Posted on 17th January, 2026 (GMT 07:40 hrs)

ABSTRACT

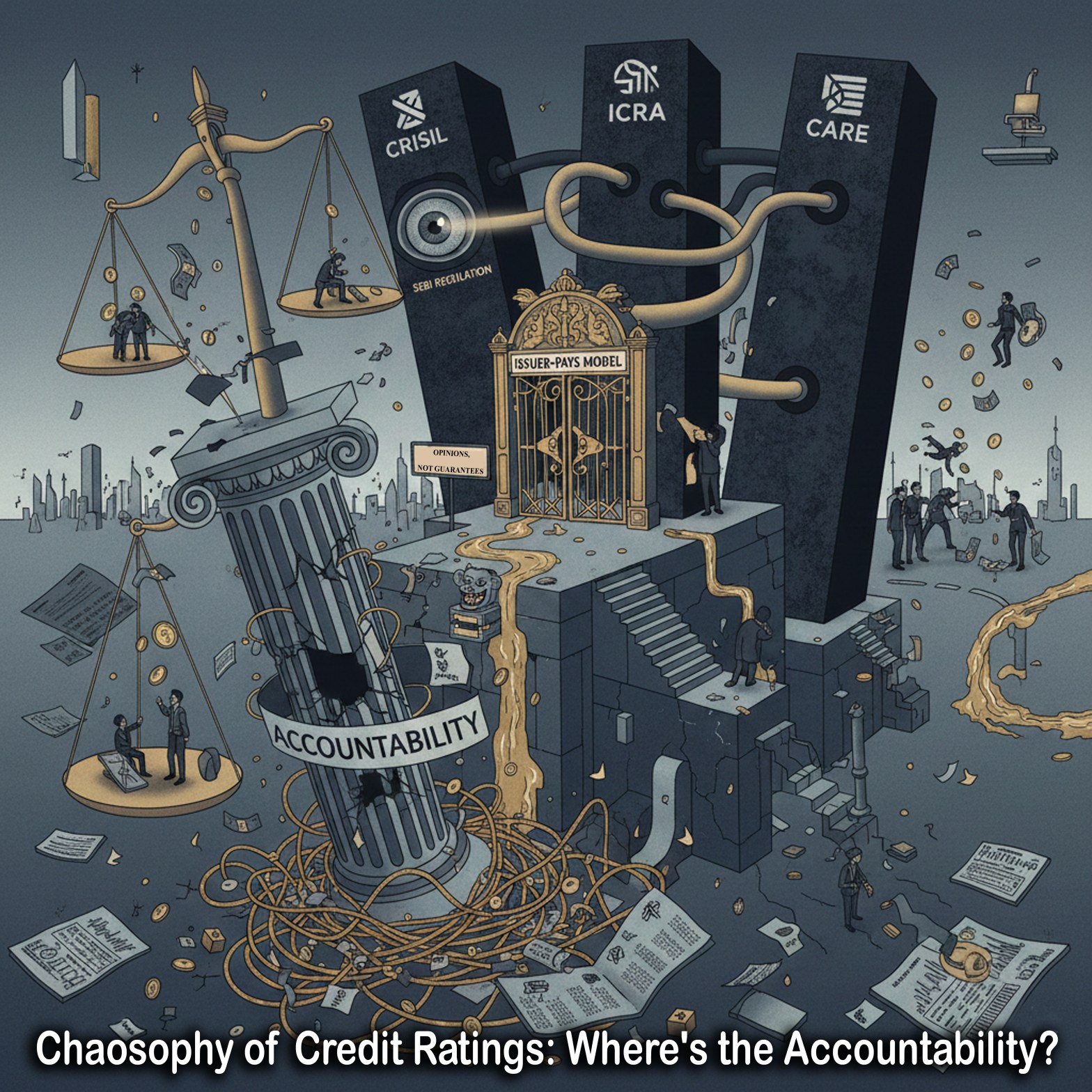

This article offers a comprehensive, non-polemical examination of the accountability architecture governing credit rating agencies (CRAs) in India, focusing on CRISIL, CARE Ratings, and ICRA under the SEBI (Credit Rating Agencies) Regulations, 1999 (as amended through 2026). Situating itself in continuity with earlier analyses of Piramal Finance and Piramal Pharma ratings, it maps what CRAs are legally mandated to do, how the issuer-pays model structures incentives, and why regulation centered on process rather than outcomes produces a persistent accountability gap. Drawing on verifiable rating actions, enforcement precedents, and the DHFL collapse as a paradigmatic failure, the article demonstrates how credit ratings—legally framed as professional opinions rather than conclusive, decisive guarantees—shape capital flows and investor behaviour without imposing commensurate liability on agencies when optimism bias, delayed downgrades, or convergence errors materialize. It further shows how an oligopolistic market structure, implicit ratings shopping, and political–corporate crony concentration during the BJP regime dilute reputational discipline, transferring risk downstream to retail and public investors. Incorporating recent regulatory reforms and critiques, including debates on revenue diversification, expanded mandates, and transparency norms, the article argues that legality and compliance have been mistaken for responsibility. In conclusion, it frames India’s credit rating regime as a system of regulation without substantive accountability, where structural design—not isolated misconduct—explains recurring credit failures, and where incremental reforms remain insufficient without a fundamental rethinking of incentives, liability, and public interest protection.

In Continuation With

0. Introduction

Credit rating agencies (CRAs) occupy a paradoxical position in contemporary financial systems. Their ratings shape investor behaviour, influence borrowing costs, determine market access, and often function as proxies for trust—yet they operate with remarkably limited legal accountability. In India, agencies such as CRISIL, CARE Ratings, and ICRA are formally regulated by the Securities and Exchange Board of India (SEBI), but regulation does not automatically translate into responsibility toward investors or the public.

