Posted on 30th December, 2025 (GMT 15:55 hrs)

ABSTRACT

This article critically examines India’s external debt surge to approximately USD 747 billion by mid-2025—a near-doubling since 2014—as a hallmark of crony capitalism under the Modi regime, where liberalized external commercial borrowings (ECBs) and public sector bank hollowing facilitate upward redistribution, oligarchic consolidation (favoring conglomerates like Adani and Ambani), and asymmetric risk socialization amid volatile private dominance (over 77% non-government), USD-heavy exposure (54%), and intergenerational burdens. Intersecting with GDP misreporting flaws (IMF C-grade accounts, unorganized sector proxies inflating growth) and colonial-era inequality peaks (top 1% holding 40% wealth), this financialized precarity—diagnosed via Toussaint’s World Bank “never-ending coup” and Lazzarato’s “indebted man”—enforces neoliberal discipline, commodifies survival, and erodes sovereignty despite orthodox “sustainability” metrics. Countering GDP fetishism’s ontological violence, it invokes Mahabharata’s aṛṇī ethics of non-indebtedness alongside nisargaṛṇa stewardship, proposing pluriversal alternatives like Felber’s Common Good Balance Sheet (non-commensurable axes of dignity, solidarity, ecology), A. K. Dasgupta’s Economics of Austerity, Raworth’s Doughnut Economics, Norberg-Hodge’s localization, degrowth/post-growth sufficiency, and gift/moneyless economies to reclaim community sovereignty from predatory entanglement toward justice, reciprocity, and unburdened flourishing.

In continuation with:

1. Introduction

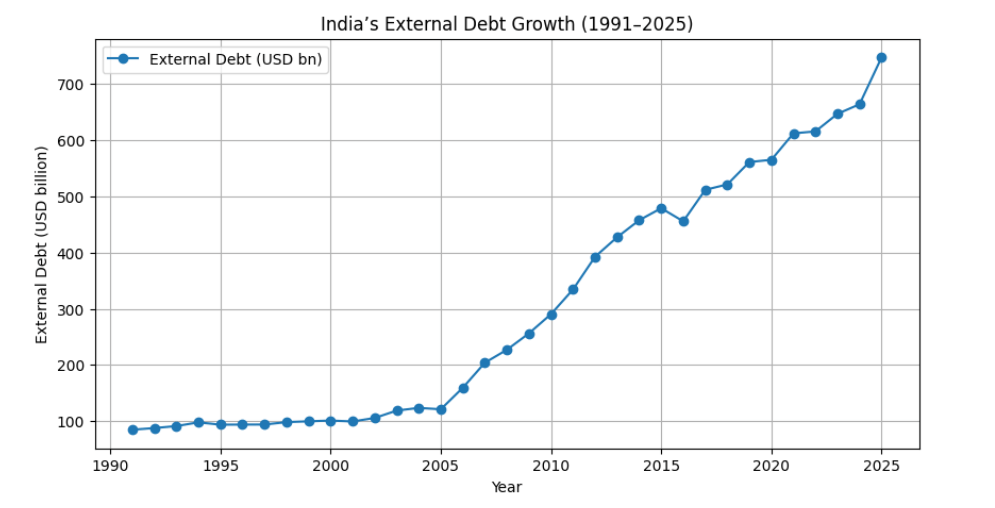

From 2014 to mid-2025, India’s external debt nearly doubled from USD 457 billion to USD 747 billion, surpassing earlier (neo-)liberalization phases. Mainstream views portray this as a benign outcome of growth and integration, but it masks a deeper political economy under the Modi regime: crony capitalism marked by corporate favoritism, erosion of public sector banks (PSBs), public disenfranchisement, and state-corporate collusion for capital accumulation. External debt has become a tool for upward redistribution, socializing risks while privatizing gains borne by the majority.

Compositionally, fragility is evident. By June 2025, external debt reached USD 747.2 billion (18.9% of GDP), with rising short-term liabilities and private corporate commercial borrowings. Post-2014 ECB liberalization, with lax oversight, fueled leveraged corporate expansion and speculation rather than productive public investment.

Politically, this aligns with a pro-business agenda favoring conglomerates like Adani, Ambani, and Piramals through opaque contracts, regulatory leniency, and monopolization. The 2016 IBC, touted as cleanup, enabled asset transfers with 60–90% haircuts, benefiting crony buyers while PSBs and the public absorbed losses.

Central to this is PSB hollowing: 2014–2024 saw INR 16.35 lakh crore (≈ USD 200 billion) in bad loan write-offs, favoring large defaulters like Mallya, Nirav Modi, and Choksi amid uneven enforcement. NPAs peaked at 14.58% in 2018, dropping to 2.5% by March 2025 not through reform but via small borrower recoveries, PSB consolidation (27 to 12), and INR 3.4 lakh crore recapitalizations (2017–2022), prioritizing optics over social lending.

Distributionally, the top 1% captures 23% of income and 40% of wealth—the highest since 1922 (World Inequality Lab, 2026)—with billionaire wealth over USD 1 trillion, ranking India third globally. This plutocracy is bolstered by electoral bonds, PM CARES, media capture, legal intimidation, and jingoism, evading accountability while downloading risks.

By late 2025, nearing USD 747 billion, debt threatens sovereignty and creditor vulnerability. IMF Article IV warnings highlight risks from financial tightening, climate costs, and contingencies, potentially pushing government debt over 100% of GDP. Debt acts as a disciplinary device, enforcing neoliberalism over social and ecological priorities, foreclosing democratic alternatives in a state of indebted unfreedom.

Post-2014 debt growth is not mere growth byproduct but a predatory regime mortgaging the future to entrench power—predation woven into policy, law, and finance. Reckoning demands confronting the political order behind the numbers.

2. India’s External Debt: Figures and the Perpetually Indebted Condition

2.1. Latest Total External Debt

As of end-September 2025, official figures from the Department of Economic Affairs remain pending (typically released late December), but end-June 2025 RBI data shows USD 747.2 billion, up USD 11.2 billion (1.5%) from March 2025 (USD 736.0 billion) and 9.6% YoY from June 2024. Valuation effects (USD 5.3 billion from dollar appreciation) mask underlying borrowing, especially private corporate.

Long-term, debt rose 65% from USD 457 billion in 2014 to nearly USD 750 billion by mid-2025 (115–230% adjusted for valuation, maturity, and private liabilities), outpacing twofold GDP growth. This gap reveals debt as a political strategy for corporate concentration, risk transfer to the public, and subordination to short-term capital interests—embedding predatory accumulation via liberalized finance and regulatory forbearance, deepening creditor dependency and limiting policy space for social and ecological needs.

2.2. Distribution by Creditor Type / Source (as of End-March/June 2025)

Debt has shifted to volatile market sources, with official aid declining. At end-June 2025:

| Creditor/Source Type | Outstanding Amount (USD Billion) | Share (%) | Key Notes/Changes |

|---|---|---|---|

| Commercial Borrowings (Private Sector ECBs, Bonds) | ~290.8 | 38.9 | Largest; surged post-2014 ECB liberalization for corporate leverage; up ~10% YoY. |

| Non-Resident Indian (NRI) Deposits | ~151.7 | 20.3 | FCNR(B)/NRE; remittance-driven but repatriation-risky; up 5% QoQ. |

| Short-Term Trade Credit | ~135.2 | 18.1 | Import-tied; volatile with rollover risks. |

| Multilateral Creditors (e.g., World Bank, ADB, IMF, AIIB, NDB, EIB, IFAD) | ~61.3 | 8.2 | Official bulk; AIIB/NDB rising for favored infrastructure. |

| Bilateral Creditors (Government-to-Government) | ~32.2 | 4.3 | Down from 4.4%; Japan leads (USD 23.3 bn, ~72%), Russia (~13.6%), Germany (~9.6%), France (~4.1%); minimal growth. |

| Other Government External Debt (OGD: Foreign-Held Securities, Defense Debt, etc.) | ~66.5 | 8.9 | Sovereign bonds; slight rise, rate-hike vulnerable. |

| Others (e.g., Portfolio Debt, IMF SDR Allocations) | ~9.5 | 1.3 | Minor; speculative inflows. |

Official creditors (multilateral/bilateral) now ~12–13% (down from 20% in 2014), while private/commercial exceed 57%, with NRI and short-term filling the rest. DEA frames this as market integration, but it recomposes dependency: concessional official debt replaced by ECBs favoring conglomerates for monopolistic expansion. Risks are asymmetric—private gains from leverage, public socialization of losses amid volatility.

2.3. Additional Contextual Indicators

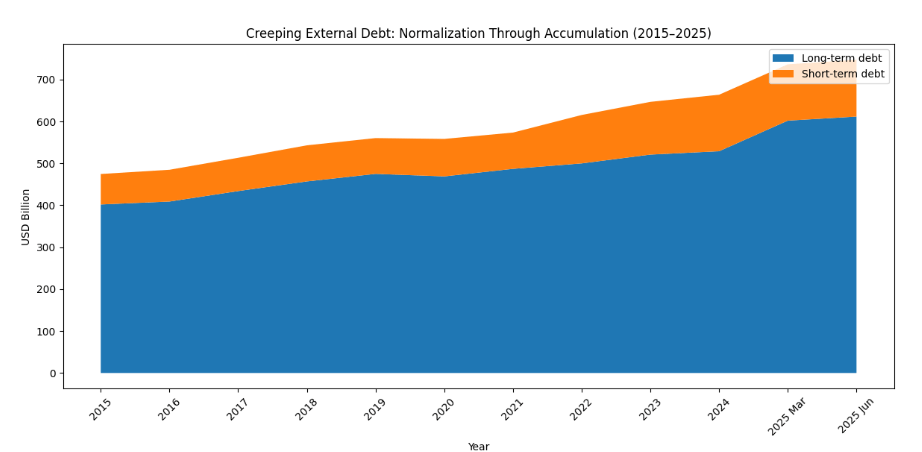

- Maturity Profile: Long-term (>1 year) USD 611.7 billion (81.9%, up USD 9.8 billion QoQ), deferring rollover but locking in repayments and compressing fiscal space; short-term USD 135.5 billion (18.1%), exposing to demand shocks and global tightening.

