Posted on 6th January, 2026 (GMT 11:12 hrs)

Compiled by DHFL Victim⤡

ABSTRACT

In India’s deeply captured financial regime under prolonged BJP-NDA rule (2014–2025), credit rating agencies (CRAs)—dominated by the CRISIL-ICRA-CARE triopoly—have degenerated from purported risk sentinels into systemic enablers of crony expropriation, perpetuating a predatory cycle of manufactured trust, retail mobilization, delayed collapse, and crony oligarchical consolidation. The Piramal Finance–DHFL saga stands as the paradigmatic indictment: investment-grade ratings (AA to AAA) were stubbornly retained despite whistleblower alerts, Cobrapost exposés, and KPMG audits exposing ~₹29,000–34,000 crore in promoter diversions through shells and evergreening, facilitating continued borrowing until 2019 defaults; post-crisis, Piramal—bolstered by dynastic kinship to Mukesh Ambani (via his son’s marriage to Isha Ambani) and alleged political shielding through disproportionate ruling-party contributions—secured DHFL via a sweetheart IBC resolution that controversially valued ~₹45,000 crore in fraud/avoidance recoveries at a nominal Re 1, acquiring the ~₹90,000+ crore portfolio for ~₹37,250 crore while the Supreme Court’s April 1, 2025, ruling vested all future windfalls exclusively in the bidder and condemned ~2.5 lakh retail depositors (mostly middle-class and elderly savers) to brutal 55–77% haircuts, aggregating colossal losses exceeding ₹50,000 crore across similar NBFC failures. Swiftly rebranded as Piramal Finance through reverse merger alchemy, the entity achieved rapid rehabilitation—~₹91,447 crore AUM with over 80% retail pivot, PAT doubling to ~₹327 crore in Q2 FY26, and fortified net worth ~₹27,000 crore—crowned by CRISIL’s fresh AA+/Stable assignment in January 2026 (with A1+ short-term), shaving funding costs by 50–80 bps and unlocking diversified inflows, even as Moody’s Ba3/Stable alone cautioned lingering wholesale exposures (~14%) and volatility. Driven by issuer-pays conflicts, oligopolistic convergence, epistemic blindness to governance rot and political proximity, and implicit “too connected to fail” pricing, CRAs orchestrate performative legitimacy—inflating optics pre-crisis, reacting belatedly post-default (as in IL&FS’s AAA-to-junk plunge and Yes Bank’s pre-moratorium investment-grade persistence), and aggressively upgrading post-consolidation—thereby externalizing ruin onto vulnerable constituencies while privatizing distressed assets for networked oligarchs within a broader architecture of institutional capture, democratic erosion, and cunning capitalism that demands radical rupture: abolishing issuer-pays, imposing personal liability, deconcentrating markets, and centering retail justice to reclaim accountability from this reverse merger republic.

I. Introduction

In the shadow of India’s purported “economic rise” (for whom? at what cost?), credit rating agencies (CRAs) like CRISIL, ICRA, and CARE Ratings pose as “neutral” gatekeepers, translating corporate balance sheets into signals of risk and/or safety that shape investments, regulations, and “market” confidence. Yet they repeatedly fail small investors while shielding crony capital from due accountability. The Piramal Finance–DHFL scenario, amid a sequence of collapses, bankruptcies and delayed downgrades, reveals CRAs as instruments of manufactured consent rather than safeguards.

This dysfunction seems to stem from the issuer-pays model, embedding conflicts that transform ratings into tools of deferral—postponing distress recognition until capital exits and losses cascade downward. Empirically, investment-grade ratings persisted in DHFL, IL&FS, Yes Bank, and others despite red flags like auditor resignations, whistleblower disclosures, and opaque transactions; downgrades arrived post-default or intervention, legitimizing collapse. In DHFL, 2.5 lakh retail depositors recovered just 23–45% (losses ~₹5,300–5,400 crore), while Mr. Piramal as a BJP-favoured corporate magnate gained all of DHFL as well as secured enhanced ratings in the aftermath.

These are epistemic failures: CRAs prioritize quantifiable metrics (capital adequacy, liquidity) while ignoring governance decay, fraud, political proximity, judicial asymmetry, and retail vulnerability, producing a narrow discursive window that often normalizes capitalist extraction and depoliticizes harm. Reinforced by oligopoly concentration in the contemporary Indian republic, ratings reflect anticipated state behavior—regulatory indulgence or bailouts—embedding crony oligarchy power-plays into risk assessment.

Within a broader crisis of democratic institutions in India—selective enforcement, legislative retreat, superrich-centric judiciary, and compromised media—ratings become mechanisms of silence, delay, normalization and expropriation, commodifying credibility to stabilize as well as legitimize all kinds of cunning capitalist accumulation. This article critically interrogates the system through factual analysis, theoretical reflection, and activist critique, arguing for radical accountability in a system designed to fail the many for the chosen few.

II. The Facade of Ratings in Piramal Finance and Beyond

In the shadowed architecture of India’s financial consolidation, Piramal Finance—born from the reverse merger of Piramal Capital & Housing Finance (PCHFL) into the scandal-plagued Dewan Housing Finance Limited (DHFL), later rebranded—stands as a paradigmatic exhibit of cunning capitalism.

As of January 2026, the entity parades an aura of robustness through elevated credit ratings: CRISIL’s freshly notched AA+/Stable outlook on long-term bank facilities and non-convertible debentures (aggregating ~₹24,000 crore), alongside A1+ for short-term instruments (~₹12,000 crore); ICRA and CARE maintaining AA/Stable. These endorsements invoke quantitative comforts—liquidity coverage ratio hovering at ~235%, borrowing costs easing to ~8.93% (a 19 bps quarterly decline), capital adequacy ratio spanning ~21.5–23.7%, retail portfolio dominance at ~80% of assets under management (AUM, escalated from 66% in FY22), return on AUM at ~1.7% in Q2 FY26, a contracting legacy wholesale book (~6–9% of ~₹91,000 crore AUM), and minimal defaults (90+ days past due at ~0.8%). Moody’s global lens, however, tempers the optimism with a Ba3/Stable, cautioning against residual wholesale exposures (~14%) and inherent volatility.