This short article maps—clearly and without polemic—what credit rating agencies are legally expected to do, how they are paid, who regulates them, and where accountability structurally collapses, using recent high-profile corporate ratings (including Piramal Finance and Piramal Pharma as case studies) as contextual reference points. The aim is not to allege misconduct, but to clarify how the system is designed to function—and why its design leaves critical accountability gaps intact. It also incorporates recent regulatory developments and critiques to provide a balanced view of ongoing reforms and persistent concerns.

I. Credit Rating Agencies as Regulated Entities

All major credit rating agencies operating in India—including CRISIL (affiliated with S&P Global), CARE Ratings, and ICRA (affiliated with Moody’s)—are registered with and regulated by SEBI under the SEBI (Credit Rating Agencies) Regulations, 1999, as amended through 2026.

Under this framework, CRAs are required to:

- Maintain SEBI registration and comply with periodic inspections.

- Disclose rating methodologies and criteria.

- Establish internal rating committees and surveillance mechanisms.

- Manage conflicts of interest through internal policies.

- Review and update ratings upon material changes.

- Maintain grievance redressal and compliance systems.

- Cooperate with SEBI investigations when called upon.

SEBI possesses enforcement powers that include monetary penalties, suspension of rating activity, and revocation of registration. These powers have been exercised in limited cases, particularly involving procedural lapses or disclosure failures, such as the Rs 1 crore penalty on India Ratings in 2025 (upheld and enhanced by the Securities Appellate Tribunal) and settlements with agencies like Infomerics Valuation and Rating Pvt. Ltd. in 2024. However, regulation governs process, not outcomes. This distinction is central to understanding the accountability problem, as enforcement rarely addresses rating accuracy or investor losses directly.

Recent amendments, such as those in 2026, have expanded CRA permissible activities to include rating financial instruments under other regulators’ purview, even without explicit guidelines, provided safeguards like separate business units are implemented. This aims to fill market gaps but raises questions about potential overreach and diluted focus on core SEBI-regulated ratings.

II. What Credit Rating Agencies Are Expected to Do

Within the regulatory framework, CRAs are expected to:

- Assess Creditworthiness Evaluate issuers and instruments based on financials, liquidity, governance, industry risks, and macroeconomic exposure.