- Currency Denomination: Dollar-heavy (53.8%), heightening Fed and liquidity risks; INR (30.6%) offers partial hedge amid rupee depreciation; yen (6.6%), SDRs (4.6%), euro (3.5%) add mismatch vulnerabilities, transmitting advanced-economy shocks to domestic burdens.

- Sustainability Metrics: Debt-GDP 18.9% (down from 19.1%), reserves cover 90.8% (up from 88.5%). These suggest stability but obscure sectoral leverage, contingencies, and shock sensitivity in stagflation or geopolitical contexts.

Overall, the profile seems manageable by orthodox measures, yet high-level long-term risks are systemically deferred—embedded in maturities, dollar dominance, and private exposure—making resilience contingent on benign conditions, with asymmetric adjustment costs on the public.

2.4. Decoding the Debt Structure: Private Dominance and Hidden Risks

Minimal bilateral debt (4.3%) underscores private, market dominance (commercial/NRI ~59%), bypassing sovereign channels but implicating the state as guarantor in crises. Long maturities defer but intergenerationalize risks, transferring corporate leverage to future public obligations. Dollar dominance inflates liabilities via depreciation (~5% YoY), eroding wages and consumption for households.

This crystallizes crony dynamics: liberalized foreign capital enables oligarchic scaling in infrastructure and platforms, with downside socialized through PSBs, contingencies, and stabilization. Intersecting elevated general government debt (81–84% GDP), IMF flags climate, growth, and liability risks, amplified externally.

Orthodox indicators reassure, but regressively: inflationary pass-through and welfare constraints burden the masses, multiplying inequality (top 1% at colonial peaks). Debt thus amplifies oligarchic capture, eroding sovereignty via domestic rather than just foreign control.

Structural rupture is needed: independent audits tracing beneficiaries/risks, progressive corporate/wealth taxes, and PSB revival for inclusive credit. Absent this, debt entrenches domination—financial, political, generational.

3. Arranging Chronologies: India’s Relentless Indebtedness?

India’s external debt spans two phases. From 1947 to ~2013, borrowing was cautious, concessional, and state-led, aligned with post-colonial sovereignty and planning, rising episodically for balance-of-payments but institutionally restrained.

Post-2014 marks rupture: aggressive liberalization swelled private/commercial liabilities, empowering crony conglomerates while heightening vulnerabilities like currency exposure and public contingencies.

This arc—from frugal developmentalism to staggering obligations—reflects political choices: evolving from guarded autonomy to financialized oligarchy, where debt consolidates power over national futures.

The following sections dissect this evolution quantitatively and structurally: first through a stark comparison of pre- and post-2014 phases, then via a concise historical overview that exposes the accelerating pace of indebtedness under the current regime.

4.1. Key Period Comparisons (1947–2013 vs. 2014–2025)

Using verified RBI and World Bank data for consistency:

- 1947–2013: Debt rose from ~$0.1B (negligible at independence, with India as a net creditor post-colonial transfers) to $427.3B. ➡️ Total increase: ~$427.2B over 66 years; annualized: ~$6.5B/year; CAGR: 13.5% (high from low base).

- 2014–2025: Debt rose from $457.5B to $747.2B (end-June 2025, latest RBI figure; end-September data pending release by late December 2025, with trends indicating stability or modest growth amid rupee volatility and trade pressures). ➡️ Total increase: ~$289.7B over 11 years; annualized: ~$26.3B/year; CAGR: 4.6% (moderate on larger base).

📌 Interpretation

- The 1947–2013 era’s larger absolute growth stems from the extended timeline and zero-start in a closed economy, but early phases were slow.

- Post-2014 acceleration in annualized terms reflects liberalization, ECB easing, and corporate borrowing surges, though lower CAGR signals maturing economy dynamics.

- Inflation-adjusted (US CPI basis): Recent real growth appears amplified, yet balanced by India’s 6–7% GDP expansion (vs. ~4% pre-1991), underscoring structural shifts toward private-led integration.

4.2. Overview

India’s external debt evolution closely tracks shifts in its political–economic regime. In the decades following independence (1947–late 1960s), external debt remained negligible, shaped by Nehruvian socialism, Five-Year Plans, import substitution, and a strong aversion to external financial dependence born of colonial experience. Development finance during this phase relied primarily on domestic resource mobilization, public sector expansion, and limited concessional aid, rather than market-based foreign borrowing.

From the 1970s through the 1980s, external debt began to rise, reflecting both structural pressures and policy choices. The Indira Gandhi period—marked by bank nationalization, expanded state control, and redistributive rhetoric—did not eliminate borrowing, but kept it state-mediated and politically constrained. Debt increases during this era were driven less by liberalization than by oil shocks, food imports, and balance-of-payments stress, culminating in the vulnerabilities exposed by the late 1980s.

The 1990s represent a decisive inflection point. The balance-of-payments crisis of 1991 precipitated structural adjustment and neo-liberalization, opening the economy to foreign capital, commercial borrowing, and market-determined exchange rates. External debt rose more sharply, though still within a framework where sovereign and multilateral lending dominated, and private corporate exposure remained limited.

Post-2000, and especially after 2014, external debt entered a qualitatively different phase. Liberalization of capital accounts, external commercial borrowings, and financial markets accelerated debt accumulation, with a growing shift from public, concessional debt to private, market-based liabilities. What began as integration into global finance has increasingly evolved into financialized accumulation, where external debt fuels corporate concentration and systemic risk rather than broad-based development.

The following table offers a compressed historical snapshot of India’s external debt trajectory from independence to mid-2025, situating numerical increases within their political-economic contexts. Rather than a linear story of “developmental necessity,” it reveals how shifts from aid-based borrowing to market-driven external commercial debt—intensified after liberalization and especially post-2014—have progressively normalized indebtedness as a structural condition of a dominant narrative of growth.

| Period/Year | External Debt (Billion USD) | Key Notes/Context |

|---|---|---|

| 1947 | ~0.1 | At independence, debt was negligible; India held claims on Britain from WWII contributions and colonial “Home Charges” (estimated ~$45B in today’s terms drained pre-1947, but no formal external borrowings). |

| 1970 | 8.4 | Early borrowings for development aid; closed economy limited exposure. |

| 1980 | 20.7 | Gradual rise via multilateral loans (e.g., IMF/World Bank) amid oil shocks. |

| 1990 | 83.5 | Pre-crisis peak; debt/GDP hit ~38% due to fiscal imbalances and Gulf War effects. |

| 2000 | 101.1 | Post-liberalization stabilization; focus on commercial borrowings. |

| 2010 | 290.4 | Surge from globalization, FDI inflows, and infrastructure needs. |

| 2013 | 427.3 | End of pre-2014 era; driven by external commercial borrowings (ECBs) amid slowing growth. |

| 2014 | 457.5 | Start of accelerated phase; policy shifts like Make in India boosted inflows. |

| 2020 | 565.0 | COVID-19 impacts; temporary slowdown but resilient due to reserves. |

| 2023 | 646.8 | Post-pandemic recovery; rise tied to private sector ECBs. |

| 2025 (June) | 747.2 | Latest high; includes $5.1B valuation loss from USD depreciation vs. INR/yen/euro/SDR. Excluding valuation, increase was $6.2B QoQ. |

Below are annual end-year (primarily end-March) external debt stocks, compiled from RBI and World Bank sources. For conciseness, only select benchmark years are highlighted here; the full post-1970 series is accessible through RBI archival data and Macrotrends.

| Year | External Debt ($B) | Key Drivers/Notes |

|---|---|---|

| 1970 | 8.4 | Aid-focused borrowings in closed economy. |

| 1980 | 20.7 | Oil shocks prompt multilateral loans. |

| 1990 | 83.5 | Pre-crisis peak; debt/GDP ~38%. |

| 2000 | 101.1 | Stabilization post-liberalization. |

| 2010 | 290.4 | Globalization, FDI, infrastructure surge. |

| 2013 | 427.3 | ECB rise amid slowing growth. |

| 2014 | 457.5 | Policy shifts boost inflows. |

| 2020 | 565.0 | COVID impacts; reserve buffers hold. |

| 2023 | 646.8 | Post-pandemic ECB recovery. |

| 2025 (June) | 747.2 | Peak; private sector dominance. |

Trends:

Prior to 1991, India’s external debt growth was episodic, driven largely by exogenous shocks (oil price spikes, droughts, balance-of-payments stress) rather than sustained market borrowing. From the early 2000s, external debt began to rise on a steadier trajectory—roughly 8–10% compound annual growth—reflecting deeper financial integration. This trend accelerated after 2014, propelled not by trade expansion alone but by systematic deregulation of external commercial borrowings (ECBs), relaxation of sectoral caps and end-use restrictions, longer maturity permissions, higher borrowing limits for large corporates, and increased reliance on market-based foreign finance. Together, these measures shifted external debt accumulation from sovereign and concessional channels toward private, corporate-led borrowing, embedding higher exposure to global liquidity cycles and currency risk.