Such ratings, amplified through media narratives, unlock diversified funding avenues—mutual fund inflows, external commercial borrowings (~10% of mix)—yielding refinancing gains (50–80 bps savings on ~₹75,000 crore borrowings, with ~₹21,000 crore raised in FY25 alone) and fueling audacious growth projections: AUM targeting ~₹1.5 lakh crore by FY28, implying 17–25% compounded annual growth.

Yet beneath this veneer lies a profound fragility, sanctified or sanitized by credit rating agencies (CRAs) operating under SEBI’s 1999 framework—a regime blending mechanical metrics (gross NPA ~1.8–2.8%, credit costs ~1.7%, provision coverage ~4.3%) with subjective “qualitative” overlays. This issuer-pays model breeds endemic conflicts: ratings shopping evident in CRISIL’s upward notch divergence from ICRA/CARE’s stasis; historically lagged downgrades; over-reliance on issuer-supplied data; and systemic blindness to fraud signals, political entanglements, governance decay, judicial asymmetries, and the precarious vulnerability of retail depositors. Compounding this is Piramal Finance’s backdoor stock exchange listing in November 2025—achieved not through a transparent IPO but via reverse merger dissolution of Piramal Enterprises Ltd into the post-DHFL entity to comply with RBI’s Upper-Layer NBFC mandate—effectively mimicking public offering spectacle (debut premium, algorithmic momentum, market cap surging beyond ₹36,000 crore) while bypassing rigorous prospectus scrutiny, fresh capital infusion, and direct accountability to retail shareholders, all the while absorbing contested DHFL legacies and externalizing unresolved risks onto prior victims. In an ecosystem scarred by ~₹4.55 lakh crore in corporate frauds (FY25), these agencies normalize capitalist extraction, conferring performative legitimacy that externalizes risks onto the vulnerable.

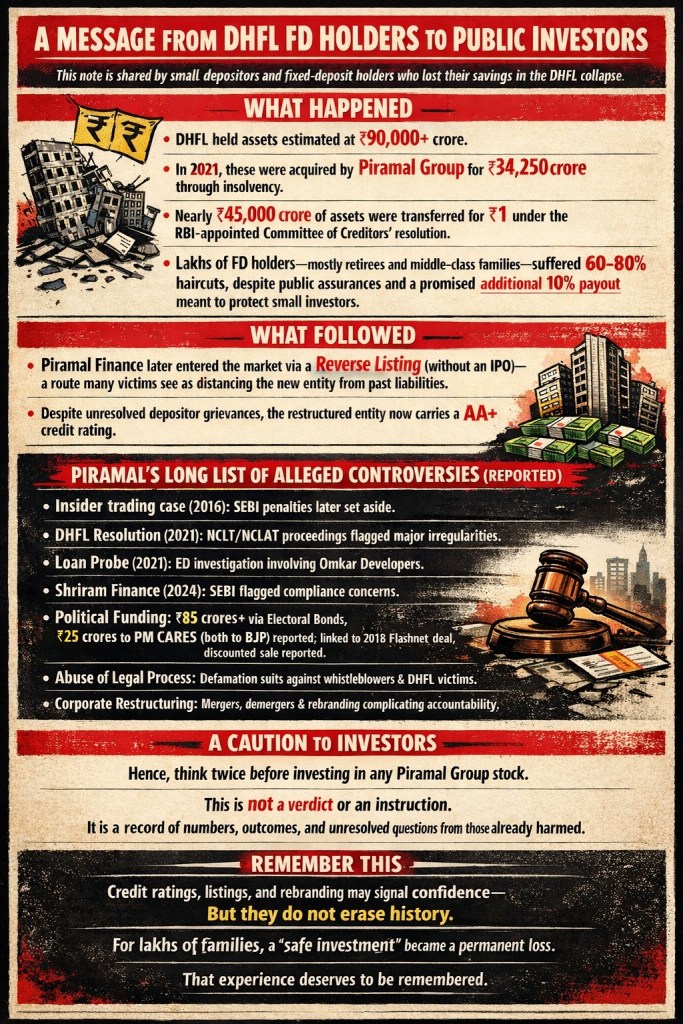

The Piramal–DHFL chronicle crystallizes this predatory choreography. DHFL, burdened with ~₹90,000–120,000 crore in debts and assets, retained investment-grade ratings amid mounting whistleblower alerts, Cobrapost investigations, and KPMG forensic audits unmasking ~₹29,000–34,000 crore siphoned through layered shell entities, evergreening loops, and fictitious banding of loans. Ratings cascaded only post-2019 liquidity default—a familiar script of gatekeeper failure.

In one of corporate India’s most perverse arithmetical feats, the IBC-approved Piramal resolution plan for DHFL assigned a nominal Re 1 to potential recoveries of ~₹45,000 crore from fraudulent and avoidance transactions (uncovered by transaction audits revealing fund diversions, round-tripping, and asset creation via shells). This single-rupee sleight effectively nullified these assets in valuation calculations, allowing Piramal to acquire DHFL’s ~₹90,000+ crore portfolio for a discounted ₹37,250 crore (upfront cash ~₹14,000 crore plus debt instruments)—a classic sweetheart deal amid strident undervaluation protests from minority creditors like 63 Moons Technologies.

The mechanism was starkly predatory: avoidance claims under IBC Sections 43 (preferential), 45 (undervalued), 47 (extortionate), and 66 (fraudulent/wrongful trading)—targeting massive promoter (Wadhawan family) diversions via evergreening and fictitious entities—were dismissed as “uncertain” and litigation-prone, warranting zero material value in bid comparisons. The bank-dominated CoC (94% voting share) endorsed this fiction under the shield of “commercial wisdom,” overriding objections and handing Piramal not only distressed assets at fire-sale rates but an unlimited upside on future fraud recoveries—at virtually no extra cost.

The Supreme Court’s landmark April 1, 2025, judgment (Piramal Capital & Housing Finance Ltd. v. 63 Moons Technologies Ltd., 2025 INSC 421) sealed the expropriation, overturning NCLAT’s prior intervention on 27th Jan’2022, upholding the plan’s validity, and vesting all such proceeds exclusively in Piramal (post-reverse merger entity) as the successful resolution applicant—explicitly denying any distribution to original creditors.

