotton cultivation is one of the most water-demanding and chemically toxic crops globally. It drives acute water scarcity, soil degradation, and chemical runoff that causes eutrophication of rivers and lakes. In India’s already parched cotton belts, this upstream theft of water and poisoning of ecosystems is systematic.

- Energy- and chemical-intensive papermaking: Converting cotton linter into security-grade paper consumes massive energy, bleaches, and industrial chemicals, generating wastewater and air emissions.

- High replacement frequency driven by engineered fragility: Low-denomination notes (₹10–₹50, ~31.7% of circulation volume) often last less than 1–2 years in humid, high-circulation conditions. The RBI destroys approximately 15,000 tonnes of unfit notes annually — previously landfilled or incinerated, releasing greenhouse gases from decomposing cellulose and toxic inks/security threads.

- End-of-life pretence: The 2025 shift to repurposing shredded notes into particle boards for furniture is a cosmetic improvement that reduces landfill use and timber demand, but it leaves untouched the massive upstream ecological debt of repeated cotton farming and papermaking.

LCAs consistently show cotton-paper notes carrying higher impacts in global warming potential (GWP), acidification, eutrophication, and land occupation precisely because fragility forces endless reprinting. In plain terms, every fragile rupee note is a quiet act of ecological violence — water stolen, rivers poisoned, carbon emitted — all concealed behind the fetish of “national currency.”

B. Ecological Hazards of Polymer (BOPP) Banknotes

Polymer notes are manufactured from fossil-fuel-derived polypropylene resin formed into durable BOPP film with opacifiers and security features.

Major hazards include:

- Fossil-fuel dependency: Production begins with crude-oil or natural-gas extraction, refining, and energy-intensive polymerization — processes that carry a high upfront carbon footprint, air pollution, and habitat destruction. Opacification and security coatings add further chemical burdens.

- Microplastic and persistence risks: If not properly collected and recycled, polymer can fragment into microplastics that persist in soil and water.

- Higher initial manufacturing impact: Per-note energy and emissions are often higher than cotton before lifespan is factored in.

Yet the decisive advantage is longevity. Independent LCAs confirm clear net superiority:

| Indicator (normalised for equivalent value in circulation) | Polymer Advantage vs Cotton-Paper |

|---|---|

| Global Warming Potential (GWP) | 32% lower (Bank of Canada) / 8–16% lower (Bank of England) / 48.8% lower (Banco de México) |

| Primary Energy Demand | 30% lower (Bank of Canada) |

| Eutrophication, Acidification, Toxicity | Significantly lower across studies |

The longer lifespan cuts production, distribution, and disposal cycles so dramatically that it outweighs the fossil-fuel starting point. The hidden cost of clinging to cotton is therefore not just fiscal — it is an indefensible ecological subsidy paid by the planet and the poor.

C. The Hidden Ecology of Metal Coins

While public outrage focuses on fragile notes, metal coins — the “eternal” backbone of small transactions — carry their own brutal, often invisible ecological burden. India’s ₹1, ₹2, ₹5, and ₹10 coins are minted from stainless steel, cupro-nickel, and aluminium-bronze alloys at four government mints. Though they last 20–40 years, the upstream destruction is catastrophic.

- Resource-intensive mining: Copper and nickel extraction generates vast tailings, acid mine drainage, heavy-metal pollution, deforestation, and biodiversity loss. Stainless steel relies on chromium and nickel; aluminium refining produces toxic red mud waste and is extremely electricity-hungry.

- Production inefficiency: Low-denomination coins (₹1 and ₹2) already cost more to mint than their face value. Many are lost, discarded, or hoarded — sunk ecological costs of metals extracted, refined, and minted only to vanish from circulation.

- End-of-life failure: No national coin-recycling programme exists. Withdrawn coins are melted at mints or leak into informal scrap markets and landfills, risking long-term soil and groundwater contamination.

Coins thus expose the same paradox as notes: fiscally and ecologically wasteful at low denominations, yet kept alive for the cash-dependent informal economy and for tactile accessibility.

D. Blockchain Environmental Impact: A Rigorous Comparison

Blockchain technology, particularly cryptocurrencies, adds another layer to the ecological ledger of money. Its footprint varies dramatically by consensus mechanism.

Bitcoin (Proof-of-Work dominant) remains an environmental disaster:

- Annual electricity consumption: 138–204 TWh (comparable to the national consumption of Thailand or Argentina) — roughly 0.5–0.7% of global electricity.

- Carbon emissions: 48.6–64.4 Mt CO₂e/year (up to 110–170 Mt for all crypto-assets), equivalent to the annual emissions of Greece or Jordan.

- A single Bitcoin transaction can emit hundreds of kg CO₂e — the equivalent of 350,000+ Visa transactions or weeks of average household energy use.

- Mining hardware generates over 21 kt of e-waste annually, comparable to the IT waste of small countries.