4. 3. Growth Analysis

- Total Increases: 1947–2013 added ~$427B; 2014–2025 added ~$290B—~68% of the long-term total in just 17% of the time.

- Annualized Metrics:

- 1947–2013: ~$6.5B/year; 13.5% CAGR (high due to low base).

- 2014–2025: ~$26.3B/year; 4.6% CAGR (moderate, aligning with emerging market norms).

- Drivers: Pre-2014 growth was episodic (e.g., 1991 crisis response, multilateral aid); post-2014 acceleration stems from ECB liberalization, rupee-denominated bonds, and private sector expansion, with pandemic borrowing spikes (2020–2022).

4.4. Debt Composition and Structure (End-June 2025)

- By Borrower: Non-financial corporations ~36% (infrastructure-heavy); deposit-taking institutions ~27%; general government ~23% (down QoQ); others ~14%. Private sector drives surges.

- By Instrument: Loans 34.8% (largest); currency/deposits 23%; trade credits/advances 17.7%; debt securities 16.8%. Long-term: 81.9% ($611.7B, +$10.3B QoQ); short-term: 18.1% ($135.5B).

- By Currency: USD 53.8% (high Fed exposure); INR 30.6%; yen 6.6%; SDR 4.6%; euro 3.5%. Reduces some translation risks but amplifies USD volatility.

- Residual Maturity: Short-term (<1 year) ~40.7% of total, signaling rollover vulnerabilities.

4.5. Sustainability Indicators

- Debt/GDP: 18.9% (June 2025), down from 19.1% (March)—low globally (vs. ~50% emerging market average).

- Reserves Coverage: Forex reserves (~$693B as of mid-December 2025) cover >90% of debt; debt service ratio stable at 6.6% of current receipts.

- International Position: Assets/liabilities ratio ~79% (improved). Overall, buffers offer shock resilience.

4A. India’s Indebtedness Hyper-Focalized (1991-2025)

The period from 1990-91 to mid-2025 is crucial because it marks India’s transition from episodic, crisis-induced external borrowing to a structurally normalized regime of debt-led growth embedded in global finance. The 1991 balance-of-payments crisis was not merely a macroeconomic rupture but a constitutive moment: it institutionalized liberalization, deregulation, and capital-account openness as permanent policy logics rather than emergency measures. What followed was a qualitative shift in the nature of external debt—from multilateral, state-mediated borrowing toward private, market-based external commercial borrowings (ECBs) tied to corporate expansion, infrastructure financialization, and speculative capital flows.

This period also captures the political economy of consolidation. Especially after 2014, external debt growth increasingly aligned with selective liberalization that privileged large conglomerates, facilitated asset concentration, and translated sovereign credibility into private leverage. Debt thus ceased to function primarily as a developmental bridge and instead became a mechanism of upward redistribution, masked by narratives of fiscal discipline, resilience, and “sustainable” growth. Reading 1990–2025 together reveals how crisis management evolved into policy capture, and how external debt became a structural feature of India’s post-liberalization accumulation regime rather than a temporary response to scarcity.

4A.1. Data Note: Latest Figures and Provisional Estimates

As of December 29, 2025, the most recent officially confirmed data covers end-June 2025, showing external debt at USD 747.2 billion. End-September 2025 figures are typically released in late December; provisional estimates suggest a range of USD 755–760 billion, reflecting continued private commercial borrowing, rupee depreciation, and exposure to global interest rate hikes. Separating the confirmed and provisional figures is essential to maintain analytical precision, avoid misleading interpretations, and clearly distinguish recorded debt stocks from short-term extrapolations, particularly in a period of volatile capital flows and currency adjustments.

Below is a consolidated historical table (end-March fiscal year-end unless noted, in USD billions, from RBI/DEA/World Bank sources):

| Year/Period | External Debt | YoY Change (%) | Notes/Context |

|---|---|---|---|

| 1991 | 84.85 | N/A | Post-liberalization baseline; debt-to-GDP ~28.3%, IMF loans dominant. |

| 1992 | 87.78 | +3.5 | Early reforms; multilateral aid key. |

| 1993 | 91.33 | +4.0 | Gradual FDI inflows. |

| 1994 | 97.90 | +7.2 | – |

| 1995 | 93.81 | -4.2 | Rupee stabilization dip. |

| 1996 | 93.97 | +0.2 | – |

| 1997 | 94.06 | +0.1 | – |

| 1998 | 98.33 | +4.5 | Asian crisis spillover; short-term rise. |

| 1999 | 99.78 | +1.5 | – |

| 2000 | 101.13 | +1.4 | Tech boom. |

| 2001 | 99.50 | -1.6 | – |

| 2002 | 105.74 | +6.3 | – |

| 2003 | 118.88 | +12.4 | Post-2000s globalization acceleration. |

| 2004 | 123.64 | +4.0 | – |

| 2005 | 121.20 | -2.0 | – |

| 2006 | 159.53 | +31.6 | Commercial borrowings surge. |

| 2007 | 204.06 | +27.9 | ECB liberalization amid liquidity glut. |

| 2008 | 227.11 | +11.3 | Pre-GFC peak. |

| 2009 | 256.31 | +12.9 | GFC stimulus. |

| 2010 | 290.43 | +13.3 | UPA infrastructure push. |

| 2011 | 334.40 | +15.1 | – |

| 2012 | 392.58 | +17.4 | Taper tantrum risks. |

| 2013 | 427.25 | +8.8 | Rupee crisis. |

| 2014 | 457.51 | +7.1 | Modi onset; ECB easing. |

| 2015 | 478.83 | +4.7 | – |

| 2016 | 455.54 | -4.9 | Demonetization precursor. |

| 2017 | 511.58 | +12.3 | GST rollout. |

| 2018 | 521.18 | +1.9 | NPA peak; IBC asset flips. |

| 2019 | 561.02 | +7.6 | – |

| 2020 | 564.98 | +0.7 | COVID moratoriums. |

| 2021 | 611.99 | +8.3 | Pandemic inflows. |

| 2022 | 615.52 | +0.6 | Inflation recovery. |

| 2023 | 646.79 | +5.1 | Rupee depreciation. |

| 2024 (End-Mar) | 663.80 | +2.6 | Commercial dominance. |

| 2025 (End-Mar) | 736.30 | +10.9 | Record surge. |

| 2025 (End-Jun) | 747.20 | +1.5 | Valuation adds $5.3B QoQ. |

| 2025 (End-Sep, Prov.) | ~755–760 | +1–2 | Pending; trade/ECB uptick. |

4A.2. Insights: A Scorching Indictment of Debt-Fueled Inequality

What: Between 1991 and 2025, India’s external debt-to-GDP ratio fell from 28.3% to 18.9%, giving the impression of macro-stability. Yet beneath this nominal decline lies a structural transformation: debt grew modestly in the 1990s (~3% YoY), surged post-2006 (10–30% YoY) with liberalized inflows, doubled after 2010, and spiked 63% post-2014. The rise increasingly financed private corporate expansion rather than public development.

How: This shift operated through financialization and selective liberalization:

- Large conglomerates accessed cheap external commercial borrowings (ECBs), leveraging sovereign credibility and forex reserves (~91% coverage, long-term ~82%) to de-risk their balance sheets.

- When leveraged positions faltered, public sector banks (PSBs) absorbed losses, socializing risk while privatizing gains.

- Over half the debt (~54%) is USD-denominated, exposing the economy to currency shocks that disproportionately impact wages and living costs, while inflows favor capital-rich sectors.

Why: The structural shift matters because it reconfigures distributional outcomes and policy logic: macro-stability narratives mask an underlying regime of upward redistribution. Debt facilitates corporate consolidation, enriches the top 1% (~40% wealth share), and entrenches wage stagnation, while the broader population bears exposure to inflation, currency shocks, and fiscal austerity. In essence, what looks like prudence is a strategic use of external debt to reinforce plutocratic accumulation under the guise of economic resilience.

4A.3. Why a Full “Creditor-Type by Year” Table Remains Elusive—and Conveniently So

Data opacity persists: RBI/DEA reports provide sporadic breakdowns (e.g., bilateral ~4%, multilateral ~8%, commercial ~39%), but historical series are inconsistent—pre-2010 emphasizes borrower type, post-2014 instruments. Bilateral shares fell from 10–15% (1990s–2000s) to <5% as private flows rose, shielding crony networks. Compiling requires mining 40+ PDFs, a barrier enabling impunity.

4A.4. What’s Available from Official Reports: A Patchwork for the Persistent

RBI’s “External Debt: Status Report” and DEA annuals offer:

- Creditor snapshots (e.g., 2024–25: bilateral USD 32.2B, multilateral ~61B).

- Maturity/instrument annually (long-term >80% since 2010).

- Borrower quarterly (non-govt ~80% by 2025).

4A.5. The Shift After 2014: A Catastrophic Pivot to Crony Oligarchic Plunder

Pre-2014, India’s external debt, while tied to the WB–IMF–WTO apparatus, retained a modicum of so-called “developmental” intent, preserving (perhaps) sovereign discretion and some social priorities despite structural flaws. Post-2014, the Modi regime shattered this framework, inflating debt by over 60% to serve crony conglomerates, subordinating national sovereignty to corporate interests, and exposing the masses to currency, fiscal, and inflationary shocks while concentrating wealth and risk in the hands of the superrich.

