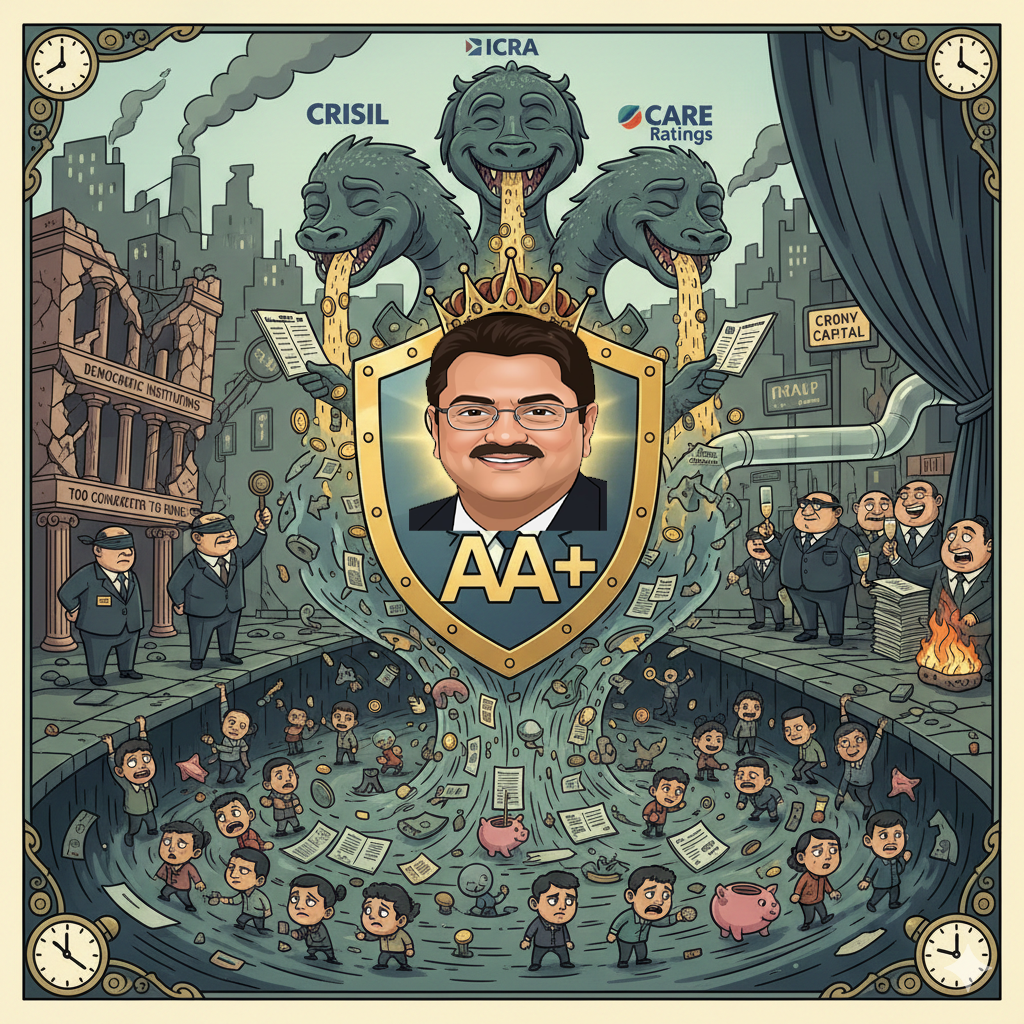

In India’s deeply captured financial regime under prolonged BJP-NDA rule (2014–2025), credit rating agencies (CRAs)—dominated by the CRISIL-ICRA-CARE triopoly—have degenerated from purported risk sentinels into systemic enablers of crony expropriation, perpetuating a predatory cycle of manufactured trust, retail mobilization, delayed collapse, and elite consolidation. The Piramal Finance–DHFL saga stands as the paradigmatic indictment: investment-grade ratings (AA to AAA) were stubbornly retained despite whistleblower alerts, Cobrapost exposés, and KPMG audits exposing ~₹29,000–34,000 crore in promoter diversions through shells and evergreening, facilitating continued borrowing until 2019 defaults; post-crisis, Piramal—bolstered by dynastic kinship to Mukesh Ambani (via his son’s marriage to Isha Ambani) and alleged political shielding through disproportionate ruling-party contributions—secured DHFL via a sweetheart IBC resolution that controversially valued ~₹45,000 crore in fraud/avoidance recoveries at a nominal Re 1, acquiring the ~₹90,000+ crore portfolio for ~₹37,250 crore while the Supreme Court’s April 1, 2025, ruling vested all future windfalls exclusively in the bidder and condemned ~2.5 lakh retail depositors (mostly middle-class and elderly savers) to brutal 55–77% haircuts, aggregating colossal losses exceeding ₹50,000 crore across similar NBFC failures. Swiftly rebranded as Piramal Finance through reverse merger alchemy, the entity achieved rapid rehabilitation—~₹91,447 crore AUM with over 80% retail pivot, PAT doubling to ~₹327 crore in Q2 FY26, and fortified net worth ~₹27,000 crore—crowned by CRISIL’s fresh AA+/Stable assignment in January 2026 (with A1+ short-term), shaving funding costs by 50–80 bps and unlocking diversified inflows, even as Moody’s Ba3/Stable alone cautioned lingering wholesale exposures (~14%) and volatility. Driven by issuer-pays conflicts, oligopolistic convergence, epistemic blindness to governance rot and political proximity, and implicit “too connected to fail” pricing, CRAs orchestrate performative legitimacy—inflating optics pre-crisis, reacting belatedly post-default (as in IL&FS’s AAA-to-junk plunge and Yes Bank’s pre-moratorium investment-grade persistence), and aggressively upgrading post-consolidation—thereby externalizing ruin onto vulnerable constituencies while privatizing distressed assets for networked oligarchs within a broader architecture of institutional capture, democratic erosion, and cunning capitalism that demands radical rupture: abolishing issuer-pays, imposing personal liability, deconcentrating markets, and centering retail justice to reclaim accountability from this reverse merger republic.