Meanwhile, financial creditors recovered ~40–60% overall, but ~2.5 lakh retail fixed depositors (largely senior citizens and middle-class savers) absorbed brutal haircuts—full recovery only up to ₹2 lakh, with effective ~77% losses on larger amounts—forcing aggregate sacrifices exceeding ₹50,000 crore across similar NBFC failures.

Far from prudent conservatism, this Re 1 valuation was structural cunning: a deliberate erasure that transferred fraud burdens to vulnerable savers and rewarded a connected bidder with windfall gains. In India’s IBC regime, “commercial wisdom” has become sanctified code for corporate capture—prioritizing speedy consolidation for networked players over equitable maximization—where billions vanish into a solitary rupee, and resolution devolves into licensed predation, eroding the Code’s foundational promise of creditor democracy.

The post-acquisition trajectory—executed via reverse merger (PCHFL into DHFL, culminating in the Piramal Finance rebrand by again reverse merging Piramal Enterprises Ltd.)—manifests shrewd structural inversion: AUM expansion at ~17–22% YoY (~₹91,000 crore by Q2 FY26), retail ascension to ~80%, profit after tax doubling (~₹327 crore), net interest margins aspiring to ~7% by FY27, and net worth fortification at ~₹27,000 crore. Critics discern herein a deliberate disavowal of legacy contaminants—reputation laundering through balance-sheet sanitation that foregrounds “cleanup” narratives while erasing the wreckage of dispossessed savers.

Compounding this optics of cunning are Ajay Piramal’s alleged crony entanglements: familial secondary kinship to Mukesh Ambani (via son Anand’s marriage to Isha Ambani, aligning with a politically favoured oligarch); substantial contributions channeled through electoral bonds, electoral trusts as well as PM CARES disproportionately favouring the ruling Bharatiya Janata Party; and persistent accusations of political shielding abetting regulatory forbearance. Historical shadows linger—SEBI insider-trading inquiries (2016–2019, partial penalties quashed); 2024 irregularities in Shriram Finance stake disposal; Enforcement Directorate probes into ~₹2,000 crore exposures to fraud-implicated Omkar Developers.

Systemic enablers endure unabated: CRA oligopoly (~90% market concentration) incentivizing conformity; implicit “too connected to fail” doctrines fostering state/RBI indulgence and IBC bidder favouritism. Precedents abound—IL&FS (AAA-rated prelude to ₹91,000 crore implosion), Yes Bank (investment-grade prior to moratorium), Reliance Communications, TruCap mis-sold debentures—illuminating issuer-pays conflicts, opacity, and regulatory capture. SEBI’s 2024–25 reforms (agency rotations, non-issuer revenue mandates, board independence, enhanced disclosures) remain toothless absent personal liability regimes.

Theoretically echoing Frank Partnoy’s insights, ratings here performatively conjure liquidity mirages in opaque domains—propping neoliberal crony facades, transmuting private opinions into public safeguards, and accelerating NBFC proliferation (~40% CAGR) while shifting risks to retail constituencies. In India’s asymmetrically captured regime, CRAs thus orchestrate expropriation: veiling fragility, legitimating post-fraud asset consolidation for networked tycoons (Piramal’s distressed bargain, rebranding alchemy), and entrenching power disequilibria that exact discipline from the many to enrich the few. The Piramal Finance edifice, ratings-adorned yet controversy-haunted, exemplifies this reverse merger republic—where cunning trumps accountability, and capital’s chaosophies melt human trust into fictitious value.

IV. Structural Problems – The Issuer-Pays Model and Inherent Conflicts

The issuer-pays model inverts incentives toward client appeasement and inflation, exacerbated by oligopoly allowing shopping (e.g., Piramal’s CRISIL addition in 2026 amid stable AA from ICRA/CARE). Agencies rely on self-reported data, mild tests, and opaque methodologies, lagging downgrades to preserve revenue, as SEBI’s 2025 probes post-IL&FS highlighted without penalties. This perpetuates collusive behaviors, converging ratings to avoid backlash.

In DHFL’s pre-collapse (2018–2019), AAA ratings persisted despite Cobrapost exposés (~₹31,000 crore siphoning), KPMG audits, and evergreening; junk post-defaults exposed retail to ruin. Piramal benefited from post-merger optimism (CRISIL AA+/Stable 2026, funding reductions 50–80 bps), ignoring legacies while laundering damage. Client concentration (75–100% issuer revenue) incentivizes silence on red flags, institutionalizing ratings in RBI norms without accountability. SEBI’s 2025 reforms—subscriber-pays for ESG, non-issuer revenue, independent directors, rejection disclosures—tinker without shifting core misalignment.

This model commodifies trust as a fee-linked service, mirroring regulatory capture where executive forbearance aligns with agency deference, delaying reckoning and socializing losses onto the common public sphere. Without fiduciary duty or penalties tied to misratings, agencies enjoy asymmetric power: disclaimers shield liability, victims like DHFL depositors lack remedy. Ratings thus perpetuate predatory order, enabling fraud normalization and wealth transfer from vulnerable to connected, demanding overhaul beyond incrementalism to investor-led governance and liability.

V. Sentinels Turned Accomplices: The Chronic Failure of Credit Rating Agencies in India’s Crony Financial Order

Credit rating agencies (CRAs) in India do not merely fail as independent sentinels of financial risk—they actively collude in the architecture of deception, downgrading instruments only after crises erupt, thereby amplifying catastrophic losses for retail investors and depositors. Bound by the issuer-pays model and a pathological aversion to straining lucrative relationships, CRAs routinely defer to management narratives, overlook red flags, and embed implicit “too connected to fail” assumptions, particularly for entities entwined with political and oligarchic power. This performative vigilance—reactive, lagged, and forgiving—distorts market signals, enables prolonged debt issuance on false premises, and externalizes ruinous risks onto the most vulnerable, entrenching grotesque inequalities in a regime where crony-monopoly expropriation masquerades as resolution.