Three policy betrayals:

- ECB Liberalization: Removed restrictions, enabling offshore borrowing for tycoons (Adani ports, Ambani refineries), offloading risks to PSBs amid rupee falls (30% since 2014).

- Abdication of State Financing: Gutted PSBs via mergers and write-offs (INR 16+ lakh crore since 2014), favoring PPPs and private leverage over public welfare.

- Corporate-Led Growth Myth: Fetishized “wealth creators,” yielding unemployment highs and billionaire surges (USD 1 trillion wealth) while exports/R&D lag.

Key indicators:

Debt-to-GDP ratio remains superficially stable at 18.8–18.9% in 2024–25, yet this veneer conceals significant structural bloat. Non-government liabilities dominate at 14.7% of GDP (up from 14.4%), reflecting the growing role of private external commercial borrowings, while government debt accounts for 4.4% (up from 4.1%), indicating modest fiscal expansion.

Short-term obligations are relatively contained at ~18.1% of total external debt (June 2025 lows), but currency mismatches and heavy USD exposure (~54%) amplify systemic vulnerability, making the economy highly sensitive to global interest-rate shocks, exchange-rate fluctuations, and sudden reversals of capital inflows. On balance, stability on paper masks deeply asymmetric risk structures, where private corporate leverage and sovereign guarantees intertwine, concentrating exposure on the broader population while insulating crony-monopoly capitalist actors.

This debt architecture systematically erodes national sovereignty, echoing IMF warnings about unsustainable exposure, and demands urgent interventions: moratoriums on predatory repayments, transparent audits of external obligations, and redirection of borrowed funds toward public investment to curb plutocratic capture and restore social accountability.

4A.6. External Debt in Modi’s “New India” (?!): 2015–2025

(USD billions, end-March unless noted; RBI/DEA/ICRA data.)

| Year | Total | Long-Term | Short-Term | Govt. | Non-Govt. | Notes |

|---|---|---|---|---|---|---|

| 2015 | 474.7 | 402.0 | 72.7 | 91.1 | 383.6 | Taper aftermath; debt-to-GDP 23.3%. |

| 2016 | 484.8 | 409.0 | 75.8 | 95.4 | 389.4 | Oil decline aids CAD. |

| 2017 | 513.4 | 434.0 | 79.4 | 102.3 | 411.1 | GST spurs inflows. |

| 2018 | 543.1 | 457.0 | 86.1 | 104.2 | 438.9 | ECB surge; NPA peak. |

| 2019 | 560.4 | 475.0 | 85.4 | 107.0 | 453.4 | Pre-COVID stability. |

| 2020 | 558.4 | 469.0 | 89.4 | 115.3 | 443.1 | Moratoriums inflate risks. |

| 2021 | 573.5 | 487.0 | 86.5 | 118.4 | 455.1 | Liquidity boom. |

| 2022 | 615.5 | 500.0 | 115.5 | 130.0 | 485.5 | Inflation recovery. |

| 2023 | 646.8 | 521.0 | 125.8 | 133.2 | 513.6 | Rupee strain. |

| 2024 | 663.8 | 529.0 | 134.8 | 141.0 | 522.8 | Commercial ~38%; debt-to-GDP 18.8%. |

| 2025 (Mar) | 736.3 | 602.0 | 134.3 | 152.0 | 584.3 | Valuation/fresh borrowings. |

| 2025 (Jun) | 747.2 | 611.7 | 135.5 | 155.0 | 592.2 | QoQ rise $11.2B; reserves 90.8%. |

| 2025 (Sep, Prov.) | ~755–765 | ~618–625 | ~136–140 | ~158 | ~597–607 | Pending; rupee pressure. |

4A.7. Critique: Risks, Policy Failures, and Systemic Vulnerabilities

Official narratives tout “sustainability” and “prudence,” but this is a grotesque deception concealing a predatory apparatus designed for plutocratic extraction. Surface metrics—18.9% debt-to-GDP, >90% reserves coverage—project calm, yet beneath lies a toxic brew of volatility and capture, where debt props up oligarchic empires while exposing the nation to cascading crises.

Layer 1: Unsustainable Trajectory and Deceptive Metrics Debt has tripled since 2010, reaching $747.2B by mid-2025, routinely surpassing GDP growth in bursts. The post-2014 4.6% CAGR is no moderation—it’s a symptom of fiscal deficits (~5–6% GDP) plugged by foreign inflows, breeding chronic dependency. USD hegemony (53.8%) isn’t strategy; it’s servitude, binding India to Fed tantrums and rupee plunges (2022’s sharp fall as proof), where servicing costs explode. Quarterly “valuation” gains/losses ($5.1B loss in June 2025) camouflage relentless fresh borrowing, transforming debt into a high-stakes wager on global whims.

Layer 2: Structural Frailties and Imminent Triggers Hidden bombs abound: ~41% residual short-term maturity invites 2008-style panics, demanding exorbitant rollovers or capitulation to creditors. Private dominance (~77% non-government) courts contagion—over-leveraged sectors (infra, telecom) could implode, migrating defaults to sovereign books. Peers expose the sham: China’s ~14% GDP ratio backed by vast reserves; Brazil’s higher levels ignite crises. India’s “low” external figure distracts from total public debt (~84% GDP including states), devouring resources for health/education while tycoons flourish. Volatile components—NRI deposits (20%), trade credits (18%)—threaten sudden reversals in stagflationary winds.

Layer 3: Policy Sabotage and Crony Complicity The regime’s “ease of business” is code for betrayal: post-2014 ECB deregulation unleashed unrestricted offshore borrowing for conglomerates like Adani and Ambani, stripping safeguards while offloading currency risks to PSBs and taxpayers. Populist excesses override reforms, with debt as lifeline amid INR 16+ lakh crore write-offs—brazen theft rewarding fugitives. The IBC? A facade for asset grabs, imposing 60–90% haircuts on public banks. Echoes of 1991’s 38% GDP crisis resound; today’s levels could detonate below 5% growth amid export stagnation or oil surges. This is engineered class assault: tycoons (~36% borrower share) insulate gains, while inflation/taxes ravage the masses, entrenching top 1% wealth at 40% (colonial-era highs).

Layer 4: Sovereignty Erosion and Power Asymmetries Debt embodies control: minor official shares (multilateral 8%, bilateral 4%) belie lurking conditionalities, poised for IMF-dictated cuts as warnings escalate (general debt risks >100% GDP in stresses). Market flows (59%) enforce invisible discipline—ratings, yields coerce pro-creditor policies, stifling alternatives like wealth taxes. Hindutva spectacles divert from this plunder, normalizing a trap where growth enriches conglomerates, inequality-adjusted HDI craters, and 800 million subsist on rations.

Layer 5: Catastrophic Outlook and Urgent Reckoning Recession, geopolitics, or climate exigencies could catapult debt to $1T by 2030, service ratios >10%, unleashing brutal austerity—gutted welfare, regressive levies, asset fire-sales. RBI’s valuation/forward alerts and IMF scenarios confirm the abyss. Absent revolutionary action—crony loan audits, punitive wealth/corporate taxes, PSB reclamation for inclusive finance—India barrels toward implosion, forfeiting sovereignty to creditors and dooming generations to plutocratic yoke.

While 1947–2013’s era built cautiously, 2014–2025’s frenzy in Modi’s “Viksit Bharat” reveals crony capitalism’s venom. Debt isn’t progress—it’s predation, necessitating fierce overhaul to wrest back an equitable path from oligarchic grasp.

5. India’s Per-Capita External Debt (2025)

India’s external debt stands at US$ 747.2 billion as of mid-2025.

With a population of approximately 1.464 billion people, this works out to roughly US$ 510 per person.

Calculation: US$ 747.2 billion ÷ 1.464 billion people ≈ US$ 510 per person.

This per-capita figure provides a simple way to grasp the scale of the country’s external debt burden when spread across every individual, including children and non-working adults.

Because population and external debt both grow over time, per-capita debt reflects the net effect of the two — which in recent years has meant a rise, due to debt rising faster than population.

5.1. Limitations & What “Per-Capita Debt” Really Means

- It is a “division-average”, not the amount each person or household actually owes. External debt is owed by the country (central + private + corporate sectors) to foreign creditors — not by each individual.

- Exchange rate, currency composition matters. External debt is denominated in multiple currencies; USD-equivalent figures may fluctuate with exchange-rates.

- Debt structure (maturity, interest, repayments) matters — high external debt but long maturities or concessional terms may be less risky than seemingly “low” debt with short maturities.

- Population estimate is approximate, especially in 2025 (mid-year, projections) — fine for ballpark per-capita, but not precise to the rupee.

6. India’s Macroeconomic Indicators, GDP Misreporting, and the Architecture of Debt

In official economic discourse, India increasingly frames itself as a rising global power on the strength of its GDP size, with multiple authoritative estimates projecting it as the world’s fourth‑largest economy in 2025. According to the International Monetary Fund’s April 2025 World Economic Outlook, India’s nominal GDP is estimated at approximately $4.19 trillion in 2025, just ahead of Japan’s roughly $4.18 trillion, thereby moving India up from fifth place in 2024 to fourth place globally behind only the United States, China, and Germany. Government and policy institutions such as NITI Aayog have cited these figures to underscore India’s purported economic emergence, noting that India’s per capita income has roughly doubled over the past decade alongside this ascent in global rankings. While these rankings attract attention in public discourse and policy narratives, headline GDP size figures do not (at all) fully account for underlying structural, measurement, and distributional complexities in the economy as part of the bigger picture of neoliberal capital-relations.