Ethereum (Proof-of-Stake post-2022 “Merge”) demonstrates that blockchain can be radically greener: energy use dropped 99.95%+, with per-transaction emissions collapsing from ~109 kg CO₂e to ~0.01 kg CO₂e.

Comparative Ecological Burden Table

| Dimension | Physical Currency (Cotton/Coins) | UPI/Digital Payments & e-Rupee | Blockchain (Bitcoin PoW) | Blockchain (Ethereum PoS) |

|---|---|---|---|---|

| Annual Energy Use | High indirect (repeated printing + mining for coins) | Very low | Extremely high (138–204 TWh) | Negligible |

| Carbon Emissions | Moderate-high (farming + replacement cycles) | Very low | 48–64+ Mt CO₂e/year | Very low |

| Other Hazards | Water stress, mining pollution, waste | Device e-waste, data-centre cooling | Massive e-waste, heat pollution | Minimal |

| India-Specific Reality | Fragility drives churn; 15,000 tonnes notes destroyed yearly | Ecological win but digital divide | Global PoW volatility strains energy markets | Aligns with green goals |

E. Comparative Ecological Burden and Critical Evaluation

When normalised over their functional lifespan, coins appear more “efficient” than fragile paper notes. A single ₹5 coin may serve millions of transactions over two decades, whereas a ₹10 note might be replaced every few months. Yet this longevity is offset by the high upfront environmental cost of virgin metal extraction. LCAs of coinage in other countries show significantly higher impacts in abiotic resource depletion, toxicity, and mining-related habitat destruction compared with paper or polymer notes.

In India’s context, the ecological load is compounded by reliance on imported nickel and copper, a coal-heavy energy mix for smelting, and the complete absence of systematic urban mining or coin-recycling infrastructure.

F. Comparative Life Cycle Assessment (LCA) Insights (Key Findings from Global Studies)

Independent studies normalise impacts for the same amount of currency value over time:

- Global Warming Potential (GWP/CO₂e): Polymer typically 8–50% lower.

- Energy Use: Polymer uses 30%+ less over the lifecycle.

- Other Categories: Lower eutrophication, acidification, toxicity, and resource depletion for polymer in most assessments.

- Sensitivity Factor: Lifespan is decisive — longer polymer life reduces production/distribution repeats, outweighing higher per-note manufacturing impacts.

In India’s tropical, humidity-driven reality, cotton’s water footprint and frequent replacements widen the gap decisively in favour of polymer.

G. India-Specific Context and RBI Efforts

The RBI produces ~15,000 tonnes of shredded note briquettes yearly. Traditional disposal (landfill/incineration) was environmentally catastrophic. The 2025 particle-board repurposing initiative is a step forward but does not touch the upstream farming impacts. No large-scale polymer adoption yet means India continues subsidising ecological failure.

H. Critical Evaluation and Policy Implications

Neither substrate is ecologically neutral. Cotton-paper is renewable in name but a machine of repeated ecological violence: water theft, chemical poisoning, and carbon debt multiplied by engineered fragility. Metal coins externalise mining scars and toxic legacies far from public view. Polymer carries fossil-fuel sins at birth but delivers decisive net reductions in total harm through longevity. Blockchain PoW is climate arson on an industrial scale; PoS versions prove that decentralised money need not destroy the planet.

Money, as Marx warned in the Grundrisse, equates the unequal and conceals the real social and ecological relations of production. A bottle of cold drink priced at Rs. 50 hides not only living labour but also cotton-field depletion, mining scars, fossil-fuel emissions, microplastic time-bombs, and the energy waste of Bitcoin mining embedded in the very notes, coins, or crypto used to buy it.

The rupee system is not merely broken — it is an active participant in ecological plunder. The RBI and Government, by clinging to fragile cotton and resource-heavy metal while rejecting proven polymer solutions, are complicit in this plunder. An India-specific full-cradle-to-grave LCA, scaled polymer pilots with mandatory closed-loop recycling, hybrid substrates as interim measures, accelerated e-rupee rollout with accessibility safeguards, and strict regulation of PoW crypto are the bare minimum required.

Anything less is not monetary policy — it is state-sponsored ecological vandalism dressed up as sovereignty. True sustainability demands moving beyond both fragile cotton and resource-heavy metal toward systems that no longer conceal the real ecological cost of money itself. The rupee must stop being an instrument of hidden environmental violence. The choice is no longer technical — it is moral and civilisational.

XI. Comparative Analysis: Physical Indian Currency (Paper Notes & Coins) vs. Risky Digital Payments, Central Bank Digital Currency (CBDC e-Rupee), and Cryptocurrency (with Evolution)

The physical rupee system—plagued by fragility of post-2016 notes, high replacement costs (₹6,372.8 crore printing in FY 2024-25), ecological burdens (cotton farming water stress + destruction waste), and accessibility failures for seniors/visually impaired—represents a tangible but inefficient medium of exchange. Digital alternatives (UPI-style payments, e-rupee CBDC, and private cryptocurrencies) promise lower operational costs, speed, and reduced physical waste, but introduce new risks: cyber fraud, digital exclusion, volatility, privacy erosion, and massive energy footprints. Below is a rigorous, data-backed comparison as of early 2026, integrating ecological hazards, fiscal/public costs, usability, and accessibility. It highlights why neither is a perfect substitute and why hybrid reforms (e.g., durable polymer notes + safe digital layers) remain essential.