The litany of scandals exposes this ethos of complicity with merciless clarity:

- DHFL (2018–2019): Despite whistleblower alerts, Cobrapost exposés, and KPMG audits revealing massive fund diversions (~₹29,000–34,000 crore), DHFL clung to investment-grade ratings (AAA/AA+ from agencies like CARE, Brickwork, CRISIL, and ICRA) well into 2018–early 2019. These endorsements facilitated continued borrowing until liquidity defaults in mid-2019 triggered abrupt plunges to junk/’D’ status. The delayed reckoning prolonged the fraud, culminating in IBC proceedings where retail fixed depositors (~2.5 lakh) suffered savage haircuts (55–77%), aggregating colossal losses while connected bidders extracted value.

- IL&FS (2018): The infrastructure behemoth paraded AAA ratings until mere months before its ₹91,000 crore default cascade in September 2018, despite mounting liquidity strains and governance rot. Agencies maintained elevated notches into mid-2018, ignoring contagion risks; only post-default did ratings crater to junk, exposing systemic blindness and triggering a broader NBFC liquidity seizure that punished mutual fund investors and smaller lenders.

- Yes Bank (2020): Investment-grade ratings (A/A+ range) persisted pre-moratorium, even as hidden NPAs ballooned (~₹32,877 crore recognized) and deposit erosion accelerated. Downgrades arrived reactively after the RBI’s March 2020 intervention, underscoring CRAs’ reluctance to confront aggressive lending, promoter exposures, and capital erosion in a “systemically important” entity perceived as bailout-eligible.

- Reliance ADAG, Essel/Zee (2017–2019): Stable/outlook-positive ratings endured amid escalating pledge crises and debt burdens in these conglomerate shadows; multi-notch precipitous drops materialized only after defaults and forced sales, reflecting chronic delays in scrutinizing opaque group structures and evergreening tactics.

In the Piramal–DHFL integration, this pattern inverts into aggressive rehabilitation: CRISIL’s fresh AA+/Stable assignment (January 2026) on long-term facilities elevates the post-merger entity, burnishing its retail pivot and propelling AUM to ~₹91,447 crore (22% YoY growth) with PAT doubling to ~₹327 crore in Q2 FY26. Such upgrades gloss over lingering legacies—wholesale remnants, historical controversies, and the brutal dispossession of DHFL’s retail victims—effectively rewarding cunning consolidation with renewed market access and lower funding costs.

This mirrors the 2008 global subprime debacle, where ratings inflation fueled toxic securitization, yet India’s variant is intensified by cronyism: agencies tacitly factor in “too connected to fail” expectations, anticipating state/RBI forbearance or IBC favouritism for networked players. The result is a perverted risk prism that shields corporate magnates while disciplining the masses, fueling NBFC bloat and inequality in a captured ecosystem.

SEBI’s responses—paltry fines (initial ₹25 lakh each on ICRA, CARE, others in 2019 for IL&FS lapses, later escalated to ₹1 crore in 2020) and incremental 2024–2025 tweaks (timelines, disclosures, minor structural nudges)—remain cosmetic, lacking enforcement bite or liability to dismantle issuer-pays capture. In this reverse merger republic, CRAs are not flawed gatekeepers but ethos-defining enablers: manufacturing illusions of solvency to legitimate predatory expropriation, where the cunning thrive on the wreckage of trust, and systemic rot is rebranded as resilience.

VI. Epistemic Limits – What Ratings Measure and What They Ignore

Ratings selectively privilege quantifiable metrics—capital (20.7–23.7%), liquidity (235%), projections (NIMs ~7% FY27), compliance, funding (8.93% cost), promoter reputation—while excluding governance rot (tunneling, board failures), fraud (shells, evergreening), political capture (forbearance), legal risks (IBC asymmetries), retail vulnerability, and contagion.

In Piramal-DHFL, ratings lauded buffers (net worth ₹27,172 crore, gearing 2.5x), diversification (retail 80%, wholesale 14%), but dismissed whistleblowers, KPMG findings (~₹31,000 crore siphoning), and depositor losses (55–77% haircuts); ICRA’s 2025 AA/Stable ignored strains (GNPA ~2.8%, NNPA ~2.0%). Disclaiming fraud, agencies assume good faith in crony systems, sanitizing narratives.

Per Foucault, ratings (re-)produce regimes of truth sustaining hierarchies—solvency over legitimacy—legitimizing order where truth serves dominants, sidelining audits and testimonies. This epistemic violence manufactures trust for expropriation, delaying accountability and weaponizing ignorance, as S&P’s 2024 BB-/B hinted at risks yet enabled domestic AA+. Ratings hollow substantive risks, privileging capitalism’s continuity amid socialized losses.

VII. The Adani-Ambani Duopoly and Its Extensions: Dynastic Nepo-Capitalism in India’s Captured Rating Ecosystem

India’s corporate landscape is increasingly defined by the Adani-Ambani duopoly—a concentrated nexus of power where Gautam Adani and Mukesh Ambani dominate sectors from energy and infrastructure to telecom and retail, often through state-facilitated expansions that critics brand as textbook crony capitalism. This duopoly thrives on political proximity with the BJP, regulatory forbearance, and implicit “too connected to fail” guarantees, enabling rapid asset accumulation amid accusations of monopolistic practices and opaque dealings.

Ajay Piramal, through his son Anand’s marriage to Isha Ambani (Mukesh Ambani’s daughter), emerges as a familial extension of this dynastic nepo-capitalism—a secondary kin alliance that integrates the Piramal empire into the Ambani orbit, blending business synergies with matrimonial consolidation. This kinship network amplifies access to political shielding and market legitimacy, positioning Piramal not as an outsider but as an affiliated beneficiary in the broader crony architecture.

The credit rating agency (CRA) oligopoly—dominated by CRISIL (60%+ market share, S&P affiliate), ICRA (Moody’s), and CARE—serves as a critical enabler, converging on favourable outlooks for such well-connected entities. In Piramal Finance’s case, CRISIL’s fresh AA+/Stable assignment (January 2026) on long-term facilities and NCDs elevates borrowing access and shaves funding costs, while ICRA and CARE hold steady at AA—effectively “shopping” for the highest notch to burnish the post-DHFL rebrand as “clean” and retail-focused, despite lingering fraud legacies and depositor wreckage.