6.1. IMF Concerns About India’s National Accounts

India’s national accounts—GDP and GVA—received a C-grade from the IMF, signaling significant statistical weaknesses. Key concerns include:

- GDP calculation methodology: Reliance on proxying the unorganized sector from organized sector trends.

- Base year (2011–12): Potentially outdated and misaligned with structural shifts.

- GDP deflator: Current reliance on the Wholesale Price Index (WPI) ignores services (the largest sector), producing overestimated real growth.

- Seasonal adjustments: Limited and insufficient, causing quarterly misrepresentation.

- Production vs. expenditure discrepancy: Growing gaps (0.5–1% pre-demonetization to 2–5% post-pandemic) reflect systemic measurement errors.

IMF stress tests and consultations (2024–2025) underline structural vulnerabilities despite moderate debt-to-GDP ratios (~18.9%) and strong reserves ($693.32 billion, RBI Dec 2025). These include sensitivity to interest-rate shocks, rupee depreciation, climate-related fiscal burdens, and latent off-balance-sheet risks.

6.2. GDP Calculation and Structural Misrepresentation

Presenting Perspective-1

- Overstated growth: Official GDP figures (~8.2% for Q2) may be 48% higher than reality; adjusted estimates suggest 4–5% growth.

- Unorganized sector (~45% of GDP, ~30% of non-agriculture GDP) is poorly captured:

- Trade (neighborhood stores), textiles, and leather goods are declining.

- Post-demonetization, GST, NBFC crises, and pandemic shocks disproportionately affected this sector.

- Benchmarking “bad years” against “good years” inflates growth.

- Quarterly GDP estimates rely heavily on organized sector proxies; lack of independent high-frequency data introduces systemic errors.

- CPI concerns: Current baskets poorly reflect consumption patterns of low-income households; GST-driven price declines mainly benefit the organized sector.

Presenting Perspective-2

- Proxies are necessary due to data limitations; direct, frequent surveys are expensive.

- GDP series revisions aim to incorporate more frequent and direct surveys, improving unorganized sector representation.

For a more detailed analysis, view the following:

6.3. Year-on-Year vs. Quarter-on-Quarter Growth Distortions

India reports GDP growth YoY, unlike most large economies (U.S., Brazil, China) that report QoQ growth:

- YoY reporting masks current momentum.

- Example: Government Q3 YoY growth = 0.4%; JP Morgan QoQ calculation = 5.7%.

- FY2021–22 budget projections of 11% YoY growth implied ~1% average QoQ growth, concealing actual quarter-to-quarter deceleration.

Implications:

- Pre-pandemic structural weaknesses—financial sector non-performing loans, sluggish exports—persist.

- Manufacturing has recovered; services sector, employing a majority of women, remains weak, generating unemployment and widening gender disparities.

- Fiscal measures (e.g., 0.2% GDP infrastructure spending) and privatization do not address these imbalances.

Conclusion: YoY reporting creates a false sense of economic recovery, while QoQ data would better inform policy interventions.

6.4. Production vs. Expenditure and Deflator Issues

- Production-expenditure gap: Inaccuracies in unorganized sector data affect both sides, complicating choice of “controlling total.”

- GDP deflator error: Using WPI rather than service-inclusive indices overstates real GDP growth; double deflation is not performed.

- Seasonal adjustment: Partial adjustments cause Q4 overstatements and Q1 understatements, though this is secondary to structural measurement flaws.

6.5. Debt as a Constitutive Feature of Contemporary Capitalism

Debt in India is not neutral; it structures contemporary capitalism and enforces distributional hierarchies:

- External debt boom: From ~$409 billion in 2013 to $747.2 billion by June 2025.

- Debt orchestrates who accrues wealth and who bears costs, embedding discipline on states, constraining democratic policymaking, and privileging corporate expansion.

Why the “Debt Is Sustainable” Argument Falls Short

- Apologists cite moderate debt-to-GDP (~18.9%), high reserves, and long-term maturities (~82%).

- Sustainability must also consider shock resilience, social legitimacy, equitable burden-sharing, and long-term viability.

- Vulnerabilities: rupee depreciation (4–5% in 2025), global rate hikes, capital flight, and creditor influence on policy tilt toward investor interests.

- Debt reallocates resources from multitudes to magnates, present to posterity, commons to corporations.

IMF Stress Tests and Vulnerabilities

- IMF Article IV consultations highlight nuanced risks despite moderate headline debt metrics:

- Interest-rate shocks elevate corporate ECB costs and public exposure.

- Rupee depreciation inflates foreign-currency obligations.

- Growth deceleration (e.g., 5–6% plausible) reduces revenue, accelerating debt accumulation.

- Climate imperatives (adaptation, mitigation) necessitate trillions in borrowing, structurally inflating liabilities.

- Hidden liabilities (utilities, SOE guarantees) can abruptly emerge on public balance sheets.

- Private external debt often converts to public exposure during crises.

- Strengths: rupee-denominated sovereign debt, reserves (~93% external coverage).

- Per-capita external debt: ~$510–515, highlighting systemic strain exceeding demographic growth.

Critical insight: Debt enforces compliance, embeds anticipatory restraint, diffuses risks downward, and constrains democratic policymaking without overt coercion, epitomizing contemporary capitalism’s operational logic.

6. Key Takeaways

- GDP overestimation: Post-demonetization, GST, and pandemic impacts disproportionately hit the unorganized sector, skewing growth figures upward.

- CPI underrepresentation: Price indices fail to capture consumption realities of the poor.

- QoQ vs. YoY distortion: Current reporting masks slowing momentum and structural weaknesses.

- Debt as governance: External debt enforces systemic asymmetries, privileging capital while constraining public autonomy.

- IMF validation: External assessments confirm measurement flaws and highlight vulnerability despite stable ratios.

- Government reforms: Efforts are underway to revise GDP, CPI, and unorganized sector metrics, but structural challenges remain significant.

Overall, India’s macroeconomic picture combines statistical misrepresentation, structural fragility, and debt-mediated governance, revealing a complex interplay between reported growth, real economic conditions, and the systemic imperatives of contemporary capitalism.

7. The Ethics of Non-Indebtedness: Defying the GDP Globalitarianism

To dismantle the GDP fetish, critique alone is insufficient. What is required is an ethical inversion—a rejection of the “financial bourgeoisie” model of prosperity in favour of what E. F. Schumacher might have called the “austerity of output”: minimum consumption, maximum socio-ecological usefulness, and minimum waste. This inversion finds a profound civilizational echo in the Yaksha Praśna of the Mahābhārata.

When asked by the Yaksha—Dharma in disguise—“Who is truly happy?”, Yudhiṣṭhira replies:

पञ्चमेऽहनि षष्ठे वा शाकं पचति स्वे गृहे ।

अनृणी चाप्रवासी च स वारिचर मोदते ॥

pañcame’hani ṣaṣṭhe vā śākaṃ pacati sve gṛhe |

anṛṇī cāpravāsī ca sa vārīcara modate ||

Yudhishthira answered, ‘O amphibious creature, a (hu)man who cooketh in his own house, on the fifth or the sixth part of the day, with scanty vegetables, but who is not in debt and who stirreth not from home, is truly happy.’

The economics of happiness here is not abundance but absence of entanglement—freedom from debt, displacement, and dependence. In contemporary India, where household indebtedness approaches 42% of GDP, this wisdom reads not as ascetic nostalgia but as a radical diagnosis of contemporary neoliberal precarity. Debt-driven consumption replaces wage growth; credit substitutes for public provisioning; survival itself is financialized.

This perspective resonates deeply with A.K. Dasgupta’s The Economics of Austerity (1975), where the eminent Indian economist critiques capitalism’s evolution into a phase of luxury consumption to sustain growth, once basic needs are met. Drawing on classical thinkers like John Stuart Mill, Dasgupta advocates for a “stationary state” of no economic growth, emphasizing equitable distribution, population control, and technical innovations for sustainable comfort without the competitive scramble for more. He aligns this with Gandhian principles of limiting wants, self-sufficiency through meaningful labour (e.g., via the charkha), and ethical trusteeship over wealth, viewing austerity not as deprivation but as instrumental for poor economies to avoid inequality and ecological strain. In Dasgupta’s words, Mill’s vision offers a “benign equilibrium” where human potential flourishes beyond growth fetishism, prefiguring modern critiques of financialized survival and debt dependency. Applied to India’s neoliberal context, Dasgupta’s austerity underscores the need to eschew luxury-driven debt cycles, prioritizing moral economics that serve the poorest (“daridranarayan”) over endless accumulation.

This financialization extends beyond national borders, finding its institutional enablers in global bodies like the World Bank, as Eric Toussaint meticulously dissects in The World Bank: A Never-Ending Coup d’État. Toussaint traces the Bank’s origins to 1944, portraying it as an enduring mechanism of imperialist control dominated by the United States and its allies, designed not for equitable development but to perpetuate dependency through debt. He details how the Bank systematically transferred colonial-era debts from European powers—such as Belgium, Britain, and France—to newly independent nations in Africa and Asia, saddling them with obligations that ensured ongoing economic subjugation. This “never-ending coup” manifests in structural adjustment programs (SAPs) that impose austerity, privatization, and market liberalization as conditions for loans, effectively overriding national sovereignty and deepening precarity in the Global South. In India’s case, the 1991 balance-of-payments crisis prompted SAPs backed by the World Bank and IMF, involving rupee devaluation, trade liberalization, subsidy cuts, and deregulation—reforms that accelerated financialization by shifting public provisioning to private credit markets, thereby inflating household debt as wages stagnated and social safety nets eroded. Toussaint argues these interventions are not neutral economic tools but deliberate strategies to maintain hegemonic power, turning debt into a perpetual instrument of control that echoes colonial exploitation in neoliberal guise.