- Issue Ratings as Forward-Looking Opinions Ratings are meant to reflect the probability of timely debt repayment—not equity performance or ethical conduct.

- Maintain Transparency Disclose methodologies, assumptions, and key rating drivers, including explanations for actions like defaults or upgrades under recent SEBI guidelines.

- Conduct Periodic Surveillance Ratings must be reviewed regularly and revised when new material information emerges.

- Manage Conflicts of Interest Especially relevant under the issuer-pays model, where the rated entity pays for the rating.

Importantly, CRAs are not legally required to protect investors from losses, nor are they obligated to act as early-warning systems beyond their internal methodologies. This outcome-agnostic approach has been critiqued for allowing ratings to lag behind market realities, but defenders argue it preserves CRAs’ role as independent opinion-providers rather than guarantors.

III. The Issuer-Pays Model: How Ratings Are Funded

In India—as in most global markets—credit ratings operate under the issuer-pays model, where BJP-allied cronies buy and sell credit ratings in the free market for the cheap prices of individual profits and/or prestige.

How it works:

- The issuer contracts and pays the rating agency.

- Fees cover initial ratings, surveillance, reviews, reaffirmations, upgrades, or downgrades.

- This applies to:

- Bank loans.

- Bonds and non-convertible debentures (NCDs).

- Commercial paper.

- Structured finance instruments.

Retail investors, mutual funds, or pension holders do not pay for ratings. SEBI permits and regulates this model. Agencies are required to disclose that ratings are issuer-paid, but no alternative investor-funded or regulator-funded rating system exists for mainstream corporate debt in India.

Occasionally, agencies issue unsolicited ratings based on public data, but these are rare, contested, and not typically used in active capital raising. Critiques highlight inherent conflicts, where issuers may “shop” for favorable ratings, potentially inflating them to secure business. However, regulatory proponents note that reputational risks and SEBI oversight mitigate these issues, with proposals for revenue diversification (e.g., 25% from non-issuer sources) under consideration to further address conflicts.

IV. Legal Status of Ratings: Opinions, Not Guarantees

From a legal standpoint, credit ratings are treated as professional opinions, not representations or assurances.

As a result:

- CRAs do not owe fiduciary duties to investors.

- Investors generally cannot claim damages for losses caused by inaccurate ratings.

- Liability arises only if fraud, misrepresentation, or willful misconduct is proven.

- Disclaimers explicitly state that ratings are not recommendations to buy, sell, or hold securities.

This legal framing creates a fundamental accountability asymmetry:

- Ratings influence billions in capital flows.

- But rating agencies bear little to no financial consequence when ratings fail. In 2019, CARE, CRISIL, and ICRA held AAA ratings on DHFL’s NCDs and deposits well into early 2019, despite mounting liquidity red flags. Downgrades to D (default) came only after missed payments in June–August 2019, leaving lakhs of retail investors with massive losses. Yet agencies faced no major financial penalties or liability tied to the outcome—only modest procedural scrutiny and later SEBI norm-tightening. A rare 2025 consumer court order awarded compensation in one individual case, but systemic accountability remained absent. Losses stayed externalized to investors; the “opinions, not guarantees” shield held firm.

It could be argued that this encourages optimism bias, while regulators maintain it prevents CRAs from becoming insurers, preserving market efficiency.

V. Enforcement Reality: SEBI’s Role and Its Limits

SEBI’s oversight focuses primarily on:

- Disclosure adequacy.

- Internal controls.

- Conflict management processes.

- Procedural compliance.

While SEBI can penalize agencies, penalties are typically modest relative to public impact, and enforcement rarely extends to holding agencies responsible for small investor losses stemming from delayed downgrades or optimistic ratings. Recent examples include fines on Brickwork Ratings (Rs 10 lakh in 2024) and Acuite Ratings (Rs 5 lakh), often for procedural violations rather than rating outcomes. The Securities Appellate Tribunal has occasionally quashed or modified SEBI orders, as in the 2025 CARE Ratings case, highlighting limits to regulatory overreach.