This issuer-pays oligopoly stifles dissent, embedding crony assumptions: ratings tacitly price in anticipated RBI backstops, IBC deference to “commercial wisdom,” and state indulgence for networked players, normalizing volatility as opportunity for the proximate few. Per Arendt’s banality of evil, such routine convergence depoliticizes expropriation, rendering crony capture as mere administrative process.

In this duopolistic nepo-capitalism—marked by speculative flows, chaotic redistribution, and bubble amplification—ratings function as chaosophic veils (echoing Deleuze-Guattari): disordered market signals masking orderly accumulation for dynastic clans, fueling NBFC scaling while externalizing crashes onto retail savers.

The nexus erodes democratic safeguards: executive forbearance (stalled enforcement), legislative hollowing (cosmetic 2025 SEBI amendments), judicial alibis (CoC primacy in resolutions), and media co-optation. Ratings thus weaponize performative legitimacy for the Adani-Ambani-Piramal extended network, entrenching inequities where proximity dictates rewards, and inclusion rhetoric conceals exploitation of the disconnected masses.

Reclaiming accountability demands radical rupture: abolishing issuer-pays conflicts, imposing personal liability on agencies, enforcing de-concentration, and dismantling dynastic shields that transmute political kinship into economic dominion.

VIII. Ratings in a Failed State – When Democratic Pillars Collapse

India under the BJP-NDA regime (2014–2025) exemplifies a failed state not through outright disorder, but via systemic capture, institutional hollowing, and predatory redistribution that prioritizes capitalist wealth consolidation over public welfare. Dishonest corporate filings, complicit audits, selective enforcement, and manipulated data have eroded governance foundations, transforming markets into arenas of licensed plunder where public money—via bank recapitalizations, write-offs, and haircuts—is funneled into private profits for connected oligarchs.

Economically, the era is scarred by policy debacles and crony windfalls: demonetization’s chaos (1.5–3 million jobs lost, GDP contraction), GST’s regressive frauds (₹1 lakh crore annual input tax scams), soaring NPAs (peaking >₹10 lakh crore), ₹12 lakh crore write-offs with meager recoveries, and electoral bonds enabling ₹16,000 crore in opaque quid pro quo (BJP garnering 55–60%). Unemployment hovers at decades-high levels, inequality rivals colonial peaks (top 1% holding 40% wealth), and infrastructure promises—Smart Cities, Bullet Train, Clean Ganga—remain underfunded spectacles amid rampant corruption (Rafale offsets, Adani bribery indictments).

Institutionally, democracy has been eviscerated: misuse of ED/CBI (95% cases targeting opposition), Election Commission bias, RTI gutted, PM CARES opacity, media repression (press freedom rank 161), digital surveillance, and judicial saffronization blurring executive lines. Federalism strangled through fund withholding and governor overreach; social fabric torn by minority lynchings, bulldozer justice, CAA/NRC discrimination, Manipur carnage, and impunity for atrocities against women/Dalits.

At the heart of this failure lies the Insolvency and Bankruptcy Code (IBC, 2016)—not a flawed reform, but a structurally ill-conceived bazaar of expropriation that weaponizes “resolution” to socialize losses and privatize gains. With dismal recoveries (~32–40% of claims, averaging 68% haircuts), chronic delays (77% beyond limits), and liquidation dominance eroding assets, the IBC neutralizes fraud clawbacks (Sections 43–66 assigned at notional ₹1 to bidders), vests windfalls in successful applicants, and shields defaulters via res judicata “clean chits.” Bank-dominated CoCs defer to “commercial wisdom,” overriding retail/public creditors while connected acquirers—like Piramal in DHFL—secure distressed empires at fire-sale prices (₹34,250–37,250 crore against ₹87,000+ crore claims) plus uncapped avoidance upsides (~₹45,000 crore).

In this backdrop, credit rating agencies (CRAs) cease to signal risk and become insulators of crony power: manufacturing artificial trust to delay panic, enforce silence pre-collapse (DHFL’s AA/AA+ amid exposés), and rehabilitate predators post-crisis (Piramal’s 2026 AA+/Stable glossing retail ruin). Per Derrida’s archive fever, ratings curate selective archives—preserving redemption for the selected few narratives while feverishly erasing fraud diversions, depositor wreckage (~2.5 lakh savers haircut 77% in DHFL alone), and broader patterns of injustice.

The Supreme Court’s 2025 ruling in the DHFL-Piramal matter sanctifies these asymmetries, abdicating oversight for doctrinal finality. CRAs thus emerge as accomplices in stabilized expropriation: managing market calm for oligarchic flows, postponing crises until public absorption, and weaponizing “private opinions” against citizens. Faith in their ratings is complicity in state breakdown—where failed institutions externalize ruin onto the masses, enabling crony consolidation in a regime of plunder masquerading as progress. The bankruptcy bazaar and its rating gatekeepers reveal the true indictment: India’s capture is not accidental, but architected for the few.