Zooming inward to the subjective terrain, Maurizio Lazzarato’s The Making of the Indebted Man offers a penetrating analysis of how this macro-level debt regime fabricates the very ontology of the modern subject. Drawing on Nietzsche’s genealogy of morality and Deleuze and Guattari’s theories of power, Lazzarato posits debt as the “archetype of social relations” in neoliberalism, a governance technique that supplants traditional discipline with self-imposed exploitation. The “indebted man” emerges not through coercion but internalization: individuals are compelled to entrepreneurialize their lives—constantly investing in human capital, managing risks, and servicing debts—to survive in a world where credit substitutes for welfare and wage growth. This process forecloses the future by neutralizing its inherent uncertainty, transforming time itself into a commodified resource pledged to creditors and preempting collective alternatives to capitalist precarity. In contemporary India, where microfinance and consumer loans proliferate amid uneven development, Lazzarato’s framework reveals how debt engenders a moral economy of guilt and responsibility, binding subjects to endless cycles of repayment that reinforce class hierarchies and stifle resistance. Together, Toussaint and Lazzarato diagnose a seamless web of entanglement—from imperial institutions to internalized subjection—urging a radical unmaking of the indebted condition as the path to true freedom.

The philosophy of nisargaśṛṅgāra (human-nature creative intimacy based on reciprocal, non-hostile, non-antagonistic, non-hierarchical connections) offers a simple yet profound guide to living in harmony with nature. Its ethics can be captured in two sayings:

I. Nisargarnam hi kevalam — “Only the debt to nature is primal.”

Everything else—money, social rules, or human obligations—is artificial. True well-being comes not from chasing endless growth or taking on more debt, but from living with sufficiency, respecting our deep dependence on the natural world by re-paying, in non-money-signifier terms, our growing debts to the natural world.

II. Ghṛtaṁ nisargasārameti grāhyam — “Accept only the essence of nature’s bounty.”

This is not primitivism. Rather, it is careful discernment: taking only what we truly need from nature, maximizing nourishment while minimizing extraction. It aligns with the idea of living within ecological limits while ensuring socio-ecologically metabolized/alchemized well-being.

Together, these principles guide a life of simplicity, balance, and ecological mindfulness, showing that respecting nature is the foundation of ethical and meaningful living.

Rabindranath Tagore articulated the eco-(w)holistic idea of what could be presently termed as “nisargaṛṇa”—an “eco-debt” that highlights our moral and reciprocal obligations to nature. Unlike human-made debts or legal obligations, this is a debt grounded in a covenant between humans and the natural world. It calls for selfless, compassionate offerings to all elements of nature, free from ego or exploitation, responding to nature’s generous gift, or “thou-bestowal.”

This is expressed through symbolic renunciation—echoing the ancient idea of bhūta-ṛṇa or bhūta-yajña—which emphasizes honoring all beings and forces of nature, not through ritualistic violence, but through mindful ecological action. In modern terms, it aligns with concepts of ecological entitlements and recognition of nature’s intrinsic rights, acknowledging its limits and scales.

By framing our responsibilities as a human-nature agreement, nisargaṛṇa moves beyond market-driven mechanisms such as carbon credits, ecosystem services, or cap-and-trade schemes. Instead, it fosters a deeper sensibility: avoiding the relentless depletion (debit) of natural resources, while actively contributing (credit) through wisdom, care, and creative engagement of heads, hands, and hearts. In essence, it envisions a life in which human flourishing is inseparable from the flourishing of the natural world—a practical ethics rooted in attentiveness, sufficiency, and reciprocal stewardship.

Together, these principles reframe prosperity as autonomy without excess, a direct repudiation of debt-fuelled growth as destiny.

7.1. Why GDP Must Be Replaced, Not Repaired

The United Nations System of National Accounts (SNA), forged in the aftermath of World War II, enshrined GDP as the sovereign metric of economic life. What was once a wartime planning tool has since hardened into a performative oracle—summoning “growth” through monetized circulation while rendering depletion, displacement, and exhaustion invisible.

Karl Polanyi’s warning against disembedded markets finds its fullest realization here: GDP severs economy from society and ecology, converting land, labor, and money into fictitious commodities. Feminist economists such as Marilyn Waring and Silvia Federici have further shown that this severance is deeply gendered and racialized, systematically erasing unpaid care, subsistence work, and community labor—the very substrates of social survival.

In India, the consequences are stark. A nominal GDP of approximately $4.19 trillion (2025) coexists with:

- Extreme wealth concentration, with the top 1% controlling over 40% of national wealth;

- Endemic informality, where nearly 80% of workers remain outside formal protections;

- Chronic underinvestment in health (~2.6% of GDP) and education (~3.6%), despite demographic pressures;

- Severe ecological stress, including groundwater depletion, air toxicity, and biodiversity loss.

GDP registers forest clearance, debt-financed infrastructure, and speculative finance as progress, while shadow work—worth an estimated 30–40% of GDP-equivalent—vanishes from the ledger. This is not oversight but ontological violence: a system that prices the priceless and normalizes what Toussaint terms the “suction pump” of odious debt, transferring today’s gains into tomorrow’s liabilities.

Repairing GDP cannot correct this logic. Replacement is necessary.

7.2. The Architecture of the Common Good Balance Sheet (CGBS)

The Economy for the Common Good (ECG), founded in 2010 by Austrian activist and author Christian Felber, proposes a post-capitalist alternative rooted in constitutional values: human dignity, solidarity and social justice, ecological sustainability, transparency, and democratic co-determination. In works like Change Everything, Felber critiques financialized growth, advocating measurement of success by contributions to human flourishing and planetary boundaries rather than GDP or profit. As of 2025, the movement—now 15 years old—includes over 11,000 supporters, 5,000 active members in 170+ regional groups, 1,400+ organizations with Common Good Balance Sheets, nearly 50 municipalities, and 200 universities across 35 countries.

Its flagship tool, the Common Good Balance Sheet (CGBS)—based on the Common Good Matrix (latest version 5.1)—assesses organizations across stakeholder relations (suppliers, investors, employees, customers, environment/society). Publicly auditable (peer or certified), it yields scores that unlock proposed incentives like tax breaks or procurement priority, contrasting shallow ESG reporting.

The CGBS deliberately rejects commensurability, refusing to aggregate values into one score that masks trade-offs. Instead, it evaluates along five irreducible axes:

- Human dignity — ensuring non-exploitative, respectful treatment across all interactions.

- Solidarity and social justice — promoting equity, inclusion, and reduced disparities.

- Ecological sustainability — respecting planetary boundaries and regenerative capacity.

- Transparency and democratic co-determination — fostering openness, participation, and accountability.

- Cooperation — prioritizing mutual aid over competition.

By preserving qualitative distinctness, the CGBS unmasks neoliberal monetization’s reductive violence, enabling pluriversal deliberation on sufficiency—and potentially freeing subjects from debt-fueled growth imperatives.

To extend this critique of financialized entanglement, a complementary framework reimagines macro-level accounting along five non-aggregable axes:

- Ecological Balance (Nature as Creditor)

Treats resource depletion, emissions, and biodiversity loss as intergenerational debt; irreversible harm registers as ethical injustice. - Social Reproduction Balance

Centers care work, health, and gendered labor; growth eroding reproductive conditions counts as social deficit. - Democratic and Ownership Structure

Assesses concentration and regulatory capture; oligopoly signals democratic erosion, not efficiency. - Intergenerational Debt and Fiscal Burden

Evaluates public liabilities and distributive asymmetry—who gains today, who bears costs tomorrow. - Commons Integrity and Access

Measures enclosure versus stewardship of land, data, water, energy; affordability and universality as core metrics.

These axes recast accounting as ethical-political inquiry, exposing precarity’s systemic roots and charting paths beyond indebtedness toward common stewardship.

Extending this ethical-political reimagining, Helena Norberg-Hodge’s advocacy for localization emerges as a potent antidote to globalized financialization, emphasizing community-scale economies that prioritize ecological and social resilience over distant, debt-fueled supply chains. As founder of Local Futures and a pioneer in the new economy movement, Norberg-Hodge critiques how neoliberal globalization perpetuates exploitation and environmental collapse, proposing instead a “localization” strategy that rebuilds interdependent, place-based systems—fostering shorter food chains, renewable energy cooperatives, and cultural revitalization to reduce dependency on volatile global markets and imperial debt structures. This approach, highlighted in her 2019 book Local is Our Future and recent discussions on resilient communities amid globalization’s “end game,” aligns with common good principles by decentralizing power and curbing the endless growth imperative that entrenches precarity.