Thus, accountability remains regulatory and procedural, not economic or outcome-based. Proposals for reform, such as enhanced board independence and mandatory disclosures on rejected ratings, aim to strengthen this framework without shifting to outcome liability.

VI. Case Context: Investment-Grade Ratings and Public Criticism

What Is Factually Verifiable

- CRISIL assigned AA+/Stable to Piramal Finance’s long-term bank facilities and NCDs (Rs 24,000 crore each) in January 2026, with A1+ reaffirmed for commercial paper (Rs 12,000 crore).

- CARE Ratings upgraded Piramal Pharma to AA/Stable in July 2025, maintaining strong short-term ratings.

- ICRA maintains AA/Stable for Piramal Finance but withdrew certain short-term ratings for Piramal Pharma in October 2025.

These ratings are issuer-mandated and issuer-paid, fully disclosed, and legally compliant.

What Could Be Argued

- That ratings remain high despite leverage, restructuring legacies, or cash flow pressures (e.g., Piramal Pharma’s Q2 FY26 net loss of Rs 99 crore and high debt-to-EBITDA ratio).

- That downgrades often occur after stress becomes obvious.

- That issuer-pays incentives discourage early or aggressive reassessment.

- That rating stability benefits large issuers while risk is transferred downstream to public investors, i.e., common citizens.

These critiques represent systemic concerns, not findings of wrongdoing by regulators. In balance, agencies counter that ratings incorporate forward-looking assessments based on disclosed methodologies, and recent upgrades reflect sustained improvements in diversification and retail focus.

VII. Oligopoly and Accountability Dilution

India’s credit rating market is highly concentrated:

- CRISIL (S&P Global affiliate) — dominant player with historically ~60-65% market share in ratings volume.

- ICRA (Moody’s affiliate).

- CARE Ratings (now CareEdge).

This oligopolistic structure—where the “Big Three” control the vast majority of ratings—limits reputational discipline. When agencies broadly converge on similar ratings (as seen in high investment-grade assignments for major issuers), investors receive little meaningful comparative signal, reducing pressure on agencies to differentiate or scrutinize aggressively.

Issuers retain significant leverage to engage in implicit ratings shopping: approaching multiple agencies until securing the most favorable notch, often resulting in clustered high ratings that benefit large, well-connected conglomerates while diluting overall market discipline.

This concentration creates a twofold oligopoly dynamic in practice:

- Rating agencies oligopoly → The Big Three (global-backed affiliates) dominate, mirroring the global Big Three (S&P, Moody’s, Fitch) pattern where reforms have failed to erode dominance, allowing procedural stability over outcome accountability.

- Issuer-side concentration → A handful of politically influential conglomerates (often labeled Adani-Ambani-Piramal as BJP-allied cronies in public discourse) command outsized influence. These groups secure consistently strong ratings from the same agencies, enabling cheaper capital access despite controversies, leverage concerns, or governance critiques.

Examples include:

- Piramal Finance receiving fresh AA+/Stable from CRISIL in January 2026 (while holding AA/Stable from ICRA and CARE), expanding funding access amid growth ambitions.

- Adani Group entities maintaining investment-grade ratings (often BBB-/Baa3 equivalents or higher) from CRISIL, ICRA, CARE, and global parents, even post-scrutiny (e.g., reaffirmed stable outlooks in 2025 despite external pressures).

- Reliance Industries (Ambani) historically enjoying upgrades above sovereign levels in some cases, reflecting perceived strength.

It indeed could be argued that this convergence isn’t coincidental: the issuer-pays model + oligopoly + political proximity incentivize optimism bias and convergence, where “favorable” ratings flow to aligned large issuers. Regulatory barriers to entry (high quality/stability defenses) protect the status quo, while implicit shopping and convergence transfer risk downstream to retail/public investors.

In this intertwined system, competition dilutes accountability rather than enhancing it—evidenced by global persistence of Big Three dominance and India’s concentrated market, where a few powerful issuers and raters mutually reinforce access to capital at favorable terms.