A. Digital Payments (UPI, Wallets, IMPS) vs. Physical Currency UPI dominates India’s digital ecosystem (81% of retail digital transactions in FY 2024-25; 20+ billion monthly transactions by Feb 2026). It eliminates most physical printing/logistics but shifts risks online.

- Durability and Usability: Digital has infinite “lifespan” (no wear/tear) and instant transfers. Physical notes degrade rapidly in humid conditions, requiring constant replacement—especially low-denomination ₹10–₹50 notes (31.7% of volume). Digital excludes offline/rural users and those without smartphones (digital divide affects ~40% of population, including most seniors/visually impaired).

- Risks: Extremely high fraud exposure. FY 2024-25: 12–13 lakh UPI cases, ₹981–1,087 crore losses (34% YoY rise). Early FY 2026: ₹805 crore across 10.64 lakh incidents (fake collect requests/QR swaps dominate). Victims often lose ₹12,000–45,000 per case with limited RBI compensation for small frauds. Physical cash has zero cyber risk but vulnerability to counterfeiting/theft.

- Ecological Hazards: Strongly favorable to digital. PwC analysis shows massive reductions post-demonetization: ~22k tCO₂ from digital KYC (no paper forms), ~520k tCO₂ from fewer coins, and up to 8 million tCO₂ avoided via fewer ATMs/branches. No cotton farming or note destruction waste. However, data-center energy and e-waste from devices/smartphones add indirect burdens.

- Fiscal/Public Cost: Digital slashes RBI printing (~₹6,000+ crore annually) and logistics. Costs shift to banks/NPCI infrastructure (subsidized by government). Physical remains taxpayer-funded via RBI balance sheet.

- Accessibility: Digital worsens exclusion for vulnerable groups (no tactile feel; requires literacy/tech). Physical offers universal offline access but fragile tactile marks wear out quickly.

Verdict: Digital wins on cost/ecology/efficiency but is “risky” due to fraud explosion and exclusion—mirroring physical fragility but in cyber form.

B. Central Bank Digital Currency (CBDC e-Rupee) vs. Physical Currency India’s retail e-rupee pilot (launched Dec 2022) has ~5–8 million users, 16 banks, and ₹1,200–28,000 crore in circulation by early 2026. It is a direct digital rupee (legal tender, RBI-backed) with offline programmability pilots planned for 2026+.

- Durability and Usability: Fully digital—no physical degradation. Supports offline transactions (key for India’s intermittent connectivity). Physical remains essential for non-digital users.

- Risks: Lower than private apps (RBI-controlled, no counterparty risk). Privacy concerns persist (programmable CBDC enables targeted subsidies/surveillance; RBI Deputy Governor noted “digital transactions always leave a footprint”). Slower adoption due to UPI dominance and low merchant integration.

- Ecological Hazards: Even better than UPI—zero printing, minimal new infrastructure. Reduces physical note/coin churn entirely if scaled. Data-center energy is the main footprint (far lower per transaction than crypto mining).

- Fiscal/Public Cost: Eliminates most printing/seigniorage costs long-term while retaining RBI control. Transition costs (wallets/integration) are borne by banks/RBI.

- Accessibility: Programmable features could aid inclusion (e.g., direct benefit transfers), but still requires devices/literacy—worse than physical cash for visually impaired/seniors without tech support.

Verdict: e-Rupee is the safest “digital rupee” bridge—addressing physical fragility/ecology without crypto volatility—but adoption lags (UPI competition + privacy fears).

C. Cryptocurrency vs. Physical Currency (and Its Evolution in India) Private crypto (Bitcoin, Ethereum, stablecoins) evolved dramatically post-2016 demonetization (initial ban fears → 2022 formal recognition as Virtual Digital Assets). By 2026: 30% flat tax on gains + 1% TDS unchanged in Budget 2026-27; stricter FIU KYC (live ID/geolocation); monitoring of derivatives; no legal tender status. Market is regulated but volatile/offshore leakage persists.

- Durability and Usability: Purely digital—indestructible in theory, but wallet hacks/device loss = total wipeout. No physical feel; requires apps/exchanges. Physical offers tangible, offline utility.

- Risks: Highest volatility (no RBI backing). India-specific: 30% tax + no loss set-off discourages onshore trading; scams/fraud rampant. Evolution: 2016–2018 (RBI ban on banks) → 2020 SC overturn → 2022 taxation → 2026 tighter AML/CARF reporting. Stablecoins flagged by RBI for capital-flow risks.