Complementing localization, Kate Raworth’s Doughnut Economics reframes prosperity within planetary and social boundaries, visualizing a “safe and just space” for humanity as a doughnut-shaped model: an inner ring ensuring foundational human needs (food, health, education) without falling short, and an outer ring capping ecological overshoot (climate change, biodiversity loss) to avoid excess. In her 2017 book Doughnut Economics: Seven Ways to Think Like a 21st-Century Economist, Raworth dismantles outdated growth-centric paradigms, advocating regenerative, distributive designs that echo CGBS axes—prioritizing sufficiency over surplus to liberate societies from debt-driven expansion. Adopted by cities like Amsterdam and organizations worldwide, this framework urges a shift from extractive metrics to holistic thriving, directly challenging the financialization that commodifies survival.

These ideas converge with the degrowth movement, which calls for a planned, democratic downscaling of production and consumption in affluent nations to respect ecological limits, reduce inequalities, and enhance well-being—critiquing capitalism’s growth-at-all-costs ethos as unsustainable and exploitative. Unlike green growth illusions, degrowth envisions strategies like work-time reduction, resource caps, and basic income to foster equity without environmental destruction, positioning it as a radical response to indebtedness by halting the cycle of overproduction that fuels precarity. Closely related, post-growth economics decouples well-being from GDP expansion, advocating prosperity through sufficiency, equity, and planetary health—reorganizing societies around human flourishing rather than accumulation, as articulated in works like Tim Jackson’s Post Growth: Life After Capitalism and initiatives by the Post Growth Institute. This paradigm, gaining traction in policy and academia, envisions voluntary transitions to sustainable systems, freeing communities from fiscal burdens and intergenerational debt.

Further radicalizing these alternatives, the gift economy subverts commodification by circulating goods and services through voluntary giving without expectation of immediate reciprocity, building social bonds and abundance through trust—evident in indigenous practices, subsistence communities, and modern examples like free libraries, mutual aid networks, and open-source software. Rooted in anthropological theories from Marcel Mauss onward, it fosters reciprocity over extraction, potentially dismantling debt’s moral grip by embedding exchange in relational webs rather than financial obligations. Echoing this, the moneyless society movement envisions resource allocation based on needs and collaboration, not currency—drawing from communist ideals, resource-based economies like The Venus Project, and contemporary initiatives such as Moneyless Society collectives that promote automation, abundance, and voluntary labor to transcend scarcity-driven hierarchies. Though challenging in implementation—requiring cultural shifts and technological support—these visions collectively chart a pluriversal exit from entanglement, toward economies of care, reciprocity, and true freedom.

7.2.1. Sectoral Illustrations

Telecom: Digital Expansion as Enclosure

Celebrated as a triumph of Digital India, telecom boasts mass connectivity and low data prices. Under the CGBS, however, the sector reveals deep structural deficits: oligopolistic concentration, debt-socialized bailouts, precarious labor, massive e-waste, and the enclosure of communicative space through surveillance capitalism. GDP captures usage; CGBS exposes loss of autonomy.

Renewables: The Green Growth Paradox

India’s renewable surge appears ecologically virtuous. Yet large-scale, debt-financed projects often displace communities, enclose commons, and lock public utilities into rigid payment obligations. Without decentralization and community ownership, renewables risk becoming green extractivism, not ecological justice.

7.3. From Ledger Sovereignty to Community Sovereignty

Across sectors, a pattern emerges: GDP growth frequently coincides with declining autonomy, ecological overdraft, and deferred social costs. The Common Good Balance Sheet reveals what aggregates conceal—that prosperity measured in volume often masks impoverishment measured in life-capacity.

A post-GDP political economy would therefore ask not How fast are we growing? but:

- Who is unburdened?

- Who is secure without debt?

- Whose future remains unencumbered?

In this sense, a-rni (un-debted) is not an ascetic ideal but a democratic horizon. The CGBS reclaims accounting from capital and restores it to life, reimagining the economy as a communal hearth rather than a plutocratic pyre—where sufficiency, dignity, and ecological grace define success.

8. Conclusion: Shattering the Mirage – Toward a Radical Reckoning with Debt and Domination

Conclusion: Beyond the Debt Mirage – Forging Liberation from Predatory Entanglement and Illusory Growth

India’s external debt trajectory, culminating in a staggering USD 747.2 billion by mid-2025, stands as a damning indictment of a decade-plus regime of crony capitalism under the guise of national resurgence. Far from a neutral byproduct of economic integration or developmental necessity, this debt explosion—from USD 457 billion in 2014—represents a calculated architecture of domination: a mechanism for upward redistribution that privatizes gains for a plutocratic groupings while socializing risks, burdens, and vulnerabilities onto the public, the precarious, and future generations. Compositionally volatile, with private commercial borrowings dominating nearly 39% and USD-denominated liabilities exposing the economy to external shocks, this debt is no badge of confidence but a chain of subjugation—binding sovereignty to creditor whims, enforcing fiscal austerity, and foreclosing democratic alternatives to neoliberal precarity.

This predatory dynamic intersects with the broader illusion of GDP supremacy, where India’s projected USD 4.19 trillion nominal economy in 2025—vaulting it to the world’s fourth-largest—masks profound misrepresentations and structural fractures. IMF critiques of national accounts, including outdated proxies for the unorganized sector (encompassing 45% of GDP), deflator distortions, and unaddressed production-expenditure gaps, reveal inflated growth figures that obscure stagnation in real wages, persistent unemployment (hovering at 8-10% officially, far higher informally), and gendered disparities in a services sector still reeling from pandemic shocks. Year-on-year reporting further distorts, concealing quarterly decelerations and fostering a false narrative of unbroken ascent. In truth, GDP fetishism—rooted in the post-WWII SNA framework—perpetuates Polanyian disembedding: commodifying land, labor, and nature while erasing unpaid care work (valued at 30-40% of GDP-equivalent) and ecological depletion. The result? A “growth” story where the top 1% commandeers 23% of income and 40% of wealth—colonial-era highs—amidst 220-234 million in multidimensional poverty, chronic underfunding of health (2.6% GDP) and education (3.6%), and environmental crises like groundwater exhaustion and air pollution that IMF stress tests flag as fiscal time-bombs.

At its core, this indebted condition is not mere fiscal imbalance but a constitutive feature of contemporary capitalism, as dissected by Toussaint and Lazzarato. The World Bank’s “never-ending coup” through odious debt transfers and SAPs—evident in India’s 1991 reforms—perpetuates imperial dependency, while Lazzarato’s “indebted man” internalizes exploitation as moral duty, entrepreneurializing survival in a financialized landscape where microloans and consumer credit proliferate amid wage stagnation. In India, household debt nearing 42% of GDP exemplifies this: a moral economy of guilt that reinforces hierarchies, stifles resistance, and commodifies time itself. Yet, ancient wisdom from the Mahabharata’s Yaksha Praśna counters this with an ethics of non-indebtedness—anṛṇī—where true happiness lies in freedom from entanglement, displacement, and dependence, cooking simple greens in one’s home without uprooting.

This ethical inversion demands rejecting GDP globalitarianism in favor of pluriversal alternatives that prioritize sufficiency, reciprocity, and stewardship. The Common Good Balance Sheet (CGBS), pioneered by Christian Felber’s Economy for the Common Good movement—now spanning 11,000 supporters and 1,400 organizations globally—reimagines accounting along non-commensurable axes of human dignity, solidarity, ecological sustainability, transparency, and cooperation. Extended macro-level, it exposes systemic deficits: ecological overdrafts as intergenerational injustice, eroded social reproduction through gendered care burdens, democratic hollowing via oligopolistic capture, fiscal asymmetries downloading costs to the future, and commons enclosure stripping access to essentials like water and data.

These principles resonate with Helena Norberg-Hodge’s localization, rebuilding resilient, place-based economies to dismantle debt-fueled global chains; Kate Raworth’s Doughnut Economics, bounding prosperity within social floors and ecological ceilings; degrowth’s democratic downscaling to halt overproduction and inequality; post-growth’s decoupling of well-being from accumulation; the gift economy’s reciprocal circulation fostering trust over commodification; and moneyless society’s needs-based allocation transcending scarcity hierarchies. Sectorally, they unmask illusions: telecom’s “digital triumph” as surveillance enclosure, renewables’ “green surge” as displacing extractivism. Philosophically, nisargaśṛṅgāra and Tagore’s nisargaṛṇa reframe our primal debt to nature—not as monetary obligation but reciprocal stewardship—urging acceptance of only nature’s essence while renouncing exploitative excess.

The per-capita lens sharpens the outrage: USD 510 per person, a “division-average” that belies asymmetric burdens—children, the informal workforce, and marginalized communities bearing the weight of currency mismatches, inflationary pass-throughs, and deferred crises without reaping conglomerate gains. With reserves at USD 693 billion offering illusory buffers against plausible shocks—global tightening, rupee depreciation (4-5% in 2025), or climate contingencies pushing total debt over 100% GDP—this architecture risks cascading implosion, as warned by RBI and IMF.

Shattering this mirage requires radical reckoning: not incremental tweaks but systemic rupture. Demand independent audits to repudiate odious debts tied to cronyism; impose progressive wealth taxes (targeting the USD 1 trillion billionaire hoard) and corporate levies to reclaim illicit gains; revitalize public sector banks for inclusive, developmental credit rather than bailout conduits; reinstate stringent ECB controls prioritizing national needs over unrestricted leverage; and democratize economic policy, freeing it from market discipline and oligarchic capture. Beyond reform, cultivate community sovereignty through localized cooperatives, universal basic services, and ecological regeneration—embodying anṛṇī as collective autonomy.