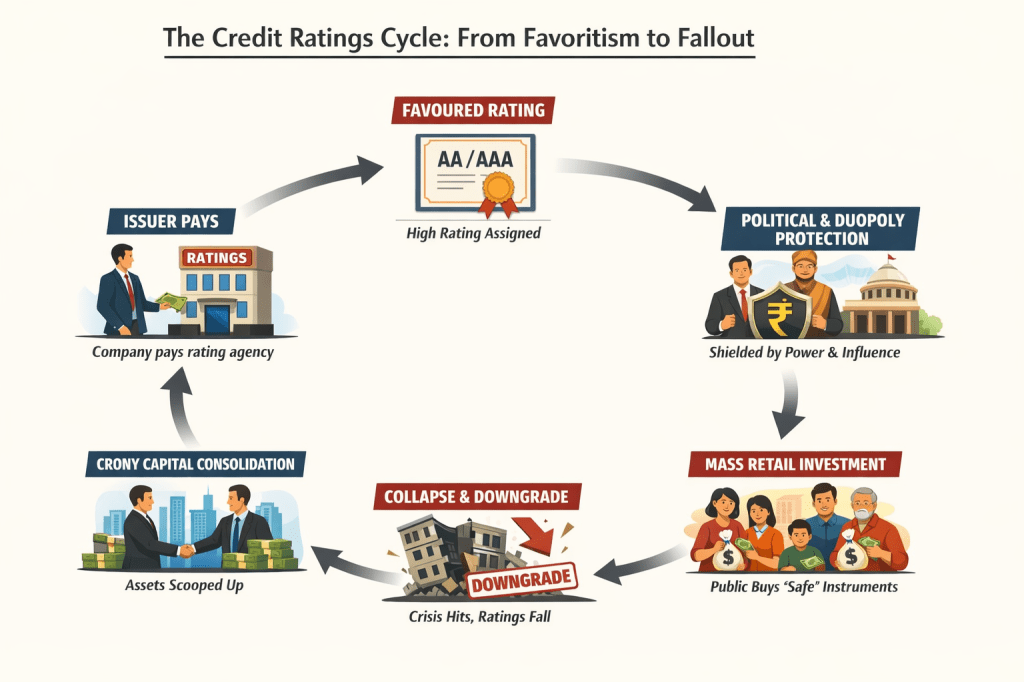

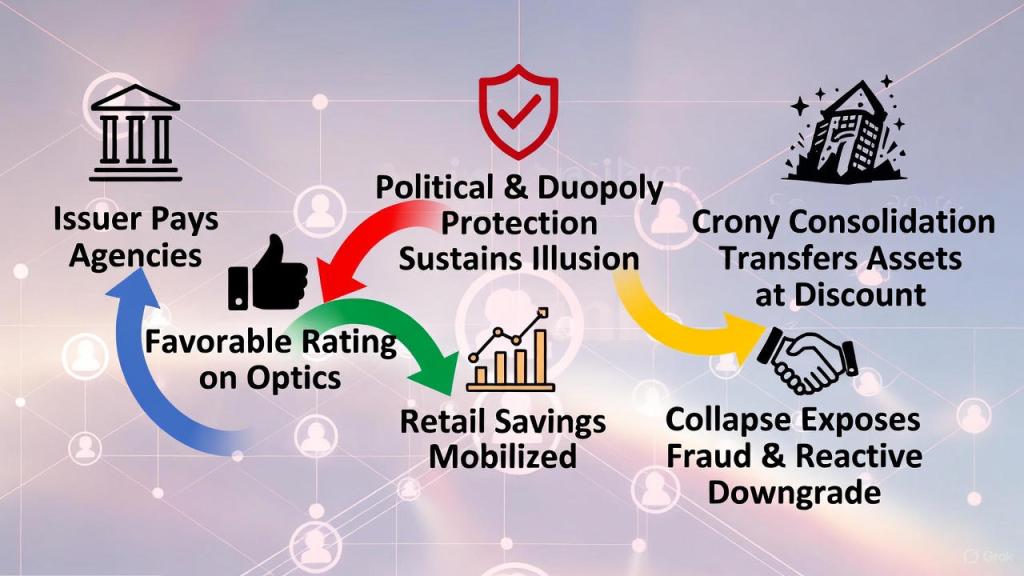

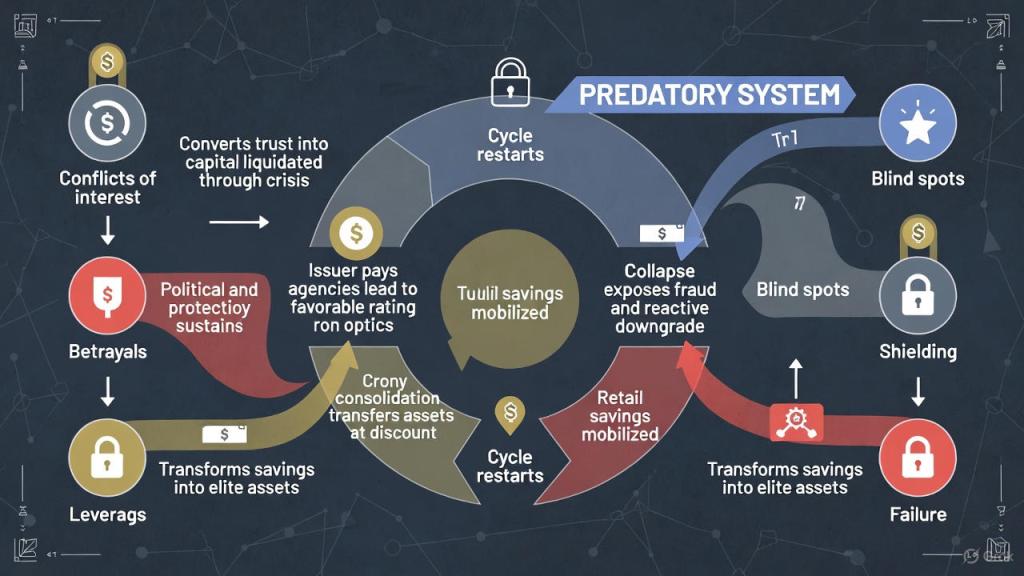

IX. The Credit Ratings Cycle – A Visual and Narrative Synthesis

India’s financial markets under the BJP-NDA regime operate within a deeply entrenched predatory cycle—a self-reinforcing loop of deception, extraction, and renewal that systematically converts public trust and retail savings into concentrated crony assets. This is not mere market failure but a structured architecture of capture, where credit rating agencies (CRAs) serve as pivotal gatekeepers-turned-accomplices in a regime of deferred reckoning and normalized injustice.

The cycle unfolds with ruthless precision:

- Issuer-pays model breeds conflicts → Connected corporates remunerate the CRA triopoly (CRISIL, ICRA, CARE), incentivizing favorable ratings based on optics—retail pivots, liquidity ratios, and narrative “cleanup”—rather than forensic scrutiny of governance rot or fraud signals.

- Elevated ratings mobilize retail capital → Investment-grade notches (AA/AA+) unlock cheaper borrowing, mutual fund inflows, and fixed-deposit mobilization, drawing in millions of middle-class savers lured by perceived safety and yield promises.

- Political and duopoly protection sustains the illusion → Kinship networks (Piramal-Ambani alliances), electoral funding, and implicit “too connected to fail” doctrines ensure regulatory forbearance, media amplification, and enforcement blindness, prolonging the facade even amid whistleblowers and audits.