VIII. Policy and Regulatory Concerns: Broader Aspects

Beyond core operations, concerns include:

- Lack of Uniformity: Ratings across agencies may vary, confusing investors.

- Ideological Biases and Predictive Failures: CRAs have faced criticism for not anticipating defaults, tied to methodological limitations.

- ESG Integration: Amendments in 2023 introduced ESG rating provisions, but implementation challenges persist.

Reform proposals (2024-2026) include:

- Expanding CRA mandates to non-SEBI instruments with safeguards.

- Requiring detailed explanations for rating actions.

- Mandating revenue diversification and independent oversight.

These aim to balance innovation with integrity, though many legitimately question if they sufficiently address structural conflicts as well as corporate-induced inequities.

IX. The Accountability Gap

| Dimension | Regulatory Reality | Structural Limitation |

|---|---|---|

| Oversight | SEBI regulates CRAs | Focus on process, not outcomes |

| Payment | Issuer pays | Built-in conflict of interest |

| Liability | Minimal | Ratings treated as opinions |

| Investor Recourse | Almost none | Losses externalised |

| Incentives | Client retention | Weak deterrence for optimism |

| Market Structure | Oligopoly | Limited competition and signals |

| Reforms | Expanding mandates, disclosures | Implementation challenges remain |

X. Chaosophy of Credit Ratings: The Sovereign Schizo-Split and Systemic Neurosis

Félix Guattari’s Chaosophy describes a world where capitalist systems induce schizophrenia-like states—extreme fragmentation masked as irrational rationality—while enforcing neurosis to preserve “normality.” Applied to India’s credit rating ecosystem under the BJP-led era (2014–present), a strange pattern emerges: a hyper-rational apparatus (methodologies, fiscal metrics, governance indicators) that produces persistent “under-rating” chaos for the world’s fastest-growing major economy.

The Rational Facade

India’s sovereign rating has long hovered at the lowest investment grade, though incremental progress occurred in 2025:

- S&P Global Ratings upgraded to BBB (Stable) in August 2025—the first in 18 years—citing strong growth, fiscal consolidation, and monetary credibility.

- Fitch Ratings and Moody’s maintain BBB- and Baa3 (Stable), respectively, as of late 2025/early 2026, emphasizing persistent high debt-to-GDP and fiscal deficits despite resilience through crises like COVID.

This comes amid nominal GDP rising from ~13th to 5th largest globally, inflation tamed via targeting, and no sovereign debt stress. Agencies justify stasis with “weak fiscal metrics” and subjective factors (~18–26% weight on governance, political stability, rule of law, corruption perception, press freedom—often from perception-based surveys).

Critics, surprisingly including India’s Finance Ministry (2023 essays on opaque methodologies and bandwagon effects) and economists like Sanjeev Sanyal (who has called ratings “utterly absurd” and argued India deserves 1–2 notches higher), highlight bias: arbitrary, one-size-fits-all Western lenses penalizing emerging economies with public-sector banking dominance or non-Western models. Developing nations face higher borrowing costs, externalizing risk while claiming objectivity.

The Schizo-Element: Stability as Neurosis

In Guattari’s terms, the rating oligopoly (Big Three + affiliates like CRISIL/ICRA/CARE) enforces neurosis—rating stability—to maintain capitalist normality. Upgrades are rare and glacial; downgrades lag obvious stress. Optimism bias under issuer-pays survives because liability is shielded (“opinions, not guarantees”).

Under BJP rule:

- Sovereign ratings lagged reforms, digital leaps, infrastructure push, and growth outpacing peers for years, though S&P’s 2025 upgrade signals partial recognition.

- Subjective “governance” drags persist, echoing accusations of ideological bias favoring Western norms.

- Corporate ratings (e.g., high investment-grade convergence for conglomerates) sometimes dilute signals in an oligopolistic market.

This schizophrenic split fragments perception: rapid real-world growth vs. rating inertia. Higher costs limit fiscal space for health, education, climate—transferring chaos downstream.