In essence, India’s USD 747 billion burden is a clarion call to resistance: against the predatory weave of debt, domination, and dispossession that mortgages futures to magnates. By embracing un-indebted ethics and post-growth visions, we can forge a liberated horizon—where prosperity is measured not in trillions accumulated but in entanglements dissolved, dignities affirmed, and commons stewarded. The alternative is continued subjugation under prosperity’s guise; the reckoning is not just overdue but imperative for a truly viksit—flourishing (not “developed”)—India, rooted in justice, sufficiency, and freedom.

References

Chancel, L., Piketty, T., Saez, E., & Zucman, G. (Eds.). (2026). World inequality report 2026. World Inequality Lab. https://wir2026.wid.world/

Department of Economic Affairs, Ministry of Finance, Government of India. (2025). India’s external debt: A status report 2024-25. https://dea.gov.in/files/external_debt_documents/Ex%20Debt%20Report%202024-25.pdf

Drishti IAS. (2025, October 8). Rise in India’s external debt. https://www.drishtiias.com/daily-updates/daily-news-analysis/rise-in-indias-external-debt

Drishti IAS. (2025, December 13). World inequality report 2026. https://www.drishtiias.com/daily-updates/daily-news-analysis/world-inequality-report-2026

Economy for the Common Good. (n.d.). Official website. https://www.econgood.org/

Felber, C. (2015). Change everything: Creating an economy for the common good. Zed Books. https://christian-felber.at/en/books/change-everything/

Ghosh, J. (2025, August 28). Modi’s billionaires in Trump’s crosshairs. Project Syndicate. https://www.project-syndicate.org/commentary/trump-trade-tactics-hit-modi-where-it-hurts-by-jayati-ghosh-2025-08

International Monetary Fund. (2025). India: 2025 Article IV consultation—Press release; Staff report; and statement by the Executive Director for India (IMF Country Report No. 25/314). https://www.imf.org/en/Publications/CR/Issues/2025/11/25/India-2025-Article-IV-Consultation-Press-Release-Staff-Report-and-Statement-by-the-572056

International Monetary Fund. (2025, November 21). India: 2025 Article IV consultation—Press release; Staff report. https://www.imf.org/-/media/files/publications/cr/2025/english/1indea2025003-source-pdf.pdf

International Monetary Fund. (2025, November 25). India: 2025 Article IV consultation—Press release; Staff report. https://www.imf.org/en/publications/cr/issues/2025/11/25/india-2025-article-iv-consultation-press-release-staff-report-and-statement-by-the-572056

International Monetary Fund. (2025, November 26). IMF Executive Board concludes 2025 Article IV consultation with India. https://www.imf.org/en/news/articles/2025/11/24/pr-25392-india-imf-executive-board-concludes-2025-article-iv-consultation

International Monetary Fund. (2025, December 17). India: 2025 Article IV consultation—Press release; Staff report. https://www.elibrary.imf.org/view/journals/002/2025/314/article-A004-en.pdf

Jackson, T. (2021). Post growth: Life after capitalism. Polity Press. https://timjackson.org.uk/ecological-economics/postgrowth-book/

Kumar, A. (2025, December 8). India’s real growth may be 2.5–3 per cent, not 8 per cent. Frontline. https://frontline.thehindu.com/economy/india-gdp-data-crisis-imf-growth-questions/article70365304.ece

Lakshmikumaran & Sridharan. (n.d.). External commercial borrowing (ECB) policy – RBI eases end-use restrictions. https://lakshmisri.com/newsroom/news-briefings/external-commercial-borrowing-ecb-policy-rbi-eases-end-use-restrictions/

Lazzarato, M. (2012). The making of the indebted man: An essay on the neoliberal condition (J. D. Jordan, Trans.). Semiotext(e). https://mitpress.mit.edu/9781584351153/the-making-of-the-indebted-man/

Local Futures. (n.d.). Official website. https://www.localfutures.org/

Mauss, M. (1990). The gift: The form and reason for exchange in archaic societies (W. D. Halls, Trans.). Routledge. (Original work published 1925). https://files.libcom.org/files/Mauss%20-%20The%20Gift.pdf

Ministry of Finance, Government of India. (2025). Annex 9: Debt position of the Government of India. https://www.indiabudget.gov.in/doc/rec/annex9.pdf

Moneyless Society. (n.d.). Official website. https://moneylesssociety.com/

Norberg-Hodge, H. (2019). Local is our future: Steps to an economics of happiness. Local Futures. https://www.localfutures.org/publications/local-is-our-future-book-helena-norberg-hodge/

Norton Rose Fulbright. (2025, October). External commercial borrowings in India: Key requirements and new developments. https://www.nortonrosefulbright.com/en/knowledge/publications/53bc5c70/external-commercial-borrowings-in-india-key-requirements-and-new-developments

Polanyi, K. (2001). The great transformation: The political and economic origins of our time (2nd ed.). Beacon Press. (Original work published 1944). https://www.beacon.org/The-Great-Transformation-P2237.aspx

Post Growth Institute. (n.d.). Official website. https://postgrowth.org/

Press Trust of India. (2025, September 30). India’s external debt rises to USD 747.2 bn at Jun-end: RBI data. https://www.ptinews.com/story/business/india-s-external-debt-rises-to-usd-747-2-bn-at-jun-end-rbi-data/2964328

Raworth, K. (2017). Doughnut economics: Seven ways to think like a 21st-century economist. Chelsea Green Publishing. https://www.chelseagreen.com/product/doughnut-economics-paperback/

Reserve Bank of India. (2013, July 1). Master circular no. 11/2013-14: External commercial borrowings and trade credits. https://www.rbi.org.in/commonman/Upload/English/Notification/PDFs/08MCNF29062013.pdf

Reserve Bank of India. (2014, July 1). Master circular no. 11/2014-15: External commercial borrowings and trade credits. https://www.rbi.org.in/commonman/Upload/English/Notification/PDFs/02MDI010714FL.pdf

Reserve Bank of India. (2014, July 1). Master circular no. 12/2014-15: External commercial borrowings and trade credits. https://bcasonline.org/Referencer2016-17/Other%20Laws/Circulars/master%20circular%2014-15/Master%20Circular%20on%20External%20Commercial%20Borrowings%20and%20Trade%20Credits%201.7.2014.pdf

Reserve Bank of India. (2016, January 1). RBI/FED master direction no. 17/2016-17 (Updated Jan 2022). https://ifsca.gov.in/Document/Legal/12mdfb8ad1b34bcb4d0a8f6869da4a53082e29042022035520.PDF

Reserve Bank of India. (2025, September 30). India’s external debt as at end-June 2025 [Press release]. https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx

Schumacher, E. F. (1973). Small is beautiful: Economics as if people mattered. Harper & Row. https://www.harpercollins.com/products/small-is-beautiful-e-f-schumacher

Shankar IAS Parliament. (2025, December 13). World inequality report, 2026. https://www.shankariasparliament.com/current-affairs/gs-ii/world-inequality-report-2026

Sitharaman, N. (2025, December 4). IMF did not question GDP growth figures. The Economic Times. https://m.economictimes.com/news/economy/indicators/imf-did-not-question-gdp-growth-figures-nirmala-sitharaman-on-lower-grade-on-national-accounts/articleshow/125769636.cms

Tagore, R. (1913). Sadhana: The realization of life. Macmillan. https://www.gutenberg.org/files/4028/4028-h/4028-h.htm

Thapar, K. (2025, November 29). IMF concerns justified – India’s GDP calculation less than reliable [Video]. YouTube. https://www.youtube.com/watch?v=ttReZu7LHJ4

The Tribune India. (2025, September 30). India’s external debt rises to USD 747.2 billion at end-June 2025: RBI. https://www.tribuneindia.com/news/business/indias-external-debt-rises-to-usd-747-2-billion-at-end-june-2025-rbi/

The Wire. (2025, December 2). Full text | How reliable is India’s GDP calculation? https://m.thewire.in/article/economy/full-text-imf-concerns-justified-indias-gdp-calculation-less-than-reliable-arun-kumar-and-pronab-sen

The Wire. (2025, December 9). Inequality in India among highest in the world, top 1% holds 40% wealth: Study. https://m.thewire.in/article/political-economy/in-charts-world-inequality-report-2026

Toussaint, E. (2007). The World Bank: A never-ending coup d’état. The hidden agenda of the Washington Consensus. Vikas Adhyayan Kendra. https://www.cadtm.org/The-World-Bank-a-never-ending-coup-d-etat

United Nations. (2025). System of national accounts 2025. United Nations Statistics Division. https://unstats.un.org/unsd/nationalaccount/snaupdate/2025/2025_SNA_Combined.pdf

United Nations Population Division. (2025). World population prospects 2025: India population estimate. United Nations. https://population.un.org/wpp/

Vyasa. (n.d.). Mahabharata (K. M. Ganguli, Trans.). (Book 3: Aranya Parva, Section 311: Yaksha Prashna). Sacred Texts. https://sacred-texts.com/hin/m03/m03311.htm

Waring, M. (1988). If women counted: A new feminist economics. Harper & Row. https://www.marilynwaring.com/publications/if-women-counted.asp

World Bank. (2025). International debt report 2025. https://www.worldbank.org/en/programs/debt-statistics/idr/products

World Bank Group. (2025, December). International debt report 2025. https://thedocs.worldbank.org/en/doc/6e72b0ded996306fa01f5db7a0c38b19-0050052021/related/IDR2025-App.pdf

World Inequality Lab. (n.d.). Home. https://inequalitylab.world/en/

5 Comments