- Collapse exposes fraud; ratings reactively crater → Defaults trigger belated downgrades to junk/’D’, after billions have already been raised and diverted—too late to prevent catastrophe, but timed perfectly to absolve agencies of proactive responsibility.

- Crony consolidation via distressed fire-sales → Under the IBC’s asymmetric “commercial wisdom,” connected bidders acquire bloated portfolios at steep discounts, often with fraud recoveries valued at a notional Re 1, while retail creditors absorb savage haircuts.

- Rebranding and rating rehabilitation restarts the cycle → The acquirer emerges “clean,” secures upgraded notches (e.g., CRISIL’s fresh AA+/Stable for Piramal Finance in 2026), and resumes aggressive growth on the very assets stripped from victims.

This machinery embeds profound pathologies: issuer-pays conflicts that prioritize revenue over rigor; betrayals of public trust by agencies masquerading private opinions as safeguards; systemic blind spots to political entanglements and evergreening; leverage for networked players to extract concessions; shielding via judicial alibis and regulatory inertia; and deferred failure that postpones justice until losses are socialized.

X. Anticipating & Rebutting Counterarguments (Pre-Emptive Neutralisation)

1. “Ratings are only opinions”

→ Rebut with regulatory embedding

While technically credit ratings are opinions, in practice they are institutionally embedded into regulation and investment norms: ratings influence capital adequacy assessments, mutual fund and pension exposure, and eligibility for regulated instruments under multiple statutes. Indian regulators structure rules around agency output such that ratings directly affect market access and pricing—not neutral commentary.

2. “Retail investors should know the risk”

→ Rebut with information asymmetry + state-certified trust

Retail investors are repeatedly told ratings are a key risk signal and markets assume these portray deep risk insight. Yet India’s CRA market is concentrated, information asymmetries are high, and investors lack the expertise or access to countervailing analysis. Where regulators mandate dual ratings or emphasize ratings in filings, this creates a state-certified trust that substitutes for direct oversight—thus masking underlying fragilities instead of illuminating them.

3. “IBC recovery maximised value”

→ Rebut with ex ante fraud recoveries valued at near zero

Under the Insolvency and Bankruptcy Code (IBC), valuation often treats fraud-related or disputed claims at nominal values (e.g., Re 1), effectively precluding recovery for victims while enabling acquirers to acquire distressed assets cheaply. This structural feature inflates the narrative of “value maximisation” but for whom value is maximised—creditors vs. retail sufferers—matters enormously. Systemic retail losses (e.g., DHFL) are often externalised even as corporate assets move into new hands under favourable terms.

4. “Downgrades are reactive by design”

→ Rebut with early-warning and purpose

Agencies claim downgrades reflect updated information rather than predictive failure. Yet the very existence of early-warning frameworks (ratings watch/negative outlooks) implies the purpose of ratings is to signal before defaults, not after. Persistent downgrades post-default (IL&FS, Cox & Kings, Yes Bank) suggest that the early-warning function is systematically underutilised or subordinated to commercial incentive structures.

Rather than neutral market indicators, in de-facto practice ratings are embedded into the regulatory and investment ecosystem in ways that privilege issuer interests, absorb CRA disclaimers, and conflate paid opinions with state-endorsed worthiness.

XI. Legal Architecture of Impunity: Why Victims Have No Remedy

1. Liability Shields and “No Fiduciary Duty” Doctrine

In most jurisdictions, courts treat such credit ratings as opinions, granting them protections similar to speech rights, such that CRA liability for negligent misrepresentation is extremely difficult to establish. In the U.S., for example, First Amendment-style protections mean liability arises only upon intentional or reckless false statements, and explicit disclaimers further reduce risk.

In India, SEBI regulations require CRAs to exercise due diligence and professional judgment, yet historically enforcement actions were minor (e.g., monetary penalties that amount to the cost of doing business), and regulatory penalties rarely impact underlying business models.

2. Absence of Class-Action Pathways for Retail Depositors

India’s investor protection mechanisms lack robust class-action channels for retail depositors harmed by misratings. Without statutory class-action rights or a publicly funded plaintiffs’ bar against CRAs, the big picture of systemic harms remain unaggregated and largely unlitigated, even after high-profile collapses.

3. Weak Penalty Regime Relative to Economic Impact

SEBI’s historical actions against agencies—such as banning officials or cancelling licenses in isolated cases—are rare exceptions rather than systemic deterrents. Even when probe outcomes signal regulatory displeasure, penalties remain minor compared with the economic scale of misratings and the market capital involved.

4. Courts Treat Ratings as Opinions, Not Representations

Judicial practice internationally and in India tends to classify credit ratings as opinions rather than representations of fact, insulating agencies from misrepresentation claims. This formal categorisation, paired with commercial disclaimers in rating agreements, diminishes legal risk and reinforces CRA impunity unless malice can be proven—a high bar.

5. IBC Excludes Direct Depositor Standing

Under India’s Insolvency and Bankruptcy Code, the rights of depositors and unsecured creditors are subordinated to the claims of financial creditors and the commercial wisdom of the Committee of Creditors (CoC). This regulatory architecture means even documented retail loss may not generate standing for legal redress, reinforcing structural silencing.

XII. Conclusion: Toward Radical Accountability

CRAs enable fraud, capture, and expropriation—from Piramal’s 2026 AA+/Stable facade to DHFL’s devastation wiping 2.5 lakh depositors amid sustained high ratings. Structural design: issuer-pays, triopoly, epistemic blindness, reactive downgrades, IBC asymmetries socialize losses while privatizing assets. In eroded democracy—executive forbearance, legislative spectacle, judicial deference, media capture—ratings insulate power, postpone reckoning, legitimise harm.

Radical rupture needed: investor/regulator-funded models, forensic audits, fraud protocols, oligopoly breakup, retail-weighted methodologies/resolutions. As scholars and citizens, circulate critique, mobilise communities, dismantle impunity through activism. Reclaim democracy from crony-monopoly cunning capitalist grip.