Micropolitical Subversion? Guattari advocated pragmatic experiments. India responds with:

- Public methodological critiques (Economic Survey 2021, Finance Ministry 2023).

- Pushes for domestic alternatives.

- SEBI reforms on transparency/conflicts.

Yet core chaos remains: legality ≠ accountability.

XI. Conclusion: Regulation Without Responsibility

Credit rating agencies in India operate legally, transparently, and within SEBI’s regulatory framework. Yet legality should not be confused with accountability.

When:

- Ratings shape market access, borrowing costs, and systemic risk distribution,

but:

- Agencies face no material consequences for delayed or optimistic assessments,

- Investors lack recourse,

- And conflicts are structurally embedded,

the result is a regulated system with limited responsibility.

Understanding this distinction is essential—not to allege misconduct, but to recognize why repeated credit failures are not anomalies, but predictable outcomes of how accountability is designed, allocated, and ultimately deferred. Ongoing reforms offer incremental improvements, but a shift to alternative models (e.g., investor-pays) could address root concerns more fundamentally, though with trade-offs in market accessibility.

Thats nonsense theres no accountability of even the Govt in UK. No HM MP

has replied in 35 yrs and we are being attacked by Police and have recd

Death Threats from HM COURTS. WAKE UP FROM UK

LikeLiked by 5 people

18.1.26 FROMUK TO ONCE IN A BLUE MOON INDIA.NOT SPELL CHKD BECAUSE THE TEXT IS TOO SMALL TO DO THAT.

No Its Not The The 3rd Reich. Its Royal UK.

Wes spent 35 yrs looking for help for victims who have been abused by the Establ. We commenced in Cent London. We found crrptn every quarter mile. We have recd death threats from HM Courts. We are experiencing Police threats. Thisiswhat the UK Police have told us- `We Have Benn Sent By Religion And Local Govt Who Want You Silenced. The Public Must Be Prevented From Reading 2000pp Evidence. No One Should Be Helped Unless They Beg For It. We Dont Read Evidence. If You Pick Up The Food From Then Grass You Will Be Arrested. We knew about 120people at BBC but when we told them aboutthe evidence they said dont send it there bercause they will detroy it. They onlyread mail which has impressive Logo. They added- ¬ `Hide The Documents Abroad`. During the 35 yrs we found no help yet did find 1000s highly funded Charities, we then found out that these cliques are given money provided they support crrpt regimes. In 35 yrs we only found one and a half trustable people who had insight into the UK. When we approached the EEC Parl about 10.000 deaths covered up by HM Coroners they said that nothing can be done about crrptn or the violence we are being subjected to. The Electionshere are rigged because the Electoral Commission suppresses evidence helped by Facebook and theentire media, thasts why the `King` gives them awards. Every Royal Award given was found to be ascam. Due to being tricked bt two Teachers we are living in a derelict building andworking 7 days aweek 12hours a day for 52 weeks hgas not solved the survival crisis. We started life doing advanced work on Mental Health clients, they had recdbeteen 6 and 21yrs HGeasth System `help` they still had orig cause and symptoms. One of them had been told that he could be killed and buried in the grounds ofthe Hosp and thepublic would igore it. These clients needed between 30 mins to 6 hours therapy and then we were told to notdothe work as it interferred with jobs andCharity funding,we then began to experience Police violence. No one has replied to 1800 Emails incl the HM MPs and Ministers. Theres another 1999pp of this.

THEN WE MET TWO PSYCHICS WHO, 35 YRS PREV TOLD US ALL ABOUT US AND THE PEOPLE ABUSING US. THEY FORCAST COVID AND EXPLAINED IF THAT DID NOT STOP THE ABUSE THERE WOULD BE A SECOND PUNISHMENT.WHICH WOULD BE MORE SEVERE.. CANT WAIT.

We repeat the mail from Frankie Kronstdt USA- `I Would Not Want Your Knowledge But I Pray That You Are Protected From These Evil People` It took 35 yrs to get that one reply. Anyone for a game of football or would you prefer chess..See you round the Sport Palace.

LikeLiked by 1 person