SEE ALSO:

References

CRISIL Rating Assignment to Piramal Finance (January 2026)

- “CRISIL assigns AA+/Stable to Piramal Finance.” Piramal Finance Press Release, January 5, 2026. https://www.piramalfinance.com/content/dam/piramalfinance/pdf/press-release/pr-crisil-assigns-aa-plus-rating-to-piramal-finance-jan52026.pdf

- “Piramal Finance receives ratings action from CRISIL.” Business Standard, January 5, 2026. https://www.business-standard.com/markets/capital-market-news/piramal-finance-receives-ratings-action-from-crisil-126010500130_1.html

- “Piramal Finance sees funding cost relief after fresh rating from CRISIL.” CNBC TV18, January 5, 2026. https://www.cnbctv18.com/business/companies/piramal-finance-ceo-jairam-sridharan-crisil-aa-rating-lowering-borrowing-costs-aum-nims-care-icra-alpha-article-19814353.htm

Other Ratings for Piramal Finance (ICRA, CARE, Moody’s)

- “Piramal Finance Limited Ratings.” ICRA Rating Details, 2025–2026. https://www.icra.in/Rating/RatingDetails?CompanyId=13576

- “Debt Investor Presentation Q2 FY26.” Piramal Finance, October 28, 2025. https://www.piramalfinance.com/content/dam/piramalfinance/pdf/stakeholder/debt-investors-presentation/pfl-debt-investor-presentation-q2fy26.pdf (Confirms ICRA & CARE AA/Stable, Moody’s Ba3)

Piramal Finance Financial Metrics (AUM, PAT, etc.)

- “Results Presentation Q2 FY26.” Piramal Finance, October 17, 2025. https://www.piramalfinance.com/content/dam/piramalfinance/pdf/stakeholder/investor-calls/q2fy26-results-presentation.pdf

- “Debt Investor Presentation Q2 FY26.” Piramal Finance, October 28, 2025. https://www.piramalfinance.com/content/dam/piramalfinance/pdf/stakeholder/debt-investors-presentation/pfl-debt-investor-presentation-q2fy26.pdf

Supreme Court Judgment on DHFL-Piramal Resolution (April 2025)

- “Supreme Court upheld Piramal Capital’s resolution plan for DHFL.” SCC Online, April 11, 2025. https://www.scconline.com/blog/post/2025/04/11/supreme-court-upheld-piramal-capital-resolution-plan-for-dhfl-and-set-aside-nclat-order/

- “SC upholds Piramal Capital’s DHFL resolution plan.” The Hindu, April 1, 2025. https://www.thehindu.com/news/national/sc-upholds-piramal-capitals-dhfl-resolution-plan/article69400967.ece

- Full Judgment: Piramal Capital & Housing Finance Ltd. v. 63 Moons Technologies Ltd., 2025 INSC 421. https://api.sci.gov.in/supremecourt/2022/5046/5046_2022_9_1501_60698_Judgement_01-Apr-2025.pdf

DHFL Fraud Scale (KPMG Audit, Cobrapost Exposé)

- “India’s Biggest-Ever Bank Loan Fraud: Rs 34,000-Crore DHFL Scam.” Outlook Business, July 7, 2023. https://www.outlookbusiness.com/news/what-is-dhfl-scam-india-s-biggest-ever-bank-loan-fraud-all-you-need-to-know-about-rs-34-000-crore-dhfl-scam-news-204346

- “KPMG’s special audit of DHFL red-flags fund misuse.” Business Today, October 24, 2019. https://www.businesstoday.in/latest/corporate/story/kpmgs-special-audit-of-dhfl-red-flags-fund-misuse-235909-2019-10-24

IL&FS Crisis and Ratings Downgrades (2018)

- “Rating agencies knew of stress at IL&FS, but gave good ratings: audit.” Reuters, July 21, 2019. https://www.reuters.com/article/world/rating-agencies-knew-of-stress-at-ilfs-but-gave-good-ratings-audit-idUSKCN1UG078/

- “The impact of the IL&FS downgrade on funds.” Morningstar, September 18, 2018. https://www.morningstar.in/posts/48660/the-impact-of-the-ilnfs-downgrade-on-funds.aspx

Yes Bank Crisis and Pre-Moratorium Ratings (2020)

- “Credit Alert: Cascading impact of Yes Bank moratorium.” CRISIL Ratings, March 6, 2020. https://www.crisilratings.com/en/home/our-analysis/reports/2020/03/cascading-impact-of-yes-bank-moratorium.html

- “Yes Bank Limited: Ratings downgraded.” ICRA, March 6, 2020. https://www.axistrustee.in/pdf/Yes%20Bank%20Limited%20-%28ICRA%29%206th%20March%202020.pdf

SEBI Reforms for Credit Rating Agencies (2024–2025)

- “Sebi issues new guidelines to streamline operations of credit rating agencies.” The Economic Times, July 5, 2024. https://economictimes.indiatimes.com/markets/stocks/news/sebi-issues-new-guidelines-to-streamline-operations-of-credit-rating-agencies/articleshow/111513851.cms?from=mdr

- “SEBI (Credit Rating Agencies) (Amendment) Regulations, 2025.” TaxGuru, April 3, 2025. https://taxguru.in/sebi/sebi-credit-rating-agencies-amendment-regulations-2025.html

DHFL Acquisition Details and Re 1 Valuation

- “DHFL Case: CoC members nix recovery of Rs 40k cr, want Re 1 ascribed value.” Business Standard, March 15, 2022. https://www.business-standard.com/article/companies/dhfl-case-coc-members-nix-recovery-of-rs-40k-cr-want-re-1-ascribed-value-122031500511_1.html

- “Supreme Court upholds Piramal Capital’s DHFL resolution plan.” CNBC TV18, April 1, 2025. https://www.cnbctv18.com/business/supreme-court-upholds-piramal-capital-dhfl-resolution-plan-sets-aside-nclat-order-19582255.htm

DHFL Retail Depositors Haircuts

- “DHFL’s Retail Depositors Prepare For Steep Haircuts.” BloombergQuint, January 16, 2021. https://www.bqprime.com/bq-blue-exclusive/dhfls-retail-depositors-prepare-for-steep-haircuts-bq-exclusive

- “Over 55,000 FD holders of DHFL brace for a two-thirds haircut.” Fortune India, December 21, 2020. https://www.fortuneindia.com/enterprise/over-55000-fd-holders-of-dhfl-brace-for-a-two-thirds-haircut/104965

15 Comments